|

| |

Defined Terms and Documents

Labyrinth of

‘Concealed Spiders’ or

Unconscionable Credit Card Advertising

or Nine Examples Of

Predatory Advertising

means:

1.

Quotes from reputable authorities about unconscionable advertising of Credit Cards by

Credit Card Issuers. Those 'reputable authorities' would be adept at identifying examples of

patent misrepresentation (eg

Example 4 below),

confusing fees and charges and a lack of transparency of costs.

2.

The Writer's

submission to the RBA on CD dated 8 Dec 2011 set out in

Attachment 'A'

of that submission

evidence of -

(A)

the

enormous variances in interest costs on

Unsecured Personal Loans

(currently

as low as 14.01%

Comparison Rate from

Westpac) up to the

Usurious Unsecured Personal Loan Interest Rates Charged On

Many Credit Cards of the Four Pillars eg.

CBA Platinum Card 20.24% on

Purchases and

21.24% on

Cash Advances and an

annual fee of $249. A few Credit Cards

offer 'loyalty reward points' as high as

3 points for

every $1 spent where the annual fee (often paid by the employer or as a tax

deduction) is very high; and

(B) mischievous and contrived

advertising of some

Credit Card Products

by too many

Credit Card Issuers intended to

mislead prospective

Credit Cardholders

with

'level 1' and 'level 2'

Financial Literacy which constitutes

Numeracy And Literacy Discrimination

and

violates the ACCC's definition of

Unconscionable Conduct

Below are

Nine Examples of

Unconscionable Conduct by

Predatory Advertising of some

Credit Cards

that the Writer commenced in 2018:

|

* Click on:

Example 1 -

Unconscionable Conduct - St George Visa Card

Example 1

notes that if

a

St George Visa Gold

Cardholder

does not pay 100% of its

Closing Balance

by the

Payment Due Date, the

Cardholder

is charged interest at a

Usurious Interest Rate

of

20% -

+ on all its

Previous Month's Purchases

(from the date of each

Purchase); and

+

forfeited its Interest Free Period

entitlement for the subsequent two months.

Therefore the

Cardholder

enjoys no

Interest Free Period

for three months even if s/he paid only $1 less than their

Closing Balance

or paid their

Closing Balance

one day after

their

Payment Due Date.

Summary information in St George Bank's monthly credit card statement

deliberately seeks to deceive level 1 and level 2

Financial Literacy

Credit Cardholders

into paying only the 2% 'Minimum Payment' which

immediately triggers the above described interest rate of 20% on all

Purchases

for three consecutive months.

Below

is an extract from the bottom of page 2 of St. George Bank's

"Conditions of Use - Credit Guide

(Effective: 20 May 2014).

62 pages of the 64 pages are in tiny Arial 9 font.

“……We

strongly recommend that you read this booklet carefully and retain it for your

future reference. If you do not understand any part of it, please contact our

staff on 13 33 30. They will be happy to explain any matter for you.”

The

Writer

defies anybody to 'carefully' read and understand the

"Conditions of Use - Credit Guide

[64 pages] (in Arial 8 font) "...read

this booklet carefully".

Requiring each

Cardholder

to read 64 pages of complex and

detailed legal clauses is Unconscionable Conduct when the key

information of the real costs

and real benefits can be set out in a dozen bullet points on a single page.

As

defined by the ACCC,

Unconscionable Conduct notes

'inter alia' under

'How to avoid engaging in unconscionable

conduct':

"do not exploit the other party when

negotiating the terms of an agreement or

contract"

"make sure your contracts are thorough,

easy to understand, not too lengthy and

do not include harsh, unfair or

oppressive terms"

"ensure you have clearly disclosed

important or

unusual terms or conditions

of an agreement"

Unconscionable Conduct notes that

the

Australian consumer law – unfair contract terms

(new provisions since 1 July 2010):

"In determining whether a term of a consumer

contract is unfair a court must take into account the extent to which

the term is transparent (that is, expressed in reasonably plain

language, legible, presented clearly and readily available to all

parties), and the contract as a whole."

