Grounds/Reasons for Written Questions

Chapter 5. The Reserve Bank removed the 18% cap on Credit Card interest rates in April 1985. As chronicled further below, the spread between the wholesale cost of funds, the Overnight Cash Rate, and max Credit Card interest rate in 1985 was less than 1%. That spread is now as high as 26% on 'Go Mastercard' after Latitude Financial's cost of funds. The Reserve Bank has failed to re-regulate Credit Card interest rates, notwithstanding that Credit Cardholders with only Level 1 and Level 2 Financial Literacy Capacity (Financially Uneducated And Vulnerable Australians) have suffered Extreme Financial And Emotional Distress due to removal of that Cap in April 1985.

Australian Credit Card Products operate on the 'User Doesn't Pay Principle'

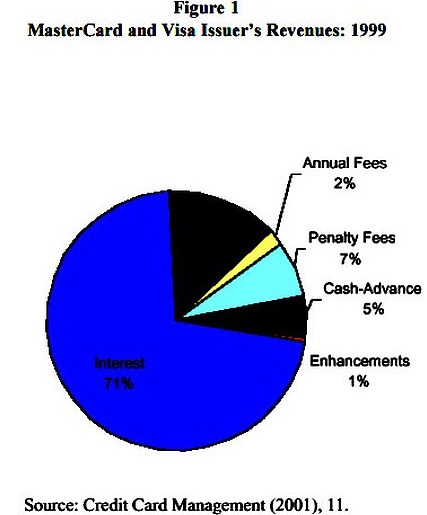

* 67% circa of Credit Cardholders are Transactors that enjoy a Free Ride with their Line/s of Credit

* 33% circa of Credit Cardholders are Revolvers that pay all Interest and Penalty Fees Revenue which covers all Credit Card Issuers operating costs, incl. write-offs/fraud

Revolvers are made up of -

* Occasional Revolvers that represent 62% circa of all Revolvers that pay 20% circa of Interest and Penalty Fees Revenue

* Persistent Revolvers that represent 38% circa of all Revolvers that pay 80% circa of Interest and Penalty Fees Revenue

Australian Credit Cards operate on the 'User Doesn't Pay Principle' if the Cardholder is a Financially Literate 'Transactor', because the minority of Cardholders that are Financially Uneducated And Vulnerable Australians, who possess only Level 1 or Level 2 Financial Literacy Capacity (as identified by the Productivity Commission and ABS - Chapter 1), known as 'Revolvers', together with some that suffer from Compulsive Buying Disorder, pay Interest And Fees Revenues levied by Credit Card Issuers, thereby enabling the 'Financially Educateds' to enjoy the substantial benefit of their Revolving Lines Of Credit as Free Riders 'year-after-year-after-year'.

Transactors make full use of the costly electronic infrastructure of the Four Party Schemes and Three-Party Schemes to each make hundreds of Purchases each year 'with a swipe', and not pay for their Purchases for up to 55 days later. The majority of Transactors make Purchases that aggregate to over $20,000 pa. Many receive over $100 per year in Reward Programme Points. Some 'Premium' Credit Cardholders receive $2 back for every $100 expended - income tax and FBT free. Some claim their Annual Credit Cardholder Fee as a tax deduction.

On the Retail Supply Side, the Credit Card Product is devoid of any semblance of the ubiquitous User Pays Principle. In fact, the opposite applies. There is no 'transaction fee' each time that a Cardholder uses its Credit Card Products. A 'transaction fee' was levied for the predecessor to the Credit Card, namely when writing a personal or company cheque ($1.50 fee) or purchasing a bank cheque ($15 fee). If one requests an overdraft on their bank account, one -

* pays a flat 'Overdraft Fee' for the 'Overdraft Limit'; and

* is charged interest on usage.

The Retail Supply Side -

(a) is made up of only two parties (Australian Credit Cardholders and Australia's Three Financial Services Regulators); and

(b) does not contain a powerful lobby group to represent the interests of Credit Cardholders (unlike the Wholesale Supply Side) to ensure equitable 'User Pay' pricing.

The Interest And Fees Revenue structure of Credit Cards preys upon Credit Cardholders with poor Financial Literacy Skills. See Re (b) above, in Chapter 3 above.

A Credit Card is the only style unsecured personal loan that does not charge the customer a 'loan limit fee' and a usage fee based on the loan outstanding unilaterally for each usage.

Chapter 18 below notes 'inter alia' that the Australian Retailers Association - Submission to RBA dated 2001 - Credit Card Schemes in Australia advocated that the:

"Merchant Service Fees should be completely abolished and replaced with market negotiated activity based fees;"

Australia's Three Financial Services Regulators -

-

that were established by Acts of Parliament to 'inter alia' act in the best interests of Australians, that are ill-equipped to -

- identify the Spiders deceitfully placed in Predatory Advertising within; and

- manage their Credit Card finances,

-

have not acted with the same vigor as the Four-Party Schemes and the Three-Party Schemes have behaved in the Wholesale Supply Side.

Reserve Bank of Australia - Our Role notes 'inter alia':

the Bank’s payments system policy is directed to the greatest advantage of the people of Australia; and

the powers of the Bank under the Payment Systems (Regulation) Act 1998 and the Payment Systems and Netting Act 1998 are exercised in a way that, in the Board's opinion, will best contribute to:

promoting competition in the market for payment services, consistent with the overall stability of the financial system.

