|

| |

Defined Terms and Documents

Transactors and Revolvers means:

National Credit Reform:

Enhancing Confidence and Fairness in Australia’s Credit Law

dated July 2010 notes:

"Credit card users are generally recognised to fall into two

broad categories — Transactors and Revolvers:

* Transactors

(67% circa of Credit

Cardholders) pay their outstanding balances on time

and therefore incur no interest charges.

* Revolvers

(33% circa of Credit Cardholders) tend to carry (or revolve)

their debt,

making minimum repayments or slightly more, and thus maintain a level of continuing debt. Due

to their outstanding balances and repayment habits, Revolvers pay more interest, and tend to

have higher default rates."

"The majority of credit card users (by

number) in Australia are Transactors, consumers who pay outstanding balances in full on or before the time the minimum monthly

repayments fall due and thus do not incur interest rate or penalty charges."

"Revolvers, who make up

the other category of credit card user (and who account for the majority of total outstanding

balances on credit cards), pay the minimum monthly repayments or some larger fraction of the

outstanding balance and are exposed to the typically high interest rates levied

on the unpaid amount."

Financially Uneducated And Vulnerable Australians

notes:

"The

majority of credit card users (by number) in Australia are

‘Transactors’, consumers who pay outstanding balances in full on or before the time the minimum monthly

repayments fall due and thus do not incur interest rate or penalty charges. 4

4

The number of Australians paying their credit card balances

in full every month has risen since the mid 2000s to over 63 % by 2009 according to statistics from the

Household, Income and Labour Dynamics in

Australia survey: see Ellis Connolly and Daisy McGregor, ‘Household Borrowing

Behaviour: Evidence from HILDA’ (2011) March Quarter Reserve

Bank Bulletin 9, 13. This is consistent

with credit card use in other mature economies, including the United States: Robert J Mann,

Charging Ahead: The Growth and

Regulation of Payment Card Markets (2006, Cambridge University Press) 75. However, the Reserve Bank of

Australia statistics indicate that revolvers account for a majority by value

of the aggregate balance

outstanding on credit cards: Reserve Bank of Australia, Statistical Table C1: Credit and Charge Card Statistics

(Last updated 14 Nov 2011) (since August 2002,

when the Reserve Bank first published this information, the aggregate amount of

balances accruing interest has consistently accounted for a majority of the total balances outstanding).

‘Revolvers’, who make up

the other category of credit card user (and who account for the majority of total outstanding

balances on credit cards), pay the minimum monthly repayments or some larger fraction of the

outstanding balance and are exposed to the typically high interest rates levied

on the unpaid amount. 5"

5

The 2011 Dunn and

Bradstreet Consumer Credit Expectations Survey found that 34% of Australian

households expect to face some level of difficulty meeting credit card

repayments, with 8% of participants stating that meeting repayments would be ‘very difficult’: Dunn and Bradstreet,

Consumer Debt Expectation Survey

(June 2011) 34. The 2010 Australian Debt Study found that 12% of survey participants

had missed a minimum credit card bill repayment: Galaxy Research, Australian Debt Study Report,

March 2010.

Credit Card Debt Accruing Interest

notes:

“In the June quarter of 2015, new credit card transactions averaged around $24

billion per month. At the end of June, the total level of credit card debt was

$51.5 billion (Graph 11). Of this amount, $33.1 billion, or around 65 per cent

was bearing interest. A simple calculation would suggest that around 75-80 per

cent of transactions on credit cards do not accrue interest. That is,

interest-paying ‘revolvers’ account for about 30-40 per cent of accounts, about

20-25 per cent of transactions, but close to two-thirds of the outstanding stock

of debt.9” Extract

from Submission 20 by the RBA

"Seventy-three per cent of credit card

holders participating in the survey reported that they typically paid off their

account in full by the due date each month (within the interest-free period).

While this implies that only 27 per cent of cardholders pay interest charges,

some industry estimates suggest that a slightly higher proportion (between 30

and 40 per cent) of cardholders pay interest; it is possible that survey

responses reflect hoped-for rather than actual behaviour."