In

the afore-mentioned

Example 1 -

Unconscionable Conduct - St George Visa Card,

forfeiting the

Interest Free Period

for three consecutive months due to not paying the entire

Closing Balance

by the

Payment Due Date

was not

transparent

to the

Credit Cardholder because

that penalty was not

"expressed in reasonably plain language, legible, presented clearly and readily

available to all parties". |

|

*

Click on:

Example 2 - Unconscionable Conduct - Coles 'No Annual Fee MasterCard' and

Coles

'Rewards

MasterCard'

Example 2

notes that if

a Coles Rewards MasterCard

Cardholder

does not pay 100% of its

Closing Balance

by the

Payment Due Date, the

Cardholder

is charged interest at a

Usurious Interest Rate

of 19.99% p.a.

on all its

Previous Month's Purchases

(from the date of each

Purchase) and also for the

subsequent two months,

because the

Cardholder

forfeits its Interest Free Period

entitlement for another two months.

Hence, the

Cardholder

enjoys no

Interest Free Period

for three consecutive months even if s/he paid only $1 less than his

Closing Balance

or paid his

Closing Balance

one day after

his/her

Payment Due Date.

Summary information in Coles' monthly credit card statement

deliberately seeks to deceive level 1 and level 2

Financial Literacy

Credit Cardholders

into paying only the 2% 'Minimum Monthly Payment' which

immediately triggers the above described interest rate of 19.99% on all

Purchases

for three months.

Coles "Contract Documents and Credit Guide"

[72 pages] for its two MasterCards (administered by GE Money) notes

at the top of page 3:

We

strongly recommend that you read these

Conditions of Use and

the Coles MasterCard Financial

Table carefully and ensure

that any additional cardholder also does so. If you have

any questions please contact us.

The Writer defies anybody to read the "Contract Documents and Credit Guide"

[72 pages] "...carefully and ensure

that any additional cardholder also does so."

Requiring each

Cardholder

to read 72 pages of complex and

detailed legal clauses is Unconscionable Conduct when the key

information of the real costs

and real benefits can be set out in a dozen bullet points on a single page.

In

the afore-mentioned

Example 2 - Unconscionable Conduct - Coles 'No Annual Fee MasterCard' and

Coles

'Rewards

MasterCard',

forfeiting the

Interest Free Period

for three months due to not paying the entire

Closing Balance

by the

Payment Due Date

was not

transparent

to the

Credit Cardholder because

that penalty was not

"expressed in reasonably plain language, legible, presented clearly and readily

available to all parties".

As

defined by the ACCC,

Unconscionable Conduct notes

'inter alia' under

'How to avoid engaging in unconscionable

conduct':

"make sure your contracts are thorough,

easy to understand, not too lengthy and

do not include harsh, unfair or

oppressive terms"

"ensure you have clearly disclosed

important or

unusual terms or conditions

of an agreement"

|

|

*

Click on:

Example 3

-

Unconscionable Conduct -

ANZ's 'First Visa Card' and 'Low Interest Visa Card'

ANZ's advertising of its 'First Card' and 'Low Interest Card' seeks to mislead

prospective new

Cardholders, particularly

Financially Uneducated And Vulnerable Australians,

that if they pay their

'Closing Balance'

(as defined on page 65 of its 98 pages

"ANZ

Credit Cards - CONDITIONS OF USE | 19.09.2014 CONSUMER

CREDIT CARDS")

in tiny Arial 9 font that

any prospective new 'First Visa Card'

or 'Low Interest Visa Card'

Credit Cardholder would

enjoy "Up

to 44 days interest free on purchases3. as asserted in

its webpage at 'Features and benefits'. But that is

not the case.

ANZ First Card offers 0% p.a. interest rate for initial 16 months asserting a savings of

$2,001 on a $8,000

Balance Transfer.