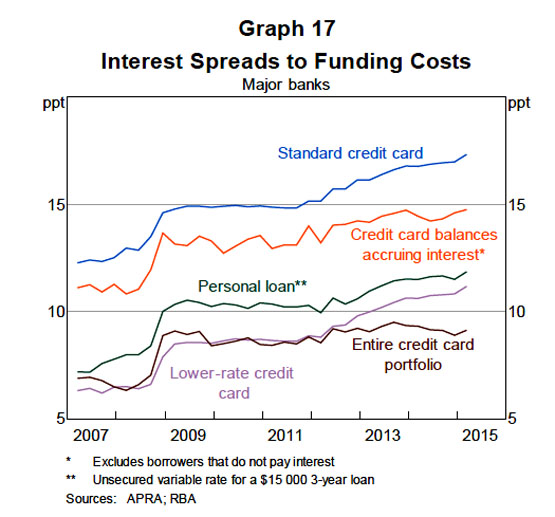

"Based on estimates of the overall cost of funds for banks, it is possible to calculate the spreads on different lending rates (Graph 17).11 The data indicate that the interest rate on bank credit card portfolios is around 9 percentage points above the cost of funds, while the spread for those borrowers who are paying interest is about 14¾ percentage points. These spreads rose significantly in the global financial crisis (when funding rates fell significantly but credit card rates fell by much less) and have remained at that level or drifted modestly higher since.

The observation that issuers compete actively for customers yet credit card interest rates are high and do not closely follow changes in funding costs is consistent with international experience and has been studied by academics. The most well-known paper addressing this issue is a study by Ausubel (1991) for the United States. The study notes the apparent paradox that a market with few barriers to entry and the presence of 4 000 competitors could be characterised by very sticky interest rates and card issuers making much higher rates of return on their credit card lending than on other lines of business. Based on the work of Ausubel and others, it seems reasonable to explain the apparent paradox as resulting to a large extent from the existence of a significant number of consumers who are either not well informed or (for various behavioural reasons) are reluctant to switch banks or seek a lower rate. At the same time, banks may have little incentive to lower interest rates, given that rates are not a determining factor for many individuals who may (possibly mistakenly) not expect to build up significant balances, while in the case of other individuals, banks may worry that lower rates may attract lower-quality borrowers."

Below is an extract from 'Summary' in

THE OFFICE OF REGULATION REVIEW dated mid-1990s which commented that should bank fees and charges change in the future the most efficient approach would be to provide specific groups of customers with fee-free basic banking services, with the Commonwealth Government reimbursing the banks for the costs of doing so:"The structure of bank fees and charges could change in the future. In that case, the argument for government intervention may become stronger. However, any such intervention would not be without cost. On balance, the ORR considers that, if the government chose to intervene, the most efficient approach would take the form of a “community service obligation” on banks to provide specific groups of customers with fee-free basic banking services, with the Commonwealth Government reimbursing the banks for the costs of doing so."

The highest Purchase interest rate is 25.9% from "Lombard Visa Card Classic". The highest Cash Advance interest rate is 29.49% from Latitude Financial's "Go MasterCard"

In November 2007 the official cash rate was 6.50% and the average credit card interest rate was 14.51%. Nine years later, in Jan 2017, the official cash rate was 5% lower at 1.50%, yet the average credit card interest rate had risen to 17.00%, being 2.39% higher than in 2007. Why are Credit Cardholders 7.39% worse off for unsecured personal lending when the Australian economy is robust?

Below is Recommendation 30 of the TREASURY SUBMISSION TO THE SENATE ECONOMICS REFERENCES COMMITTEE INQUIRY INTO MATTERS RELATING TO CREDIT CARD INTEREST RATES - 11 August 2015 to Strengthening regulators’ focus on competition (Recommendation 30) "has fallen on deaf ears":

"The Inquiry noted that there is currently no process for regularly assessing the state of competition in the financial system, nor a requirement for regulators to demonstrate that they have given consideration to the trade-offs between competition and their other objectives, creating the risk that competition issues may be ignored.

The Inquiry recommended reviewing the state of competition in the financial system, as well as improving the way in which regulators report how they balance competition against their core objectives and to include explicit consideration of competition in ASIC’s mandate. The review would examine and report on whether there are barriers which are inappropriately limiting competition or imposing barriers to foreign or domestic market entrants. "

Based on the above 5 extracts, Revolvers account for 33% [30-40 per cent (3rd extract) + 30 per cent (4th extract) / 2] of Credit Cardholders.

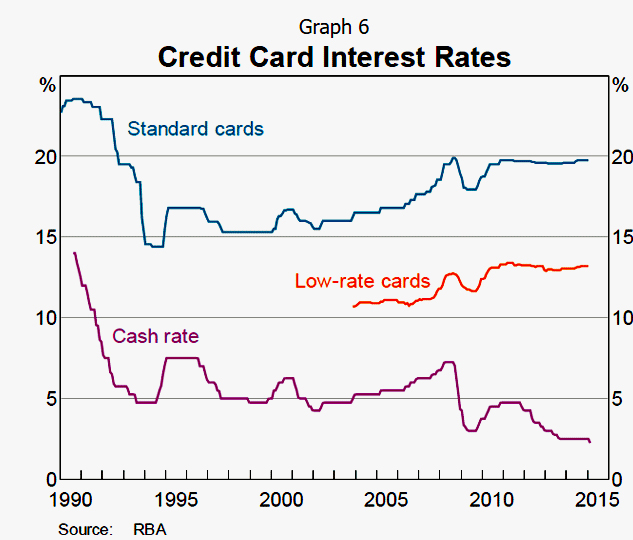

Below are two insightful graphs from RBA Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - Aug 2015:

-

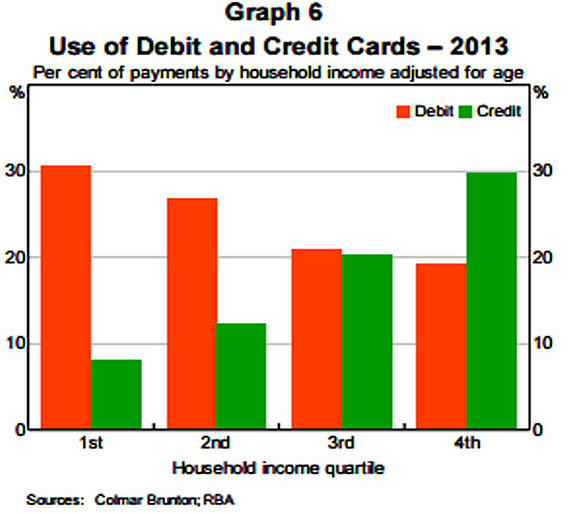

Graph 6 below evidences that higher-income households use credit cards much more frequently that debit cards; however debit card use is more common for lower-income households.