Extract from Submission 20 by the RBA

The

RBA's 2013 Consumer Use Survey showed that 73 per cent of cardholders participating in the survey typically pay off their

account in full within the interest free period, implying that 27 per cent typically do

not. Industry estimates suggest the proportion of cardholders who typically pay interest

is slightly higher, at between 30 and 40 per cent. The RBA ventured that the gap

between its survey results and industry data may reflect hoped-for, rather than actual

behaviour on the part of consumers.22"

|

Transactors

Credit card

Transactors make only a very small contribution to the revenues earned by

credit card issuers (Table 5). Transactors pay, at most, an annual fee to

hold a credit card but receive interest-free credit and may be eligible for

loyalty points which accrue in proportion to the value spent on their credit

card. Around one quarter of credit card balances outstanding do not attract

interest. Based on information provided to the Joint Study by card scheme

members, revenues received from transactors from annual fees fall short of

the cost of providing the interest-free period and loyalty points by around

$90 million a year. That is, Transactors are subsidised by this amount each

year.

The below extract from

RBA's Consultation Document

titled

Executive Summary -

Reform of Credit Card Schemes in Australia:

RBA's "A Consultation Document" –

Dec 2001

notes -

* under point 6 of 'Introduction'

that some

Credit Cardholders

enjoy the

convenience of their

Revolving Line/s of Credit

without

materially contributing to

Credit Card Issuers'

operating costs:

"Within the latter group, there is a third group which directly

contributes very little to the costs of credit card schemes – these are

the cardholders (known as

Transactors) who settle their credit card

account in full each month. Although they

normally pay an annual fee, they pay no

transactions fees, enjoy the benefit of an

interest-free period and in many cases earn

loyalty points for each transaction."

* on page 15:

"The other two-thirds of total

issuing revenues is generated by cardholders who make use of the

revolving line of credit (“revolvers”),

that is, who do not pay off their accounts by the end of the

interest-free period. Preliminary data from the Reserve Bank’s new

payments system collection indicate that about three-quarters of credit

card outstandings are interest-bearing. Credit cardholders who use

the credit card purely as a payment instrument (“transactors”),

that is, who pay off their balance by the end of the interest-free

period, make only a very small contribution to total issuing revenues,

mainly through annual fees."

Many

Transactors

are

Convenient Free Riders that

enjoy

considerable

convenience of 'swiping their plastic'

(reliant upon costly

electronic infrastructure of the

Four Party

Schemes and

Three-Party Schemes) to make hundreds of

Purchases each

year, and not pay for their

Purchases for up to 55 days. The majority

of

Transactors make

Purchases that

aggregate to over $20,000 pa. Many receive over $100 per year in

Reward Programme

Points - income tax and FBT free. Some claim their

Annual

Cardholder Fee as a tax deduction.

The American Express

Platinum Business Card has an Annual Fee of $1,500 (tax deductible) and

provides copious untaxed personal income.

It

"..... would cease to

exist if and when the ATO required recipients of the flyer-point income-in-kind

to declare it as income and pay tax on it."

|

|

Revolvers

Financially Uneducated And Vulnerable Australians

notes that approx.

20% of

Credit Cardholders,

which include

Persistent Revolvers

and some

Occasional Revolvers,

in Australia who are over 18 years of age and -

1.

Lack Financial Acumen due to

possessing low

Financial Literacy

Capacity;

and/or

2. suffer from

Compulsive Buying

Disorder,

who have paid

Interest And Penalty Fees Revenue on

Credit Cards and

are classified by the below mentioned

Productivity Commission Staff Working Paper as

'level 1' or 'level 2'

Financial Literacy

Australians

The Senate - Economics References Committee's submission "Interest

rates and informed choice in the Australian credit card market" -

December 2015 notes:

"2.9

While

the RBA advised that

about 75 to 80 per cent of credit card transactions do not

accrue interest, about 65 per cent of the total quantum of

credit card debt (or, as noted above, $33.1 billion) is accruing

interest. To clarify, interest paying cardholders 'account

for about 30–40 per cent of accounts, about 20–25 per cent of

transactions, but close to two-thirds of the outstanding stock

of debt'.9

Below are two an

extracts from

RBA Submission

to the Senate Inquiry into Matters Relating to Credit Card Interest Rates -

Aug 2015:

