* enjoy the

convenience of their

Revolving Line/s of Credit

(often not paying for Purchases for up to 55 days

after receipt of goods and services); and

* Noted that

".....

In addition, many credit card

holders take advantage of interest-free periods such that they do not

pay interest on their card balances

" identified by the RBA as

Transactors.

"The

Payment Systems (Regulation) Act 1998 also gives the RBA

extensive powers

"....to

gather information from payment system participants and operators."

* the Reserve Bank has

significantly greater powers/responsibilities to "...the economic prosperity

and welfare of the people of Australia",

than the Bank of England

or the

U.S. Federal Reserve has

to the economic prosperity and welfare

of the U.K. and U.S. citizens respectively.

* (2) It is the

duty of the Reserve Bank Board, within the limits of its powers, to ensure that

the monetary and banking policy of

the Bank is directed to the greatest

advantage of the people of Australia and that the powers of the Bank under

this Act and any other Act, other than the Payment Systems (Regulation)

Act 1998, the Payment Systems and Netting Act

1998and Part 7.3 of the

Corporations Act 2001,

are exercised in such a manner as, in the opinion of the Reserve Bank Board,

will best contribute to:

(a) the

stability of the currency of Australia;

(b) the

maintenance of full employment in Australia; and

(c)

the

economic prosperity and welfare of the people of Australia.

* RBA's key areas of focus included

capacity for richer information with payments.

* "On current scheduling the New

Payments Platform will deliver a fast payments service

with rich information

and addressing capabilities in the second half of 2017.

"Before 1981, activities of major Australian

banks, including the manner they dealt with

customers, were

subject to detailed regulations imposed by the Federal Government. Following the 1981

Campbell

Committee Report, banking regulations were significantly reduced."

* Request

to the Reserve

Bank of Australia, hereinafter the RBA, to

implement the same

"competitiveness and efficiency"

that it has overseen in the 'wholesale supply side' of the debit and credit cards products to the

Retail Supply Side of

credit cards, because banks profits from credit cards are not derived

from the User Pays Principle

*

All users should pay the cost of their credit card

transactions, and not some "unlucky" users paying a disproportionate burden

which has further gapped the "Haves" from the "Have Nots"

A) "gather

information from payment system participants and operators"

by proceeding to obtain datafor a

particular month (or quarter)

from over 70 issuers

for the

330 different

types of cards that are available which shows:

1. Number of cards

that repaid total indebtedness and aggregate dollar amount of those

repayments.

2. Number of cards

that repaid > or =50% of total indebtedness and aggregate dollar amount of those

> or = 50% repayments.

3. Number of cards

that repaid<50% but >5% of total indebtedness and aggregate dollar amount of

those <50% but >5% repayments.

4. Number of cards

that repaid <=5% of total indebtedness and aggregate dollar amount of those <=5%

repayments;

10. In order to test the

Writer'scalculations listed at

(A), (B) and (C) in this 1st Question, it would be necessary for the Royal

Commission to request Australia's largest six or seven

Credit Card Issuers,

that included Citibank and Latitude Financial,

to provide Credit Card data over at

least 12 months that lists the -

Next, I would like to

discuss data and transparency.

We welcome the

Commission’s strong focus on data and harnessing new technologies to

facilitate consumer understanding.

ASIC, like the

Productivity Commission, supports the proposed open banking regime. With

appropriate regulatory settings, increasing consumers’ access to their

own data has the potential to empower decision making and stimulate

competition and innovation within the financial services sector.

The Commission

has made a number of other specific recommendations on data."

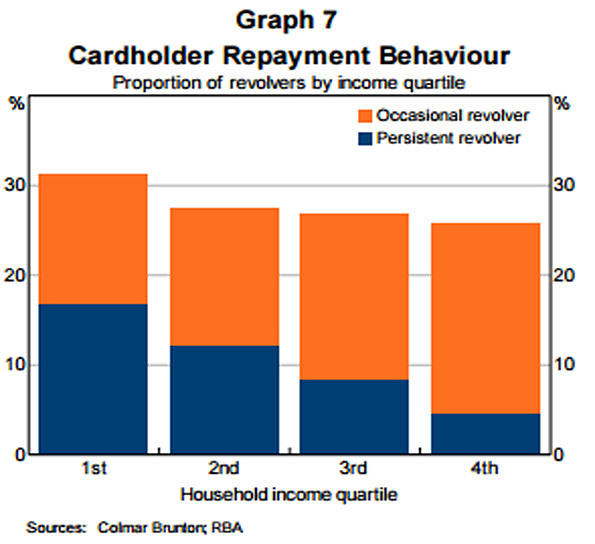

Data from the household, income and

labour dynamics survey in Australia (HILDA), the household expenditure survey

and the survey of housing and income shows households in the lowest income

quintile have more credit card debt relative to their incomes and pay more in

credit card interest relative to their incomes than higher income households,

though overall differences in interest payments between quintiles are small

(Figure 1).1

These surveys also show households in

the bottom two quintiles by net worth also pay the most in credit card interest

relative to their income (Figure 2).

(A.)

LOAN

RATE STICKINESS: THEORY AND EVIDENCE - RBA 1992 (by

Philip Lowe and Thomas Rohling) informed that the

Reserve Bank regulated lending interest rates until

1985 and post-deregulation lending interest rates,

in particular Credit Card interest rates, did not

fall in line with the

Overnight Cash Rate, and when falls were

passed on, it wasn't done quickly or completely,

whereas when the Overnight Cash Rate increased, these

increases were passed on by way of higher lending

interest rate and more quickly. Hence, Credit

Card interest rates were particularly

stickywhentheOvernight Cash Ratefell, as

Credit Card interest rates regularly remained 'stuck'

at their existing interest rate.

"From 1966, when personal loans were introduced, the maximum rate

that banks could charge was set by the Reserve Bank. Once again, in

April 1985, the controls were removed.

At the same time, the maximum interest rate that could be charged on credit cards was

deregulated. Prior to this time the maximum rate had been set at 18 per cent per

annum.

As detailed above, most lending rate ceilings were lifted in

April 1985.

For the housing, credit cards and personal

loan rates, the ranking in terms of the degree of stickiness is maintained.

Even after nine lags are included the sum of the coefficients on all three

of these rates remain significantly less than one. The same is true for

the standard overdraft rate.

In contrast,

the rates on personal loans and credit cards do not appear to be

more flexible in the deregulated period."

4.

36 years ago when the

Campbell Committee

recommendations were being implemented, the prospect of a

Royal Commission

into

ostensibly

Unconscionable

Conduct within the

'financial services sector'

would have been

viewed as implausible to

those Australians that lived through the lengthy regulated interest rate epoch

in Australia's financial history, because

-

(i)

the Reserve Bank

and its predecessor the then Govt. owned, Commonwealth Bank, had increasingly

regulated 'with an iron fist in a velvet glove'

the commercial banks since 1911 as chronicled in Chapter 17;

and

(ii) historically when de-regulation

resulted in adverse consequences, re-regulation

by Australia's 'central bank' ensued.

Between 1960 and

1980 the Reserve Bank diligently regulated commercial Australian bank interest

rates relying on, inter alia, Section 50

of the

Banking Act 1959.

5.

Chapter 5

mathematical calculates/quantifies the circa financial burden upon

Revolvers and includes

the following:

Below is an extract fromConsumer Affairs Victoria

- Regulating the cost of creditwhich evidences that in

the past if de-regulation did not achieve the desired results, then re-regulation

followed. But not with regard to re-introducing a max interest rate cap on

Credit Cards, notwithstanding

that -

"The tide of utilitarianism rose

slowly, and a lengthy campaign was necessary before the financial

deregulation of 1854, which abolished the British interest rate cap.

However, one act of deregulation cannot quell an argument that has been going on for millennia. Over the following century the tide gradually turned towards re-regulation, culminating with detailed requirements imposed on the financial sector (particularly the banks) during and immediately after the Second World War.