What

is not explained in the ANZ offer documents (5 pages posted to the Writer's home

address) is

that -

A. the only

way to achieve the material savings of $2,001 in interest

costs on an $8,000 Balance Transfer is to

NOT make any Purchases

during the initial 16 months; making

Purchases is the fundamental

purpose of applying for a Credit Card. If any

Purchases are made whilst ever any part of the

Balance Transfer amount @ 0% interest for 16 months remains unpaid, then interest is charged (at the below

interest rates) from the date

of each Purchase (with no

Interest Free Period

entitlement):

* "First Card" @

19.74% p.a.

* "Low Rate Card"

@ 13.49% p.a; and

B if a

Cardholder makes any

Purchases and does not repay

the Balance Transfer amount 'in toto' he/she pays interest on a

"First Card" @

19.74% p.a. on all Purchases during that month from the date of each

Purchase.

In addition,

s/he forfeits

the Interest Free Period for the subsequent two months, whereupon

a "First Card" Cardholder continues to

pay interest at the Usurious Interest Rate

of 19.74% p.a.

for an additional two months until his/her

Interest Free Period is re-installed - a

total of three months interest on all

Purchases @ 19.74%

p.a. from the date of each

Purchase.

ANZ recognizes (on

page 10

of its

98 pages booklet titled "ANZ

Credit Cards - CONDITIONS OF USE | 19.09.2014 CONSUMER

CREDIT CARDS") that it has misled many new

Cardholders, which includes

its

First Visa Card Low annual fee $30, into believing that they

would enjoy, with regard to the

First Visa Card,

"Up

to 44 interest free days on purchases3"

when, in fact,

First Visa

Cardholders

are charged at the Purchase interest rate of

19.74% pa from the date of each

Purchase. This acknowledgement of a

misconception

by ANZ is

reprinted in yellow

background immediately below

and evidenced in detail further below in this page:

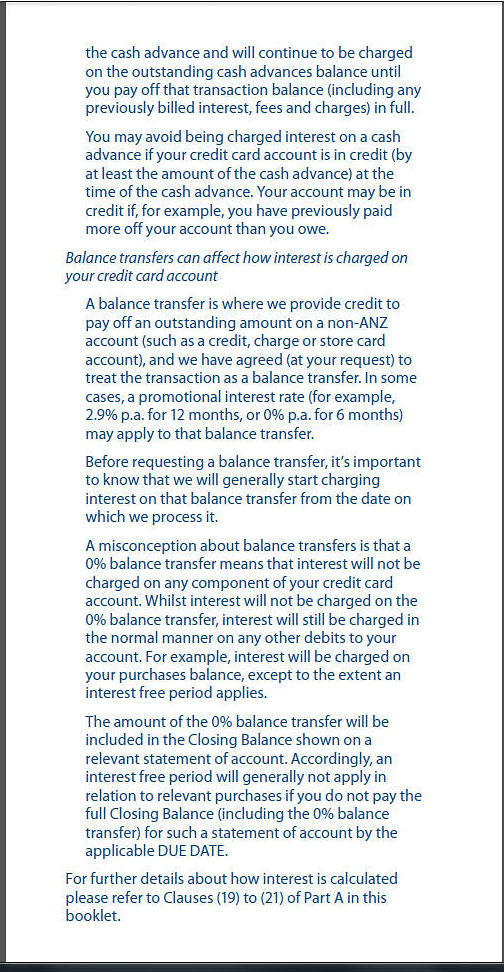

"A

misconception

about

balance

transfers

is that

a

0% balance

transfer

means

that interest

will

not

be charged

on

any

component

of

your

credit

card

account.

Whilst

interest

will

not

be

charged

on

the

0% balance

transfer,

interest

will

still

be

charged

in the

normal

manner

on

any

other

debits

to your

account. For

example,

interest

will

be

charged

on

your

purchases

balance,

except

to the

extent

an interest

free

period

applies."

The

amount of the

0%

balance

transfer

will

be included

in the

Closing

Balance

shown

on

a relevant

statement

of

account. Accordingly, an interest

free

period

will

generally

not

apply

in relation

to relevant

purchases

if

you

do

not

pay

the

full

Closing

Balance

(including

the

0%

balance transfer)

for

such

a

statement

of account

by the applicable

DUE

DATE.