"Seventy-three per cent of

credit card holders participating in the survey reported that they typically

paid off their account in full by the due date each month (within the

interest-free period). While this implies that only 27 per cent of cardholders

pay interest charges, some industry estimates suggest that a slightly higher

proportion (between 30 and 40 per cent) of cardholders pay interest; it is

possible that survey responses reflect hoped-for rather than actual behaviour. Subject to this caveat, the survey suggests that the proportion of

Revolvers is

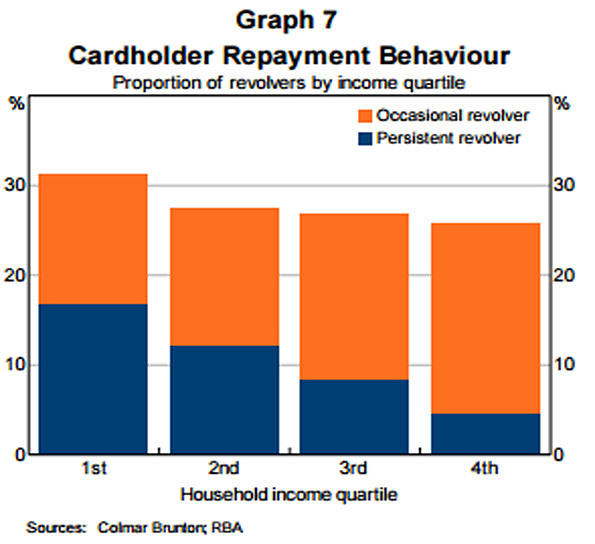

somewhat higher for lower-income households than higher-income ones (Graph 7)."

|

|

|

Occasional Revolvers |

Persistent Revolvers |

ORs |

PRs |

Agg. |

% of PRs |

|

1st (lowest) Household income quartile |

|

45% |

55% |

34 |

42 |

76 |

55.3% |

|

2nd (second lowest) Household income quartile |

|

55% |

43% |

46 |

35 |

81 |

43.2% |

|

3rd (second highest) Household income quartile |

66% |

33% |

44 |

22 |

66 |

33.3% |

|

4th (highest) Household income quartile |

|

80% |

20% |

46.5 |

11.5 |

58 |

19.8% |

|

|

|

246% |

152% |

|

|

|

|

|

|

251% |

61.87% |

Occasional Revolvers |

|

|

|

|

|

|

149% |

38.13% |

Persistent Revolvers |

|

|

|

|

|

|

400% |

100.00% |

|

|

|

|

|

Casual empiricism

of the above (Graph 7) as

calculated in the immediately above table suggests that approx. -

*

almost two thirds of

Revolvers,

referred to by the RBA as

Occasional Revolvers, pay interest

occasionally.

*

over one third of

Revolvers,

referred to by the RBA as

Persistent Revolvers, pay 17% Interest (average) on 100% of their

Credit Card Debt.

Improving consumer outcomes and

enhancing competition - Aust Govt - May 2016

"According to the Australian Bankers’ Association, around 20 per

cent of credit card accounts in 2014 — over 3 million accounts —

had outstanding balances of over $7,500.

Around 6 per cent of accounts had balances of over $15,000.

Not all of these balances will be incurring interest. However,

the Reserve Bank of Australia estimates that 30 to 40 per cent

of credit card accounts incur

interest and

that credit card users who incur interest charges have larger

balances than users who do not pay interest.

|

RBA's Submission

to the Senate Inquiry into Matters Relating to Credit Card Interest Rates -

August 2015

noted:

"In the June quarter of 2015, new credit card transactions

averaged around $24 billion per month. At the end of June, the total level of

credit card debt was $51.5 billion (Graph 11). Of this amount, $33.1 billion, or

around 65 per cent was bearing interest. A simple calculation would suggest that

around 75-80 per cent

[(51.5–33.1) ÷ 24 ≈ 0.77%]

of transactions on credit cards do not accrue interest. That is, interest-paying ‘Revolvers’ account for about 30-40 per cent of

accounts, about 20-25 per cent [1.00 - 0.77

≈

0.23%] of transactions, but close to two-thirds of the

outstanding stock of debt.9"

Below is an extract

from Australian Treasury’s Submission to Senate Economics References Committee -

August 2015

"According

to a 2013 RBA survey, only around 30 per cent of credit card users reported that

they pay interest on their credit card balances (the ‘Revolvers’)."

See:

Occasional Revolvers Persistent

Revolvers

| |

|