We now trace the

gradual lead-up to this second phase of regulation."

"Obviously this is a pretty radical

act, and it will be fought," he replied. "But I think the American people

are disgusted with the financial industry. They want change.

You could argue that an interest rate of 15% or 18% is more than enough to

accommodate any amount of risk on the lender's part.

If a loan appears

riskier than that, don't make it. What we have to ask as a nation is

whether it's ethical to charge people 30% interest rates," Sanders said.

"This is loan sharking. Let's call it what it is."

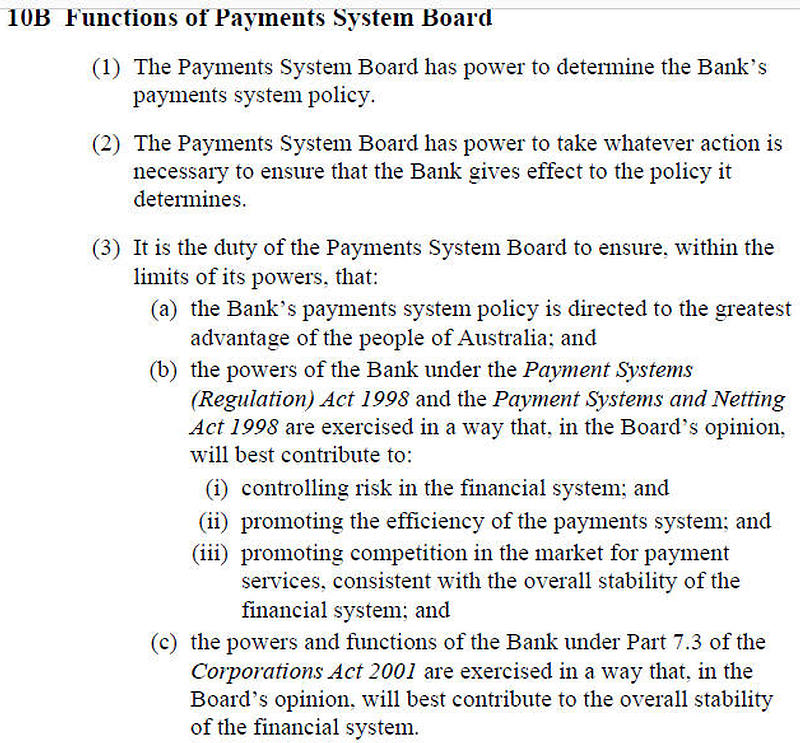

"determine rules for participation in a payment

system and set Standards for safety and efficiency, incl. issues such as

performance benchmarks"

by proceeding to implement

"cost-based benchmarks"

[akin to (I.), (II.) and (III.)

in Section 2 [of this letter to the RBA] by -

(a) setting

a regulatory cap for all

the

330 different types of cards which fall under the jurisdiction of the

RBA of -

i) 850 basis

points above the RBA official interest rateas the maximum annual on-going

interest rate charged by Credit Card Issuers in Australia for Purchases, where Credit Card Issuers can reach, but not exceed, this Purchase Interest Rate Cap;

ii) 950 basis points above the RBA official interest rate as the maximum

annual on-going interest rate charged by Credit Card Issuers in Australia for

Cash Advances, where Credit Card Issuers can reach, but not exceed, this Cash Advance Interest Rate Cap - refer

50% cap on Cash Advances in D) below;"

*

iterate the reasons why our primary financial services regulator, Australia's 'central

bank' regulated

interest rates 'with

an iron fist in a velvet glove'

over Australia's commercial banks until Campbell; and

"Looking back in time, Australian banks collapsed in almost every

decade of the 19th century. In 1893 after the failure of

fraudulent land banks in Victoria triggered a wholesale run on

banks. In the space of six weeks, 12 banks closed their doors. Those

banks accounted for two-thirds of the total banking assets in

Australia.

That crisis increased pressure - which had been building for some

time - for the formation of a central bank. The Commonwealth Bank

was formed by the Federal Government in 1911 to issue notes which

would be backed by the resources of the nation.

Banking became more tightly controlled during World War II, with the

central bank dictating overdraft rates and, later, statutory reserve

deposit ratios and liquid asset ratios.

To avoid a patent conflict of interest, the Commonwealth Bank's

'central banking powers' were transferred to the newly formed

Reserve Bank of Australia in 1959."

The below four quotes from "Overview

of Financial Services Post-Deregulation"by (Dr) Diana

Beal, Director, Centre for Australian Financial Institutions, University of

Southern Queensland,

evidence that the Reserve Bank

rigorously regulated bank deposit rates until 1980 when restrictions on interest rates

were dismantled after adopting Campbell Committee recommendations:

"Interest-rate

ceilings on deposit accounts restricted the banks’ ability to attract funds

particularly during the 1970s when inflation was rampant. In the June

quarter of 1975, inflation rose to 16.9% pa. At the same time, interest

payable on amounts held in savings accounts offered by savings banks, for

example, was restricted to 3.75% from 1969 to 1980 (Foster, 1996). In contrast, the

interest rates offered by non-bank financial institutions (NBFIs) were not

controlled and they were able to pay around 10% on passbook accounts."

"Banks in 1980 still operated in a highly regulated environment which was an

artefact of previous economic and social conditions. Indeed, an extensive

collection of controls remained from regulation introduced under the

National Security Regulations in 1941."

"Interest rate ceilings on trading bank and savings bank deposits were

dismantled from 1980; some limits on minimum and maximum terms on fixed

deposits remained."

"The maximum interest rate payable on small

balances in savings accounts was fixed by regulation at 3.75% from 1969

to 1980."

8

.

Below is a quotation from Westpac's submission to the

Wallis

Inquiry

1997

by the then CEO, Bob Joss:

Writer's investigations suggest that the

Wallis Inquiry

1997 did not adopt

Westpac's prudent recommendation for on-going monitoring of any changes in

interest rates in either its

Discussion Paper- Released Nov 1996

or Final Report- Released March 1997.

"Regulation of all markets for goods and services can be

categorised according to three broad purposes.

First, regulation is to help

ensure that markets work efficiently and

competitively, and thus to overcome

sources of market failure.

Second, regulation can prescribe particular

standards or qualities of service, especially where the consumption of goods

and services carries risks, so that safety is a focus of concern.

Third, regulation can

help achieve social objectives such as, for example, 'community service obligations' which typically take the form of price controls."

11.

The U.S. has set the precedent. The interest rate charged for the

majority of Credit Cards issued in the USA is based on an agreed margin above

the U.S.

Prime Rate.

Many credit cards base their

variable interest rates on the

prime rate. A variable interest rate is one that changes based

on another interest rate.

For example, the APR on a credit card might be the prime rate plus

13%. The interest rate your credit card issuer charges on top of the

prime rate is known as the "spread." In our example, the

"spread" is 13%. If the prime rate is 3.25%, the current APR on that

variable rate card would be 16.25%. That means the prime rate has a

direct, but typically small, impact on the

finance charges you pay on your

credit card when you carry a balance. The higher the prime rate, the

more you'll pay to revolve a credit card balance. You can avoid

paying any interest at all by paying your credit card balance in

full each month.

If your credit card has a variable interest rate based on the prime

rate, your credit card interest rate will follow the movement of

the prime rate.

If the prime rate goes up, you can expect your credit card interest

rate will soon go up. On the other hand, if the prime rate goes

down, your credit card interest rate should go down.

Credit card issuers don’t have to give advance notice of interest

rate changes if you have a variable interest rate.

"The aim should be to reduce bank profits

to one per cent or less as a share of GDP, the level they were at two decades ago.

Other policy changes that would contribute to this aim include:

•

legislating to ensure

that interest rates charged by banks move in line with changes to the RBA cash rate and are set and advertised as

a mark-up over the cash rate

• restricting the

interest rates that can be charged on unsecured credit to levels that reflect the underlying risk to the lender.

⎕ Section 5 explains how

real people, rather than the consumers of economic theory, make financial decisions, and

how banks exploit human nature in their approaches to marketing.