-

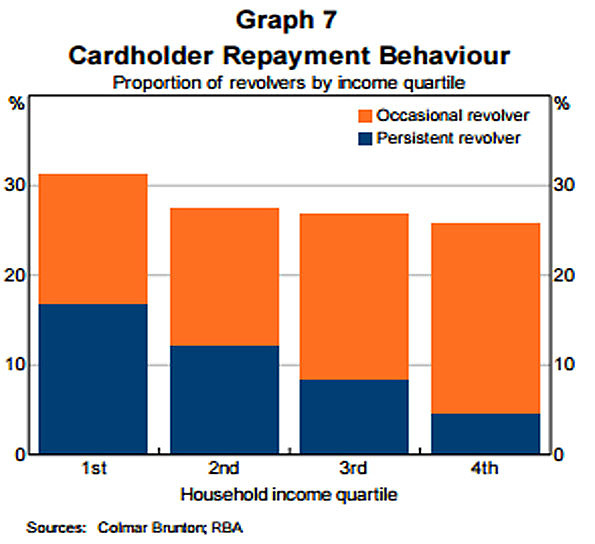

Graph 7 below evidences that over one third of Revolvers are Persistent Revolvers.

| Occasional Revolvers | Persistent Revolvers | ||

| 1st (lowest) Household income quartile | 45% | 55% | |

| 2nd (second lowest) Household income quartile | 55% | 45% | |

| 3rd (second highest) Household income quartile | 66% | 34% | |

| 4th (highest) Household income quartile | 82% | 18% | |

| 248% | 152% | ||

| 248% | 62% | Occasional Revolvers | |

| 152% | 38% | Persistent Revolvers | |

| 400% | 100% |

Casual empiricism of the above immediately above table (calculated from RBA Graph 7 above) suggests that approx. -

* 62% of Revolvers, referred to by the RBA as Occasional Revolvers, pay interest occasionally.

* 38% of Revolvers, referred to by the RBA as Persistent Revolvers, pay 17% interest rate (average) on 100% of their Credit Card Debt Accruing Interest.

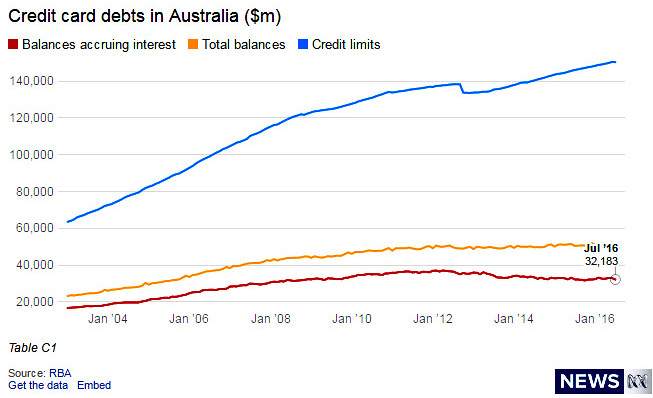

Revolvers represent 33% of Credit Cardholders transactions. Revolvers carried $32.183 billion (see above graph as at July '16) of interest accruing Credit Card debt at an average per Credit Card debt of $6,095 paying interest @ an ave. 17% p.a. = $1,036 pa. interest on average per Credit Card used. This $1,036.20 pa. circa takes no account of Late Payment Fees.

|

Table 'A' |

||

| Agg Credit Card debt - July '16 | $32,183,000,000 | |

| Total number of Credit Cards | $16,000,000 | |

| Revolvers |

33% |

$5,280,000.00 |

| Ave debt | $6,095.27 | |

| Ave. interest rate |

17% |

|

| Ave. interest per Card per Revolver | $1,036.20 | |

|

Table 'B' |

||

| Total Revolvers | 33% | of all Credit Cards |

| Persistent Revolvers' | 38% | of all Revolvers |

| Total 'Persistent Revolvers' | 12.58% | of all Credit Cards |

| Total 'Persistent Revolvers' hold |

2,006,400 |

Credit Cards |

The immediate above 'Table B' evidences that 12.58% circa of Credit Cards are held by Persistent Revolvers (Revolvers = 33% of Credit Cardholders. Persistent Revolvers = 38% of Revolvers. 38% of 33% = 12.58%)

McKinsey Report - May 2014 categorizes 'Five Segments' of Credit Cardholders in the USA. Below is an extract from the 'Third Segment', namely 'Financially stressed':

"Carry heavy credit card debt—nearly four times the average, at USD$7,453."

Australia's nomenclature for USA McKinsey's 'Financially stressed' Credit Cardholders is Persistent Revolvers that "Carry heavy credit card debt—nearly four times the average with unpaid debt. Occasional Revolvers therefore contribute approx one quarter of Interest and Penalty Fees Revenue.

The above Australian calc of AUD$6,095 average debt is per Credit Card of the 5,280,000 (33% of all Credit Cards) held by Revolvers of the 16.09 million Credit Cards owned by Australians. The above ave of USD$7,453 from the McKinsey Report represents agg. debt per Credit Cardholder amongst the 'Financially stressed'.

The Senate Economics References Committee received 39 written submissions in 2015. It then published it findings "Interest rates and informed choice in the Australian credit card market" - 107 pgs. On the subject of Financial Literacy the Committee's "Recommendation 9 - The government should consider expanding financial literacy programs such as the Australian Securities and Investments Commission's MoneySmart Schools Program."

