|

| |

Grounds/Reasons for

Written Questions

Chapter

8. The U.S. Central Bank, namely the

U.S. Federal Reserve, has provided an

annual written report to the U.S. Congress on

the Profitability of Credit Card Operations of

"large U.S. Credit Card banks"

for the last

26 years

A simple 'pie chart' for Revenue and Costs tells a lot

Over 5,000

'Depository Institutions' in the USA, including commercial banks, credit unions

and savings institutions, issue VISA and MasterCard credit cards.

In June 2012, the

U.S. Federal Reserve submitted its 25th annual written

"Report to the U.S. Congress on the Profitability of Credit Card Operations of

Depository Institutions" [12 pgs] which

"limits its focus to the 14 credit card banks

that have at least $200 million in assets".

For the last 26 years the U.S. Central

Bank has provided a written annual report to the U.S. Congress

on the Profitability of

Credit Card Operations of major Depository Institutions which

"...accounted

for approx 66 percent of outstanding credit card balances on the books of

commercial banks or in pools underlying securities backed by credit card

balances."

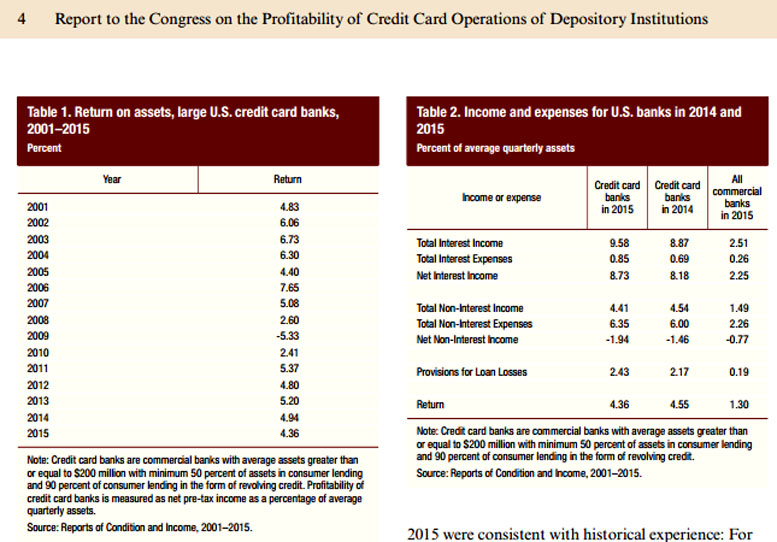

The U.S. Federal Reserve's annual

Report to the Congress

on the Profitability of Credit Card Operations of Depository Institutions - June 2016

includes the below Table 2 which

shows that 'USA Credit Card Banks' in 2015 had Net Interest Income of 8.73% and

Net Non-Interest Income of -1.94% of average quarterly assets.

USA Credit Card Banks are defined as commercial

banks with average assets greater than or equal to $200 million with minimum 50

percent of assets in consumer lending and 90 percent of consumer lending in the

form of revolving credit.

|

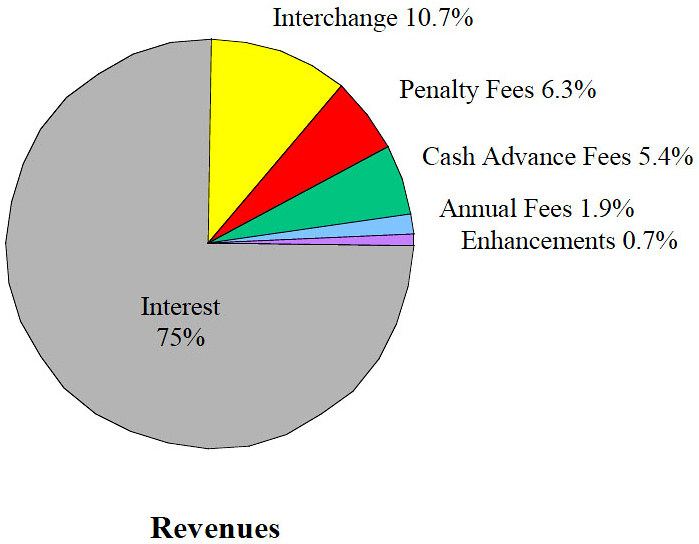

The below two 'pie charts' appears in a journal report titled

"Who Pays for Credit Cards?"

