An Interchange Fee is charged by the Card Issuer to the Merchant for putting the Merchant in funds 'same day' of a Purchase by a Credit Cardholder.

(ii)

paid to the Card Issuer to cover -

a)

funding cost up to 55 days;

b)

electronic hardware and software handling costs;

c)

fraud and bad debt costs; and

d)

the risk involved in approving the payment.

A typical

Credit Card or

Debit Card

transaction involves

Four Parties:

(i)

Credit

Cardholder,

(ii)

Credit

Cardholder's

Bank (known as the 'Credit Card

Issuer'),

(iii)

Merchant and

(iv)

Merchant's bank (known as the 'Acquirer

Bank or Card Acquirer'

Interchange Fees are fees that the Credit Card Issuer charges the Merchant's bank (the Card Acquirer Bank) for each Credit Card or Debit Card transaction accepted by a Merchant. The Interchange Fee applies when a customer pays for products using a card issued by one institution, but the Merchant uses another institution to process its card payments. The Interchange Fee comprises a significant part of the Merchant Service Fee charged by Card Acquirer Bank to their merchants.

In 1993, MasterCard and Visa introduced domestic interchange fees in Australia determined collectively by their Australian members. Australian credit laws were amended, inter alia, to allow Credit Card Issuers to charge annual fees on Credit Cards and Merchants to charge different prices for accepting different payment instruments.

8 In August 2002, the PSB decided that from July 2003 the schemes would be subject to a standard which set an interchange fee benchmark for each scheme and increased transparency of these fees. The benchmark was based on the average costs of the issuers of each scheme. Since November 2006, there has been a common cost-based average interchange fee benchmark of 50 basis points for both MasterCard and Visa.The Standard on interchange fees, came into effect in July 2003.

4Interchange Fees are levied on the Wholesale Supply Side that are set by Credit Card Schemes such as MasterCard, Visa and eftpos that require payments from the Merchant's bank, known as the Card Acquirer, to the Credit Card Issuer on every transaction - see Why does the RBA regulate interchange fees? which includes:

"The tendency for interchange rates to rise to high levels is most apparent in unregulated jurisdictions like the United States where credit card interchange rates in the MasterCard system are as high as 3.25 per cent plus 10 cents, implying that – after scheme fees and acquirer margin – some merchants may pay over 3½ per cent in merchant service fees for high rewards cards."

"What are the RBA's new interchange standards?

If a Credit Cardholder makes a $100 Purchase with its Credit Card, the Merchant would receive approximately $97.23 'same day'.

The remaining $2.77, known as the Merchant Service Fee, gets divided up:

* $0.50 to Card Acquirer

* $2.00 approx. Interchange Fee would go to the Credit Card Issuer - a flat fee plus a percentage of the purchase price (including taxes)

* $0.20 approx. On Charged Scheme Fee would go to Visa or MasterCard

* $0.07 (remaining) fee [referred to as a discount rate, an add-on rate, or passthru] would go to the Merchant's bank known as the Card Acquirer.

Interchange fees vary depending on:

· The brand of the card, e.g. MasterCard ®

· Where the card was issued, e.g. Australia or overseas

· How the transaction was processed, e.g. card present or card not present

· Card product type, e.g. premium card, business card

· Merchant industry type, e.g. Merchant Category Code

In more recent years, however, the structure of credit card pricing and product offerings have changed. Credit Card Payment Schemes have found ways, within the bounds of the Reserve Bank’s regulation, to charge a Merchant Service Fee. Hence, a credit card system with high Interchange Fees may result in Merchants effectively subsidising Cardholders who use that system, unless Merchants are able to pass these costs on to Cardholders.

Australian Retailers Association - Submission to RBA - Credit Card Schemes in Australia sourced on the RBA website (overtly marked Confidential) was highly critical of the RBA's inept and complicit role in Credit Card Issuers imposing an Interchange Fee upon Merchants when the contract is between the Card Issuer and the Cardholder.

{kind=link}

Below are pertinent extracts from Australian Retailers Association - Submission to RBA dated 2001:

"1.1 Confidentiality

The contents of this report are confidential. Data relating to the business of the Australian Retailers Association (ARA) or its members and contained within this submission is confidential and is not to be released into the public domain."

"

Executive SummaryThe thrust of this paper by the Australian Retailers Association (ARA) can be summarised by a quotation from the RBA / ACCC paper ‘Debit And Credit Card Schemes in Australia – A Study of Interchange Fees And Access’; Page 52 states:

“ Simple economics shows that when a service is under priced, it tends to be over-used”.