67% circa of all Credit Cardholders, being Transactors, enjoy a Free Ride. Those Free Riders' Revolving Lines of Credit are paid for by 33% circa of Credit Cardholders that are Revolvers of which 38% of Revolvers are Persistent Revolvers that -

* hold 12.58% of the 16.1 million Credit Cards in Australia; and

* pay 80% of Interest and Penalty Fees Revenue - displayed in Figure 3 in Chapter 8 below.

The Pareto Principle, colloquially known as the '80-20 Rule', is that 20% of customers generate 80% of the revenue for a particular business. The Pareto Principle has been 'blown away' because 12.58% of Credit Cardholders (not 20%), namely Australia's Persistent Revolvers (referred to by McKinsey in the USA as 'Financially stressed'), identified in the above RBA Graph 7 "Cardholder Payment Behaviour" (in RBA report RBA Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - Aug 2015), pay 80% circa of Interest and Penalty Fees Revenue. This is a shocking indictment of the RBA due to the apparent concern about banks not passing on interest rate cuts that the present Governor of the Reserve Bank, Phillip Lowe, expressed in LOAN RATE STICKINESS: THEORY AND EVIDENCE in June 1992 which identified 25 years ago that:

· "The rate on credit cards is found to be the most sticky, followed by personal loan rates, the housing loan rate and the small business overdraft rate.

· In contrast, the rates on personal loans and credit cards do not appear to be more flexible in the deregulated period."

The RBA would likely retort that it de-regulated loan and deposit interest rates following the recommendations in the Campbell Report. Chapter 17 notes:

"The Campbell Committee was established in 1979 and reported in 1981. The recommendations of the inquiry were targeted at ..... the abolition of direct interest rate and portfolio controls on financial institutions. Campbell did not recommend removal of any powers held by the Reserve Bank to regulate interest rates or demand financial information. The Campbell recommendations were made following an extended period of high interest rates. High deposit interest rates by NBFIs existent circa 1980 are no longer an impediment to regulating credit card interest rates. The abovementioned reference to Chapter Nine (in Chapter 15 above): 'Stability and Payments' of the Wallis Enquiry noted "the RBA should retain overall responsibility for the stability of the financial system, the provision of emergency liquidity assistance and for regulating the payments system."

Below is an extract from Consumer Affairs Victoria - Regulating the cost of credit which evidences that in the past if de-regulation did not achieve the desired results, then re-regulation followed. But not with regard to re-introducing a max interest rate Cap on Credit Cards, notwithstanding that the spread between the current Cash Rate of 0.1% and the Credit Card Purchase Interest Rate of 20% is 19.9%. (As at April 2017, the highest Purchase interest rate was 25.9% from "Lombard Visa Card Classic" and the highest Cash Advance interest rate was 29.49% from G.E. Money's "Go Mastercard"):

"The tide of utilitarianism rose slowly, and a lengthy campaign was necessary before the financial deregulation of 1854, which abolished the British interest rate cap. However, one act of deregulation cannot quell an argument that has been going on for millennia. Over the following century the tide gradually turned towards re-regulation, culminating with detailed requirements imposed on the financial sector (particularly the banks) during and immediately after the Second World War. We now trace the gradual lead-up to this second phase of regulation."

"Obviously this is a pretty radical act, and it will be fought," he replied. "But I think the American people are disgusted with the financial industry. They want change.

You could argue that an interest rate of 15% or 18% is more than enough to accommodate any amount of risk on the lender's part. If a loan appears riskier than that, don't make it.

What we have to ask as a nation is whether it's ethical to charge people 30% interest rates," Sanders said. "This is loan sharking. Let's call it what it is."

The majority of Revolvers are on low incomes and suffer Extreme Financial And Emotional Distress. Managing money whilst on a low income is infinitely more difficult than for those that are, or have been, on good salaries, inherited wealth etc. Other Revolvers succumb to Compulsive Buying Disorder.

The Commonwealth Treasury noted in 2010 in its submission to National Credit Reform: Enhancing Confidence and Fairness in Australia’s Credit Law that

the Standing Committee on Economics found that ‘there was anecdotal evidence that in some cases at least the impost of high default fees is marginalising people who are already struggling to feel they belong in society.’22Hence, the above "Recommendation 9 - The government should consider expanding financial literacy programs such as the Australian Securities and Investments Commission's MoneySmart Schools Program" totally ignores assisting the 33% of Credit Cardholders that are Revolvers' that carry 100% of the $33.1 billion of interest bearing debt.

Correcting Usurious Interest Rates that are as high as 25.9% for Purchases and 29.49% for a Cash Advance, by Australia's longstanding banking regulator, namely the Reserve Bank, re-introducing a cap on Credit Card interest rates that applied up to April 1985 would be infinitely more effective than increasing expenditure on the likes of a MoneySmart Schools Program (proposed above).

