Example 1 - Unconscionable Conduct - St George Visa Gold Card

A friend of the Writer is Pete aka CampyAficinado. Pete has a St. George Visa Gold Card # 4_64 _5_1 0_91 _3_0

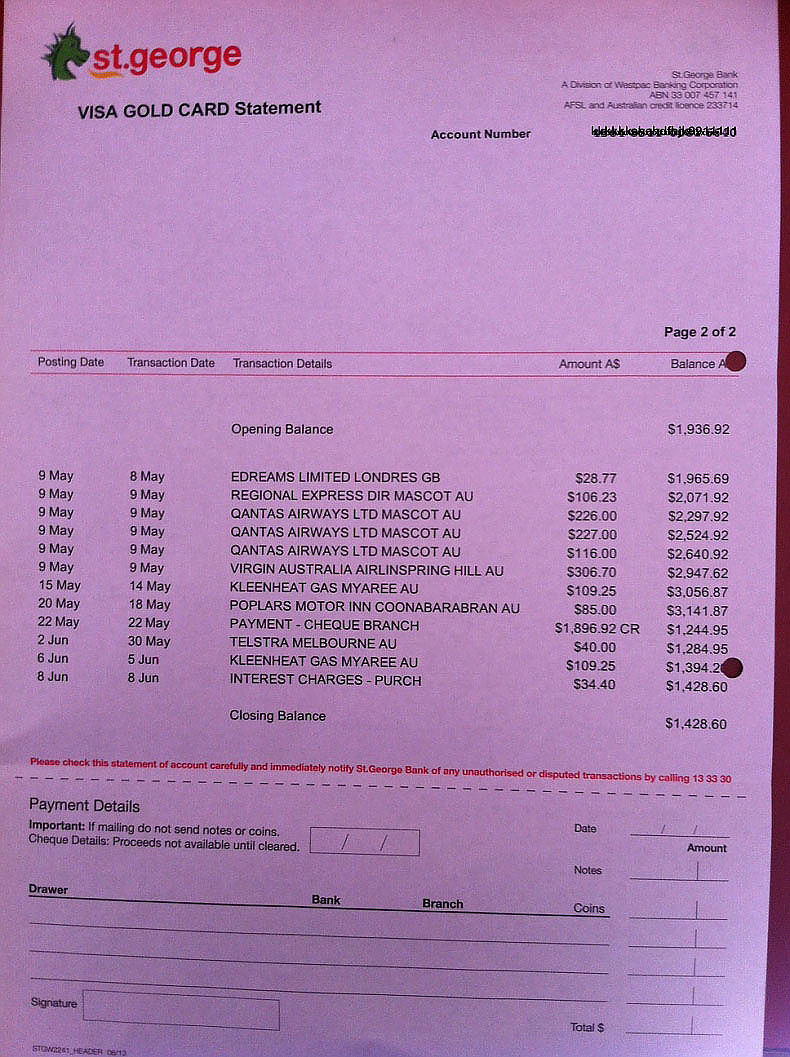

'Statement Period' for 9 April ‘14 to 8 May ‘14 lists a Payment Due Date of 2 June '14 for Peter to pay the Closing Balance of $1,936.92 so as to not get charged interest @ 20% on his Purchases. Peter paid $1,896.92 on 22 May '14 which was a shortfall of $40 on his Closing Balance of $1,936.92. Pete intended to pay the $40 shortfall from another bank account, but forgot to.

Peter's next monthly statement for 'Statement Period' 9 May '14 to 8 June '14 shows that Peter was charged interest of $34.40 on 8 June ‘14 for all his Purchases which aggregated to the previously listed Closing Balance of $1,936.92 @ 20%, notwithstanding that St. George Bank had received $1,896.92, being 97.94%, of Peter's Closing Balance 10 days prior to the Payment Due Date.

{kind=link}

St George Bank also withdrew Peter's Interest Free Period for the following two months, because of the 2.16% shortfall in payment of his Closing Balance, being $40. St. George Bank relied upon the below paragraph of Clause 18.1 "Interest charges on purchases and our fees" of its "Conditions of Use - Credit Guide (Effective: 20 May 2014) of a 62 page document in Arial 8 font because Peter did not pay the entire Closing Balance of $1,936.92 but paid $40 less.

