|

| |

Defined Terms and Documents

Credit Cardholders or Credit Card Users

The below Credit Card

ownership and usage statistics

are sourced from:

-

ASIC

MoneySmart 'Credit

card debt clock

shows that $32.287 billion dollars in Credit

Card

Outstanding Indebtedness

is accruing interest @ 17.34% p.a. ave =

$5.60 billion interest paid p.a. by

Revolvers.

The average Credit Cardholder is paying around $700 in

interest per year if their interest rate is

between 15 to 20%.

-

Australian

Credit Card and Debit Card Statistics 2017 -

Finder showed:

- 16,735,686 Credit

Cards on issue as at 31 Oct 2016

- $32.144 billion of

Outstanding Indebtedness on

Credit Cards accruing interest

- $1,933 ave. Credit

Card balance accruing interest

@ 17.22% p.a. ave

- 70.19% of Australians

own a credit card - DOUBTFUL as you

have to be 18 or older, and some Australians

don't use plastic at all, and others use a debit

card only

-

7,515,000 Credit

Cardholders in Australia (Source:

Roy Morgan Research, 12 month average June 2016)

- on ASIC's MoneySmart webpage.

-

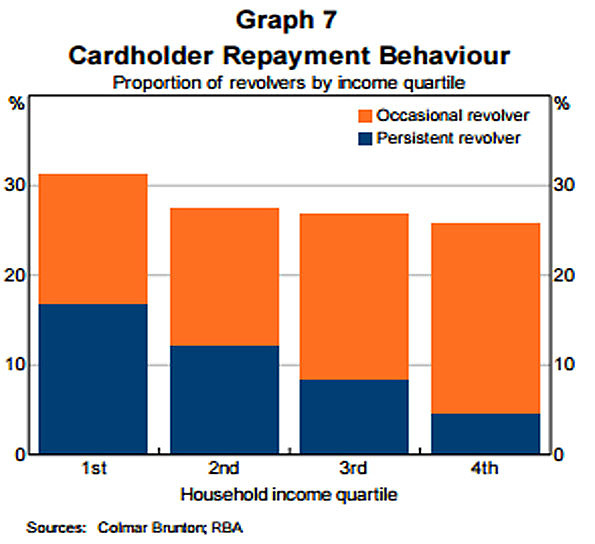

Below RBA Graph 7 "Cardholder

Payment Behaviour" (in RBA report

RBA Submission

to the Senate Inquiry into Matters Relating to Credit Card Interest Rates -

Aug 2015)

splits the 33% of

Credit Cardholders

that are

Revolvers into

Occasional Revolvers

(62.75%)

and

Persistent Revolvers

(37.25%)

-

Revolvers

represent 33% of

Credit Cardholders

transactions.

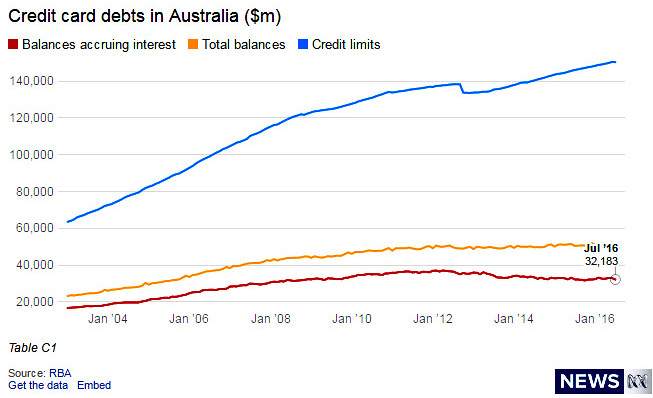

Below

'Credit Card debts in Aust ($1m) graph as

at July '16)

shows that

Revolvers carried $32.183 billion (of interest

accruing Credit Card debt at an ave per Credit Card debt

of $6,095 paying interest @ an ave. 17% p.a. = $1,036 pa. interest on average

per Credit Card used. This $1,036.20 pa. circa takes no account of

Late Payment Fees.

-

RBA's Submission

to the Senate Inquiry into Matters Relating to Credit Card Interest Rates -

Aug 2015

noted:

"In the

June quarter of 2015, new credit card transactions averaged around $24

billion per month. At the end of June, the total level of credit card

debt was $51.5 billion (Graph 11).

Of this amount, $33.1 billion, or around 65 per cent was bearing interest.

A simple calculation would suggest that around 75-80 per cent

[(51.5–33.1) ÷ 24 ≈ 0.77%]

of transactions on credit cards do not accrue interest. That is,

interest-paying ‘Revolvers’ account for about 30-40 per cent of

accounts, about 20-25 per cent [1.00 - 0.77

≈

0.23%] of transactions, but close to two-thirds of the

outstanding stock of debt.9"

-

Australian Treasury’s Submission to Senate Economics References Committee -

Aug 2015 noted:

"According

to a 2013 RBA survey, only around 30 per cent of credit card users reported that

they pay interest on their credit card balances (the ‘Revolvers’)."

-

Chapter 5 includes "Five extracts

that evidence that Financially Savvy Users Don't Pay - some Are Paid".

Below are the 4th extract and 5th extract:

4th extract:

From

Australian Treasury’s Submission to Senate Economics References Committee -

August 2015 noted:

"According

to a 2013 RBA survey, only around 30 per cent of credit card users reported that

they pay interest on their credit card balances (the ‘Revolvers’).

However, the share of outstanding balances that actually attract interest is

higher, at around two-thirds.".

This disparity between 30% and two thirds indicates that a small portion of

Credit Cardholders are carrying very high

Credit Card Debt Accruing Interest.

5th extract:

A footnote in

Consumer Credit Reform and Behavioural Economics: Regulating Australia’s Credit Card Industry -

2013 (provided by three eminent academics) that seeks to quantify the number of

Revolvers'

suffering

Extreme Financial And Emotional Distress,

thereby being

Persistent Revolvers. :

9 There is limited evidence

to conclude with certainty the number of Australian credit card consumers who

carry unmanageable debt, in part due to the lack of consistent

reporting by lenders.

The recent ANZ Financial Literacy Report indicates that 13% of respondents paid only the minimum

repayments on credit card balances, and 23% of respondents stated they had been charged interest on credit card

debt in the last 12 months, above n 1, 46.

It is difficult to determine, however,

what percentage of these

revolving consumers fall into the category of those experiencing unmanageable debt.

RBA figures from 2001 analysed

by the NSW Office of Fair Trading placed the figure

as high as 10% of

credit card holders, cited in

Ministerial Council on Consumer Affairs,

Responsible Lending Practices in Relation to Consumer Credit Cards,

Consultation Regulatory Impact Statement, August 2008, 16.

RBA data from 2004

suggested that 0.8% of outstanding balances were

in default, after 90 days of non‐payment: Reserve Bank of Australia, ‘Box A: Credit Card indicators’,

Financial Stability Review (September, 2004).

There were 7,515,000 Credit

Cardholders in Australia

(Roy Morgan Research, 12 month

ave. June 2016) - on ASIC's MoneySmart webpage.

Re the immediately above

"...

as high as 10% of

credit card holders,

10% of the

7,515,000 Credit

Cardholders in Australia as at June 2016 is 751,500 Credit Cardholders

being

Persistent Revolvers.

* Number of credit

and

Charge Card

accounts: 16.66

million accounts

* Credit

and charge card balance total: $52.463

billion

*

Average credit card balance: $3,160

*

Credit card and Charge Card balance total (accruing

interest): $32.207 billion (61.4% of the total

Australian credit card balance is

accruing interest)

Findings

from Roy Morgan’s Single Source survey of over

50,000 consumers pa which includes detailed coverage

of over 39,000 with major cards in "High

incomes run up relatively less debt on major cards"

- Dec 12, 2016 note:

"In the 12 months to October 2016,

holders of major cards (VISA, MASTERCARD, AMEX) intended to carry forward to

their next statement an average monthly debt of $19 billion between them.

The main contributors to this were the lower-income card holders, who on

average owed an amount equivalent to a much higher proportion of their

incomes than the higher-income groups."

McKinsey Report - May 2014 categorises 'Five Segments' of Credit

Cardholders in the USA:

1: Prosperous and content

Keep their

finances in order, use credit cards for 59 percent of their purchases and

love rewards; they dislike revolving debt. They

look for convenience and minimum effort, preferring to “set it and forget

it” rather than get closely involved with banks or card issuers.