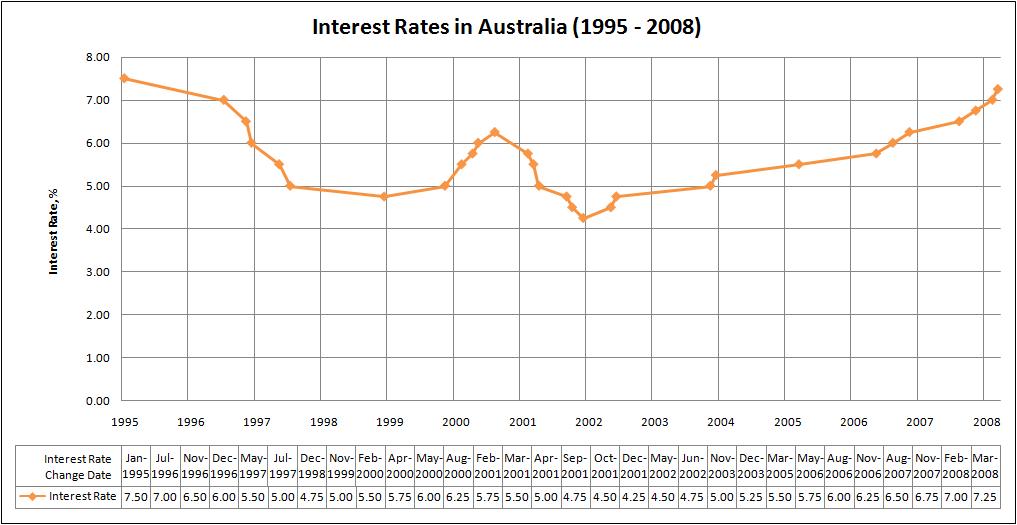

Above graph is drawn from RBA Excel file f01dhist_NEW.xls

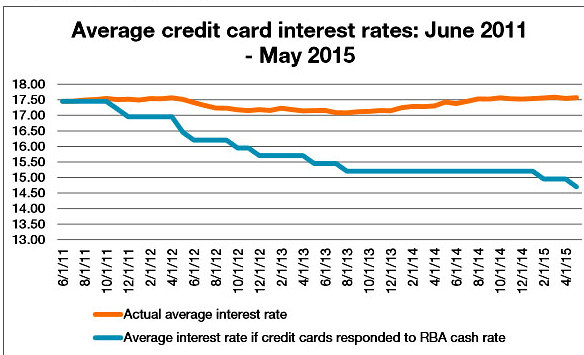

Below is an extract from CUTTING CREDIT CARD CONFUSION - CHOICE - Submission to Senate Economics References Committee - Matters related to credit card interest rates - Aug 9, 2015

"Interest rates have increased

The average credit card interest rate at 31 May 2015 was 17.61%. Instead of falling in line with the cash rate, the average credit card interest rate has risen by 0.2% over the last four

years from 17.41% in June 2011. 1

1 Based on an analysis by Mozo of interest rate changes of over 170 credit cards between 2011 and 2015. Unless otherwise noted, all data in section oneis based on figures supplied by Mozo.

The graph above compares the average credit card interest rate on all cards to the interest rate if cards responded to RBA announcements. If credit card interest rates had moved in line with RBA cash rate announcements, as they largely had before 2011, the expected average interest rate in May 2015 would have been 14.70%.

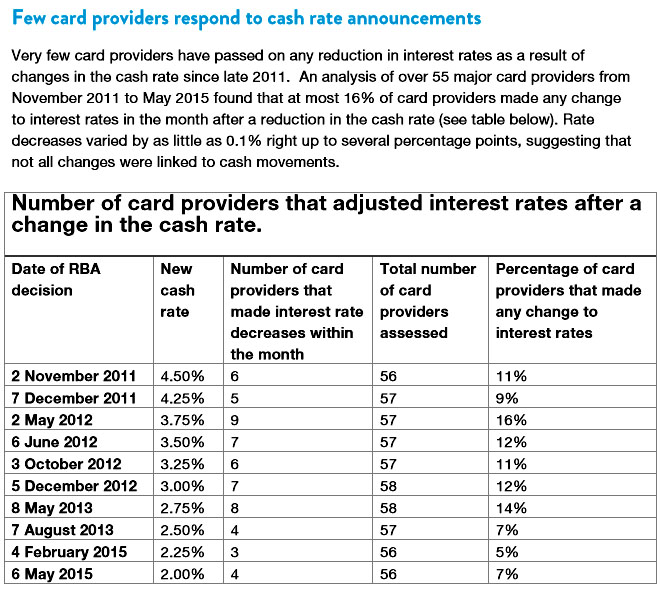

Few card providers respond to cash rate announcements

Very few card providers have passed on any reduction in interest rates as a result of changes in the cash rate since late 2011. An analysis of over 55 major card providers from November 2011 to May 2015 found that at most 16% of card providers made any change to interest rates in the month after a reduction in the cash rate (see table below). Rate decreases varied by as little as 0.1% right up to several percentage points, suggesting that not all changes were linked to cash movements."

