|

| |

Extensive

Regulatory Powers and Responsibilities of the RBA to All

Australians

"The Reserve Bank is the

principal regulator of the

payments system

through the PSB."

Below are 5

Sections that explain the RBA's 'extensive powers'

and responsibilities,

including thinking outside the square as

obligated in Sections 3. & 4. below):

1.

Reserve Bank control over

deposit/investment and loan interest

rates that it relied upon to cap

deposit/investment rates from 1969 to

1980

Chapter

17

explains that the

Banking Act 1959 as amended

includes the below authority, under

Section 50,

which the Reserve

Bank exercised to set

both deposit/investment and loan

interest rates upon commercial banks

with diligence from

1969 until 1980:

"Control of interest rates:

(1) The Reserve Bank may, with the

approval of the Treasurer, make

regulations:

(a) making

provision for or in relation to the

control of rates of interest payable to

or by

ADIs,

or to

or by other persons in the

course of any banking business carried

on by them;

(b) making

provision for or in relation to the

control of rates of discount chargeable

by ADIs, or by other persons in the

course of any banking business carried

on by them;

(c) providing that

interest shall not be payable in respect

of an amount deposited with an ADI, or

with another person in the course of

banking business carried on by the

person, and repayable on demand or after

the end of a period specified in the

regulations; and

(d) prescribing

penalties, for offences against the

regulations, not exceeding:

(i)

if the offender is a natural person--a

fine of $5,000; or

(ii)

if the offender is a body corporate--a

fine of $25,000."

SMH article "Banks need reining in, but an act is not the way" by

Professor Milind Sathye dated

22 Oct 2010 included:

"Parliament has already

conferred powers on the government to control interest rates, under

section 50 of the Banking Act 1959."

|

|

2. Reserve Bank's responsibility to seek

necessary financial information from the ADIs, or the

major ADIs, in order to comply with (2)(a), (b)

and (c) in Point 3. below

Part 5—Miscellaneous, Section

26 'Persons to give Reserve Bank

information'

of

The

Payment Systems (Regulation) Act

1998

gives the Reserve Bank 'extensive

powers' to gather information

from a

payment system or from individual

participants."

"The Payments System Board was established by

the Commonwealth Govt. in 1998 so as to

best contribute to: .......... and

promoting competition in the market for

payment services."

Red

Book 2011 "Payment,

clearing and settlement systems in

Australia - 2011"

notes:

"The

Payment Systems (Regulation) Act 1998 also gives the RBA

extensive powers

to gather information from payment system participants

and operators."

"The Payments System Board of the

Reserve Bank was established on 1

July 1998, with a mandate to promote

the safety and efficiency of the

payments system in Australia. This

marked a watershed in governance of

the payments system. The new

regulatory regime, introduced in

response to the Financial System

Inquiry (the Wallis Committee), was

an acknowledgment of the importance

of the payments system to financial

stability and of the scope to reap

significant gains in efficiency.

***

The Board has been given the backing

of strong regulatory powers,

unique among central

banks. At the

same time, the Government has

indicated its preference for a

co-regulatory approach and it has

balanced the Board's powers with

safeguards for private-sector

operators.

To date, the Board's strategy has

been to treat its powers as ‘reserve

powers’ to be exercised if other

methods of persuasion and

implementation prove to be

ineffective. Its main

priority over its first year has

been to undertake a detailed

stocktake of the safety and

efficiency of the Australian

payments system, as the basis for

determining an initial work

program."

The Reserve Bank's

Submission

to the Financial System Inquiry - March 2014

noted:

"In 1998, the government

implemented a range of reforms that were generally in line with the broad

structure and powers recommended by the Wallis Committee. The responsibility for

oversight of the payments system was entrusted to the PSB. The PSB’s

responsibilities and powers are set out under four key pieces of legislation:

*

Reserve

Bank Act 1959,

*

Payment Systems

(Regulation) Act 1998 (the PSRA),

*

Payment Systems and Netting Act 1998

(the PSNA), and

*

Part 7.3 of the Corporations Act."