This statement in our view distills the essence of credit card pricing and use both here and internationally. From inception, the Merchant community has been paying a disproportionate share of the cost of credit cards. Consumers have been paying less than the true cost of services provided to them by Credit Card Issuers. This we believe was the result of credit cards at inception not having a viable economic rationale for the consumer and Credit Card Issuers and Acquirers structuring the product economics in order to enhance take up. Had credit cards been priced in a competitive environment, then it is highly likely that they would not have gained such a major global presence.

The global Merchant community has, made a major contribution to the revenues and profits of Credit Card Issuers and Acquirers. Credit card services have been overpriced to Merchants and under priced to Cardholders.

Our paper will argue that:

1. interchange between Card Issuers and Card Acquirers should be completely abolished and replaced with activity bases fees or fees for service;

2. credit card interchange is passed on to Merchants via the Merchant Service Fee. Our own experiences have seen interchange put to us as a ‘floor’ to the Merchant service fee rate advanced by Acquirers;

3. Merchant Service Fees should be completely abolished and replaced with market negotiated activity based fees;

4. the current credit card scheme no surcharging or non-discrimination rule be abolished across all card types, and that Merchants and the market not be restricted (subject to competition law) from setting their own pricing policies.

We would encourage the RBA to take this opportunity to address a major inequity in the Australian payments environment."

Below are pertinent arguments:

Argument 1 - The risk of extending credit to cardholders:

Argument 2 - The cost of the Issuer processing the transaction

"It is therefore reasonable for the Issuer to seek cost recovery and a competitive margin for this service – from the cardholder with whom a relationship exists and for whom a service is being performed. Such a fee for service should reflect the exact nature of the services offered by the Issuer to the cardholder.

The fee should be ‘internal’ to that relationship.

We would therefore argue that the cost of the Issuer processing a credit card transaction does not warrant an Interchange Fee being levied to the Card Acquirer and ultimately passed on to the Merchant via Merchant Service Fee. We would cite a number of reasons in support of this:

The Issuer is acting on behalf of their Cardholder in processing a credit card transaction. The Cardholder is instructing the Issuer to perform the transaction;

It is the Cardholder who is seeking to effect payment to the Merchant via a credit card. It is at the Cardholder's discretion to select a payment method. The Cardholder initiates the entire credit card processing cycle and should bear the costs of the party (the Issuer) acting directly on their behalf;"

Argument 3 - Costs associated with the interest free period attached to credit cards

"We agree that the interest free period encourages potential Cardholders to take up card products and existing cardholders to utilise their cards. It is very useful and beneficial for consumers to delay payment for goods and services for some 55 days. We would point out that certain credit cards have zero interest free days, yet still attract identical interchange and Merchant Service Fee levels.

The interest free period is again, a Card Issuer / card holder relationship cost.

The introduction and length of interest free periods was determined by credit Card Issuers to facilitate credit card take up and usage – both revenue generating activities for themselves. We find it implausible that Issuers sought to introduce interest free periods for any reason other than to increase their own income levels."

Argument 4 - The cost associated with providing a payment guarantee to merchants

"We would expressly reject that any credit losses resulting to the Issuer from this process (card holders lodging bogus charge backs and then not paying when proof of purchase is provided), should be passed back to the Merchant via Merchant Service Fee that has interchange as a major cost component. This is an Issuer / Cardholder credit matter."

The above submission contends that 'ad valorem' Merchant Service Fees "should be completely abolished and replaced with market negotiated activity based fees", seemingly based on the User Pays Principle for all enjoying such a Credit Card Line Of Credit.

Given that Credit Card Issuers under the Four-Party Scheme receive an Interchange Fee from which they may fund rewards programs, they have an incentive to issue and promote cards that attract a higher Interchange Fee for each transaction. In line with this, the Four-Party Schemes have an incentive to put in place an Interchange Fee pricing structure that encourages financial institutions to issue and promote their Credit Cards; while the card scheme does not directly generate revenue from Interchange Fees, it charges fees to Card Issuers and Acquirer Banks based on the volume of credit card transactions.

In contrast to Four-Party Schemes, there are no Interchange Fees in Three-Party Schemes because the card scheme itself is the sole acquirer for transactions on its cards, and typically also the sole issuer. Instead, rewards programs in this model are funded directly through fees paid by the Merchant.

Hence, the higher the average Merchant Service Fee for a Three-Party Scheme, the more generous the rewards that scheme is able to offer. At the same time, a high Merchant Service Fee tends to discourage Merchants from accepting Credit Cards for payments. To some extent this acts as a competitive discipline on Merchant Service Fees, although some Merchants may feel that declining to accept a particular card is not a realistic option.