Effective Date Change in % points Cash Rate Target

Graph 6

|

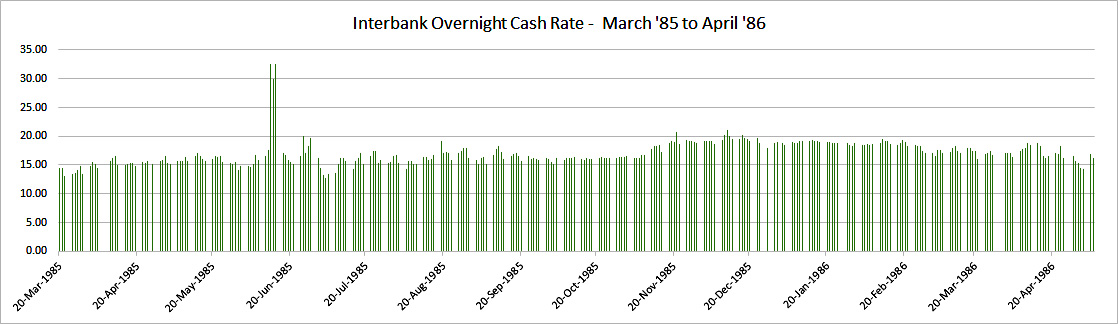

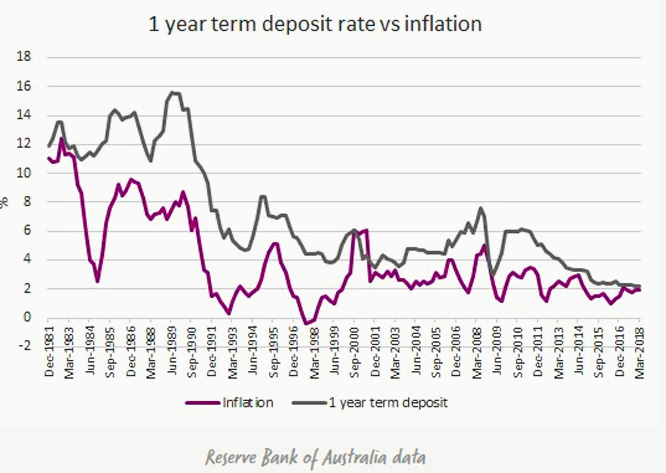

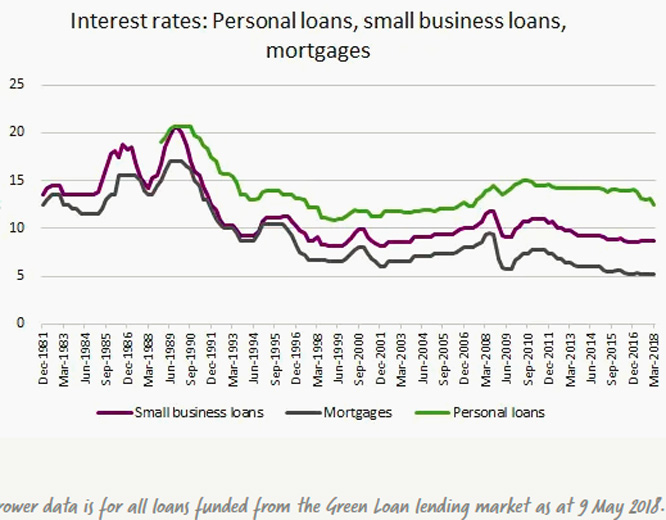

The spread between the wholesale cost of funds and Standard Credit Card Purchase Interest Rate has widened and widened and widened:* was less than 1% when the 18% cap was removed in April 1985 * was 10% in 2001 * was 18.5% in March 2017 * June 1986 - less than 1% Below is an extract from BANKING LEGISLATION AMENDMENT BILL 1986: "For example, at the end of June 1985 interest rates were in the range 17.25% to 19%."

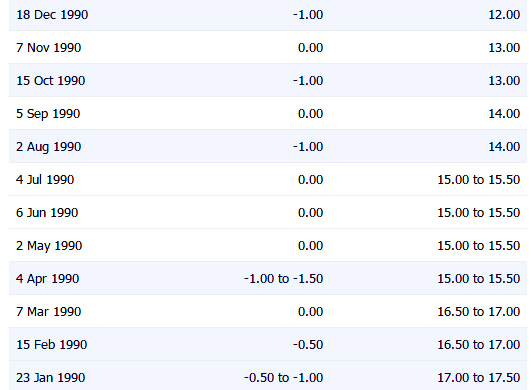

* December 1987 - spread 2½% Based on the immediately above two Light Blue RBA graphs titled "Simple Measures Of Bank Margins" that appear in RBA's "Bank Interest Rate Margins dated 1992, that 2½ years after the cap was removed in April 1985, namely in Dec 1987, the variance between the then Overnight Cash Rate and the Standard Credit Card Purchase Interest Rate was 2½% (13½% minus 11%). * January 1990 - spread 5.5% The RBA website page Cash Rate does not list Cash Rates prior to 23 Jan 1990. On that (oldest) date, five years after the 18% cap on Credit Card interest rates was removed in April 1985, the Overnight Cash Rate was 17.5% on 23 Jan 1990 (using the Interactive hover mouse on that RBA webpage) or reviewing the below " Graph of the Cash Rate''. The below RBA Graph 6 'Credit Card Interest Rates' (sourced from Developments in the Card Payments Market - Mar 2015) shows the Standard Credit Cards Purchase Interest Rate @ 23% on January 1990 and a spread of 12.5% (23% minus 17.5% = 5.5%).* July 1990 - spread 8%

The

Interactive hover

mouse on that RBA webpage

Cash Rate displays the

Cash Rate at 15% in July 1990. * Sept 1990 - spread 9.5%

The

Interactive hover

mouse on that RBA webpage

Cash Rate displays the

Cash Rate at 14% in Sept 1990. * January 1991 - spread 11.5%

The

Interactive hover

mouse on that RBA webpage

Cash Rate displays the

Cash Rate at 12% in Jan 1991. * July 1991 - spread 12.5%

The

Interactive hover

mouse on that RBA webpage

Cash Rate displays the

Cash Rate at 10.5% in July 1991. * June 1992 - spread 16.25% When Messrs. Lowe and Rohling wrote their Discussion Paper, LOAN RATE STICKINESS: THEORY AND EVIDENCE in June 1992 - seemingly on a topic of some significance - the Interactive hover mouse on that RBA webpage Cash Rate Target displays the Cash Rate at 6.5% in June 1992. The table below notes 6.5% Overnight Cash Rate in June 1992. The below RBA Graph 6 'Credit Card Interest Rates' (sourced from Developments in the Card Payments Market - Mar 2015) displays the Standard Credit Cards Purchase Interest Rate @ 23% in June 1992 - a spread of 16.25%. Little wonder Messrs Lowe/Rohling wrote their Discussion Paper highlighting that the Credit Cards Purchase Interest Rate had been markedly sticky or stucky, because the spread had blown out from 12.5% to 16.25% in 11 months because credit card interest rates were 'stuck'. * July 2001 - spread 11.5% The Interactive hover mouse on that RBA webpage Cash Rate displays the Cash Rate at 5% in July 2001. The below RBA Graph 6 'Credit Card Interest Rates' (sourced from Developments in the Card Payments Market - Mar 2015) displays the Standard Credit Cards Purchase Interest Rate @ 16.5% in 1 July 2001, with a spread of 11.5%. * March 2015 - spread 17.25% The Interactive hover mouse on that RBA webpage Cash Rate displays the Cash Rate at 2.25% in March 2015. The below RBA Graph 6 'Credit Card Interest Rates' (sourced from Developments in the Card Payments Market - Mar 2015) displays the Standard Credit Cards Purchase Interest Rate @ 19.5% with a spread of 17.25%. * March 2017 - spread 18.5% The spread between the Overnight Cash Rate of 1.5% pa in March 2017 and the - (i) 'standard cards' Purchase Interest Rate of 20% p.a. is an 18.5% spread; and

(ii)

The highest

Purchase interest rate is 25.9% from "Lombard

Visa Card Classic" evidences a spread of

22.9%.

