Grounds/Reasons for Written Questions

Chapter 1.

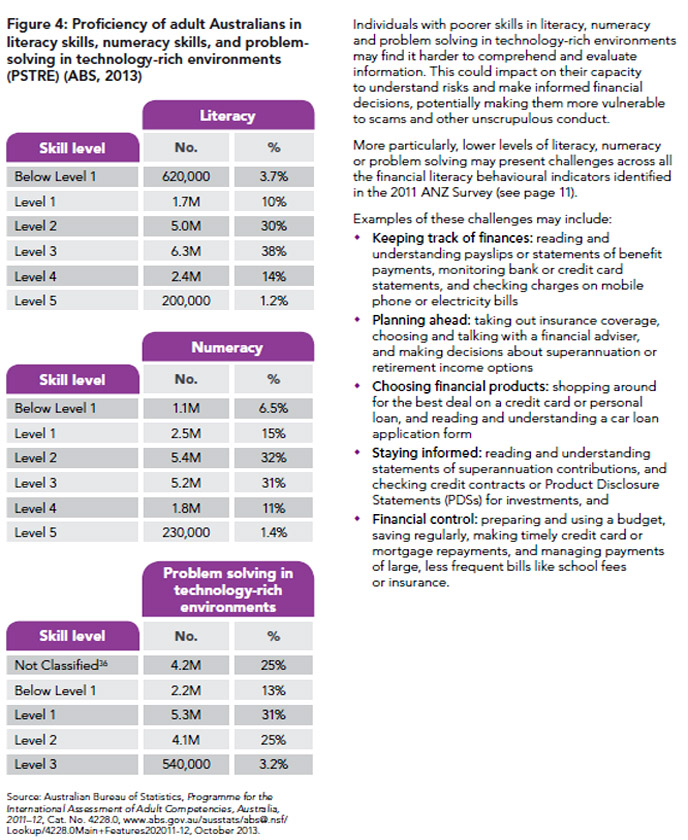

Productivity Commission and the ABS rank Australians as having between Level 1

(low) and Level 5 (high) for Numeracy

and Literacy Skills.

A person assessed at Level 5 possess up to five times the skills within the

particular domain (eg Numeracy, Literacy, Prose etc) than a person assessed at

Level 1.

Level 3 or above is required "to meet the complex demands of everyday life and work in the emerging knowledge-based economy"

ASIC

2010 report notes "These

findings have implications for our regulatory regime, which relies upon

disclosure as a critical element of our consumer protection system. "

St. George and Westpac test Credit Cardholders with even Level 5 Numeracy

and Literacy Skills by

expecting all their Credit Cardholders to read/comprehend voluminous Conditions

of Use in a

tiny font.

Productivity Commission's Staff Working Paper "Links Between Literacy and Numeracy Skills and Labour Market Outcomes" dated Aug 2010 noted:

For nearly half of the population were assessed at either levels 1 (the lowest level) or 2, both of which are below the minimum level deemed necessary to participate in a knowledge-based economy (level 3).

In 2006, the proportion of the working-age population (15–64 years) who had Language Literacy Numeracy (LLN) skills at levels 1 or 2, supposedly lower than the minimum required, was 44 per cent for prose literacy and document literacy, and 50 per cent for numeracy (figure F.1). The proportion at level 3 was 39 per cent for prose literacy, 37 per cent for document literacy and 33 per cent for numeracy. Productivity Commission Impacts of COAG Reforms: Research Report - April 2012

ABS report Adult Literacy and Life Skills Survey, Summary Results, Australia, 2006 included:

* "On the numeracy scale, approx. 7.9 million (53%) Australians were assessed at Level 1 or 2, 4.7 million (31%) at Level 3 and 2.4 million (16%) at Level 4/5".

* On the problem solving scale, approx. 10.6 million (70%) Australians were assessed at Level 1 or 2, 3.7 million (25%) at Level 3 and 800,000 (5%) at Level 4 (table 1)"

* ABS - APPENDIX 1 - LEVELS OF SKILLS for PROSE LITERACY, DOCUMENTS SKILLS, NUMERACY and PROBLEM SOLVING - explains the criteria for ABS's rankings.