The paper concludes that the

high degree of concentration in the

banking market and the huge profits it generates are inevitable in a

deregulated banking system such as Australia’s. With consumers powerless to change

corporate behaviour and new entrants unable to compete on a level playing field, the

big four banks are relatively free to gouge as much money from the Australian

economy as they are able. Better regulation in banking is urgently needed."

"Reform of credit card

schemes will also have a direct impact on credit cardholders and is likely to

result in some re-pricing of credit card payment services. However, this

is the means by which the price mechanism is to be given greater rein in the credit

card market. A movement towards a “user pays” approach to credit card

payment services would be consistent with the approach adopted by Australian

financial

institutions in pricing other payment instruments under their control. As the ABA itself has

confirmed: “Pricing services efficiently provides consumers with choice to use lower cost

distribution channels and, therefore, facilitates a more efficient financial

system. It is also fairer and efficient, because consumers only pay for what they use.”

* Point 5 under Supporting Evidence

re 1st Question;

and

* Point 7 under Supporting Evidence

re 3rd

Question (shortly below).

5.

Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001evidences that Reserve

Bank

advocated (on page 116) a

movement

".....towards a

'user pays' approach to credit

card payment services

would be consistent with the approach adopted by Australian financial institutions in pricing

other payment instruments under their control”which

never crystallised perhaps because the Four Pillars exerted

pressure as evident in the below extract from

Son of Campbell ... byGlenda Korporaal,

The Australian,

Hockey vividly remembers one day in the early 1990s

when he was a junior adviser to then NSW finance minister George Souris. The

minister received a visit from the chiefs of the big four banks, who were

opposed to plans to introduce a financial institutions duty. "The four chief

executives came in to bully," Hockey says. "There was Bob Joss [Westpac],

Don Argus [National Australia Bank], David Murray [Commonwealth Bank] and

Don Mercer [ANZ]. They came in - just the four of them - to belt up this

minister. I was his adviser. There were only six of us in the

room.

"I well remember their attitude and I thought to

myself: Well, it is good to provide the respect, but it is also the case

that they are in it for themselves and their banks - as they should be. But

I am in it for the community."

"B) determine rules for participation in a payment

system and set Standards for safety and efficiency, incl. issues such as

performance benchmarks"

by proceeding to implement

"cost-based benchmarks"

[akin to (I.), (II.) and (III.)

in Section 2 [of this letter to the RBA] by -

(a)

iii) $90 for the

maximum Annual Credit Card Fee that a Credit Card Issuer can charge

(in 1993 restrictions on annual fees for credit

cards were removed, so it is not unreasonable to introduce a cap,

particularly as some cards charge inordinately high annual fees to provide

'inter alia' high loyalty points which surprisingly avoid income and FBT

taxes. Why should a Credit Cardholder be entitled to claim as a tax

deduction an annual fee of $395 to then earn 3 points for every dollar spent

and not pay income tax on that earning?)

(b)

learning from point 1. of CBA's research in Section 4, set an 'Access Regime'

that each credit card issued in Australia to a person who has

not previously owned a credit card be a Provisional Charge Card,

hereinafter PCC, with a conservative credit limit where the owner of the

PCC is required for the initial 12 months to repay the

outstanding balance on the PCC in full by the due date (9 days from the Issue

Date and 7 days from the normal receipt date for postal delivery) or be subject to severe late fees and restrictions on future

PCC use,

with

deferment of receiving a traditional Credit Card until the PCC owner complies with the PCC

repayment obligations for 12 months without breach.

C) reduce the non-interest period from 'up to 55 days' to 'up to 42 days' to reduce the cost burden on

Credit Card Issuers

because electronic payments enable Credit Card Users to pay their monthly

repayments within a few days of notification of the final monthly balance.

D) continue to sanction the market practice of not providing a non interest period

for Cash Advances, but restrict the limit for Cash Advances to 50% of the

total credit limit because as Wikipedia explains - * "a

credit card is a small plastic card issued to users

as

a system of payment"; and

* the original cards

"required

the entire bill to be paid with each statement".

E) increase the

minimum repayment required from 2.5% to 25% of the outstanding debit balance

which shouldn't faze over >60% of credit card owners and will materially reduce the

interest burden on the remaining <40%.

F) allow Credit Card Issuers to levy -

a) an explicit 'Lost Card Fee' for -

* placing a stop on an account; and/or

* issuing a replacement credit card(s) commensurate with the cost to the Credit Card Issuers of

issuing a replacement credit card(s); and

b) a 'Fraud Provision Fee' upon each

credit card user each month based on the quantum of transactions and the

outstanding undrawn indebtedness (eg. for a credit card user with a $5,000

credit limit, who made 10 purchases in a month, with an outstanding undrawn

balance of $3,000 (vulnerable to fraudulent access) the 'Fraud Provision Fee'

for that month would be say 10 @ 0.15c = $1.50 + say $3,000 @ 0.0003c = $0.90 for a total monthly

'Fraud Provision Fee' of $2.40 for enjoying the convenience of using a

credit card

for 10 transactions with a $5,000 credit limit.

G) establish a

uniform credit evaluation methodology that all Credit Card Issuers must

observe similar to NAB's Microenterprise Loans because to many Australian adults are obtaining credit cards

with excessive interest rates which would be lower if the defaults were lower

due to a robust standard credit analysis methodology.

H) prosecute the

case on behalf of the "unlucky" Australians with

Baycorp Advantage'et al'and the Credit Card Issuers to establish and

regulate protocols and systems so"unlucky" Australianscannot obtain

between 6 and 10 credit cards, as evidenced by Tony Devlin, Head

Financial Counsellor,

Salvation Army's Moneycare service, in Section 4 above."

* Chapter Five: 'Philosophy of Financial Regulation'

"Third, regulation can help achieve social

objectives such as, for example, 'community service obligations' which

typically

take the form of price controls."

* Chapter Nine: 'Stability and Payments'

"There is scope for increased competition in the payments system which will help

to lower its costs of operation. However, this must be balanced against

the need to maintain stability in the financial system. The payments system provides one central

way in which instability can be generated. The RBA should retain overall

responsibility for the stability of the financial system, the provision of

emergency liquidity assistance and for regulating the payments system."

* Chapter Eleven: Promoting Increased Efficiency

"Cross-subsidies are derived from

historical product bundling [evident in (a) to (g) of

Chapter 3 above], earlier

difficulties with apportioning costs, and community expectations that

institutions should meet community service obligations. The unwinding of

such cross-subsidies can increase efficiency in the financial system."

9.

Reserve Bank webpage

Credit Cards Regulatory Decisionsevidences that the Reserve Bank, the

legislative appointed protector

of Credit

Cardholders, did naught for theRetail Supply Sideprior to March 2014.

Will the Royal Commission

recommend that the Governor of the Reserve Bank

draw upon its

existing powers to replace the debt 'lure' of anInterest Free Periodwith

a

-

Former Qld Premier, and

now Australian Bankers Association chief executive, Anna

Bligh, has been chartered with lifting the credibility of 'inter alia'

Credit Card Issuers,

after her predecessors, David Bell and the long running, Steven

Münchenberg, facilitated bank greed involving Unconscionable Conduct.

(A). informs that

the current CEO of the ABA, Anna Bligh, announced in late Dec 2017 that the ABA

had just lodged a 'Banking Code of Practice' with the Australian Securities and

Investments Commission (ASIC) for approval; and

(B). lists several changes that will be legally binding on all 'member banks' of the

ABA which includes:

"Customers only paying interest on what remains on a credit card and not the full

amount of purchase if a loan is being paid down."

Hence, the ABA has ruled it mandatory that its members desist

(A) above. The Writer has validated that St. George Bank has so ceased

this practice because the St. George Credit Cardholder referred to in

Example 1of

Labyrinth of ‘Concealed Spiders’checked with St.

George Bank.