* July 2019 - spread 19% The spread between the Overnight Cash Rate of 1% pa in July 2019 and the - (i) 'standard cards' Purchase Interest Rate of 20% p.a. is a 19.5% spread; and

(ii)

The highest

Purchase interest rate is 25.9% from "Lombard

Visa Card Classic" evidences a spread of

23.9%.

* Oct 2019 - spread 19.25% The spread between the Overnight Cash Rate of 0.75% pa in Oct. 2019 and the - (i) 'standard cards' Purchase Interest Rate of 20% p.a. is 19.25% spread; and

(ii)

The highest

Purchase interest rate is 25.9% from "Lombard

Visa Card Classic" evidences a spread of

23.9%.

* 20 March 2020 - spread 19.75% The spread between the Overnight Cash Rate of 0.25% pa on 20 March 2020 and the - (i) 'standard cards' Purchase Interest Rate of 20% p.a. is 19.75% spread; and

(ii)

The highest

Purchase interest rate is 25.9% from "Lombard

Visa Card Classic" evidences a spread of

23.9%.

|

|

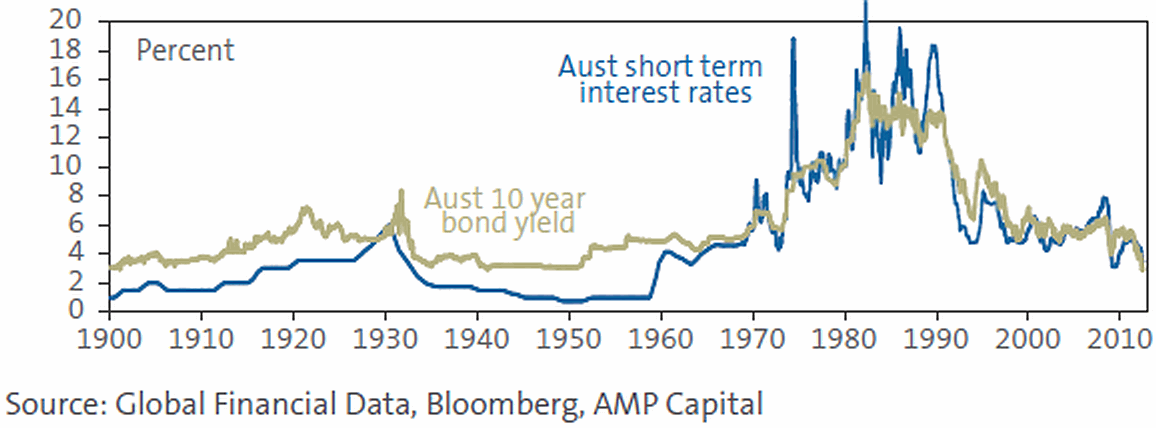

The Writer accepts why Australia's Principal Regulator of the Payments System was comfortable to remove the 18% cap on Credit Card interest rates in April 1985 when "...at the end of June 1985 interest rates were in the range 17.25% to 19%." - below Bloomberg graph. But 31 years later in 2017, how can Australia's Three Financial Services Regulators continue to tolerate Credit Card Issuers - * sourcing funds at 2% circa to lend to Credit Cardholders; and * charging an ave. of 17.22% as applied by ASIC MoneySmart ' Credit card debt clock', particularly when Transactors (67% of Credit Cardholders) that were "Lucky in Life" to become Financially Educated enjoy a Free Ride?The Cash Rate was 1.5% in 2017, but commercial banks cannot fund credit card borrowings exclusively by borrowing from the RBA. Commercial banks need to also use deposited funds, although each of the Four Pillars are holding $200 million circa in standard bank accounts at no interest or 0.1% p.a. interest and charge an ave. of $5 p/m 'account keeping fee', when infrastructure/computer costs to administer bank accounts for 'depositors balances' have plummeted to less than 10% of the cost of legacy systems circa 1990s. How can the Three Financial Services Regulators countenance Credit Card Issuers charging interest on Purchases (after expiry of the Interest Free Period) at 19% circa, and as high as 29.49% for a Cash Advance (using a Latitude Financial Go Mastercard), when Reserve Bank's Copious Publications on Credit Cards (Chapter 8 below), together with detailed written submissions from other agencies such as Treasury’s Submission to Senate Economics References Committee - Aug 2015, acknowledge the likes of the following:

" According to a 2013 RBA survey, only around 30 per cent of credit card users reported that they pay interest on their credit card balances (the ‘Revolvers’)."RBA's Consultation Document titled Executive Summary - Reform of Credit Card Schemes in Australia: RBA's "A Consultation Document" – Dec 2001 notes:

[Above two extracts sourced from "Five extracts that evidence that Financially Savvy Users Don't Pay - some Are Paid" above in this Chapter 5].