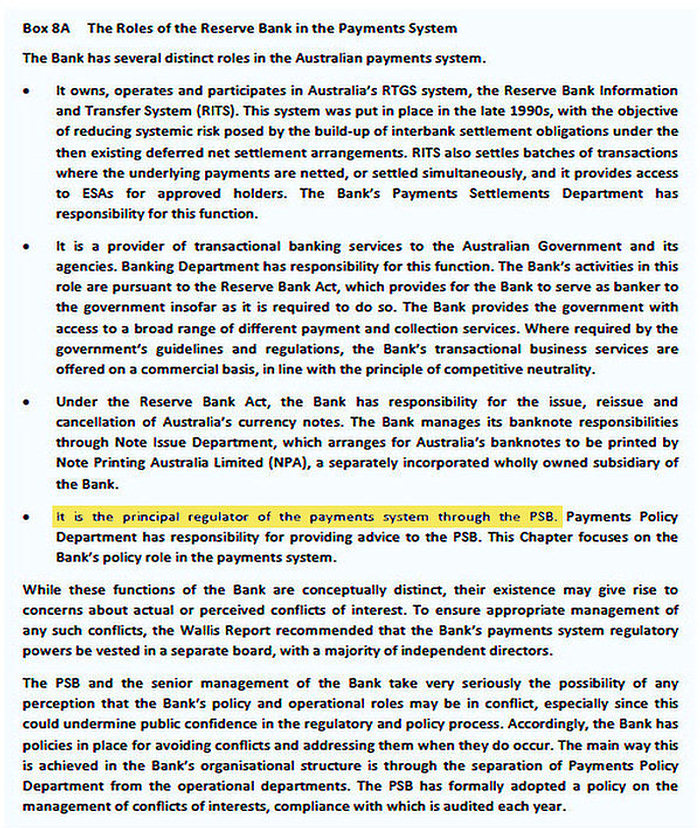

"The

Reserve Bank’s policy-making role is one of the four different roles of the Bank in the

payments system (see ‘Box 8A: The Roles of the Reserve Bank in the Payments

System’).

The Reserve Bank is the

principal regulator of the

payments system

through the PSB.

Payments Policy

Department has responsibility for providing advice to the PSB."

"The

Payment Systems (Regulation) Act 1998 gives the Reserve Bank of Australia

'extensive powers' to gather information from

a payment system or from

individual participants."

"The Payments System Board was

established by the Commonwealth

Govt. in 1998

so as to best contribute to:

.......... and promoting

competition in the market for

payment services."

Below is an extract of part of

' Box

8A

: The Roles of the Reserve Bank

in the Payments System’

referred to just above:

***

The Reserve

Bank of Australia's -

A.

powers to gather financial

information from ADIs; and

B.

responsibilities to

'inter alia'

"best

contribute to.......... the

economic prosperity and welfare of the

people of Australia",

are

"unique among central

banks"

and

more

extensive/inflexible

than the -

1.

Bank of England,

that was not

nationalised as

Britain's central bank

until 1946, which is a

corporation wholly owned

by the UK government -

the 'Corporate governance: Board responsibilities' –

SS5/16 (Short form) focus on the Corporates it

regulates with no

apparent obligation to

best contribute to the

peoples of Britain; and

2.

U.S. Federal Reserve

that was established as

the United States'

central bank in 1913

has the below obligation

to "

research to

increase understanding

of the impacts of

financial services

policies and practices

on consumers and

communities."

in the below item

7. "Promoting Consumer Protection and

Community Development.":

"The Federal Reserve

advances supervision,

community reinvestment,

and research to increase

understanding of the

impacts of financial

services policies and

practices on consumers

and communities."

|

|

3. Reserve Bank's

"catch-all"

responsibility, pursuant to the below

Reserve Bank Act (1959), Part II, Section 10

''Functions of Reserve Bank Board",

to

determine the policy of the Bank in relation

to any matter, other than its payments

system policy, and to take such action as is

necessary to ensure 'inter alia'

(2)(c) below:

(1) Subject to this Part, the Reserve Bank

Board has power to determine the

policy of the Bank in relation to any matter, other than its payments system

policy, and to take such action as is necessary to ensure that effect is

given by the Bank to the policy so determined.