When

Dr. Edey was questioned before the

Senate Economics Legislation Committee

regarding a dearth of competition in Credit Card interest rates when the

Overnight Cash Rate is at an

all-time low of 1.5%, Dr. Edey responded:

"...

we do not have an interest rate regulator in

Australia............... What we do have is

an ACCC that can investigate uncompetitive conduct if they see it, but they

clearly have not seen it in this market".

Will the Royal Commission ask the Governor of the Reserve Bank

why the former Assistant Commissioner, Dr. Malcolm Edey,

made the below comments

on 1 June 2015 that resiled the RBA's obligations and responsibilities to ".....promoting competition in the market for payment services,

.....", pursuant to -

How could a very senior representative of the

RBA with over 20 years experience working for the RBA not know that the RBA

shouldered all of the ACCC's obligations re ensuring competition from 23 Feb 2004? It

defies belief for Dr. Edey to have responded

"What we do have is

an ACCC that can investigate uncompetitive conduct if they see it, but they

clearly have not seen it in this market".

The above extract from an address by Dr. Malcolm Edey (RBA) contradicts the

below indented extracts fromReserve Bank of

Australia Bulletin - July 1998 - Australia’s New Financial

Regulatory Frameworkthat chronicles the Reserve Bank's powers, set out in the

Payment Systems

(Regulation) Act 1998,

that allow the Reserve Bank

to undertake more direct regulation of ‘designated’ payments systems

to "... promote

competition in the market for payments services, consistent with the overall

stability of the financial system..." when it judges it to be

"in the public interest" whichmay involve the imposition

of access rules or operating standards for participants in such systems:

"The new Payments

System Board is responsible for the Bank’s payments system policy, the

objectives of which are:

•

controlling risk in the financial system arising from the operation of the

payments system;

•

promoting the efficiency of payments systems; and

• promoting

competition in the market for payments services, consistent with the overall

stability of the financial system.

The Bank’s powers in this area, set out in the

Payment Systems

(Regulation) Act 1998,

allow it to undertake more direct regulation of ‘designated’ payments systems

when it judges it to be in the public interest. This may involve the imposition

of access rules or operating standards for participants in such systems. The Act

also provides a framework for regulation of purchased payment facilities, such

as travellers cheques and stored-value cards."

The Reserve Bank's

publicationPayment, clearing and settlement systems in

Australia - 2011 includes the following

extract that would have allowed

the RBA at any time to determine if a particular cohort of Credit Cardholders,

namely those with poor Financial Literacy Capacity, were being Unconscionably

burdened with paying the costs of Credit Card Issuers' providing

Revolving

Line/s of Credit to Transactors,

frequently -

"1.8 Dr Edey quite

rightly made the point that Australia does not

regulate interest rates, and, as such, there is no

interest rate regulator. He told

the committee that Australia does have 'an ACCC [Australian Competition and

Consumer Commission] that can investigate uncompetitive conduct if they see it,

but they clearly have not seen it in this market'.3

It

was put to Dr Edey that the issue was not so much whether there was

uncompetitive conduct in the market, but whether regulatory settings were

conducive to the promotion of sufficient competition to put downward pressure on

credit card interest rates.4

In part,

the committee's inquiry has been directed at understanding whether existing

regulatory settings in relation to credit cards are appropriate in this respect. More broadly, the committee has sought to determine what might be done to

improve competition in the credit card market or otherwise put downward pressure

on credit card interest rates."

Will the Royal Commission ask the Governor of the Reserve Bank

if he agrees with Dr. Malcolm Edey's

below responses to the

Senate 'Economics Reference Committee', because it is contrary to the findings in

LOAN RATE STICKINESS: THEORY AND EVIDENCE in June 1992

and empirical evidence in the USA, the UK and Australia over the subsequent 26 years:

"Dr Edey: Yes, the

financial system works through competition. The

basic wholesale interest rate is the cash rate,

which we set, and then competitive forces will

cause other interest rates to move up and down

with the cash rate. That is the way the effect

of policy is transmitted to the wider economy."

=================================================

Supporting Evidence re 7th Question

1.

Extracts from the Reserve Bank Research

Discussion Paper

titledLOAN

RATE STICKINESS: THEORY AND EVIDENCE - RBA 1992

(by Philip Lowe and Thomas Rohling)

dated June 1992informed that the

Reserve Bank regulated lending interest rates until

1985 and post-deregulation lending interest rates,

in particular Credit Card interest rates, did not

fall in line with the

Overnight Cash Rate, and when falls were

passed on, it wasn't done quickly or completely,

whereas when the Overnight Cash Rate increased, these

increases were passed on by way of higher lending

interest rate and quickly. Hence, Credit

Card interest rates were particularly

sticky

when the Overnight Cash Rate

fell, as

Credit Card interest rates regularly remained 'stuck'.

'Up like a rocket, down like a feather':

Credit cards and the RBA cash rate

3.6 Professor Valadkhani (Department

of Accounting, Economics and Law, Swinburne University of Technology)

provided the committee with research he had undertaken indicating that

credit passed on 112 per cent of RBA cash rate increases (the full value

of increases, plus 12 per cent), but only 53.7 per cent of rate cuts: but

cuts were delayed by an average of two-and-a-half months. Professor

Valadkhani has suggested this asymmetry is an example of the

'rockets-and-feathers' effect: credit card interest rates 'shoot up like a

rocket' in response to RBA cash rate increases, but 'float down like

feather' when the cash rate is decreased.4

This means that over time the gap

between the RBA cash rate and credit card interest rates has grown, and

consumers have been left paying higher rates of interest overall.

3.7 Professor Valadkhani took issue with the

banks tendency to downplay the relevance of the cash rate to credit card

interest rates:

"We do

not have enough information about what their funding sources are. The

argument they always make is: 'We cannot pass rate cuts on because our

sources of funding are different—it is not just the cash rate; it is our

external sources.' My argument to banks is: if that is the case, how

come, when the cash rate goes up, you immediately lift your rates? You

may have other external sources that are not related to the cash rate,

but you increase your rates anyway. When the cash rate goes down,

though, you resort to the argument of external sources.5"

3.8 CHOICE noted that despite a falling cash

rate, average credit card interest rates had gone up for both standard-rate

and low-rate cards in recent years. This was of particular concern to

CHOICE, because:

…if

you must have a credit card and you are on a low income that means you

cannot pay off your balance every month, a low-rate card is the best

option. So to see banks taking advantage of drops in interest rates to

dip their hands deeper into the pockets of low-income consumers is of

deep concern.6

Credit card

interest rates have been unresponsive to movements in the cash rate

"Despite a 2.75 percentage point decline in the cash rate since late 2011,

credit card interest rates have remained high. The rates on ‘standard’ cards are

currently around 20 per cent, while the rates on ‘low-rate’ cards are around 13

per cent (Figure 3). This has prompted concern that there is a lack of

competition in the Australian credit card market."

"We will also be clear in

the Statements of Expectations that regulators should explain in each

annual report how they have balanced competition with other elements of

their mandates."

Will the Royal Commission ask the Governor of the Reserve Bank

if he agrees the logic in Dr. Malcolm Edey's

below verbal exchange with the Acting Chair of the

Senate 'Economics Reference Committee'

on 1 June 2017, because

there is Welter Of Evidence

that -

*

some Credit Card Issuers, notably Citibank, offer Zero Balance Credit Cards (to

other bank Credit Cardholders) that consolidate (other bank)

Credit Cardholders cumulative debts; and

*

Zero Balance Credit Cards are profitable because they target other bank Credit

Cardholders with poor Financial Literacy Capacity,

Dr Edey: We often

get asked that question. I have heard that

question put a lot in relation to mortgage

interest rates, because there was a period of

time, particularly during the GFC, where

mortgage rates were not moving one for one with

the cash rate as well. The response that we have

always given to that is that the cash rate is a

still a significant driver of those rates, so it

is still having an influence. We take into

account movements in the margins between those

rates in determining what the appropriate level

of the cash rate is. In principle, the same is

true for the credit card rates. Referring back

to what I said earlier, the amount of credit

card debt and interest is much smaller than is

the case for mortgages and for business loans,

so it is not—

ACTING

CHAIR:

I can understand why from the perspective of a

bank, and the Reserve Bank's perspective, it is

smaller in terms of overall impact for the

economy. But it is fair to say that for the

people who are caught in things like debt traps

and who are caught with credit card debt—and

they may be small numbers—it is quite

significant isn't it?