The implicit interest margin between the Cash Rate and the 'Standard cards' interest rate for Purchases that is displayed in RBA's Graph 6 "Credit Card Interest Rates" (RHS below) has hovered around 10% (1,000 basis points) since 1991 - 26 years. The margin is presently 17.5% (19% interest rate for Purchases for 'Standard cards' [Graph 6 RHS shortly below] and the 1.5% Cash Rate. That implicit interest margin might possibly be more tolerable if the User Pays Principle applied to all Credit Card usage where all Credit Cardholders paid for their Revolving Lines of Credit according to "usage". But Revolvers (33% of Credit Cardholders) pay all Interest and Penalty Fees Revenue ; such revenue accounts for over 80% of all Credit Card Issuers' Revenue. At the same time, 67% of Credit Cardholders, known as Transactors, have enjoyed a Free Ride 'for years and years and years' , whilst Australia's Principal Regulator of the Payments System and ASIC have "sat on their hands" regarding Usurious Interest Rates and Unconscionable Conduct that have increasingly beset Credit Card Products where Predatory Advertising is patently targeted at Credit Cardholders with low Financial Literacy Capacity.

Extensive Powers And Responsibilities of the Reserve Bank notes: * " The Board has been given the backing of strong regulatory powers, unique among central banks."* "The Reserve Bank is the principal regulator of the payments system through the PSB." Box 2 of Extensive Powers notes: "The Reserve Bank of Australia's - A. powers to gather financial information from ADIs; and B. responsibilities to 'inter alia' "best contribute to.......... the economic prosperity and welfare of the people of Australia",

Chapter 17 (below) includes "Reserve Bank was aware as early as 1992 that deregulation was not going to evidence Credit Card Issuers lowering Credit Card Interest rates when the wholesale cost of funds (Overnight Cash Rate) fell". The Reserve Bank Research Discussion Paper - June 1992: LOAN RATE STICKINESS: THEORY AND EVIDENCE - RBA 1992 (by Philip Lowe and Thomas Rohling) identified excessive Price Stickiness of Credit Cards when the Cash Rate falls, because interest rates charged for Purchases (after the lure of the Interest Free Period) and Cash Advances remained 'stuck' at their existing interest rates. That Discussion Paper which recognised that Credit Card Issuers were not going to pass on interest rate cuts to the interest rates charged for Purchases (after the Interest Free Period) and Cash Advances was published 25 years ago. The wholesale cost of funds (measured by the Cash Rate) has plummeted during that quarter century.

|

|

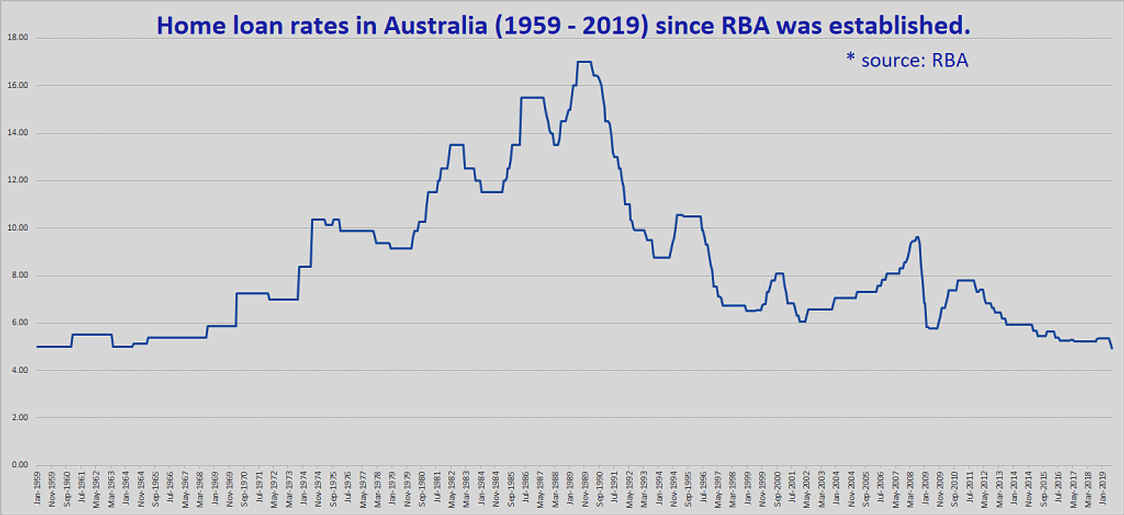

Refer: Standard Variable Home Loan Interest Rates 1959 - 2016 Australia

|

{kind=link}

{kind=link}

History of Interest Rates in Australia - InfoChoice

35 years of Australian interest rates - RateSetter

https://www.rba.gov.au/statistics/historical-data.html

Persistent Revolvers discussed in Chapter 20 below have paid a hefty additional interest burden from removal of the 18% cap, to the material benefit to the 67% of Credit Cardholders that are Transactors that have enjoyed a Free Ride.

One can only ponder whether "Loan Rate Stickiness" is still a concern of the Reserve Bank, but it was in 1992 - at least to the two authors:

The '16.5% Differential' [between the Overnight Cash Rate of 1.5% (as at 27 Dec 2016) and the 18% 'Cap On Credit Card Interest Rates' (for Purchases and Cash Advances)] could be 'locked in'. Whereupon if the Overnight Cash Rate increased to say 3%, the 'Cap On Credit Card Interest Rates' would increase to 19.5% ('16.5% Differential' + 3%).

Requiring Credit Card Issuers and the two Credit Card Payment Schemes to reprice Credit Cards under the User Pays Principle so that all 'Users' pay their way, and do not 'leach off' Australians with poor Financial Literacy, or those that are a prisoner to Compulsive Buying Disorder, would evidence material improvement that government .... expanding on financial literacy programs such as MoneySmart Schools Program".

Imposing a $0.50 'transaction fee' and replacing the lure of up to 55 days Interest Free Period, with a Concessional Interest Rate Period of 1% for up to 50 days, would enable a material reduction in Purchase and Cash Advance interest rates which would benefit Revolvers' infinitely more than more style MoneySmart schools programs.

=====================================================================================

Refer:

Summary Page re Written Questions and the Grounds/Reasons

Grounds/Reasons (one document with 21 Chapters)

Grounds/Reasons (21 separate Chapters)

Written Questions (one document with Written Questions)

Written Questions (Individual Written Questions)