|

|

The Reserve Bank had previously 'lined up all the requisite wood ducks' to set Standards for Credit Cards to 'inter alia' reimpose a maximum Purchase interest rate and a maximum Cash Advance interest rate for 'public interest issues' (To Act In The Public Interest)

Chapter 5 and Chapter 17 note inter alia that between 1960 and 1980 the Reserve Bank diligently regulated Australian commercial bank interest rates relying on the below Section 50 of the Banking Act 1959 as amended. Hereunder, the Writer - * explains the three steps for the Reserve Bank to re-impose a Purchase and a Cash Advance maximum interest rate on Credit Cards; and * asserts that two of these steps have been implemented, and the third step has two precedents in setting Standards for Interchange Fees in May 2016 and Surcharge Fees in 2003 and 2016. The RBA -

Back in 2011 when the Writer shared emails with Ms. Sharon van Etten, Public Relations Officer, Media & Public Relations Office, RESERVE BANK, Ms. van Etten's email sent 10 Nov 2011 commented to him:

The Reserve Bank holds Extensive Powers and Responsibilities to All Australians "to best contribute to the economic prosperity and welfare of (ALL) the people of Australia", in particular obligations under Point 3 & 4. of Extensive Powers and Responsibilities).

The below analysis of steps 1. 2. and 3 (listed above) behove that the Reserve Bank to have relied upon - * Division 4, Section 18 of the Payments System Regulation Act 1998 to make 'standards' for payment systems that are "in the public interest"; * Section 50 of the Banking Act 1959 as amended for "Control of interest rates" to, with the approval of the Treasurer, make regulations; and * Section 8 'Meaning of public interest' of the Payments System Regulation Act 1998 in particular "The Reserve Bank may have regard to other matters that it considers are relevant, but is not required to do so", to re-regulate a maximum interest rate on Credit Cards (explained in Chapter 17) after it published LOAN RATE STICKINESS: THEORY AND EVIDENCE (in June 1992 - 25 years ago - written by the present Governor of the Reserve Bank, Phillip Lowe and Thomas Rohling) which established that Credit Card interest rates were 'sticky': · "The rate on credit cards is found to be the most sticky followed by personal loan rates, the housing loan rate and the small business overdraft rate. · In contrast, the rates on personal loans and credit cards do not appear to be more flexible in the deregulated period."

Rationale:

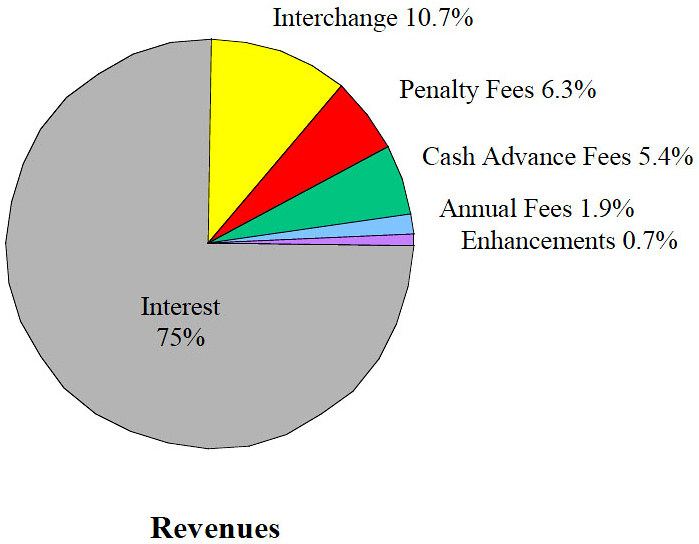

(a) The blue table midway down Chapter 5 establishes that the spread between the Wholesale Cost Of Funds and Standard Credit Card Purchase Interest Rate has widened and widened and widened: * was less than 1% when the 18% cap was removed in April 1985 * was 10% in 2001 * was 18.5% in March 2017; AND (b) Persistent Revolvers that hold 12.58% circa of the 16.686 million Credit Cards held by Credit Cardholders in Australia often with Level 1 or less Financial Literacy Capacity] have suffered Extreme Financial And Emotional Distress and contributed 80% circa of Interest and Penalty Fees Revenue to Credit Card Issuers of which 80% of all Revenues to Credit Card Issuers from Credit Card Products is Interest and Penalty Fees Revenue; ipso facto Persistent Revolvers that hold only 12.58% circa of the 16.8m Credit Cards held by Credit Cardholders are paying 64% of all Revenues from Credit Card Products - get that, 12.58% circa of Credit Cards are paying 64% of all Revenues and the Reserve Bank is aware of detailed written reports by the Productivity Commission, ABS and ASIC (that date back to 2006) re the material disparity in Financial Literacy Capacity across Credit Cardholders (Chapter 1).

Below is an extract from Media Release "Designation of Credit Card Schemes in Australia" issued 12 April 2001:

"The Bank will now proceed to establish, in the public interest, standards for the setting of interchange fees and a regime for access to the credit card systems. However, the standards will not cover the setting of credit card fees and charges to cardholders and merchants, or interest rates on credit card borrowings." Australia's central bank, with a Board that has been given the backing of strong regulatory powers, unique among central banks, could have Determined Standards to re-impose a maximum interest rate on Credit Cards, or a maximum interest rate for Purchases and a maximum interest rate for Cash Advance, at any time that it wanted to. The below Media Release - Reform of Credit Card Schemes in Australia – Access Regime - DateNumber 2004-02 seems to inform 'inter alia' that the ACCC no longer had any obligations to monitor Credit Card Issuers because following Designation on 12 April 2001 and subsequently imposing an Access Regime on 23 Feb 2004 on each of the three designated credit card schemes in Australia Visa, MasterCard and Bankcard meant that the RBA is solely responsible to the behaviour of these three Credit Card Issuers:

Below is an extract from "Access Regimes" in Chapter 7. CONCLUSION AND FINAL REFORM MEASURES dated Aug 2002:

The access regime provides that any authorised deposit-taking institution in Australia, including the new class of specialist credit card institutions, is eligible to apply to participate in the designated credit card schemes in Australia. However, in response to comments received, the Reserve Bank has made some changes to the drafting to clarify the rights and obligations of the schemes and their members, and to simplify the application of the access regime. The access regime now makes explicit that a designated credit card scheme is free to impose its own business and operational criteria in assessing applications to participate in its scheme. However, it must not discriminate between specialist credit card institutions as a class and other authorised deposit-taking institutions as a class in relation to any of these criteria, or to the rights and obligations of participants in the scheme. Each scheme must also publish the criteria it imposes in assessing applications for participation in Australia. This replaces the requirement in the draft access regime that the schemes publish their rules governing eligibility for participation and the terms of participation. The requirement that the schemes give prior notice to the Reserve Bank of any changes to the rules governing eligibility for participation has been removed. The access regime prohibits the imposition of any restrictions or form of penalties on participants seeking to specialise in acquiring. APRA has released its draft prudential standards on risk management of credit card activities that will apply to authorised deposit-taking institutions, including the new class of specialist credit card institutions. The draft prudential standards and authorisation guidelines for specialist credit card institutions are given in Attachment 6.See: ATTACHMENT 1: EXTRACTS FROM PAYMENT SYSTEMS (REGULATION) ACT 1998

|

|

|

|

{kind=link}