Regardless of the model, the costs of funding rewards for Cardholders has been borne by Merchants in the first instance through higher Merchant Service Fees – either through the pass-through of higher Interchange Fees (for four-party schemes) or directly (for three-party schemes). Moreover, card schemes in many credit card markets have rules in place that prevent Merchants from passing their card acceptance costs directly through to cardholders in increase incentives for Card Issuers to promote particular products within their suite of offerings; Card Issuers have responded, particularly through new strategies focusing on the premium segment of the market. Some of these new pricing strategies have focused on upgrading existing cardholders – offering platinum cards with additional benefits or more generous rewards for no additional annual fee – which has the effect of generating increased interchange revenue for the issuer every time a customer uses their card. There have also been a number of merchant-branded platinum cards that have entered the market in recent years. Separately, American Express has modified its product offerings, entering into arrangements with major banks to issue ‘companion’ American Express cards with MasterCard or Visa products.

Some of these recent developments have changed the effective price to some Cardholders of a credit card transaction, and correspondingly added to costs on the acquiring side of the market. Merchant Service Fees have remained relatively stable in the past few years, though these recent developments could put upward pressure on some fees if they continue.

Interchange Fees

Interchange Fees are often a feature of Four-Party Schemes (Figure 2.1), which include the debit and credit schemes operated by eftpos, MasterCard and Visa. Card Acquirers, the Merchants’ providers of payment acceptance facilities, pay Interchange Fees to Card Issuers, the Cardholders’ payment card providers. The fees enable issuers to recover the cost of processing transactions. Payment schemes can also set Interchange Fees to incentivise financial institutions to issue their payment cards. Issuers can incentivise Cardholders to use their cards by passing on a proportion of Interchange Fees as reward points, interest-free periods or other benefits.

Figure 2.1: Simplified example of a Four-Party Scheme

Payment schemes designated by the RBA (eftpos, MasterCard and Visa) ensure that the weighted-average value of their Interchange Fees complies with caps established by the RBA. The caps are 0.5 per cent of the value of transactions for credit card schemes and 12 cents per transaction for Debit Card schemes. The RBA established these caps following a cost-based benchmarking exercise.

The RBA caps Interchange Fees for a number of reasons:

- Price signals are not efficient in four-party payment schemes, which can result in competition and paradoxically lead to higher prices. Merchants generally exhibit low price sensitivity to Merchant Service Fees for widely used payment schemes, such as those operated by eftpos, Visa and MasterCard. If merchants do not accept these cards, they may lose sales to the majority of merchants that do. In comparison, cardholders are often more price sensitive. They have access to a range of payment schemes, and will respond to incentives like reward points when determining which scheme to use. Payment schemes therefore have an incentive to set high Interchange Fees, which issuers can use to offer reward points for cardholders.

- Interchange fees act like price floors for Merchant Service Fees. To break even, at a minimum, acquirers set Merchant Service Fees at the cost of Interchange Fees, plus the cost of processing transactions.

- Cross-subsidisation will occur if merchants do not recover Merchant Service Fees through customer surcharges. The cost of absorbing Merchant Service Fees would be reflected in higher prices for goods and services. This would result in cross subsidisation from customers using low-cost payment mechanisms, such as eftpos and cash, to those using high-cost payment schemes – an inefficient outcome.

Amex and Diners Club operate three-party payment schemes. In three-party schemes, the scheme takes the role of issuer and acquirer. As no Interchange Fees are involved, these schemes are not covered by Interchange Fee regulation. Issues with the regulation of a variation of three-party schemes, known as companion cards, are discussed below.

Interchange fee is a term used in the payment card industry to describe a fee paid between banks for the acceptance of card based transactions. Usually it is a fee that a merchant's bank (the "acquiring bank") pays a customer's bank (the "issuing bank") however there are instances where the Interchange Fee is paid from the issuer to acquirer, often called reverse interchange.

In a credit card or Debit Card transaction, the card-issuing bank in a payment transaction deducts the Interchange Fee from the amount it pays the acquiring bank that handles a credit or Debit Card transaction for a merchant. The acquiring bank then pays the merchant the amount of the transaction minus both the Interchange Fee and an additional, usually smaller, fee for the acquiring bank or ISO, which is often referred to as a discount rate, an add-on rate, or passthru. For cash withdrawal transactions at ATMs, however, the fees are paid by the card-issuing bank to the acquiring bank (for the maintenance of the machine).