(2) It is the duty of the Reserve Bank Board, within the limits of its

powers, to ensure that the monetary and banking policy of

the Bank is directed

to the greatest advantage of the people of Australia

and that the powers of

the Bank under this Act and any other Act, other than the

Payment Systems (Regulation) Act 1998, the

Payment Systems and Netting Act 1998

and Part 7.3 of the

Corporations Act 2001, are exercised in such a manner as, in the opinion of

the Reserve Bank Board, will best contribute to:

(a) the stability of the currency of Australia;

(b) the maintenance of full employment in Australia; and

(c)

the economic prosperity and welfare of the people of Australia.

Reserve Bank

of Australia - Our Role

(and the 2nd paragraph in

Chapter

5) establishes that

-

*

The

Payment Systems (Regulation) Act 1998 gives the Reserve Bank of Australia

extensive powers to gather information from a

payment system or from individual participants.

* the Reserve Bank Board’s

obligations with respect to monetary policy are laid

out in

Sections 10(2) and

Section

11(1) of the

Act.

Sections 10(2) of the

Reserve

Bank Act 1959, which is often referred to as the

Bank’s ‘charter’, says:

‘It is the duty of the

Reserve Bank Board, within the limits of its

powers, to ensure that the monetary and banking

policy of the Bank

is

directed to the greatest advantage of the people

of Australia and that the powers of the Bank ...

are exercised in such a manner as, in the

opinion of the Reserve Bank Board, will best

contribute to:

-

the stability of the

currency of Australia;

-

the maintenance of

full employment in Australia; and

-

the

economic prosperity and welfare of the

people of Australia.’

|

4.

The PSB

is responsible for promoting competition

in the market for payment services,

consistent with the overall stability of

the financial system

The RBA is the principal

regulator of the payments system through

the PSB

This responsibility has

broadened the Bank's traditional focus

on the high-value wholesale payment

systems which underpin stability, to

encompass the retail and commercial

systems

where large transaction volumes provide

scope for efficiency gains

"Designation is the first

step in 'establishing standards' and

'access regimes'

for a

payment system

to deal

with public interest issues."

Below are extracts from

Reserve Bank of

Australia Bulletin - July 1998 -

Australia’s New Financial Regulatory

Framework that

chronicles the Reserve Bank's powers,

set out in the

Payment Systems (Regulation) Act 1998,

that allow the Reserve Bank to undertake

more direct regulation of ‘designated’

payments systems to –

"... promote competition in the market

for payments services, consistent with

the overall stability of the financial

system..."

when it judges it to be

"in the public interest" which

may involve the imposition of access

rules or operating standards for

participants in such systems:

"The new Payments System Board is

responsible for the Bank’s payments

system policy, the objectives of which

are:

• controlling risk in the financial

system arising from the operation of the

payments system;

• promoting the efficiency of

payments systems; and

• promoting competition in the

market for payments services, consistent

with the overall stability of the

financial system.

The Bank’s powers in this area, set out

in the

Payment Systems (Regulation) Act 1998,

allow it to undertake more direct

regulation of ‘designated’ payments

systems when it judges it to be in the

public interest. This may involve the

imposition of access rules or operating

standards for participants in such

systems. The Act also provides a

framework for regulation of purchased

payment facilities, such as travellers

cheques and stored-value cards."

"The Payments System Board has just

released its 1999 Report outlining its

activities during its first year.

The Board's strategy has been to

treat its extensive powers as

‘reserve powers’

to be exercised if other methods of

persuasion and implementation prove to

be ineffective. Where it can, it

would much prefer to rely on

information-gathering and consultation

with industry participants to meet its

objectives. This is the co-regulatory

approach envisaged by the Government."

The PSB's mandate is set out in the

Reserve Bank Act 1959.