Dr Edey: It is

significant for the people who are paying it.

But it is just not particularly big for the

economy as a whole.

Another thing that has been

going on over the last couple of years is that

there are interest-free cards, or low-interest

cards, that you can get by being prepared to

switch if you are on a standard credit card

rate. Increasingly, people have been doing that,

or they have been paying off their loans more

quickly so that they do not incur interest.

ACTING

CHAIR:

Hang on. That is a furphy of an argument. The

point is, and you just agreed to this a minute

ago: the gap is at a record high for low-rate

cards as well as high-rate cards. For all cards,

it is at a record level, isn't it? It is not as

if I can go to a low-rate card and I will be

okay. Even for the low-rate cards, the gap

between that and the cash rate has now reached a

record level.

Dr Edey: That gap

has gone up as well.

But there are also

zero-rate cards. The banks do offer switching

packages where you can get an interest-free card

if you switch banks.

Mr

Campbell: For a few

months.

Dr Edey: For

limited periods. What I am saying is that there

are ways you can take advantage of the

competition that is there to reduce your

interest.

ACTING

CHAIR:

I just want to be very clear, Dr Edey, on what

you are saying. I want to be able to walk away

from this and get a good understanding. The

point you seem to have been making is this—and I

want to put this together; tell me if this is

incorrect. Firstly, what you are saying, from

the evidence that you seem to be presenting,

does question some of the assertions that have

been made as to why the gap is so high. The

point you seem to be making is:

'Yes, we are

talking'—and you are going to get us the exact

figures, but the default rates are quite small;

the non-performance rate is quite small. We want

to get to the bottom of how and why the gap

between credit card rates and the cash rate has

reached a record level. We are asking you, Dr

Edey, whether it is something the Reserve Bank

is prepared to look at, and it seems to be that

the answer you are giving us is, 'No.'

Dr Edey: No, I am

not saying 'No' at all.

All I am really saying

is: somebody should look at it, and I think that

we should consult with our colleagues in other

agencies to determine who is the best placed to

lead it.

"Amid mounting evidence of bank

gouging on credit cards,

Australia’s corporate watchdogs are failing to protect consumers.

Dr Edey’s comments during the hearing

also highlighted fundamental flaws in the way banks and other

financial institutions are regulated in this country.

The truly big revelation in Dr Edey’s comments to parliament was

that no regulator in the country has recently seen fit to

investigate the gaping margin between credit card costs and the

prices at which they are sold.

In

response to questions from Labor senator Sam Dastyari and

independent senator Nick Xenophon, Dr Edey acknowledged that it was

an important issue that should be examined by a regulator, but he

wasn’t sure which one.

This

raises another issue, namely the failure of the

Council of

Financial Regulators – which the Reserve Bank coordinates – to

identify credit card pricing as an area worthy of inspection by

regulators.

The RBA and the Australian Prudential Regulation Authority have the

power to access sensitive data on the banks’ credit card businesses

and even though a persuasive case already exists that price gouging

is occurring, no regulator has fired a salvo.

If the Council was doing its job

properly the knowledge of the banking regulators would have already

been shared with the competition watchdogs – the Australian

Securities and Investments Commission and the Australian Competition

and Consumer Commission.

The fact

that it hasn’t underlines a major flaw in the current regulatory

framework.

That probably has a lot to do with the

RBA’s co-ordinating role in the Council’s work and the central bank’s alarming

indifference towards competition as a policy concern.

If part of the RBA’s mandate is to protect the welfare of

Australians in its execution of monetary policy, the Governor’s

commentary on credit cards pricing is a fail."

Mr. Byres also agreed

with Treasury, the RBA, and the Australian Securities and Investments

Commission officials that there ought to be closer scrutiny of the interest

rates banks are charging on their credit cards, because the current "spread"

between the official cash rate and rates charged on credit cards was at

record levels.

"I understand the point fully that the margins on credit card business

look very high, certainly to any other form of credit, and certainly I

can't sit here today with an explanation of why that is," Mr Byres said.

"Informing us all about that is probably a useful piece of work."

Post the

APRA

Chairman's above

undertaking almost three years ago, to

· The

institutional responsibility in the financial system for supporting

competition is loosely shared across APRA, the RBA, ASIC and the ACCC. In a

system where all are somewhat responsible, it is inevitable that (at

important times) none are.

Rather, we

need: regulatory settings that do not thwart competition between existing

institutions; more customer-oriented providers that consider their existing

customers (not just potential new customers);

less of a blizzard of new

but barely-distinguishable products with labels that obfuscate; much

better and far more open information on product prices and conditions; and

scope for consumers to more easily become unstuck (should they wish to be)

from their current banks and insurers.

The

financial system needs a competition champion

Competition in Australia’s financial system is without a champion among the

existing regulators — no government agency is tasked with overseeing and

promoting competition in financial markets, including forcing consideration

of whether actions by regulators materially harm competition. Under

the current regulatory architecture, promoting competition

requires a

serious rethink about how the RBA, APRA and ASIC consider competition and

whether the Australian Competition and Consumer Commission (ACCC) is

well-placed to do more than it currently can for competition in the

financial system.

As a forum for coordinating input

from financial system regulators on regulatory interventions, the CFR should

be a key avenue through which consideration of competition impacts is

promoted, analysed and made more transparent.

Shedding light on regulator decision making

As part of the broader adjustment in

regulatory focus required, greater transparency around decision making by the

financial regulators, including the CFR, is essential to ensure accountability

and an active consideration of effects on competition.

As a first step in this process, and

as a matter of priority for the Government, the Statements of Expectations for

ASIC and APRA need to be updated from their 2014 versions and reported against

annually. Such statements would provide financial regulators with the

Government’s perspective on their strategic direction and most crucially, allow

assessment after the fact to see if performance matched expectations. This draft

report should influence those documents.

The decisions made at the CFR are

profound in their impact on the financial system and the economy but there is no

public transparency around them. Regulation has tended to err on the side of

financial stability. Due to a lack of transparency, it is difficult to establish

whether this approach is justified in all cases.

The

CFR's consideration of competition analysis (and other market interventions)

should be minuted and published, as the RBA Board meetings are.An assessment that analyses in depth

the competition implications of a proposed regulatory intervention should be

discussed at the CFR meeting prior to the intervention starting. Regulators

should, in their Statement of Expectations, be required to consider amending

policies to alleviate adverse impacts on competition."

"Informing us all

about that (the current "spread" between the official cash rate and rates

charged on credit cards was at record levels) is probably a useful piece of

work."

Sadly, that ".....

useful piece of work"

failed to materialise at the quarterly October CFR meeting of

Australia's three statutory appointed regulators.

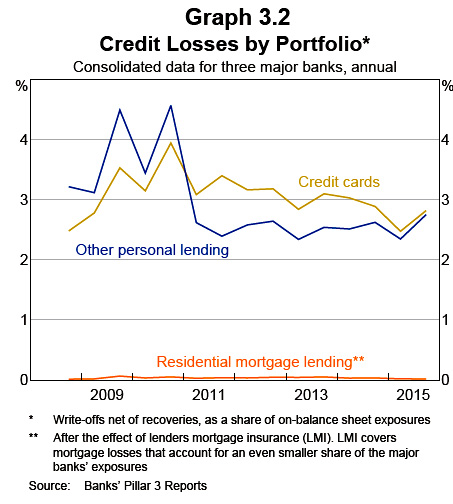

"In contrast, at around 2–3 per

cent over recent years, write-offs on credit card debt and other personal

lending have been higher, consistent with some portion of this lending being

extended to borrowers with a relatively weak credit profile and on an

unsecured basis. Although credit card and personal lending is riskier, it

represents only a small share of banks’ total domestic loans."