What came as a bigger shock was when Peter downloaded and read clause 18.1 titled ''Interest charges on purchases and our fees" and then 'phoned St. George's Phone Help Desk 13 33 30 and asked it to explain the below yellow highlighted paragraph and the subsequent paragraphs in clause 18.1:

The St. George's Phone Help Desk eventually explained that Peter would be charged interest on all his Purchases at the Usurious Unsecured Personal Loan Interest Rate of 20% for the next two months. Peter was able to take some comfort that should he prepay to St. George Bank outstanding Purchases, then he would only be levied interest @ 20% for only those days where the Purchases were not repaid.

This practice by St. George Bank and many other Credit Card Issuers of charging a Usurious Interest Rate is Unconscionable Conduct which relied upon the ACCC's webpage Unconscionable conduct.

St. George Bank patently lies when advertising its Credit Cards on its website:

-

Up to 55 interest free days on purchases when you pay the closing balance in full by the statement due date because it makes no mention that the Interest Free Period is not available for the following two months even if the Cardholder repays its Closing Balance by the Payment Due Date in the subsequent.

Pete aka CampyAficinado paid the Closing Balance on the subsequent two months but did not receive "...Up to 55 interest free days on purchases for those two months.

Both the webpage advertising the Vertigo Platinum Visa Card and the Amplify Visa Card both represent that:

˃ Up to 55 interest free days on purchases when you pay the closing balance in full by the Statement Due Date

Below is an extract from the bottom of page 2 of St. George Bank's "Conditions of Use - Credit Guide (Effective: 20 May 2014) which has 62 pages of the 64 pages document in Arial 8 font.

“……We strongly recommend that you read this booklet carefully and retain it for your future reference. If you do not understand any part of it, please contact our staff on 13 33 30. They will be happy to explain any matter for you.”

Relying upon the Productivity Commission and the ABS rankings for the domains/categories of Numeracy and Literacy skills, less than half of the top Level 5 Cardholders could comprehend several of the clauses in the above 62 pages Conditions of Use - Credit Guide with 60 pages written in tiny 8.5 Helvetica font. St. George "... strongly recommends that you read this booklet carefully....". Clause 18.1 "Interest charges on purchases and our fees" has evidenced a lot of St George Cardholders losing their Interest Free Period for a minimum of three months and paying 20% on all Purchases from the date of each Purchase

Financially Uneducated And Vulnerable Australians, Financial Literacy and Numeracy And Literacy Range Of Australians provide empirical evidence that almost 50% of Australians aged between 18 and 75 possess only Level 1 or Level 2 Literacy and Numeracy skills which are patently too low to read and comprehend the St. George Bank's "Conditions of Use - Credit Guide.

There are several consequential clauses in this Conditions of Use - Credit Guide with similar negative financial impact as clause 18.1 which is why St. George Bank includes the above “……We strongly recommend that you read this booklet carefully. It is 64 pages of convoluted legalese as evident on attempting to understand afore-mentioned clause 18.1.

The National Consumer Credit Protection Amendment (Home Loans and Credit Cards) Act 2011 which obligates all Credit Card Issuers to "Make it mandatory for credit-card application forms to include a clear summary of key account features."

Below is a 'paste' of a deceitfully contrived summary of key information in Peter's 'Statement Period' for 9 April ‘14 to 8 May ‘14 which, if Peter was to pay only the 'Minimum Payment - Due' of $39 as instructed at Payment Due $39.00, then Peter would immediately -

{kind=link}

A.) be charged interest on all his Purchases for that month at the Usurious Interest Rate of 20%; and

B.) forfeit his interest free days (between 28 and 42 days) for the next two months and be charged interest on all his Purchases for those two future months at the Usurious Interest Rate of 20% from the date of Purchase.