The PSB is responsible for

-

* determining the RBA's

payments system policy in a way that

will best contribute to controlling risk

in the financial system;

* promoting the efficiency of

the payments system; and

*

promoting competition in

the market for payment services,

consistent with the overall stability

of the financial system.

-

The Reserve Bank

Act 1959

establishes the

Payments System

Board.

Section 10B(3) of

the Act states:

-

'It is the duty

of the Payments

System Board to

ensure, within

the limits of

its powers,

that:

-

the Bank's

payments

system

policy is

directed

to

the greatest

advantage of

the people

of Australia;

and

-

the powers

of the Bank

under the

Payment

Systems

(Regulation)

Act 1998

and the

Payment

Systems and

Netting Act

1998

are

exercised in

a way that,

in the

Board's

opinion,

will best

contribute

to:

-

controlling

risk in

the

financial

system;

and

-

promoting

the

efficiency

of the

payments

system;

and

-

promoting

competition

in the

market

for

payment

services,

consistent

with the

overall

stability

of the

financial

system…'.

While the PSB determines the RBA's

payments system policy,

the powers to

carry out those policies are vested in

the RBA. These powers are set out in

three separate Acts, 6 of which the

centrepiece is the Payment Systems

(Regulation) Act 1998, under which the

Bank may:

*

"designate"

a particular payment system as being

subject to RBA regulation.

Designation is simply the first of a

number of steps the Bank must take to

exercise its powers;

* determine rules for

participation in a payment system,

including rules on access for new

participants;

* set Standards for safety and

efficiency for any payment system. These

may deal with issues such as technical

requirements, procedures and performance

benchmarks; and

* arbitrate on disputes in

that system over matters relating to

access, financial safety,

competitiveness and systemic risk, if

the parties concerned so wish.

The Payment Systems (Regulation) Act

1998

also gives the RBA extensive powers to

gather information from payment system

participants and operators.

In 1998, the government

implemented a range of reforms that were generally in line with the broad

structure and powers recommended by the Wallis Committee. The responsibility for

oversight of the payments system was entrusted to the PSB. The PSB’s

responsibilities and powers are set out under four key pieces of legislation:

*

Reserve Bank Act 1959,

*

Payment Systems (Regulation)

Act 1998

(the PSRA),

*

Payment Systems and Netting Act 1998

(the PSNA), and

*

Part 7.3 of the Corporations Act.

The

Bank’s policy-making role is one of the four different roles of the Bank in the

payments system (see ‘Box 8A: The Roles of the Reserve Bank in the Payments

System’).

The RBA is the principal

regulator of the payments system through the PSB. Payments Policy

Department has responsibility for providing advice to the PSB.

The Government's intent was that the

Bank would treat these powers

as 'reserve

powers', to be exercised if

other means of promoting efficiency,

competition and stability proved

ineffective. Accordingly, the Government

built considerable flexibility into the

new regulatory regime. Under this

co-regulatory approach, the private

sector continues to operate its

payment systems and may enter into

cooperative arrangements, which may be

authorised by the ACCC under the

Competition and Consumer Act 2010.

However, if the Bank believes that there

may be benefits in exercising its formal

powers in a system that it oversees to

improve access, efficiency or safety, it

may, as a first step, invoke its powers

to designate that system. It may then

decide, in the public interest, to set

an Access Regime or impose Standards for

that system. In doing so, the Bank is

required to take into account the

interests of all those potentially

affected, including existing operators

and participants. Full public

consultation is required and the Bank's

decision-making processes are subject to

judicial review.7

"Increasingly, central banks are being given

explicit authority for payments system safety and

stability,

but the Board's legislative responsibility and

powers to promote efficiency and competition in the

payments system are unique.

This

responsibility has broadened the Bank's traditional focus on the high-value

wholesale payment systems which underpin stability, to encompass the retail

and commercial systems where large

transaction volumes provide scope for efficiency gains.

The Bank's

wide-ranging powers in the payments system are set

out in the

Payment Systems (Regulation) Act

1998. It may:

The

Payment Systems (Regulation) Act 1998

also gives the Reserve Bank of Australia (RBA)

extensive powers to gather information from a

payment system or from individual participants."