These fees are set by the credit card networks,[1] and are the largest component of the various fees that most merchants pay for the privilege of accepting credit cards, representing 70% to 90% of these fees by some estimates, although larger merchants typically pay less as a percentage. Interchange fees have a complex pricing structure, which is based on the card brand, regions or jurisdictions, the type of credit or Debit Card, the type and size of the accepting merchant, and the type of transaction (e.g. online, in-store, phone order, whether the card is present for the transaction, etc.). Further complicating the rate schedules, Interchange Fees are typically a flat fee plus a percentage of the total purchase price (including taxes). In the United States, the fee averages approximately 2% of transaction value.[2]

In recent years,

Interchange Fees have become a controversial

issue, the subject of regulatory and antitrust investigations. Many

large merchants such as Wal-Mart have the ability to negotiate fee

prices,[3]

and while some merchants prefer cash or PIN-based

Debit Cards, most

believe they cannot realistically refuse to accept the major card

network-branded cards. This holds true even when their

interchange-driven fees exceed their profit margins.[4]

Some countries, such as Australia, have established significantly

lower Interchange Fees, although according to a U.S. Government

Accountability study, the savings enjoyed by merchants were not

passed along to consumers.[5]

The fees are also the subject of several ongoing lawsuits in the

United States.

Review of Card Payments Regulation - 2. The Bank's Card System Reforms - Issues Paper - March 2015

"However, the Review identified an opportunity to step back from direct regulation of interchange fees, predicated on there being a sufficiently strong competitive environment to prevent interchange fees rising over time from their regulated levels. Two approaches to addressing this risk were identified:

-

Industry could strengthen competition through measures which included: enhancement of the eftpos system to allow it to compete more effectively with the international card schemes and the development of an alternative system for online payments; further modifications to the honour-all-cards rules to allow merchants to make separate acceptance decisions for any card for which there was a separate interchange fee; and more transparent scheme fees.

-

Four-party schemes could directly address the Board's concerns that interchange fees might rise by providing voluntary undertakings that the weighted average of credit card interchange fees would not rise above 0.5 per cent.

The Board indicated that, if industry was not able to make sufficient progress on these, interchange regulation would be retained and the benchmark for credit card interchange fees could be reduced to 0.3 per cent. " are incentive programs operated by Credit Card Issuers where a percentage of the amount spent by a Credit Cardholder is paid back to the Credit Cardholder by means of points earned. Many Credit Card Issuers run programs to encourage use of their Credit Card Products where the Credit Cardholder earns loyalty points, often referred to as Reward Points, frequent flyer miles or a monetary payment.

Credit Cards that offer the highest Rewards Programs charge the highest Interchange Fees and charge the highest Annual Fees which are attractive to small and large companies, as well as sole traders, that can charge Annual Fees as a legitimate tax deduction. Rewards under Rewards Programs are not assessed as taxable income by the ATO.

The former is a fee for performing (ii) a) to d) at top of page. The latter is a lure to entice Credit Cardholders to make Purchases with their Credit Card/s.

RBA's The Personal Credit Card Market in Australia: Pricing over the Past Decade - March 2012 noted:

"In four-party card schemes (such as MasterCard and Visa), rewards programs are, for the most part, funded by interchange fees."

The following statement is from the Reserve Bank's Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - August 2015

"The rewards programs offered by credit card issuers are due in large part to the existence of interchange fees."

Interchange Fees and Transparency of Card Payments - 2015-16 Review of Card Payments Regulation.

"Issues Paper" dated March 2015 "Review of Card Payments Regulation 3. Developments in the Card Payments Market" includes 15 graphs which 'prima facie' evidences that the Reserve Bank enjoys virtually unlimited access to data from MasterCard and Visa Four Party Scheme Providers.

|

Below RBA Graph No 8 (as at March 2015) evidences the substantial range of Interchange Fees Categories: * MasterCard - 18 Categories * Visa - 23 Categories |

|

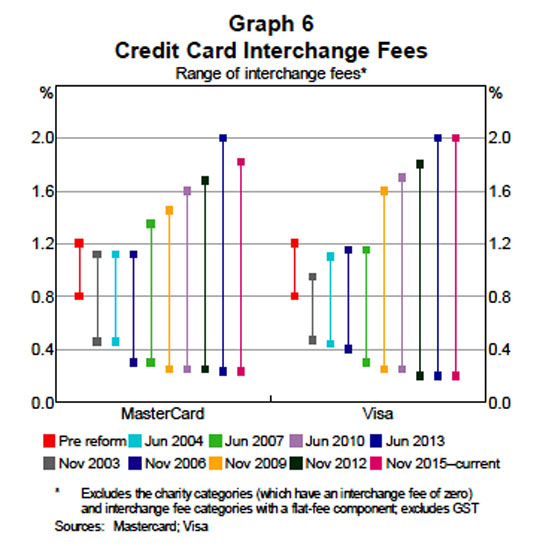

Below RBA Graph No 6 (as at March 2015) evidences the substantial range of Interchange Fees from Nov 2015: * MasterCard - from as low as a quarter of one percent up to 1.75 percent fee * Visa - from as low as a fifth of one percent up to 2 percent fee |

See Cost of Credit Cards to Merchants, Fees Levied On The Wholesale Supply Side and Two-Sided Market