ASIC Report 224 "Access to financial advice in Australia" - December 2010 includes:

These results, when considered together with Australian Bureau of Statistics‘ research into Australians‘ general document literacy and numeracy,15 in particular their ability to meet the complex demands of a knowledge-based economy, suggest that about one in two Australians do not have the skills required to make informed choices in their interactions with the financial services sector.16 There is also an identifiable age link, with document proficiency tending to decrease with age.51

14 For example the 2008 ANZ study of financial literacy found that ‗67% of respondents said that they understood the principle of compound interest, but only 28% were rated with a good level‘ of comprehension when they solved the problem‘, ANZ Banking Group Limited, ANZ survey of adult financial literacy in Australia, (The Social Research Centre) ANZ Banking Group, Melbourne, 2008, p. 19.

15 As part of an international study, the ABS measured skills in document literacy, prose literacy, numeracy and problem solving and found that approximately 7 million (46%) of Australians (and 7.9 million (53%) of Australians aged 15 to 74) had proficiency less than the minimum required for individuals to meet the complex demands of everyday life and work emerging in the knowledge-based economy‘ for document literacy and numeracy respectively‘, Australian Bureau of Statistics, Adult literacy and life skills survey results, cat. no. 4228.0, ABS, Canberra, 2006, p. 5.

16 These findings have implications for our regulatory regime, which relies upon disclosure as a critical element of our consumer protection system.

The Australian Govt & ASIC National Financial Literacy Strategy 2014–17 included:

"The ABS research groups literacy and numeracy into six skill levels (where below Level 1 is lowest and Level 5 is highest), and problem solving in technology-rich environments (PSTRE) into four skill levels (where Below Level 1 is lowest and Level 3 is highest).33

The Productivity Commission’s analysis of these results highlights that many Australians have relatively low literacy and numeracy skills and this limits the range and type of tasks that they can do in comparison with those with relatively higher skills.34

Groups with relatively low literacy and numeracy skills include: ‘people with low levels of education; older persons; people not working; and immigrants with a non-English speaking background’.

35Behavioural indicators

Research tells us that Australians have differing attitudes to money and varying levels of financial knowledge and proficiency.22 People may perform well on some aspects of financial literacy, but poorly on others.23

The latest report on Australians’ financial literacy, the 2011 ANZ Survey of Adult Financial Literacy in Australia (ANZ Survey), is the fourth in a series of national snapshots conducted by the ANZ Banking Group since 2003.24

Many people underestimate the extent of their own knowledge gaps. So their behaviour, even in simple day-to-day money management, may not be consistent with how confident they are in their abilities. As discussed on page 8, individual financial decision-making behaviour may also be influenced by personal or environmental circumstances.

The 2011 ANZ Survey also highlighted a number of areas of behavioural vulnerability, particularly in keeping track of finances and planning ahead:

one third (36%) found dealing with money stressful, even when things were going well

Results of the 2011 ANZ Survey confirm the complex and variable nature of individual financial decision-making. A range of factors were found that may help explain differences in financial literacy levels, such as financial attitudes, age, financial knowledge and numeracy, household income, and education and occupation.29

The Productivity Commission’s analysis of these results highlights that many Australians have relatively low literacy and numeracy skills and this limits the range and type of tasks that they can do in comparison with those with relatively higher skills.34 Groups with relatively low literacy and numeracy skills include: ‘people with low levels of education; older persons; people not working; and immigrants with a non-English speaking background’.35

Research shows that Australian women typically have lower numeracy levels, find dealing with money stressful or overwhelming and have more difficulty with retirement-related investment decisions than men.63"

The above extract of page 13 of the National Financial Literacy Strategy 2014–17 notes that according to the ABS 21.5% of the Australian population do not posses the Numeracy Skills to "shopping around for the best deal on a credit card" or making timely credit card or mortgage repayments.

"A necessary part of financial literacy is knowing how to track your expenses and live within your means. Data from Roy Morgan Research in 2012 shows that, within the 16–24 age group, one in 10 carry forward more than $2,000 in credit card debt each month, suggesting difficulties in managing money.49"

"Feedback from the 2013 Consultation also identified the need for a mechanism to share relevant findings from existing national surveys (for example, focusing on the savings and credit card behaviour of Australians)."