Relying upon Clause 8 of the Payment

System (Regulation) Act 1998, the

Reserve Bank may, in writing, determine

standards to be complied with by

participants in a designated payment

system

if it considers that

determining the standards is in the public interest.

-

The authority to

designate a payment

system is conferred

on the Bank by

Section 11 of the

Payment

Systems (Regulation)

Act 1998. The

Act states that 'The

Reserve Bank may

designate a payment

system

if it

considers that

designating the

system is in the

public interest'.

Section 8 of the Act

defines the meaning

of public interest:

-

"In determining,

for the purposes

of this Act, if

particular

action is or

would be in, or

contrary to, the

public interest,

the Reserve Bank

is to have

regard to the

desirability of

payment systems:

-

being (in

its

opinion):

-

financially

safe for

use by

participants;

and

-

efficient;

and

-

competitive;

and

-

not (in its

opinion)

materially

causing or

contributing

to increased

risk to the

financial

system.

The Reserve Bank may

have regard to other

matters that it

considers are

relevant, but is not

required to do so."

|

|

5.

Determine Standards to 'inter alia'

re-cap Credit Card interest rates

for 'public interest issues':

1.

'Designated'

Credit Card Schemes in Australia on 12 April 2001,

relying on

Division 2, Section 11 of the Payment Systems

(Regulation) Act 1998

2.

'Impose

an Access Regime'

on 23 Feb 2004 on each of the

three designated credit card schemes in Australia (Visa, MasterCard and

Bankcard)

relying upon

Division 2, Section 12 of the

PAYMENT SYSTEMS (REGULATION) ACT 1998;

and

3.

Determining 'Standards' pursuant to

Division 4, Section 18 of the

Payments System Regulation Act 1998

|

Wallis Inquiry report noted:

*

"The ACCC and the Payment System

Board should monitor the delivery fees charged on credit and debit cards

while the ACCC should monitor the rules of international credit card

associations to ensure they are not overly restrictive.

*

"Fifth, accountability requires that

regulatory agencies operate independently of sectional interests, be subject to

regular reviews and evaluations and be open to scrutiny by their stakeholders."

*

"There is scope

for increased competition in the payments system which will help to lower its

costs of operation. However, this must be balanced against the need to maintain

stability in the financial system. The payments system provides one central way

in which instability can be generated.

The RBA should retain

overall responsibility for the stability of the financial system, the provision

of emergency liquidity assistance and for regulating the payments system."

At the beginning of the

definition of

User Pays

Principle is noteworthy evidence

that

Australia's Principal Regulator of the Payments

System,

namely the Reserve Bank issued "RBA's

Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001

with

lofty

goals to apply the

User Pays

Principle

to -

(i) better meet the public interest

by lower interest rates and fees; and

(ii)

lower

Interchange

Fees levied upon Merchants through requiring

the

Four Party

Schemes to publish their

Interchange Fee

rates:

"The

Bank determined that it would be in the public

interest to designate these systems (bank‐issued

American Express companion card system, the

Debit MasterCard system and the eftpos,

MasterCard and Visa prepaid card systems)

and, following a resolution of the Board, did so

in October 2015. The designation of a system is the

first of a number of steps that the Bank must

take to exercise any of its powers, such as

imposing an access regime or setting standards."

The

Unpleasant Truth About Australian Banking

notes:

"Before 1981, activities of major Australian

banks, including the manner they dealt with

customers,

were

subject to detailed regulations imposed by the Federal Government. Following the 1981 Campbell

Committee Report, banking regulations were significantly reduced."

Mindful of

RBAInfo's email to the

Writer sent 30 Jan 17, should the author of

The

Unpleasant Truth About Australian Banking

have written

"imposed

by government.",

that is to use a lower case 'g' and omit

Federal.

Or maybe not?

See:

*

Parliamentary Bestowed Mandate

*

Australia's Principal Regulator of the Payments

System

*

Some facts about the Reserve Bank of Australia

*

RBA - Our Role

*

Monetary

Policy

*

Payments System Board

| |

|

{kind=link}