Merchant Service Fee

Westpac website informed that when a Merchant's customers use a MasterCard or Visa Credit Card under the Four-Party Scheme to make a payment, and the Merchant banks with Westpac (ie. Westpac is the Card Acquirer) charges a combined Merchant Service Fee based on volume and rate per card type and is charged as a % of either the net or gross dollar value processed.

If a Credit Cardholder makes a $100 Purchase with its Credit Card, the Merchant would receive $97.23 (approx.) 'same day'.

The remaining $2.77 (approx.) known as the Merchant Service Fee, is divided up:

* $0.50 to Card Acquirer Fee

* $2.00 approx. Interchange Fee would go to the Credit Card Issuer - a flat fee plus a percentage of the purchase price (including taxes) for funding the Merchant 'same day', whilst the Credit Cardholder would not repay the Credit Card Issuer for up to 55 days

* $0.20 approx. On Charged Scheme Fee would go to Visa or MasterCard

* $0.07 (remaining) fee [referred to as a discount rate, an add-on rate, or passthru] would go to the Merchant's bank known as the Card Acquirer for the Card Acquirer's processing and other costs and profit margin.

A Merchant Service Fee also is payable under a Three-Party Scheme to Diners Club or AMEX.

See Fees Levied On The Wholesale Supply Side.

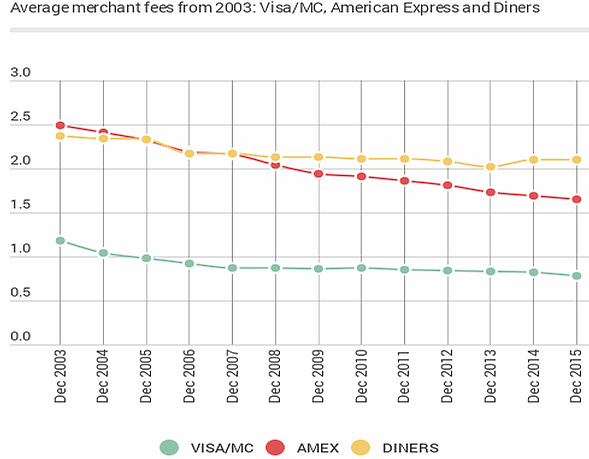

The average merchant service fees for 2013 from RBA report:

See

Cost of Credit Cards to MerchantsMerchant Service Fee Income (RBA Explanatory Notes)

This quarterly return 22KB collects data on income earned from merchants by card schemes and financial institutions that acquire debit, credit or charge card transactions.

Data are collected for the March, June, September and December quarters. The reporting period runs to the last calendar day of the quarter.

Survey respondents are to complete the return in respect of their merchant acquiring activities. The acquirer is the organisation that, under arrangement with and on behalf of an issuer, discharges the obligations owed by that issuer to the relevant cardholder when the cardholder undertakes a transaction via an access point owned/controlled by the acquirer. The arrangement with the issuer may be direct or through a third party.

Amounts should be reported in thousands of Australian dollars, rounded to one decimal place. Definitions of the terms used in the survey are provided below.

| Merchant service fee income received | Total income derived from transaction-based fees charged to merchants for acquiring card transactions, whether collected on an ad valorem or flat basis. Data should reflect transactions involving cards issued to individuals or business, either domestically or abroad. Income from merchants is to be reported net of rebates, concessions and GST. |

|---|---|

| Other acquiring fees received from merchants | Total income from merchants other than merchant service fee income, including annual fees, terminal fees, terminal rentals, monthly fees, joining fees and other fees or associated costs charged to the merchant. Each income item should be allocated to the relevant transaction type (as outlined below) or apportioned across transaction types using an appropriate method – for example, according to the number or value of transactions. |

| Credit and charge transactions | ‘Credit and charge transactions’ refers to general-purpose credit card and charge card transactions that are acquired by the reporting organisation. A general-purpose credit or charge card can be used at many different merchants to make transactions and thus differs from a store card, which can only be used at one merchant or chain of merchants. A credit card enables a cardholder to access a revolving credit facility. The credit card holder can use the card to make transactions up to a pre-arranged limit. A charge card enables a cardholder to access a non-revolving credit facility. Charge cards typically do not have an explicit credit limit. |

| EFTPOS transactions | ‘EFTPOS transactions’ refers to transactions made with debit cards, using the proprietary EFTPOS network, that are acquired by the reporting organisation. A debit card transaction involves a cardholder accessing funds in a deposit account at an authorised deposit-taking institution. |

| Domestic Scheme debit transactions | ‘Domestic Scheme debit transactions’ refers to transactions made with scheme debit cards issued by another domestic issuer, using a scheme network – such as Visa Debit, MasterCard Debit, Maestro or Visa Plus – that are acquired by the reporting organisation. A scheme debit card transaction involves a cardholder accessing funds in a deposit account at an authorised deposit-taking institution. |