Credit Card Debt Accruing Interest

ASIC's Money Market website showed that $32.287 billion (at 1 March 17) of Australia's Credit Cardholders' total Outstanding Indebtedness of $51.5 billion is accruing Interest - based on Reserve Bank of Australia statistics.

The Four Pillars account for around 80 per cent of the credit card market.

14-041MR Smart people not so smart with their money - ASIC

-

-

Over half a million Australians carry more than $5,000 in credit card debt [1]. It may come as a surprise to know that it is often middle income earners, managers and degree qualified people who are most likely to carry $5,000 or more compared to the general population.

-

Research by Roy Morgan shows 22% of Australians over the age of 18 earn more than $70,000 per year, and these people make up 42% of those who carry credit card debt over $5,000.

-

12% of the population are managers and managers make up 26% of those with debt above $5,000.

-

42% of Australians have a degree or diploma they represent 49% of those carrying $5,000 or more in credit card debt.

-

Around 2 million Australians do not pay off their personal credit card debt in full each month, rising from 24% of personal credit card holders in 2009 to 27% of personal credit card holders in 2013 [3].

-

Australians have over $34 billion owing on credit cards where interest is being charged and pay $6.2 billion a year in interest [4].

Findings from Roy Morgan’s Single Source survey of over 50,000 consumers pa which includes detailed coverage of over 39,000 with major cards in "High incomes run up relatively less debt on major cards" - Dec 12, 2016 note:

"In the 12 months to October 2016, holders of major cards (VISA, MASTERCARD, AMEX) intended to carry forward to their next statement an average monthly debt of $19 billion between them. The main contributors to this were the lower-income card holders, who on average owed an amount equivalent to a much higher proportion of their incomes than the higher-income groups."

Below is an extract from RBA Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - August 2015 - Submission 20 - Senate Economics References Committee - Introduction

"Credit card debt

Each month, cardholders receive statements of their use of credit for transactions over the previous month. For a cardholder who has paid off their previous balance in full, credit cards typically offer an interest-free period of up to 55 days on new transactions, given that the cardholder typically has about 25 days following the end of the statement period to repay the statement balance. If the balance is not paid off in full, interest becomes due from the date of each transaction (and the cardholder will not benefit from an interest-free period the following month).

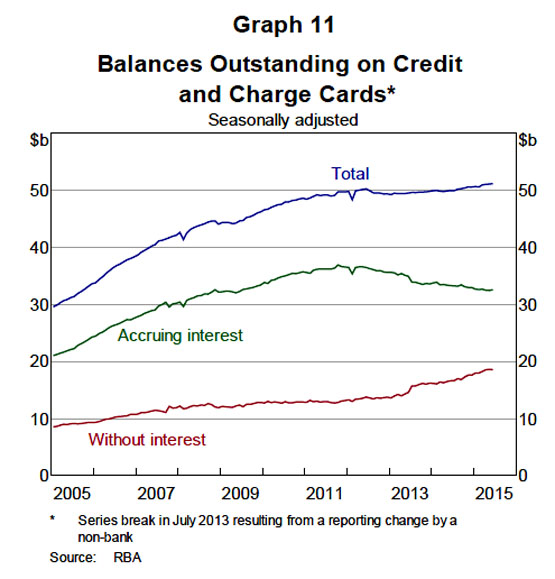

In the June quarter of 2015, new credit card transactions averaged around $24 billion per month. At the end of June, the total level of credit card debt was $51.5 billion (Graph 11). Of this amount, $33.1 billion, or around 65 per cent was bearing interest. A simple calculation would suggest that around 75-80 per cent of transactions on credit cards do not accrue interest. That is, interest-paying ‘revolvers’ account for about 30-40 per cent of accounts, about 20-25 per cent of transactions, but close to two-thirds of the outstanding stock of debt.

9

The proportion of the stock of debt that accrues interest has fallen from around three-quarters of balances in 2012. Balances accruing interest have also fallen in absolute terms after peaking in late 2011 (Graph 11). This decline possibly reflects a range of factors such as changes in consumers’ financial behaviour, government reforms in 2012 relating to repayments and limit increase arrangements, and possibly also the effect of competition for balance-transfer offers.

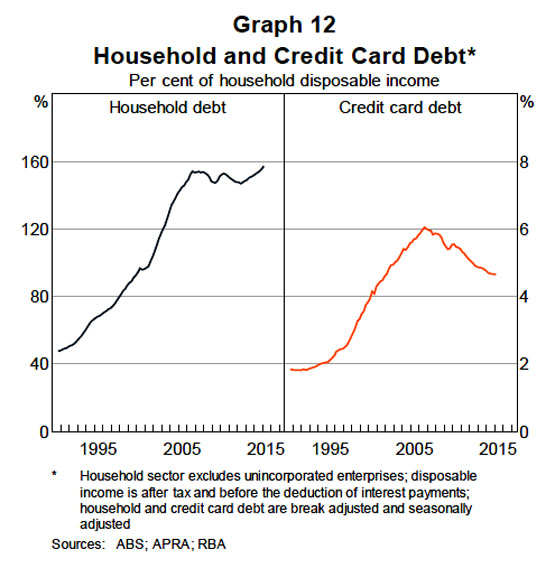

More broadly, credit card debt has represented a declining share of household borrowing over the past decade. Credit card debt peaked as a share of household debt at around 4½ per cent in 2001 but now represents a little below 3 per cent of household debt. While the ratio of overall household debt to income has been relatively steady over the past decade, the ratio of credit card debt to household income has declined (Graph 12). The decreased share of credit card debt may partly reflect the high cost of credit cards relative to mortgage interest rates and the increasing ability of households to use mortgage offset and redraw facilities as a source of low-cost funds. These products have become increasingly common over the past decade or two, with most loans now including such a facility (see RBA (2015b)). The amount available under these facilities has grown from less than 10 per cent of household income in early 2008 to over 20 per cent of household income (or around $220 billion) in mid 2015.

See:

Credit Risk To Credit Card Issuers

Cost of Credit Cards to Merchants

Interest rates on credit card debt

Cost of Credit Card transactions to Cardholders