Below is clause 3 under 'Important information' from the below ANZ First

Card webpage:

3.

Interest free periods on the purchases do not apply if you do

not pay your Closing Balance (or, if applicable, your 'Closing

Balance' less Instalment Plan and Buy Now Pay later plan

balances) shown on each statement of account in full by the

applicable due date. Payments to your account are applied in the

order set out in the

ANZ Credit Cards Conditions of Use.

ANZ has commenced the words

Closing Balance

with a capital letter which

constitutes a 'Defined Term' or 'Definition'.

ANZ has not provided a definition of

Closing Balance

in its below

extracted webpage advertising its

First Visa Card Low annual fee $30.

ANZ provides the

below definition of 'Closing Balance' on page 65 of its

100 pages "ANZ

Credit Cards - CONDITIONS OF USE | 19.09.2014 CONSUMER

CREDIT CARDS". (Page 65 commences 48

'Definitions' under heading 'Meaning of words'):

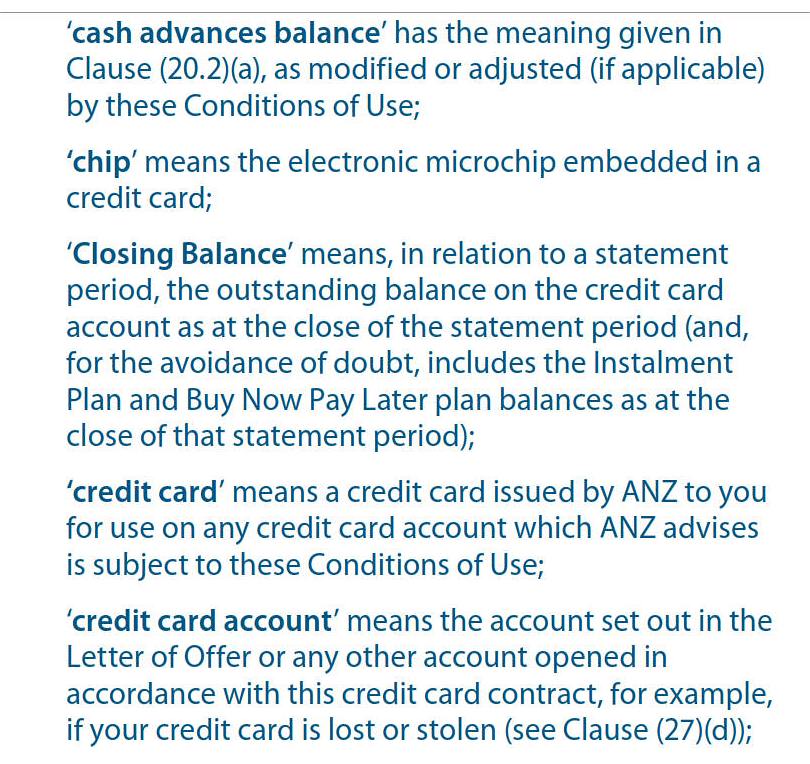

‘Closing

Balance’

means,

in

relation

to a

statement

period,

the

outstanding

balance

on the

credit

card

account

as at the

close

of

the

statement

period

(and,

for the

avoidance

of

doubt,

includes

the

Instalment

Plan

and

Buy

Now

Pay

Later

plan

balances

as at the

close

of

that

statement

period);

Significantly, ANZ's above 'Definition' of

Closing Balance

does NOT include 'the amount of any

0% balance transfer' as a part of the

Closing Balance which

materially flaws ANZ reliance upon

page 10 of

"ANZ Credit

Cards - CONDITIONS OF USE | 19.09.2014 CONSUMER CREDIT CARDS" [100 pgs] as part

of "Important things to know about using your ANZ credit card - Balance

transfers can affect how interest is charged on your credit card account"

which includes:

"A

misconception

about

balance

transfers

is that

a

0% balance

transfer

means

that interest

will

not

be charged

on

any

component

of

your

credit

card

account.

