|

|

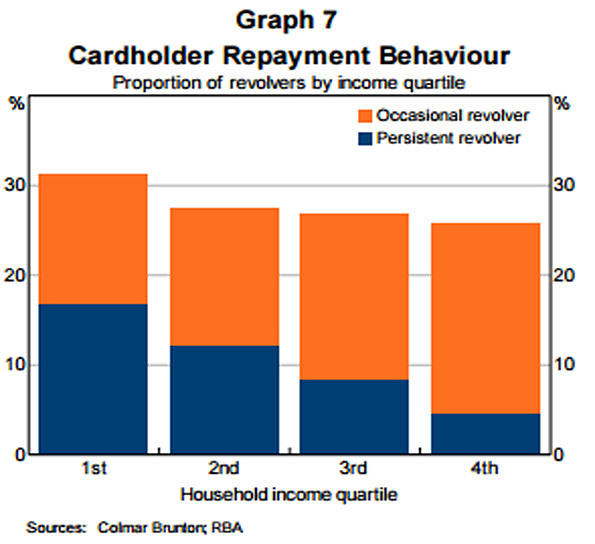

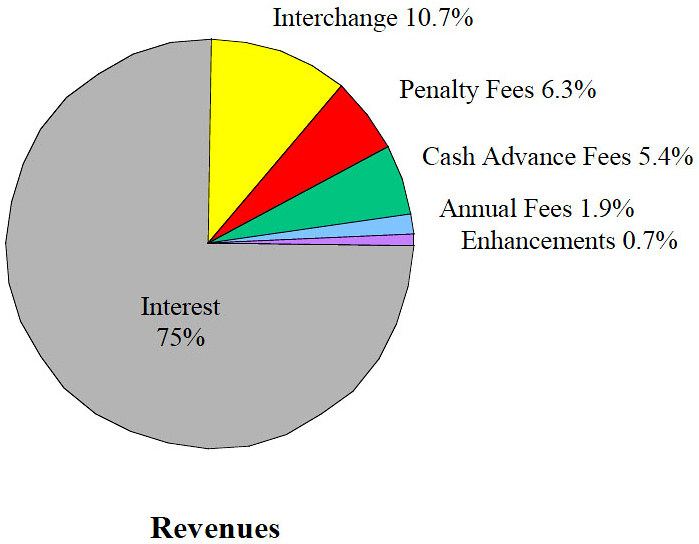

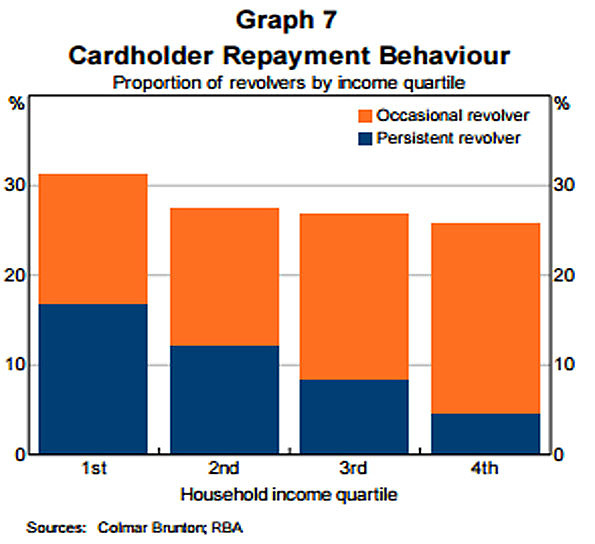

Three Landmark RBA Published Papers in the last 26 years that recognised the ever increasing spread between the Overnight Cash Rate and Highest Credit Card Interest Rates As identified by the RBA in Graph 7 'Cardholder repayment behaviour', Persistent Revolvers invariably possess only Level 1 or Level 2 Financial Literacy Capacity (as measured by the Productivity Commission and the ABS). Persistent Revolvers have paid a horrible price since the 18% cap on Credit Card interest rates was removed by the RBA in April 1985 – Latitude Financial's Money Go MasterCard credit card had a Cash Advance interest rate of 29.49% until March 2019. It is now 25.9%, but now incorporates a Cash Advance Fee of $3 or 3% of the cash advance, whichever is greater = 28.9%. Latitude Financial's Money Go MasterCard charges its Cardholders a nasty fee, even if they blink. There are over 16 million Credit Cards in Australia. Persistent Revolvers hold 12.58% circa of those 16 mil Credit Cards. Persistent Revolvers pay 80% circa of the Interest, Penalty Fees and Cash Advance Fees shown in the Credit Card Revenue pie chart. -------------------------------------------------------------------------------