The FSR discussed the following

issues mentioning the word 'competition',

but not about what APRA

Chairman,

Wayne Byres told senators "....is probably a useful piece of

work."

nominal housing price growth

Funding and liquidity

the owner-occupier part of the

mortgage market and in parts of the business lending market.

a further deterioration in banks’ asset

quality in conjunction with slower rates of credit growth and the potential for

net interest margins to narrow if the liberalisation of interest rates increases

price competition for funding.

Household and Business Finances

competition in the owner-occupier

lending market remains strong

price competition for business lending

mortgage

lending insurance

price competition for new and lower-risk

owner-occupier borrowers

competition

for new large corporate loans

cost of banks’ domestic deposit funding

Profitability

competition in the mortgage market and

the housing price cycle

If the Royal Commission wants to

understand why Australia's 'central bank' has never exercised its rights -

These results, when considered together with Australian Bureau of

Statistics‘ research into Australians‘ general document literacy and

numeracy,15in particular

their ability to meet the complex demands of a knowledge-based economy,

suggest that about one in two Australians do not have the skills required to

make informed choices in their interactions with the financial services

sector.16

There is also

an identifiable age link, with document proficiency tending to decrease with

age.

14 For

example the 2008 ANZ study of financial literacy found that ‗67% of

respondents said that they understood the principle of compound interest,

but only 28% were

rated with a good level‘ of comprehension when they solved the problem‘,

ANZ Banking Group Limited,

ANZ survey of adult financial literacy in Australia, (The Social Research Centre) ANZ Banking Group, Melbourne, 2008, p. 19.

15As part of an

international study, the ABS measured skills in document literacy, prose

literacy, numeracy and problem solving and found that approximately 7

million (46%) of Australians (and 7.9 million (53%) of Australians aged 15

to 74) had proficiency less than the minimum required for individuals to

meet the complex demands of everyday life and work emerging in the

knowledge-based economy‘ for document literacy and numeracy respectively‘,

Australian Bureau of Statistics,

Adult literacy and life

skills survey results, cat. no. 4228.0, ABS, Canberra, 2006, p.

5.

16

These findings

have implications for our regulatory regime, which relies upon disclosure as

a critical element of our consumer protection system.

These results, when considered together with Australian Bureau of

Statistics‘ research into Australians‘ general document literacy and

numeracy,15in particular

their ability to meet the complex demands of a knowledge-based economy,

suggest that about one in two Australians do not have the skills required to

make informed choices in their interactions with the financial services

sector.16

There is also

an identifiable age link, with document proficiency tending to decrease with

age.

14 For

example the 2008 ANZ study of financial literacy found that ‗67% of

respondents said that they understood the principle of compound interest,

but only 28% were

rated with a good level‘ of comprehension when they solved the problem‘,

ANZ Banking Group Limited,

ANZ survey of adult financial literacy in Australia, (The Social Research Centre) ANZ Banking Group, Melbourne, 2008, p. 19.

15As part of an

international study, the ABS measured skills in document literacy, prose

literacy, numeracy and problem solving and found that approximately 7

million (46%) of Australians (and 7.9 million (53%) of Australians aged 15

to 74) had proficiency less than the minimum required for individuals to

meet the complex demands of everyday life and work emerging in the

knowledge-based economy‘ for document literacy and numeracy respectively‘,

Australian Bureau of Statistics,

Adult literacy and life

skills survey results, cat. no. 4228.0, ABS, Canberra, 2006, p.

5.

16

These findings

have implications for our regulatory regime, which relies upon disclosure as

a critical element of our consumer protection system.

Senator

XENOPHON:The

amount of credit card debt is $45 billion to $48

billion—$33 billion accrues interest. We are

sort of talking about the numbers of the Rudd

stimulus package in 2009. It is a lot of money

in the economy. What I am trying to understand

is this: you said that the banks say that the

interest rate is greater because of the risk

factor. Has the Reserve Bank tested, in terms of

the default rate for the banks, whether it has

gone up over the years, and that is why the gap

has increased and turned into a chasm? Have you

checked that? That seems to be what the banks

are saying: more risk; therefore higher interest

rates. Has the increase of interest rates, in

relative terms, been due to an increase in

defaults?

Dr Edey:We have

not tried to test that.

Senator

XENOPHON:Shouldn't that be tested though? That is an

underlying assertion on the part of the banks.

Dr Edey: I think

it is well worth somebody's while to test that.

Senator

XENOPHON:Right.

But you could liaise with APRA to get that

information. Is that right?

Dr Edey:I think

so.

Senator

XENOPHON:But does

it concern you, as Senator Dastyari pointed out,

with apologies to Elvis, that in terms of debt

people are caught in a trap and they just cannot

get out of it? Does it concern you that there

are many thousands of Australians who are stuck

in a debt trap because of credit card debt and

very high interest rates, who will not be able

to get on with their lives, will not be able to

get a decent credit rating and will not be able

to get their first home, because of interest

rates that appear to be much higher than a

well-functioning market would dictate.

Dr Edey: I think

it is a problem if people are in that situation.

I do not doubt that there are many people who

struggle with that sort of issue. But you need

to remember that the Reserve Bank has a top-down

systemic risk focus. So if there is enough of

that happening that it is a risk to the system

as a whole, that is our concern.

Senator

XENOPHON:But right now it is a known

unknown. We just do not know how many people

have been deeply affected by credit card debt,

and that itself might point to some systemic

issues.

Dr Edey: I cannot

put a number on how many people there are, but

we know how much debt there is.

Senator

XENOPHON:It would

be desirable to put a number on how many people

are deeply affected by credit card debt, would

it not?

Dr Edey:I am not

sure why quantifying that is an issue for the

Reserve Bank. We know how much debt there is. We

know what the non-performance rates are on

consumer debt. It is only about three per

cent—that sort of magnitude.

"The

Government agrees with the Inquiry’s objective of strengthening the

regulator accountability framework but does not support the creation of

a new Financial Regulator Assessment Board.

We

consider that new requirements in the

Public Governance,

Performance and Accountability Act 2013 (PGPA Act) and the

Government’s Regulator Performance Framework provide avenues to

strengthen regulator accountability along with other existing mechanisms

such as Parliamentary hearings.

We

will reconstitute the Financial Sector Advisory Council with refreshed

Terms of Reference to include providing advice on the performance of the

financial regulators by the end of 2015.

We

support providing regulators with clearer guidance in Statement of

Expectations and consider that the PGPA Act requirements are consistent

with the Inquiry’s recommendation for increased use of performance

indicators for regulator performance.

We

will update the regulators’ Statements of Expectations in the first half

of 2016, including providing a Statement of Expectations to the Payments

System Board for the first time."

"In contrast, at around 2–3 per

cent over recent years, write-offs on credit card debt and other personal

lending have been higher, consistent with some portion of this lending being

extended to borrowers with a relatively weak credit profile and on an

unsecured basis. Although credit card and personal lending is riskier, it

represents only a small share of banks’ total domestic loans."

contains the following references to the

Payment Systems (Regulation) Act 1998):

Subdivision D—Administration

16AJ Requiring assistance

(1)

APRA may, by written notice given to any of the following persons, require

the person to give APRA such reasonable assistance in the performance of its

functions, and the exercise of its powers, under this Division as is

specified:

(a) an ADI (whether or not it is a declared ADI);

(b) an administrator appointed under subsection

13A(1) to take control of an ADI’s business;

(c) a liquidator appointed in connection with the

winding up, or proposed winding up, of an ADI.

(2)

Without limiting subsection (1), APRA may require a liquidator to assist

APRA in APRA’s function of paying account holders their entitlements under

Subdivision C.