Whilst

interest

will

not

be

charged

on

the

0% balance

transfer,

interest

will

still

be

charged

in the

normal

manner

on

any

other

debits

to your

account. For

example,

interest

will

be

charged

on

your

purchases

balance,

except

to the

extent

an interest

free

period

applies."

The

amount of the

0%

balance

transfer

will

be included

in the

Closing

Balance

shown

on

a relevant

statement

of

account. Accordingly, an interest

free

period

will

generally

not

apply

in relation

to relevant

purchases

if

you

do

not

pay

the

full

Closing

Balance

(including

the

0%

balance transfer)

for

such

a

statement

of account

by the applicable

DUE

DATE.

Having regard to the afore-mentioned inconsistencies about what indebtedness

constitutes the

Closing Balance, any prospective

Cardholder of an ANZ First Visa Card is entitled to

believe that if it pays the

Closing Balance as defined above that it

would

enjoy "Up

to 44 days interest free on purchases3. as asserted in

its webpage at 'Features and benefits' below. But that is

not the case.

Little wonder that ANZ notes

"A misconception about balance transfers is that a 0% balance transfer means that interest will not be charged on any component of your credit card

account because ANZ has advertised that

"Up

to 44 interest free days on purchases3

if the Closing Balance

is paid by the Due Date.

ANZ has been mischievous in its

Key

Facts Sheet

for

its First Visa Card

whereupon too many new customers with a

Balance Transfer

believed that they would enjoy an

Interest Free Period

on

Purchases

provided they have paid their

Closing Balance

(defined above)

by the

Due Date.

ANZ

has breached its obligations under

Regulation 28LFA

of the

National Consumer Credit

Protection Amendment

(Home Loans and Credit

Cards) Act 2011 due

to a legal drafting error in its definition of

Closing Balance

which does not

include

Balance Transfer

amount;

this omission has

resulted in ANZ charging vast amounts of interest at 19.74% p.a. on its

'First Card' and

13.49% p.a. on its

'Low Rate Card' against the terms of its definition of

Closing Balance.

As

defined by the ACCC,

Unconscionable Conduct notes

'inter alia' under

'How to avoid engaging in unconscionable

conduct':

"make sure your contracts are thorough,

easy to understand, not too lengthy and

do not include harsh, unfair or

oppressive terms"

"ensure you have clearly disclosed

important or

unusual terms or conditions

of an agreement"

|

|

*

Click on:

Example 4 -

Unconscionable Conduct -

Bankwest More MasterCard

Bankwest's

"0% p.a. on balance transfer

for 18 months"

offer letter to Ms. K. Gord_n dated 12 Jan '15 [1 pg] -

a)

informs "Start the year fresh

with a great balance transfer offer of 0% for 18 months^,

plus be rewarded with up to 50,000 bonus points"

b) but

does not inform the high Purchase rate of

19.99% p.a. and high

Cash

Advance rate of

21.99% p.a

If a new Bankwest More MasterCardholder makes any

Purchase/s, until the

Purchase/s and

Balance Transfer amount is repaid

'in toto', the Bankwest More MasterCardholder -

(i)

continues to be charged interest @ 19.99% p.a. on the

Balance Transfer

amount, plus the Purchases from the date of

each Purchase, unless both are repaid in full by the

Due Date; and

(ii) forfeits

its Interest Free Period.

*

Click on:

Example 5 -

Unconscionable Conduct -

American Express

Low Rate Card

Offers a

$7,500 or 50% of your approved

Credit Limit whichever is less at 0.99% Balance Transfer fee. After the 6 months, any o/s 'Balance Transfer' amount is

charged @ 11.99% p.a, as are

Purchases. You have to learn in the exceedingly fine print in 'Terms and

Conditions' that

Interest free days do not

apply if you do not pay your Closing Balance (which includes any outstanding

balance transfers, cash advances, purchases and fees) in full by the due date

each month. This key additional cost is not set out in the key features.

