Interest And Fees Revenue means Credit Card Issuers under Four-Party Schemes and Three Party Schemes derive a material amount of their annual revenue from -

* Fees Levied On The Wholesale Supply Side; and

* Credit Cardholder Fees and Interest (on the Retail Supply Side) where approx 33% of Credit Cardholders known as Revolvers pay -

(i) interest on Purchases (after any prevailing Interest Free Period) and Cash Advances (from the date of any Cash Advance) often levied at Usurious Unsecured Personal Loan Interest Rates;

(ii) Forfeit Interest Free Period Purchase Interest often levied at Usurious Unsecured Personal Loan Interest Rates on Purchases for up to three consecutive months upon not paying the entire Closing Balance for the previous month by the Payment Due Date as evidenced in -

* Example 1 - Unconscionable Conduct - St George Visa Card; and* Example 2 - Unconscionable Conduct - Coles 'No Annual Fee MasterCard' and Coles 'Rewards MasterCard'

(iii) other fees levied on the Retail Supply Side are not limited to Annual Cardholder Fee, Balance Transfer Fee, Cash Advance Fee, Foreign Transaction Fee, Late Payment Fee, Over-the-Limit Fee and Surcharge Fee.

"RateCity.com.au estimates Australia’s total credit card interest bill for January 2022 was $257 million. This is based on a balance accruing interest of $17.39bil @ RBA estimated average credit card rate of 17.38 per cent." It is likely that the RBA's average credit card rate is the ave. Credit Card Purchase Interest Rate. However, 20% of this $257 million indebtedness could be on Cash Advances paying 5% or higher interest rates.

The RBA publishes a veritable welter of financial statistics on many financial instruments. Relying on RBA Excel file c01hist.xlsx Philip Johnston created adjoining worksheets 'CreditCardsSummayData' and 'KeyCreditCardStats'. He estimates that aggregate interest levied on Credit Cards in Australia upon Revolvers during the year ended 30 Sept 2022 was $3.889 billion circa based on an average interest rate of 21.5%.

Latitude Financial's 'Go MasterCard' had a Cash Advance interest rate of 29.49% until March 2019. Presently it is 25.9%, but now incorporates a Cash Advance Fee of $3 or 3% of the cash advance amount, whichever is greater = 28.9%. It also charges an explicit 'Late fee' of $35 and $8.95 monthly account service fee when outstanding balance is greater than $10. Little wonder that Credit Cardholders with low Financial Literacy Capacity (independently classified by the Productivity Commission, ABS and ASIC) get lured into applying for a Latitude Financial GO Mastercard because of deceptively offering 'Enjoy now. Pay later. Interest Free'.

Extract from RBA's Consultation Document titled Executive Summary - Reform of Credit Card Schemes in Australia: RBA's "A Consultation Document" – December 2001 notes under point 6 of 'Introduction':

"Within the latter group, there is a third group which directly contributes very little to the costs of credit card schemes – these are the cardholders (known as ‘transactors’) who settle their credit card account in full each month. Although they normally pay an annual fee, they pay no transactions fees, enjoy the benefit of an interest-free period and in many cases earn loyalty points for each transaction."