(3)

For example, APRA may, by notice issued under subsection (1), require the

liquidator to do the things specified in the notice, including:

(a) carrying on the business of the ADI so far as

necessary, or doing any other act or thing, to facilitate APRA’s payment to

account holders in accordance with Subdivision C; or

(b) seeking the re-entry of the ADI into a payment

system (as defined in section 7 of the

Payment Systems (Regulation)

Act 1998); or

(c) transferring the entitlements of account holders

to accounts held by the account holders in another ADI.

The

Banking Act 1959

contains the following references to the

Reserve Bank of Australia, in particular

Part V—Interest

rates

50 'Control of interest rates':

2 Commencement

Except as otherwise provided by this Act, this Act shall come

into operation on the day on which the Reserve Bank Act 1959

comes into operation.

8 Only the Reserve Bank and bodies corporate that are ADIs may

carry on banking business

11C Division not to limit operation of other provisions

Nothing in this Division is intended to limit the operation of

any other provision of this Act or of the Reserve Bank Act 1959.

11CE Supply of information about issue and revocation of

directions

Power to publish notice of directions in Gazette

(1) APRA may publish in the

Gazette notice of any direction made under

Subdivision A or B or section 29. The notice must include the name of the ADI or

authorised NOHC given the direction and a summary of the direction.

Requirement to publish notice of revocation of certain

directions in Gazette

(2) If APRA publishes notice of a direction made under

Subdivision A or B or section 29 and then later revokes the direction, APRA must

publish in the Gazette

notice of that revocation as

soon as practicable after the revocation. Failure to publish notice of the

revocation does not affect the validity of the revocation.

Requirement to provide information about direction to Treasurer

and Reserve Bank

(3) If the Treasurer or the Reserve Bank requests APRA to

provide information about:

(a) any directions under Subdivision A or B or section 29 in

respect of a particular ADI or authorised NOHC; or

(b) any directions made during a specified period under

Subdivision A or B or section 29 in respect of any ADIs or authorised NOHCs;

APRA must comply with the request.

16AE Advice and information for decision on making declaration

(1) The Minister may give APRA, ASIC or the Reserve Bank a

written request for advice or information about a matter relevant to making a

decision about making a declaration under section 16AD (including a matter

relating to the affairs of an ADI).

(2) As soon as reasonably practicable after being given the

request, APRA, ASIC or the Reserve Bank must give the Minister the advice or

information about the matter.

(3) In making the decision, the Minister must take into account

the advice and information (if any) that he or she has been given before making

the decision. This does not limit what the Minister may take into account in

making the decision.

Part V

—Interest

rates

50 Control of interest rates

(1) The Reserve Bank may, with the approval of the Treasurer,

make regulations:

(a) making provision for or in relation to the control of rates

of interest payable to or by ADIs, or to or by other persons in the course of

any banking business carried on by them;

(b) making provision for or in relation to the control of rates

of discount chargeable by ADIs, or by other persons in the course of any banking

business carried on by them;

(c) providing that interest shall not be payable in respect of

an amount deposited with an ADI, or with another person in the course of banking

business carried on by the person, and repayable on demand or after the end of a

period specified in the regulations; and

(d) prescribing penalties, for offences against the regulations,

not exceeding:

(i) if the offender is a natural person—a fine of $5,000; or

(ii) if the offender is a body corporate—a fine of $25,000.

1.

number, indebtedness and demography of the Credit Cardholders (which may include

a husband and wife

collectively) that the

Financial Counsellors are assisting; and

·$10,000 but

less than $20,000 - (eg. 2,556 Credit Cardholders (

individual or couples)

own

10,767 Credit Cards (= 4.2 Credit Cards per person or husband and wife/partner)

across 10 largest

community organisations) ·$20,000

but less than

$50,000 ·$50,000

but less than

$100,000 ·$100,000

but less than

$125,000 ·$125,000

but less than

$150,000 ·$150,000

or higher

Will the Royal Commission ask the

Chairman of the ACCC, Mr. Rod Sims, if the below extracts from 'Conditions

of use' booklets issued by St. George Bank, ANZ and

Westpac with text

in small fonts

constitute

Unconscionable Conduct?

*

St George Bank

"We strongly recommend

that you read this booklet carefully

and retain it for your future reference"

a 76

pages

Conditions of Use - Credit Guide

document of Conditions.

The word 'interest' appears in the 'Contents' twice and 78 more times throughout

the 76 pages. The word 'fee' or 'fees' appears 53 times.

*

ANZ's 'CONDITIONS

OF USE 20.06.2016 CONSUMER CREDIT CARDS'

is a 97 page booklet printed in 9

font. Cardholders

are requested to read voluminous parts of it as well as their Credit Card

Contract. The word "interest' appears 216 times in the booklet. The word 'fee' or

'fees' appears 104 times.

* "Ignite

by Westpac - Consumer Credit Card Conditions of Use". The

word 'interest' appears in the 'Contents' once and 92 more times throughout

the 43 pages. The word 'fee' or 'fees' appears in the

'Contents' once and 74 more times throughout the 43 pages. "This User

Guide forms part of your Credit Card Contract, along with the information

set out on the reverse of your welcome letter which advises you of your credit

limit and other prescribed information we are required to give you by law."

Clause 17 is "Do I have any other rights and obligations?" "Yes.

The law will give you other rights and obligations.

You should also READ YOUR

CONTRACT carefully."

These results, when considered together with Australian Bureau of

Statistics‘ research into Australians‘ general document literacy and

numeracy,15in particular

their ability to meet the complex demands of a knowledge-based economy,

suggest that about one in two Australians do not have the skills required to

make informed choices in their interactions with the financial services

sector.16

There is also

an identifiable age link, with document proficiency tending to decrease with

age.

14 For

example the 2008 ANZ study of financial literacy found that ‗67% of

respondents said that they understood the principle of compound interest,

but only 28% were

rated with a good level‘ of comprehension when they solved the problem‘,

ANZ Banking Group Limited,

ANZ survey of adult financial literacy in Australia, (The Social Research Centre) ANZ Banking Group, Melbourne, 2008, p. 19.

15As part of an

international study, the ABS measured skills in document literacy, prose

literacy, numeracy and problem solving and found that approximately 7

million (46%) of Australians (and 7.9 million (53%) of Australians aged 15

to 74) had proficiency less than the minimum required for individuals to

meet the complex demands of everyday life and work emerging in the

knowledge-based economy‘ for document literacy and numeracy respectively‘,

Australian Bureau of Statistics,

Adult literacy and life

skills survey results, cat. no. 4228.0, ABS, Canberra, 2006, p.

5.

16

These findings

have implications for our regulatory regime, which relies upon disclosure as

a critical element of our consumer protection system.

Will the Royal Commission recommend to the

Three Financial Regulatorsthat they use their existing

regulatory powers to require all Credit Card Issuers to simplify their Credit

Card Products so that their Credit Cards 'Conditions of Use' booklet,

together with any Schedule/s referred to therein, do not exceed 50 pages in text no smaller than Arial 10?

=================================================

Supporting Evidence re 18th Question

*

St George Bank

"We strongly recommend

that you read this booklet carefully

and retain it for your future reference"

a 76

pagesConditions of Use - Credit Guide

document of Conditions.

The word 'interest' appears in the 'Contents' twice and 78 more times throughout

the 76 pages. The word 'fee' or 'fees' appears 53 times.

*

ANZ's 'CONDITIONS

OF USE 20.06.2016 CONSUMER CREDIT CARDS'

is a 97 page booklet printed in 9

font. Cardholders

are requested to read voluminous parts of it as well as their Credit Card

Contract. The word "interest' appears 216 times in the booklet. The word 'fee' or

'fees' appears 104 times.

* "Ignite

by Westpac - Consumer Credit Card Conditions of Use". The

word 'interest' appears in the 'Contents' once and 92 more times throughout

the 43 pages. The word 'fee' or 'fees' appears in the

'Contents' once and 74 more times throughout the 43 pages. "This User

Guide forms part of your Credit Card Contract, along with the information

set out on the reverse of your welcome letter which advises you of your credit

limit and other prescribed information we are required to give you by law."