These results, when considered together with Australian Bureau of Statistics‘ research into Australians‘ general document literacy and numeracy,

15 in particular their ability to meet the complex demands of a knowledge-based economy, suggest that about one in two Australians do not have the skills required to make informed choices in their interactions with the financial services sector.16 There is also an identifiable age link, with document proficiency tending to decrease with age.The above published reports from the Productivity Commission, ABS and ASIC is patent evidence that a

“community service obligation” has existed for at least 20 years for the (small 'g') government to take stringent action because during that post-deregulation era Credit Card Issuers have -(a) targeted Australians with low Financial Literacy Capacity that are Financially Uneducated And Vulnerable to Unconscionable Conduct through Predatory Advertising

(b) by promoting some Credit Card Products that charge Usurious Interest Rates and apply excessive Late Payment Fees,

because the below Chapter 8 evidences that the 12.58% circa of Credit Cardholders that are identified by the Reserve Bank in its Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - Aug 2015 - Submission 20, as Persistent Revolvers, that are contributing 80% circa of Interest and Penalty Fees Revenue - displayed in Figure 3 in Chapter 8 below.

Relying upon the Productivity Commission and the further ABS above rankings for the domains/categories of Numeracy and Literacy Skills, less than half of the top Level 5 Credit Cardholders (approx 5% of Credit Cardholders) could read and comprehend the follow three Conditions of Use booklets from St. George, ANZ and Westpac:

|

St George's 62 pages Conditions of Use - Credit Guide "Effective 20 May 2014" - 60 pages are written in tiny 8.5 Helvetica font. The word 'interest' appears in the 'Contents' twice and 77 more times throughout the 62 pages. The word 'fee' or 'fees' appears 53 times. Page 2 of the Conditions of Use - Credit Guide includes: "We strongly recommends that you read this booklet carefully....". |

|

ANZ's 'CONDITIONS OF USE 20.06.2016 CONSUMER CREDIT CARDS' booklet contains 97 pages in tiny Arial 9 font. Page 6 notes:

'Introduction' "The credit card

contract governs the operation of the credit card account and your use of a

credit card. It is important that you read and understand the credit card

contract. The credit card contract is set out in your Letter of Offer and Parts

A and B of this booklet." Part A of the booklet has 51 pages. Part B has 22 pages. Further in 'Introduction' is: "Finally, you should also read the notice ‘Things you should know about your proposed credit contract’, which is included in this booklet following Parts A and B." ' 'Things you should know about your proposed credit contract’ is 7 pages. Hence, ANZ tells its Credit Cardholders to read the entire 97 pages of its booklet. Clause (4) 'Allowing use by others' includes:

The word "interest' appears 216 times in the booklet. The word 'fee' or 'fees' appears 104 times. |

|

Westpac has two separate Credit Card booklets both "Effective as at 28 Oct 2016": - "Combined

Conditions of Use and Credit Guide' for Credit Cards"

in Arial 11 font: Sub clause (c) of clause 1.1 'Introduction' notes: "These Conditions of Use do not, on their own, contain all the terms applying to your Credit Card, so it is important that you read all of the documents comprising the Credit Card Contract carefully and retain them for future reference." Clause 17. 'Do I have any other rights and obligations?': "Yes. The law will give you other rights and obligations. You should also READ YOUR CONTRACT carefully."

- "Ignite

by Westpac - Consumer Credit Card Conditions of Use" in

HelveticaNeue-Light 9 font. |

|

CBA's Credit

Cards 'Conditions

of Use' booklet in Arial 10 font is only 21 pages. Clause 1. of the booklet titled 'Your contract with us" notes: "Please read both these Conditions of Use and the Schedule of Credit Card Particulars in your letter of offer, which together make up your contract and include the information we must give you." |

Refer:

Summary Page re Written Questions and the Grounds/Reasons

Grounds/Reasons (one document with 21 Chapters)

Grounds/Reasons (21 separate Chapters)

Written Questions (one document with Written Questions)

Written Questions (Individual Written Questions)