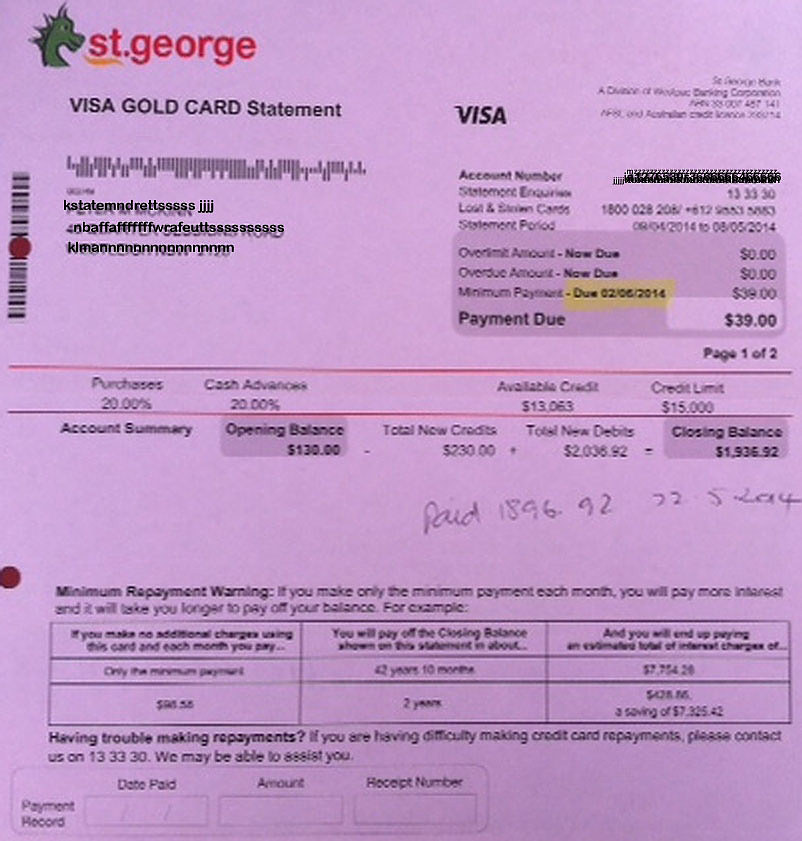

Below is the full page 1 of Pete's statement. The Closing Balance (further down the page) is highlighted in Bold. 'Payment Due $39' should not appear.

This practice by St George Bank and possibly some other Credit Card Issuers of listing in Bold Font Payment Due $39.00 which is only 2% of the Closing Balance of $1,936.92 is Unconscionable Conduct and would immediately render the Credit Cardholder -

(i) charged interest @ 20% of all Purchases for the previous month; and

(ii) forfeit his/her Interest Free Period for the subsequent two months, meaning being charged interest at the Usurious Interest Rate of 20% from the date of any/all Purchases, as explained in Forfeit Interest Free Period And Pay Interest On Each Purchase From The Purchase Date.

What is the Credit Card Key Facts Sheet (KFS)? - St. George Bank breaches 'information provision obligations' required SCHEDULE 6.

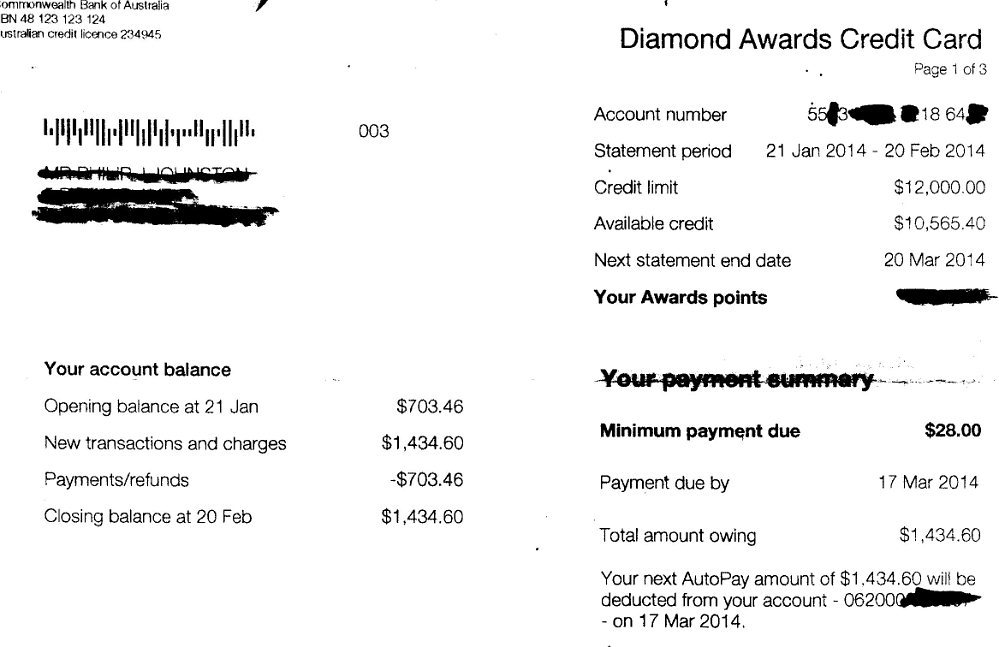

The Reserve Bank should legislate 'a standard format for Summary Credit Card Information' that is similar to the CBA statement below. The Minimum Payment should NOT be highlighted. Any interest and fees that would be triggered if only the Minimum Payment is made should be listed: