Rewards Programs or Reward Points are incentive programs operated by Credit Card Issuers where a percentage of the amount spent is paid back to the Cardholder by means of 'Rewards Points' earned. Many Credit Card Issuers run programs to encourage use of their Credit Card where the Cardholder earns 'Loyalty Points', often referred to as 'Reward Points', frequent flyer miles, travel insurance or a monetary amount.

Where a Card Issuer operates such a scheme/program, Cardholders typically receive between 0.5% and 2% of their net expenditure (purchases minus refunds) as an annual rebate, which is either credited to the Credit Card account or paid to the Cardholder separately.[1]

are incentive programs operated by Credit Card Issuers where a percentage of the amount spent by a Credit Cardholder is paid back to the Credit Cardholder by means of points earned. Many Credit Card Issuers run programs to encourage use of their Credit Card Products where the Credit Cardholder earns loyalty points, often referred to as Reward Points, frequent flyer miles or a monetary payment.Credit Cards that offer the highest Rewards Programs charge the highest Interchange Fees and charge the highest Annual Cardholder Fees which are attractive to small and large companies, as well as sole traders, that can charge Annual Fees as a legitimate tax deduction. Rewards under Rewards Programs are not assessed as taxable income by the ATO.

Convenient Free Ride notes:

"If Rewards Programmes 'Reward Points' are converted to flight tickets, luxury items or cash and the Credit Cardholder of the 'Citi Select Credit Card' (or comparable) is -

(a) an employee and the Credit Card is provided by the employer, then the ATO should deem such receipts as a fringe benefit and therefore income taxable; and

(b) not an employee, then the ATO should deem such receipts as taxable income in the same manner that the ATO deems bank interests receipts as taxable income."

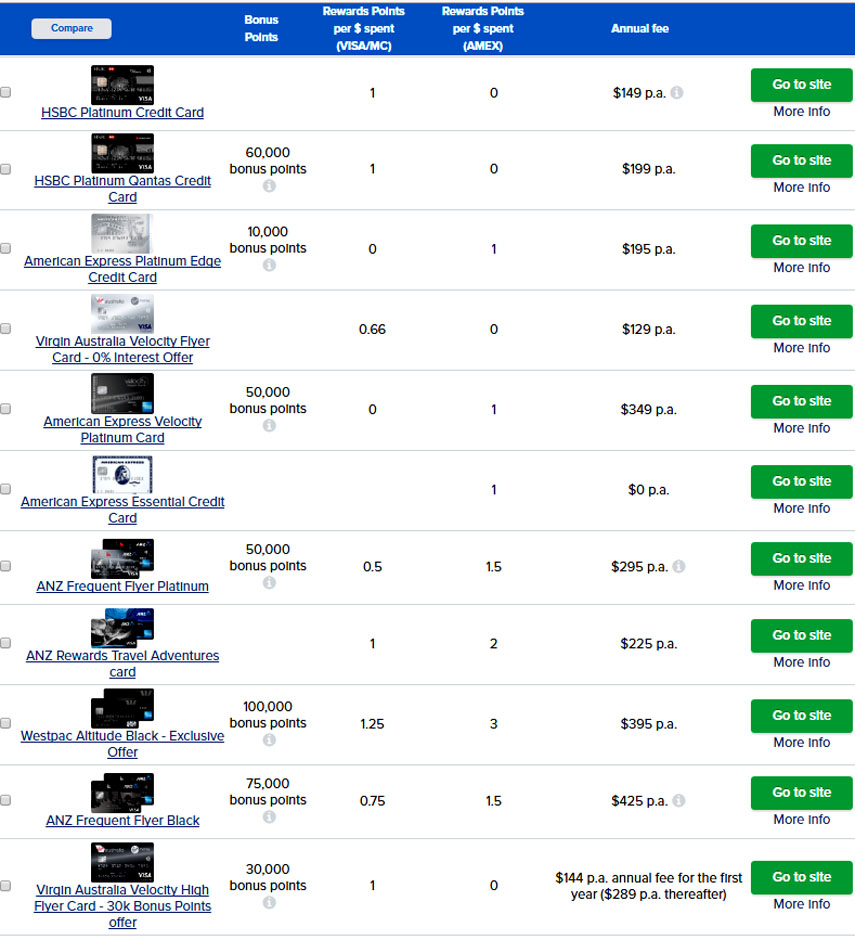

Look at 'Bonus Points' and 'Rewards Points per $ spent' below:

When accepting payment by Credit Card, Merchants pay a percentage of the transaction amount known as the Merchant Service Fee which includes an Interchange Fee which incongruously largely funds Rewards Programs.

Rewards based Credit Card Products like receiving cash back are more beneficial to consumers who pay their credit card statement off every month. Rewards based products generally have higher Annual percentage interest rate on Purchases and Cash Advances. If the balance were not paid in full every month the extra interest would eclipse any rewards earned. Most consumers do not know that their rewards-based credit cards charge higher fees to the vendors who accept them without vendors having any notification.

"The rise of rewards cards and complimentary extras (2000s to present)

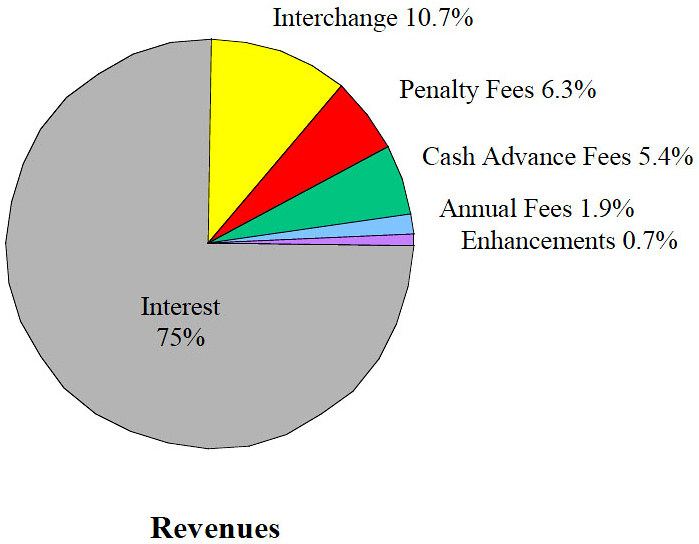

The RBA's Submission 20 to the Senate Economics References Committee in Aug 2015 noted that Rewards Programs are funded "...in large part..." from Interchange Fees. Yet 80% circa of Revenues received by Credit Card Issuers are from net Interest Revenue and Late Payment Fees revenue.

{kind=link}

Submission to the Financial System Inquiry 8. Developments and Innovation in the Payments System notes :

Below is an extract from "Fewer perks, but more competition from credit card rule change - SMH - Clancy Yates - 30 Jun 2017 that evidences that Reward Points are worth less and less:

"Interest rate comparison website Mozo said Westpac, NAB and CBA would all cut the rate at which customers earn loyalty points on companion cards from July, and NAB would cap the amount of rewards points that could be earned each month.

Mozo's director of marketing, Kirsty Lamont, said that on average, customers needed to spend almost $20,000 to receive enough points for a $100 gift voucher. That is an increase of $1789 in the required spend, compared with two years ago.

"The upshot is the value of your reward program is being absolutely slashed. It now takes a lot more spending to earn what you did previously," Ms Lamont said.

The generosity of credit card loyalty schemes was already declining before the latest changes, after the Reserve Bank last year introduced a cap on interchange fees paid by Visa card and Mastercard to the banks."

Credit card reward value falls 63 per cent over past year - SMH - 1 September 2017 - John Collett