dated 2001 which displays a break-up of

Card Issuers' Revenues for the

aggregate of Visa, MasterCard and Discover Credit Cards in the USA. It shows

that U.S. Interest Revenues of 75% and associated Penalty Fees Revenue (Late

Payment Fees and

Overlimit Fees)

of 6.3% and Cash Advance Fees of 5.4% aggregate to 86.7% of U.S. Card Issuers' Annual Revenue.

Interchange Fees charged to Merchants were only 10.7%.

|

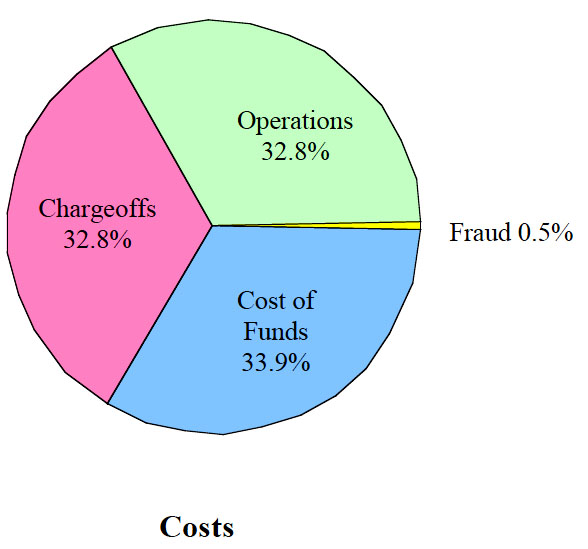

'Chargeoffs' are bad debts written-off or

sold to a collections agency.

It is a sad reflection of any unsecured personal loan lending product

that almost one third of operating 'Costs' is debt written off annually.

No other lending

product could survive with writing off one third of lent money annually.

This lending product can only be maintained because of the extraordinary

quantum of interest/fees based revenue stream evident in below Revenues

'pie chart'. |

|

|

|

|

|

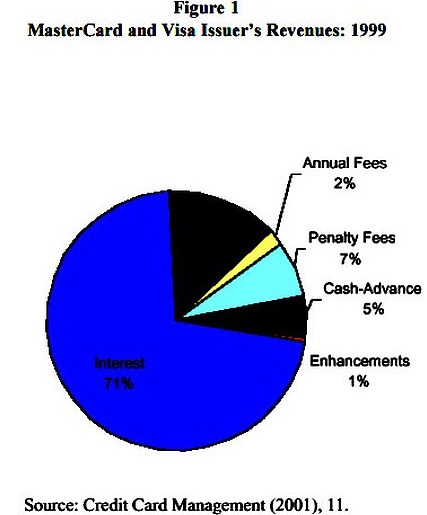

Below are extracts from 'Estimating

the Volume of Payments-Driven Revenues' dated 2003 published by

POLICY STUDIES presented by

Federal Reserve Bank of Chicago which relate to Figure 1 on LHS that breaks up

the revenues from US Banks that issued Visa and MasterCards in 1999:

"...... the major credit card issuers

(Visa, MasterCard) have been able to discern the percent of revenue earned from

different payments-related credit card services.

Credit Card Management (2001) breaks

down the 1999 revenues of Visa and MasterCard issuers into six subcategories:

interchange fees, annual fees, penalty fees, cash-advance fees, enhancements,

and interest. We consider interchange fees, annual fees, and enhancements to be

payments-related revenues. Based on this figure, 14 percent of total MasterCard

and Visa issuer revenues come from interchange fees, another 2 percent from

annual fees, and 1 percent from enhancements."

The pie chart shows that net U.S. Interest Revenues from Credit Cards of 71%, Penalty

Fees Revenue (Late

Payment Fees and

Overlimit Fees)

of 7% and Cash Advance Fees of 5% aggregate to 84% of U.S.