1st Publication -

June 1992

2nd Publication -

Dec 2001

21. Having weighed a range of arguments from interested parties, the Reserve Bank is of the opinion that the main regulations established by the credit card schemes in Australia do not meet the public interest test."

The Reserve Bank may use its powers to impose an access regime or determine a standard if it is in the public interest to do so. The public interest test is the critical test for any intervention in the normal competitive processes of the market, whether it be proposed action by regulatory authorities or potentially anti-competitive conduct by market participants (which must be authorised under the Trade Practices Act 1974)." 5.2 Scheme regulations and competition benchmarks includes:

T he Executive Summary - Reform of Credit Card Schemes in Australia: RBA's "A Consultation Document" – Dec 2001 notes that -I. "...One group are those cardholders who use the revolving line of credit, who pay interest rates significantly above rates on other forms of unsecured lending." (".....who use the revolving line of credit refers to Credit Cardholders who do not repay their Closing Balance by the Payment Due Date, but rather carry a large Outstanding Indebtedness at around 20% p.a. interest rate.) II. "Nor is it surprising that banks and other deposit-taking institutions are promoting most actively the credit card because it is the payment instrument for which they receive the highest return" III. "This regulatory structure is unique in Australia; a comparable set of restrictions (in Australia) has not been permitted in any other market without authorisation under the Trade Practices Act 1974." (This highlights the ''extensive powers'' that the Reserve Bank possess, but has not deployed to identify which Credit Cardholders are paying the vast bulk of Interest And Penalty Fees Revenue by asking the 13 Questions.) 3rd Publication - August 2015 RBA Submission 20 to the Senate Inquiry into Matters Relating to Credit Card Interest Rates evidenced that, notwithstanding that the above '2nd Publication' that asserted "A movement towards a “user pays” approach to credit card payment services would be consistent with the approach adopted by Australian financial institutions in pricing other payment instruments under their control" was published over 20 years ago, the User Pays Principle still did not apply any more to Retail Supply Side of credit cards in Australia: * Graph 7 titled ''Cardholder Payment Behaviour" quantified the gross interest burden upon Persistent Revolvers [and earlier similar RBA findings noted in Persistent Revolvers and Revolvers] that possess very low Financial Literacy Capacity and fall within Financially Uneducated And Vulnerable Australians represent 12.58% circa of the 7,515,000 Credit Cardholders (June 2016), namely 945,000 [cell b36] Credit Cardholders (ASIC 'Credit card debt clock' 27-Apr-17) pay a whopping 80% circa of Interest And Penalty Fees Revenue levied by Credit Card Issuers annually; and * Noted that "..... In addition, many credit card holders take advantage of interest-free periods such that they do not pay interest on their card balances " identified by the RBA as Transactors. The term, Persistent Revolvers, was first identified by the Reserve Bank in Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - Aug 2015 - Submission 20. It appears in the below Graph 7 titled "Cardholder Payment Behaviour" on page 6. The explanation of (v) to (xii) [listed above] is set out below. Senate Report - Interest rates and informed choice in the Australian credit card market - 16 Dec 2015 in Chapter 2 - "Overview of the Australian credit card market" notes:

The definition of Persistent Revolvers evidences the enormous share of Credit Card Issuers revenues that are paid by Persistent Revolvers that represent only 12.58% circa of the 7,515,000 Credit Cardholders (June 2016) As an example Persistent Revolvers pay 80% circa of all Interest and Penalty Fees Revenue generated from Credit Card Products. Interest and Penalty Fees Revenue accounts for over 80% of all Credit Card Issuers Revenues. The RBA has failed to rectify that patent inequality, notwithstanding the RBA's undertaking in 5.2 above to act. |

|

|

|

{kind=link}

{kind=link}

{kind=link}