|

| |

Grounds/Reasons for

the Written Questions

Chapter 9. There are over 100 voluminous

'Submissions', 'Reviews', 'Reports', 'Discussion Papers', 'Staff Working Papers'

and 'Enquiries'

in Australia in the last 10 years on Credit Cards. None

have identified the 'Fundamental Information', namely the percentage and

aggregate that

Interest and Penalty Fees

contribution to aggregate Card Issuers' annual revenue.

Credit Card Issuers

and

Credit Card Networks on

the

Wholesale Supply Side have done a masterful job in concealing the overwhelming

returns from

Interest and Penalty Fees

and which

Financial Literacy Demographic Quintiles

of Credit Cardholders are paying it

The Reserve Bank can require Australian banks to provide any financial data to

the Reserve Bank that

it wants to appraise - "any financial data"

Reserve

Bank has failed to draw upon its

Extensive

Powers

and Responsibilities to (All) Australians

to require major

Credit

Card Issuers (Four Pillars ) to provide financial information for

Credit Card Products

that identify cohort/s of

Credit Cardholders

that have paid an excessive burden of

Interest And Late Payments Fees (Chapter

9 and

Question 9), even after the

Reserve

Bank identified the material

Outstanding Indebtedness

carried by

Persistent Revolvers

(in Aug 2015),

whilst

67% circa

of

Credit Cardholders

Transactors

enjoy

a

Free Ride

with their

Revolving Lines of Credit

The

Four Pillars enjoy 80%

of the

Credit Card Market.

The below 'repeat' of the further above extract from

5. IMPACT ANALYSIS

of

RBA 2002

evidences that the

Scheme Providers,

as are the other parties under the

Wholesale Supply Side,

are masterly at concealing fundamental empirical evidence of the break-up of

aggregate Credit Card Revenues. Notwithstanding that there have been over

100 voluminous

'Submissions', 'Reviews', 'Reports', 'Discussion Papers', 'Staff Working Papers'

and 'Enquiries'

on Credit Cards by RBA, ABA, banks,

Credit Card Networks,

Senate Committees, regulators, Treasury,

Australian Retailers Association 'et al' in the last 10 years.

The Reserve Bank's

Submission

to the Financial System Inquiry - March 2014

noted:

"In 1998, the government

implemented a range of reforms that were generally in line with the broad

structure and powers recommended by the Wallis Committee. The responsibility for

oversight of the payments system was entrusted to the PSB. The PSB’s

responsibilities and powers are set out under four key pieces of legislation:

*

Reserve Bank Act 1959,

*

Payment Systems (Regulation) Act 1998 (the PSRA),

*

the Payment Systems and Netting Act 1998

(the PSNA), and

*

Part 7.3 of the Corporations Act."

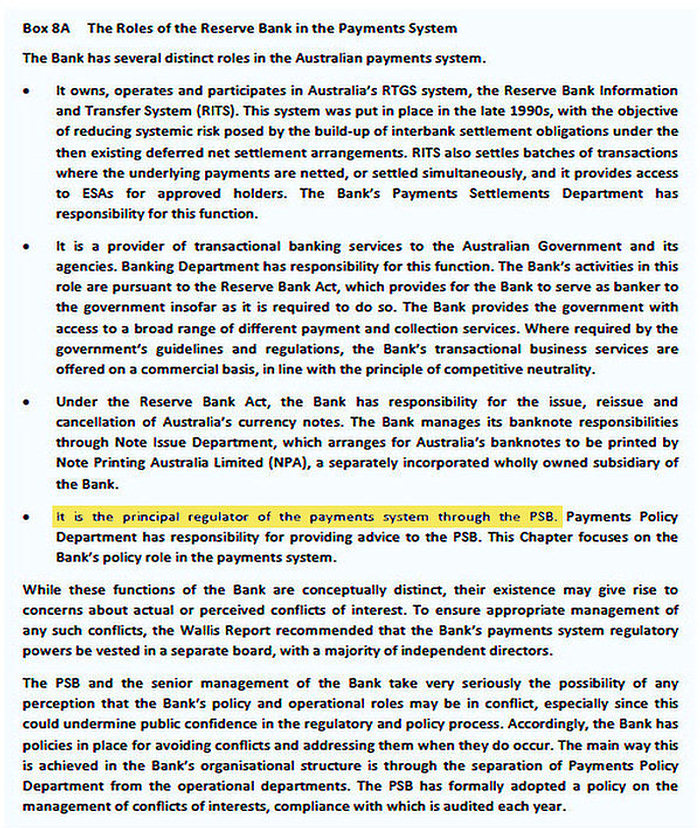

"The

Reserve Bank’s policy-making role is one of the four different roles of the Bank in the

payments system (see ‘Box 8A: The Roles of the Reserve Bank in the Payments

System’).

The Reserve Bank is the principal

regulator of the payments system through the PSB. Payments Policy

Department has responsibility for providing advice to the PSB."

"The

Payment Systems (Regulation) Act 1998 gives the Reserve Bank of Australia

'extensive powers' to gather information from a

payment system or from individual participants."

"The Payments

System Board was established by the Commonwealth

Govt. in 1998 so as to best contribute to:

.......... and

promoting competition in the market for payment

services."

As elaborated in Chapter 15 below,

Section

10(2) of the

Payment Systems (Regulation) Act 1998

says:

‘It is the duty of the

Reserve Bank Board, within the limits of its

powers, to ensure that the monetary and banking

policy of the Bank

is

directed to the greatest advantage of the people

of Australia and that the powers of the Bank ...

are exercised in such a manner as, in the

opinion of the Reserve Bank Board, will best

contribute to

...........the

economic prosperity and welfare of the

people of Australia.

The Reserve Bank can

exercise its

"...extensive powers"

under the

Payment Systems (Regulation) Act 1998

to

"gather

information from payment system participants and operators"

by requesting each of the

Four Pillars

to provide (to the Reserve Bank) financial information of their combined

Credit Card Products for the

financial year ended 30 June 2016 which enables the Reserve Bank to present to the

Australian Parliament the -

(i) same

style 'pie charts' for "Card Issuers'

Revenue" [that quantifies at least seven revenue sources] and "Card Issuers'

Costs" [that quantifies at least five costs, which include

Rewards Programs] that is displayed in

Chapter 8;

(ii) same style

"annual

Report to the

Congress on the Profitability of Credit Card Operations of Depository

Institutions (displayed in

Chapter 8) that the

Board of

Governors of the U.S. Federal

Reserve provided to the US Congress for annual financial accounts as at June 2016;

(iii) annual

cost of

Rewards Programme

and the contribution to this annual cost from

Interchange Fees; and

(iv) aggregate and the percentage of

gross interest revenue

that is paid by the highest paying 20% of

Interest

paying

Credit Cardholders

to assist appraisal of the application of the

User Pays Principle

for

Credit Cardholders

that

hold

over

16 million Credit Cards

in Australia.

=====================================================================================

Refer:

| |

|