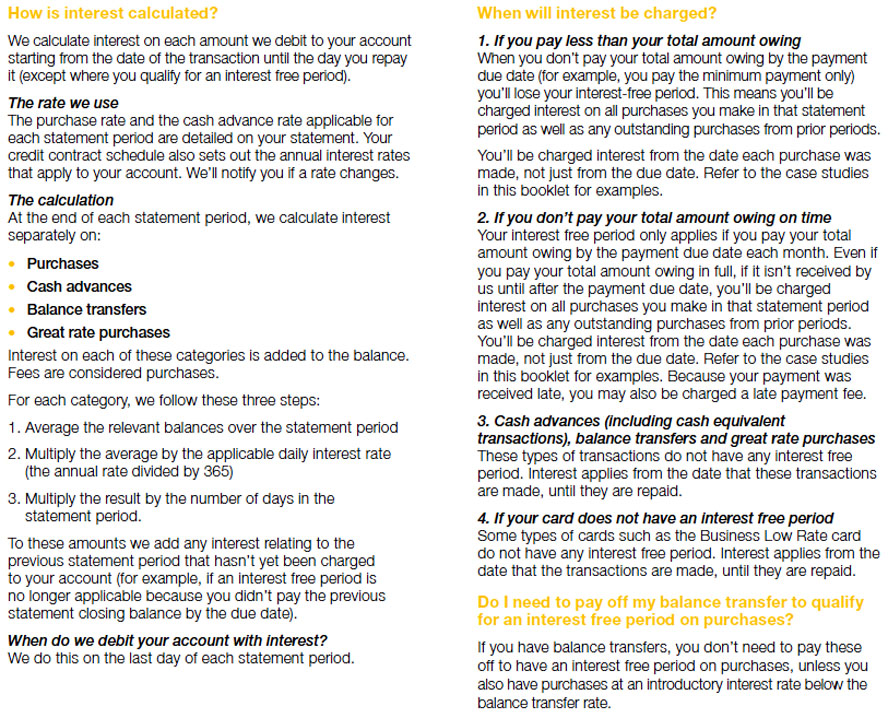

Interest Free Period means the number of interest free days from the date of a Purchase to when interest is charged on that Purchase if the total Total Amount Owing is not repaid. There is no Interest Free Period on a Cash Advance.

Interest Free Period is known as the 'Grace Period' in the USA and Europe. Diners Club and American Express' decision to provide a Grace Period as an inducement/lure when mass marketing their 'new fangled' Credit Cards in the early 1960's has proven to be a marketing 'master stroke'.

Interest on the Total Amount Owing is charged if a Cardholder does not pay their Total Amount Owing in full at the end of the one-month statement period. As Cardholders generally have about 14 to 25 days from receipt of their monthly statement to pay their previous month's Total Amount Owing, this means there is usually an Interest Free Period of between 44 days and 55 days.

A Cardholder can forfeit the Interest Free Period for up to three months if repayment of its monthly Total Amount Owing is a day late or a dollar short, whereupon the applicable Interest Rate is charging (at an interest rate up to 25% pa) from the date of each Purchase;

Several Credit Card Issuers cancel the Interest Free Period for up to three months, if the Credit Cardholder does not pay 100% of the Total Amount Owing by the Payment Due Date, meaning the Interest Free Period is not available for three months, the Credit Cardholder is charged interest at up to 25% from the date of each Purchase, notwithstanding that the Official Cash Rate is 1½%.

Below is the Australian Retailers Association - Submission to RBA dated 2001 - Credit Card Schemes in Australia - sourced on the RBA website (marked Confidential) was highly critical of the RBA's inept and complicit role in Credit Card Issuers imposing an Interchange Fee upon Merchants when the contract is between the Card Issuer and the Cardholder. The Australian Retailers Association supported the User Pays Principle for all enjoying a Credit Card/s Line Of Credit by recommending that the 'ad valorem' Merchant Service Fees "should be completely abolished and replaced with market negotiated activity based fees".

{kind=link}

Cardholders to take up card products and existing cardholders to utilise their cards.....The interest free period is again, a Card Issuer / card holder relationship cost......The introduction and length of interest free periods was determined by credit Card Issuers to facilitate credit card take up and usage – both revenue generating activities for themselves. We find it implausible that Issuers sought to introduce interest free periods for any reason other than to increase their own income levels.""We agree that the interest free period encourages potential