Clause 17 is "Do I have any other rights and obligations?" "Yes.

The law will give you other rights and obligations.

You should also READ YOUR

CONTRACT carefully."

Does each of the Four Pillars reducing their low interest credit card by

5% circa

in recent months, amidst the prospect of a Royal Commission,

evidence that the Four Pillars that issue 80% of Credit Cards used in

Australia, were uncompetitive during the

Council

of Financial Regulators'watch', when each of the RBA, ASIC and

APRA have regulatory obligations to the australian public

to ensure real competition amongst Credit Card Issuers?

Will the Royal Commission recommend that Reward Programs be banned?

=================================================

Supporting Evidence re 20th Question

Rewards Programs constitute tax evasion because benefits received can be

measured as 'income' or 'cash outlays avoided', but such receipts are not income taxed.

Credit Card Products informs inter alia that the humble means of

obtaining a 'Product' and/or a 'Service' on credit, by presenting a Credit Card

to aMerchant, now

renders those plastic cards to be the most differentiated product in the Western

World for the simple reason of Credit Card Issuers maximising their profits

amidst a diverse range of

Financial Literacy

Capacity

and inadequate laws/regulations.

Credit card reward schemes are mostly a gimmick

unless you're a big spender, since rewards cards

nearly always charge hefty annual fees and high

interest rates.

Credit card reward programs deliver little or

nothing to consumers who don't spend generously via

their credit cards.

A

CHOICE investigation of 63 rewards credit cards

found that consumers would need to spend at least

$2000 a month to get any return, while those who

spent $1000 a month or less

would pay more in annual fees than they got back in

rewards.

Our research has also shown that cards that

reward you with frequent flyer points are a far

better deal than gift card or cash back rewards

cards, where rewards accumulate at a much slower

rate."

"When the benchmarks for credit card interchange

fees were introduced in 2003, the Board’s aim was to

limit the tendency for competition between schemes

to drive up interchange fees. By setting the

benchmarks in weighted average terms, the Bank

allowed schemes significant flexibility to set

different interchange fees for different

transactions, some of which could be over the

benchmark.

Schemes

have taken advantage of this, and of the current

infrequent compliance arrangements, to develop

commercial strategies that encourage issuers to

maximise interchange revenue. The result has been

that actual average interchange fees have tended to

be higher than the regulatory benchmark and have

drifted further above the benchmark between the

three yearly compliance points. Accordingly, the

benchmark has not represented an effective cap on

average interchange fees."

Will the Royal Commission recommend to the

Three Financial Regulatorsthat they use their existing

regulatory powers to ban Credit Card Issuers paying third party credit card

websites such as the following from marketing in any way, shape or form their

Credit Card Products

because such advertisements are often misleading and deceptive and targeted at

Credit Cardholders with low

Financial Literacy Capacityas quantified by the Productivity Commission

and the ABS inChapter

1?

* Request

to the Reserve

Bank of Australia, hereinafter the RBA, to

implement the same

"competitiveness and efficiency"

that it has overseen in the 'wholesale supply side' of the debit and credit cards products to the

Retail Supply Side of

credit cards, because banks profits from credit cards are not derived

from the User Pays Principle

*

All users should pay the cost of their credit card

transactions, and not some "unlucky" users paying a disproportionate burden

which has further gapped the "Haves" from the "Have Nots"

Below is an extract from Section 1 titled

'Summary of eight Attachments' of

(i) entrusted to be

banker and financial agent for the Commonwealth; and

(ii) with a charter to protect

"

....the

economic prosperity and welfare of the people of Australia".

if

CreditCards.com(parent site ofaustralia.creditcards.com)

is being paid by some

or all ofOur

Bank/Issuer Partners(ANZ, Aussie, Bank Mecu, Bankwest, citi, NAB, St George, Virgin, Westpac)

for providing links to those banks' websites credit card products at

,

because some like NAB's Low Interest Credit Card, Bank mecu's Low Interest Rate

Credit Cardand

Bankwest'sBreeze MasterCardare patently deceptive.

2. The only party that should make

representations about the respective benefits, or costs, of a Credit Card, which

is a material financial 'borrowing instrument' available to Australian's with

poor Financial Literacy

Capacity, should be the Credit Card Issuer. Removing the above

'web platform sellers' should reduce the delivery costs of Credit Card Issuer

and avoid a lot of misinformation and deception. Due to the internet,

together with more traditional media (newspapers, radio and TV), there are ample media

options available to Credit Card Issuers to advertise their own Credit Cards.

"Brian Cole, of Capital One in the UK, the bank that first introduced

zero-interest balance transfers to Britain in the 90s, says: "There's a lot

of practice in the [banking] marketplace that is shameful, and credit card

companies are not immune. [Balance transfer] customers think they're going

to progress in getting out of debt, and get some relief from interest

payments. But make a mistake and you will end up making money for your

credit card company."

"CBA's head of retail banking services, Matt Comyn,

claimed it had never offered zero rates on balance transfers because it

could become a "debt trap" for customers.

"We view that such arrangements are not the right thing to offer our

customers," he said"

Commonwealth Bank said zero per cent balance transfers

should be banned

and mandatory minimum repayments of interest and principal should be imposed for

card holders of up to 2.5 per cent.

NAB question CBA's motives

However, NAB – which has the smallest credit card market share of the major

banks at 10.5 per cent – told the same hearing 0 per cent balance

transfers helped competition and questioned the motives of CBA as the dominant

credit card issuer with about a quarter of the market.

Mr Comyn denied the bank's enthusiasm for banning zero per cent balance

transfers was more about reducing the ability of competitors to take its

customers. He said CBA competed on other features, including technological

innovation such as giving customers the ability to block overseas transactions."

"For instance, the number of cards that offer a balance transfer at an interest

rate of zero have more than doubled in the past year, Finder.com.au reports."

Credit card companies just

love to advertise low or no interest rates for debts transferred from other

cards, purportedly to help you get

out of debt. But it's really a ruse to bring new customers on board and get

them paying interest down the road.

The interest rate applying to

the balance transfer generally ranges from 0% to 5%, for a period of four

months up to as long as it takes you to repay the debt. It can seem like an

offer too good to refuse.

One big thing to bear in

mind, though, is that the low-interest or no-interest offer generally

applies to the amount you transfer over from another card only – not to any

new purchases with your new card – and you will likely be charged a fee

based on the amount you're transferring, one that can go as high as 3%

(meaning you would pay $30 to transfer over $1000 and $300 to transfer over

$10,000).

The longer the interest-free

period, the higher the balance transfer fee.

Switching to a no-interest or

low-interest balance transfer credit card can be a good way to get a handle

on your debt or to avoid making repayments for a certain period of time.

But for the unsuspecting or

undisciplined, balance transfer cards can go terribly wrong.

And bear in mind that

flipping your debt to a low-interest or no-interest promo deal too often can

affect your credit rating, as can having multiple credit card applications

rejected.

The top five balance transfer credit card

traps

1. The 'payment hierarchy' con

When you make repayments,

they're firstly applied to the balance transfer amount – even if the card

has a 0% interest rate, and even if other purchases and cash advances are

accumulating interest at higher rates. In other words, the credit card

people have rigged it so you'll end up paying as much interest as possible.

As one credit card provider

puts it: "Payments made to your credit card account are first applied to any

amounts transferred from other credit cards, charge cards or store cards

under this promotion, before they are applied to any other purchase or cash

advance amount. This means that the portion of your outstanding account

balance that is subject to a lower interest rate will be paid off first."

Katherine Lane, Principal

Solicitor with the Consumer Credit Legal Centre in NSW, told us this payment

hierarchy technique "is a trick most often used in interest-free deals to

trigger interest being charged. It is completely unfair."

2. High interest on

new transactions

After you transfer your debt

to a low-interest card, any new transactions you make usually attract