Card Issuers' Annual Revenue. Interchange Fees

charged to Merchants are only 14. Notwithstanding that

Interchange Fees are levied at a materially

higher amount in the USA,

Interchange Fees account for

less than 11% of aggregate U.S. Card Issuers' Revenue in the first above

pie-chart.

|

|

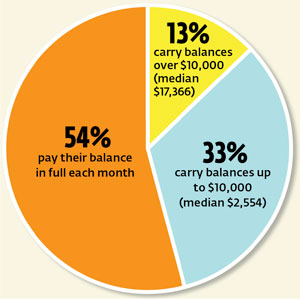

"A

third of Americans do not own a credit card, according to our

survey. Of those who use them, here's how much money they owe"

|

|

The disturbing disclosure from the above two 'Revenue' pie

charts is that the aggregate of Interest, Cash Advance Fees, and Penalty Fees

(Late Payment and Overlimit) aggregate from a high of 86.7% down to 84% of aggregate

Credit Card Issuers 'Revenue'.

Annual Fees do not exceed 2% of 'Revenue' in either above pie chart.

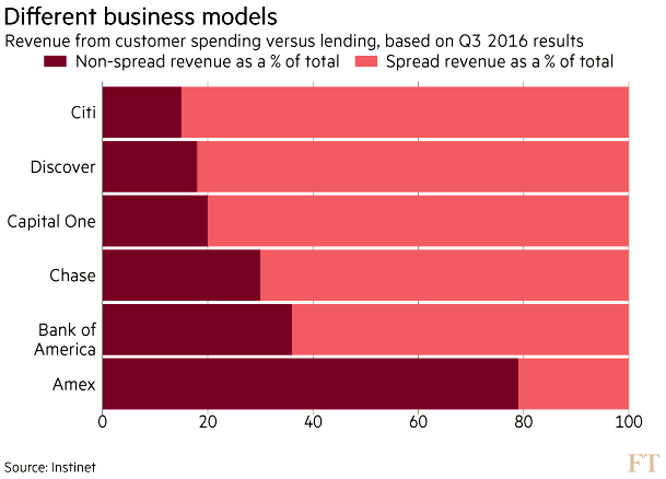

The above graph appeared in the

USA

Financial Times on Dec. 23, 2016 article discussing credit cards. One of the

charts (“Different business models”) shows a breakdown of spread revenue vs.

non-spread revenue for six major Credit Card Issuers in the USA.

Patently the top five Credit Card Issuers are deriving "The Lion's Share" of Revenue from the implicit

interest margin between "where they borrow money and the interest rates they

charge out" on

Purchases and Cash Advances on some credit cards.

Fee

income is relatively minor, except for Amex, BoA and perhaps Capital One.”

Section 8 of the Fair Credit and Charge Card Disclosure Act of 1988 directs the

U.S. Federal Reserve Board to transmit annually to the U.S. Congress a written

report about the profitability of credit card operations of depository

institutions. Last August the

Board of Governors of the

Federal Reserve System presented its 26th "Report

to the Congress on the Profitability of Credit Card Operations of Depository

Institutions".

The Reserve Bank's webpage "Accountability"

provides a section titled 'Accountability to Parliament' which notes that the

Governor of the Reserve Bank has provided every few years since 1998 to the Commonwealth Parliament a Statement on the

Conduct of Monetary Policy.

A precedent is therefore in place with the U.S. Federal Reserve reporting

annually in writing to the U.S. Congress on various aspects of Credit Cards

Profitability, for the Reserve Bank to similarly report annually to the

Commonwealth Parliament on various aspects of Credit Cards profitability which

would include Credit Card Issuers complying with

Section 3.4.8

Changes to benchmark compliance.

=====================================================================================

Refer:

Chapter

9.

Summary Page re Written Questions and the Grounds/Reasons

Grounds/Reasons

(one document with 21 Chapters)

Grounds/Reasons

(21 separate Chapters)

Written Questions

(one document with Written Questions)

Written Questions

(Individual Written Questions)

| |

|