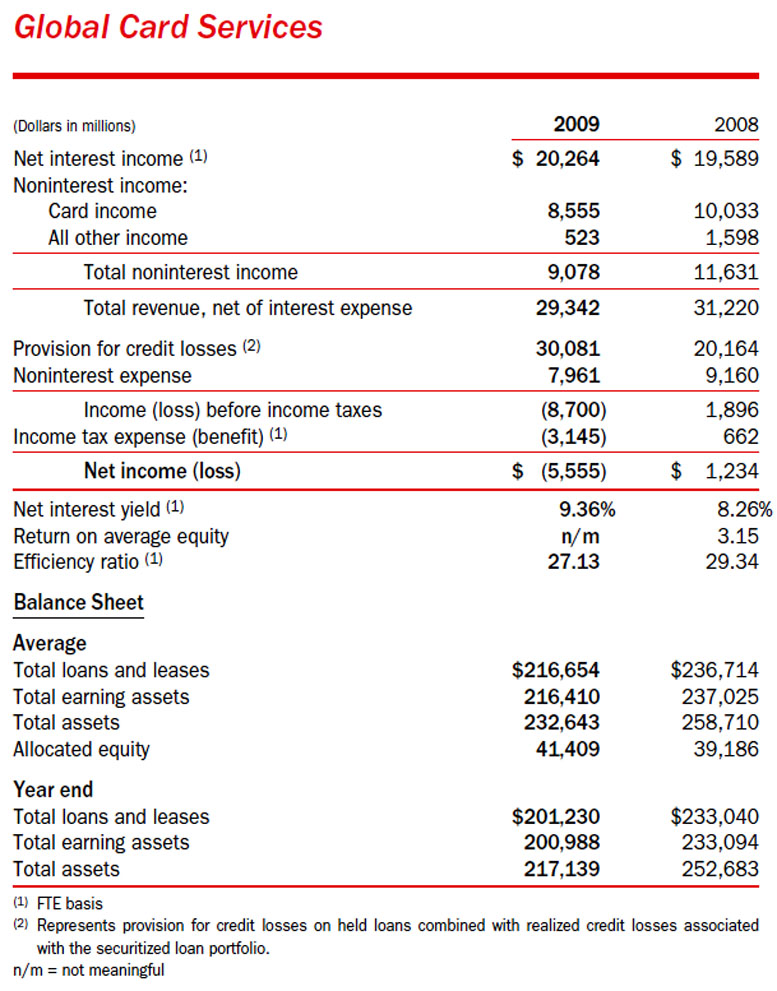

Vital information on the percentage of revenue sourced from the Retail Supply Side and the Wholesale Supply Side (eg. the percentage of revenue from Credit Cardholder Fees and the percentage from Merchant Service Fees) is remarkably scant - perhaps not remarkable. A 2009 annual report by Bank of America reported that its 'Global Card Services' division sourced roughly two thirds of revenue came from the Cardholder Fees and one third from Merchant Service Fees.

{kind=link}

Chapter 5 explains that Revolvers that hold 33% circa of the 16.65 million Credit Cards in Australia in 2017) paid all Interest and Penalty Fees Revenue which covers all Credit Card Issuers operating costs, incl. Rewards Programs and write-offs/fraud.

Australian Retailers Association - Submission to RBA - Credit Card Schemes in Australia noted that "Over 30% of card issuer income is generated by interchange (Source: Reserve Bank of Australia)".

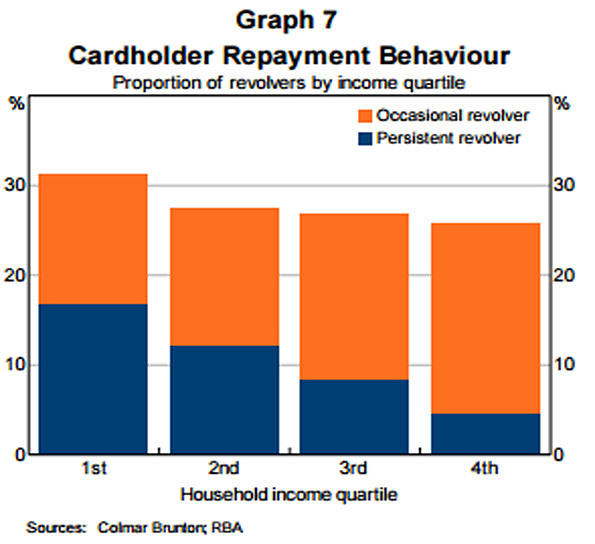

12.58% circa of Credit Cardholders, namely Australia's Persistent Revolvers (referred to by McKinsey in the USA as 'Financially stressed') identified in the below RBA Graph 7 "Cardholder Payment Behaviour" (in RBA report RBA Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - Aug 2015) have paid 80% circa of Interest and Penalty Fees Revenue.

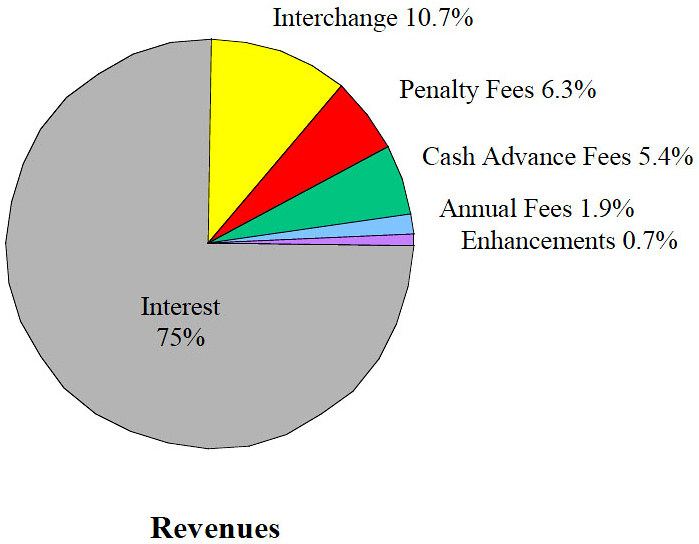

Interest and Penalty Fees Revenue represent 80% circa of Credit Card Issuers' Gross Revenue. After removing Merchant Service Fees (ostensibly Interchange Fees and Card Acquirer Fees) from Credit Card Issuers' Gross Revenue, Interest and Penalty Fees Revenue paid by Persistent Revolvers accounts for 89% circa of Credit Cardholders' "Contribution To Gross Revenue".

Further substantiated in Interest and Penalty Fees Revenue and Interest and Fees Revenue.

| Occasional Revolvers | Persistent Revolvers | ||

| 1st (lowest) Household income quartile | 50% | 50% | |

| 2nd (second lowest) Household income quartile | 55% | 45% | |

| 3rd (second highest) Household income quartile | 66% | 34% | |

| 4th (highest) Household income quartile | 80% | 20% | |

| 251% | 149% | ||

| 251% | 62.75% | Occasional Revolvers | |

| 149% | 37.25% | Persistent Revolvers | |

| 400% | 100.00% |

|

See:

Interest And Penalty Fees Revenue