*

Click on:

Example 6 - Unconscionable Conduct - Citi Rewards Signature Credit Card

Nowhere in the web add, which includes

'Important Information', does

it inform the Purchase interest rate of

20.99% p.a. Nor does

it list the annual fee of $395 from 2nd year.

Nor does it inform that there is no

Interest Free Period

if you have a

Balance Transfer.

Citibank's Late Payment Fee

(for accounts opened prior to 1 July 2012) of $10 is "Charged

when the Total Minimum Payment Due is not paid by Payment Due Date and every 7 days thereafter until the Total Minimum Payment Due is made

Citibank's Key Facts Sheet

which confirms the above Purchases interest rate an that the

Late Payment Fees

is levied every 7 days, is not accessible from this

advertisement for

Citi Rewards Signature Credit Card.

*

Click on:

Example 7 - Unconscionable Conduct -

HSBC Platinum Credit Card

Enjoy 0% p.a. on

Balance Transfer for 15 months from non HSBC credit cards

(reverts to the variable cash advance rate 21.99% p.a.).

In the Fine Print in 9 font Arial is "There

are no interest free days for cash advances or

balance transfers.".

Meaning if you utilise the 15 months

Balance Transfer

@ 0%

p.a. option, you pay interest on all Purchases @ 19.99% p.a. from the

date of each Purchase.

The Key Facts

Sheet notes "Interest-free

period - Up to 55 days on purchases".

This

is incorrect, as

pursuant to clause 21.2

of

HSBC Credit Card Conditions of Use -

effective 1 April 2016

if

the full

closing balance

is not repaid by the

due date,

then the Cardholder forfeits the

"Interest-free

period - Up to 55 days on purchases"

for the subsequent month:

"until

the closing balance of that statement of account and any

subsequent statement of account is repaid in full by the due

date.".

This

Conditions

of Use

of

72 pages notes on page 2:

"We strongly recommend that

you and any

additional cardholder

read

this booklet carefully

and retain it for future

reference."

It informs

that all interest rates, fees and Card Limit 'et al' are in the

Schedule which the Definitions note

"the schedule that is set out in the letter we sent you

advising of our approval of your application for the

card". HSBC "strongly

recommend that

you read this

booklet carefully,

but you

cannot access the

Schedule

(referred to 80 times in

Conditions

of Use)

until after the prospective Cardholder has applied On-line', been

accepted and paid the Annual Fee.

*

Click on:

Example

8 -

Unconscionable Conduct - Citibank Platinum Card, Citibank Classic

Card and Citibank Simplicity Card

The

Citibank webpage for the above three Citibank Credit Cards presents

the few Benefits and encourages readers to

Apply

Now without reading the 'Important information' that

contains

9 Spiders.

*

Click on:

Example

9 - Unconscionable Conduct -

American Express Explorer Credit Card

Features:

*

"Earn

100,000 Bonus Points3"

"if you spend $1,500 on your Card

within the first 2 months."

* "Start exploring with a $400 Travel

Credit every year4"

are in tiny 1em font (8½

Helvetica

font) and hidden at end.

The 12

are displayed only three clauses at a time A reader has to scroll down and cannot read

the entire T&Cs in their entirety, but only in small sections.

Some Credit Card Issuers deploy

the small window scroll so that readers cannot look at all the terms and

conditions a page at a time, rather 12 lines at a time in tiny font. Often in

dark grey font not black.

Clause 2 in

notes that if you have a Balance Transfer amount, there is no Interest Free Period.

So the metre is running at 20.74% interest rate on all Purchases, from the date

of each Purchase.

|

3.

The Writer understands that most of the websites

which pop up using Google (see 3 websites below) that purport to alert Australians of the pitfalls of

Credit Card Products

are funded by different groups of

Credit

Card Issuers.

These websites are conflicted and understandably promote their funders'

Credit Card Products as good

value.

