|

|

Australia's Principal Regulator of the Payments System or "The Reserve Bank is the principal regulator of the payments system through the PSB" or Parliamentary Bestowed Mandate means the Role of the Reserve Bank of Australia, as decreed under the - includes "....to ensure that the monetary and banking policy of the Bank .... is directed to the greatest advantage of the people of Australia and that the powers of the Bank ... are exercised in such a manner as, in the opinion of the Reserve Bank Board, will best contribute to ...... the economic prosperity and welfare of the people of Australia.'’

"This document sets out the Reserve Bank's policies for dealing with potential conflicts of interest arising from its roles as the principal regulator of the payments system and as provider of banking services to the Australian Government." Below are extracts from Reserve Bank of Australia Bulletin - July 1998 - Australia’s New Financial Regulatory Framework that chronicles the Reserve Bank's powers, set out in the Payment Systems (Regulation) Act 1998, that allow the Reserve Bank to undertake more direct regulation of ‘designated’ payments systems to – "... promote competition in the market for payments services, consistent with the overall stability of the financial system..." when it judges it to be "in the public interest" which may involve the imposition of access rules or operating standards for participants in such systems: "The new Payments System Board is responsible for the Bank’s payments system policy, the objectives of which are: • controlling risk in the financial system arising from the operation of the payments system; • promoting the efficiency of payments systems; and • promoting competition in the market for payments services, consistent with the overall stability of the financial system. The Bank’s powers in this area, set out in the Payment Systems (Regulation) Act 1998, allow it to undertake more direct regulation of ‘designated’ payments systems when it judges it to be in the public interest. This may involve the imposition of access rules or operating standards for participants in such systems. The Act also provides a framework for regulation of purchased payment facilities, such as travellers cheques and stored-value cards." The Reserve Bank brought credit card schemes in Australia under its regulatory oversight on 12 April 2001. However, the PSB Standards (CONVENIENTLY) did not cover the setting of credit card fees and charges to cardholders and merchants, or interest rates on credit card borrowings".

On 23 Feb 2004, the Reserve Bank imposed an Access Regime on each of the three designated credit card schemes (Visa, MasterCard and Bankcard) in Australia which 'inter alia' removed the ACCC's obligations to monitor these three credit card schemes as chronicled in the MOU between the RBA and the ACCC which includes:

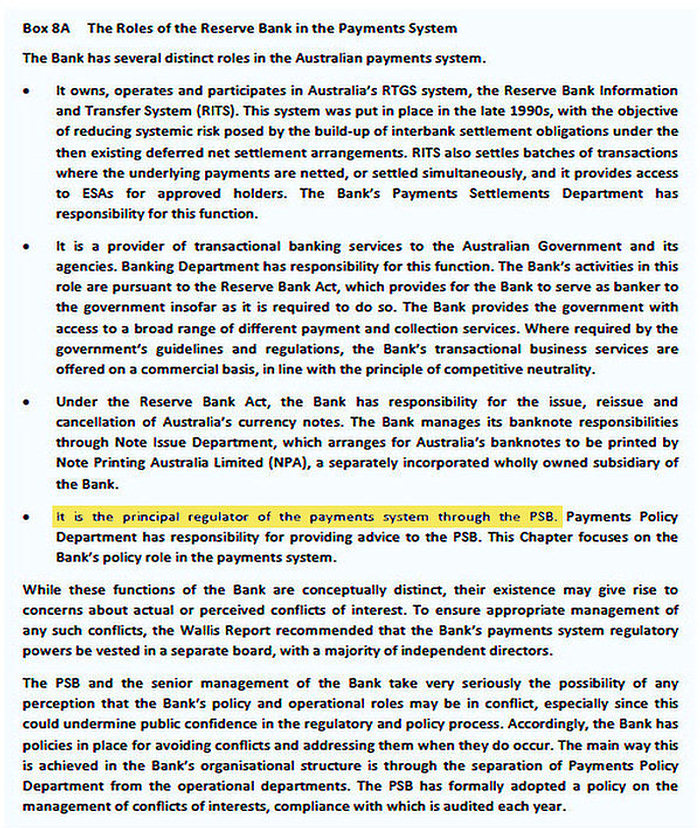

The Reserve Bank's Extensive Powers and Responsibilities of the RBA to All Australians notes: A. The Board has been given the backing of strong regulatory powers, unique among central banks.*** At the same time, the Government has indicated its preference for a co-regulatory approach and it has balanced the Board's powers with safeguards for private-sector operators. B. The Reserve Bank is the principal regulator of the payments system through the PSB (see ‘Box 8A: The Roles of the Reserve Bank in the Payments System’).

*** The Reserve Bank of Australia - A. has powers to gather financial information from ADIs under Part 5—Miscellaneous, Section 26 of the Payment Systems (Regulation) Act 1998; and

B.

has

responsibilities to

'inter alia'

"best

contribute to.......... the

economic prosperity and welfare of the

people of Australia" in terms of

Section 10(2) 'Functions

of Reserve Bank Board' of Reserve Bank Act 1959 which

includes

- to set Standards that "are in the public interest" relying on Division 4, Section 18 of the Payments System Regulation Act 1998 for a Payments System that it Designated on 12 April 2001 (under Division 2—Section 11 of the Payment Systems (Regulation) Act 1998; and to re-regulate commercial bank interest rates relying on Section 50 of the Banking Act 1959 that "are in the public interest",

Chapter 17 explains that the Banking Act 1959 includes Section 50 which the Reserve Bank exercised to set both deposit/investment and loan interest rates upon commercial banks with diligence from 1969 until 1980.

The RBA ignored the Wallis Report by doing naught to require Credit Card Issuers to lower interest rates in line with the fall in the Cash Rate.

Chapter Nine: 'Stability and Payments' of The Wallis Report on the Australian Financial System: Summary and Critique - 23 June 1997 proposed:

The abovementioned reference to Chapter Nine (in Chapter 15 above): 'Stability and Payments' of the Wallis Enquiry noted "the RBA should retain overall responsibility for the stability of the financial system, the provision of emergency liquidity assistance and for regulating the payments system." .."The ACCC and the PSB should monitor the delivery fees charged on credit and debit cards while the ACCC should monitor the rules of international credit card associations to ensure they are not overly restrictive."

|

|

|

|

{kind=link}