2: Deal

chasers

Average revolving debt of

$3,802— twice the average— move their balances around to chase the best

transfer rates. This segment is the most likely to have a cobranded card (24

percent compared with 17 percent overall) and to pay an annual fee for a

reward card (19 percent compared with 13 percent). Deal chasers are highly involved

with financial products and nearly as satisfied with their financial

situation as the prosperous and

content segment

(34 and 37 percent respectively, compared with 20 percent overall), and rank

second in both income ($65,000 median) and financial assets ($150,000).

Despite carrying higher debt, they are confident about managing it and view

the economic outlook as positive. Use online banking frequently, with half

making online transactions three times a week. Acquiring and keeping

these customers calls for a balancing act, as they see themselves as pitted

against issuers in a win-or-lose game. Always striving to borrow at the

lowest cost, they try to steal the bait from issuers’ traps without

triggering fees or higher rates through mishaps or oversights.

3: Financially stressed

Carry heavy credit card

debt—nearly four times the average, at $7,453—and consider themselves unable

to control their spending or stick to a budget. Some are chronic

spendthrifts; others are mired in circumstances that force them to borrow on

credit cards to pay for essentials. Seldom shop around for better

places to put their outstanding balances and doubt they will ever get out

from under their burden of debt. Expect financial trouble for themselves and

the wider economy. Poorest among the segments, with just a quarter of the

financial assets (a mean of $44,000) of the average cardholder. Credit plays

a crucial role in satisfying this group’s day-to-day needs: keeping a roof

over their head, paying for their daily commute, keeping a prescription

filled. This is not a sustainable path, but they are unable to abandon it

just yet. Value simplicity and transparency in fees, rates and terms,

but their biggest need is for something that no credit card offers: a

mechanism allowing them to impose their own spending limits which would

enable them to carry a credit card for larger purchases that take time to

pay off, without fearing they might be tempted to use it for non-essentials.

4: Recovering credit users

Avid budgeters

who pride themselves on keeping their financial house in order, although

they still revolve an average balance of $1,726. Wary of financial

institutions, avoid the stock market as too risky, fear their bank deposits

are unsafe and blame issuers when consumers accumulate debts and fees they

are unable to pay off. Avoid using credit cards for routine purchases and

seldom respond to zero-percent teasers or high-reward offers. They prefer to

deal with bank staff in person and are less likely than other segments to

use online banking, with just 49 percent doing so. This group’s

adversarial view of issuers suggests they need reassuring that they can use

a credit card without stumbling into a “gotcha” fee or triggering a penalty

rate. Need a product that helps them budget and manage their

spending—for instance, by allowing them to define spending “buckets” for

various merchant types with monthly limits (e.g., $200 at grocery stores,

$80 at mass merchants and $150 at restaurants).

5: Self-aware avoiders

Avoid using credit cards, although

they blame themselves rather than issuers for their debt problems and worry

about the damage they could do to themselves with a credit card. Use debit

cards and cash for three-quarters of their POS purchases.

Numeracy And Literacy Range Of Australians

explains that only slightly over half the Australian population

possess the minimum required

Financial Literacy

and numeracy skills of level 3

"...to meet the complex demands of everyday life and work in the emerging

knowledge-based economy".

ABS 4228.0 2006 page 5

Financially Educated Australians are ranked level 3, level 4 or level 5 in the -

* Productivity

Commission's Staff Working Paper

Links Between Literacy and Numeracy

Skills and Labour Market Outcomes dated Aug

2010;

*

Australian Bureau of Statistics'

Adult Literacy and Lifeskills Survey

(ALLS) - 2006; and

* Australian Bureau of Statistics'

Survey of Aspects of Literacy

(SAL) -

1996.

Unlike the

Wholesale Supply Side where all the

parties (Credit Card Issuers,

Card Acquirers and

Merchants) have powerful lobby groups to protect their commercial interests, the

Retail Supply Side contains

exceedingly powerful and too often unscrupulous participants amongst the

Credit Card

Issuers, whereas

almost 8 million Australian

Credit Cardholders have no lobby group to protect their commercial interests because

Australia's Principal Regulator of the Payments System, namely the RBA considers that

"The Payments System Board of the Reserve Bank has no regulatory power over

these aspects of credit cards", notwithstanding

Unconscionable Conduct

by some Credit Card

Issuers as evidenced in

Labyrinth of

‘Concealed Spiders’. | |

|