-

www.australia.creditcards.com

Credit card news archive

CLOSED ITS AUSTRALIAN WEBSITE AFTER THE WRITER'S SUBMISSION TO RBA

-

www.creditcardfinder.com.au/ lists

both

Purchases

rate and

Cash Advances

rate on primary add page -

high integrity

-

http://www.creditcards.com.au

"CreditCards.com.au

may receive payment for providing credit service referrals from

affiliated partners and agencies, including financial institutions,

in the form of sponsorship, commissions and/or advertising.

We recommend that you seek the advice of your own financial adviser

before making a decision on a product solely on the information you

obtain from this website. If you choose to apply for a product

please be aware that you will be dealing with the financial

institution and not this website."

(a)

does not

list its quoted "Interest Rate" as only applying to

Purchases;

intended to mislead; and

(b) provides a URL to the

Credit Card Issuers

particular

Credit Card Product.

The RBA has

failed level 1 and level 2 Australians by not regulating

'Primary

Information' that should be prominently displayed in a regulated summary format on

the opening page of every

Credit Card Product advertisement be it a 'personal offer

letter', brochure, newspaper add or webpage.

The

above 3 websites (under point 3. above) that purport to be identifying the best credit card deals, that

are paid

for by some

Credit Card Issuers,

generally do not announce the interest rate on

Cash Advances on their primary advertising webpage patently targeting

Australians with 1 and level 2 Financial Literacy by only seeing the

Purchases interest rate which

is often around 5% lower than the associated

Cash Advance interest rate.

Unconscionable Conduct notes

'inter alia':

Australian consumer law – unfair contract terms

(new provisions since 1 July 2010)

"The unfair contract term provisions apply to

'standard form consumer contracts'. Standard form contracts are commonly

used across a range of industries including telecommunications,

utilities, domestic building and finance. Consumers and investors enter into standard

form contracts for financial products and financial services every day.

Contracts for home loans, credit cards and client or broker agreements

for example, are almost certainly standard form contracts."

"In determining whether a term of a consumer

contract is unfair a court must take into account the extent to which

the term is transparent (that is, expressed in reasonably plain

language, legible, presented clearly and readily available to all

parties), and the contract as a whole.

If a court finds that a term in a standard

form consumer contract is unfair, the term is void.

This means that the

term is treated as if it never existed. However, the contract will

continue to bind parties if it is capable of operating without the

unfair term."

If a

Credit Card Issuer

pays third party credit card comparison websites that

do not prominently note a second higher interest rate, namely the

Credit Card Issuer's

Cash Advance

interest rate, is the

Credit Card Issuer legally allowed to charge in excess of

the

advertised interest rate?

Predatory

Sale Of A Financial Product summarises that

Balance Transfer Interest-Free Period Offers

have been fraught with

Unconscionable Conduct both -

* prior to enactment

on 1 July 2012 of

The National Consumer Credit

Protection Amendment (Home Loans and Credit Cards) Bill

and subsequent to banning an 'Order of Payments'

Allocation Practice, where some

Credit Card Issuer's

applied the monthly repayment of the

Closing Balance

for the Previous Month's Purchases to the

Balance Transfer amount;

and

*

after

enactment of

The National Consumer Credit

Protection Amendment (Home Loans and Credit Cards) Bill

where some

Credit Card Issuer's

are concealing that the only way to enjoy the advertised saving of

interest on a

Balance Transfer amount

is to not make any

Purchases during the 'Teaser Interest Rate' (Nil

or low interest rate)

'Introductory Period' (from 3 months to 24 months).

The brilliant,

blunt Governor of the Reserve Bank of Australia between 1949-1968, Dr H.C.

Coombs, famously recalled that, when he was trying to explain the complexities

of central banking to a friend, the friend replied:

"Come the

Revolution, you will be hanged as high as the rest, but as they bear you off

to the nearest lamp post, you will be crying plaintively, “But I am a

CENTRAL banker!”‘ (quoted from Fast Money 2, Edna Carew, Allen & Unwin,

1985, page 46).

| |

|

{kind=link}

{kind=link}