Numeracy And Literacy Targeting or Targeting Credit Cardholders With Low Financial Literacy Capacity means some Credit Card Issuers have engaged in Predatory Advertising of Unconscionable Credit Card Products with Concealed Spiders and charged Usurious Unsecured Personal Loan Interest Rates by overtly presented newspaper, brochure and webpages advertisement of Credit Card Products that have concealed Material Interest And Fees which have preyed upon Credit Cardholders with only 'level 1' and 'level 2' Financial Literacy Capacity (Financially Uneducated And Vulnerable Australians), "the most vulnerable in society", whereupon this susceptible demographic cohort known as Revolvers have paid effectively all Interest And Fees Revenue, whilst many of the Financially Educated Transactors have enjoyed a Free Ride with their Line/s Of Credit on their Credit Card Products at virtually no cost, with some Transactors having enjoyed, from their Line/s Of Credit, a net profit thru Rewards Programs.

This vulnerable cohort of Credit Cardholders:

(a) is recognised/identified/acknowledged by the Productivity Commission's Staff Working Paper "Links Between Literacy and Numeracy Skills and Labour Market Outcomes" dated Aug 2010 and the ABS' PIAAC 2011-12 report which evidences that over 40% of Australians possess numeracy and literacy skills less that level 3 - Chapter 1; and

(b) explained in Foundation skills attainment by COAG.

Nine Examples Of Predatory Advertising evidences patent Numeracy And Literacy Targeting and provide 'Print Screens' of offending advertisements.

The range from Level 1 to Level 5 of Financial Literacy Capacity is explained at Numeracy And Literacy Range Of The Australian Population.

Below is an extract from page vii of RBA paper "Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001" which identified that the few, identified by the RBA as Revolvers, were paying the usage costs of the many, identified by the RBA as Transactors:

"Reform of the credit card schemes

21. Having weighed a range of arguments from interested parties, t

he Reserve Bank is of the opinion that the main regulations established by the credit card schemes in Australia do not meet the public interest test."

Below is an extract from page 117 of the above-mentioned RBA Consultation Document:

198"Reform of credit card schemes will also have a direct impact on credit cardholders and is likely to result in some re-pricing of credit card payment services. However, this is the means by which the price mechanism is to be given greater rein in the credit card market. A movement towards a “user pays” approach to credit card payment services would be consistent with the approach adopted by Australian financial institutions in pricing other payment instruments under their control. As the ABA itself has confirmed: “Pricing services efficiently provides consumers with choice to use lower cost distribution channels and, therefore, facilitates a more efficient financial system. It is also fairer and efficient, because consumers only pay for what they use.

The principles that consumers should face prices that take into account the relative costs of producing goods and services, as well as demand conditions, and that resources should be free to enter a market in response to above-normal profit opportunities, have been the guiding principles for tariff reform and market deregulation in Australia. Such market reforms may impact unevenly on different groups – some gaining, some losing – but they are now the well-established route to more efficient use of resources in the Australian economy."

Notwithstanding the above two noble intentions by the RBA (back in Dec 2001) for a movement towards the User Pays Principle to the pricing (fees and interest charges) of Credit Card Products, the concerns explained in the above Consultation Document have essentially exacerbated in the subsequent 19+ years.

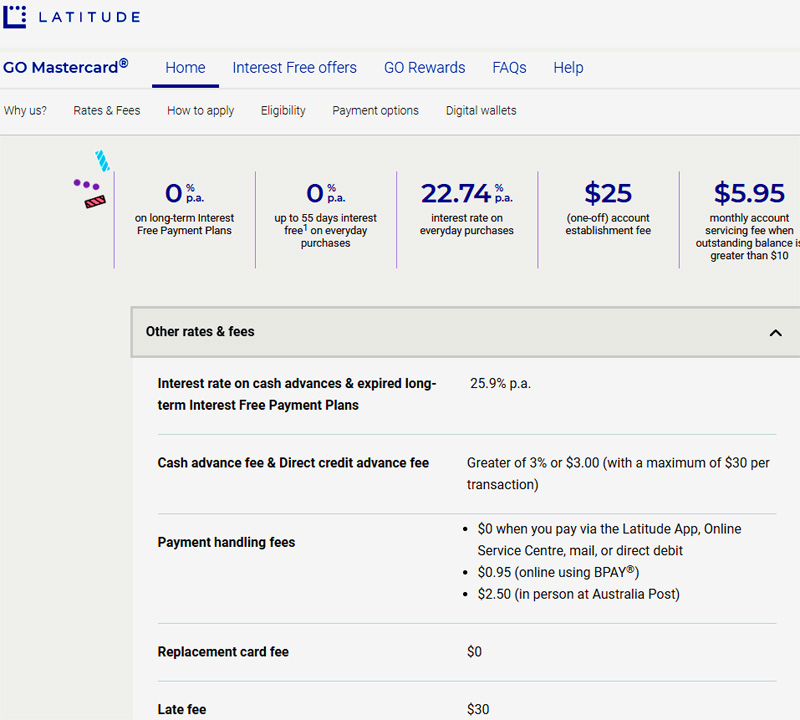

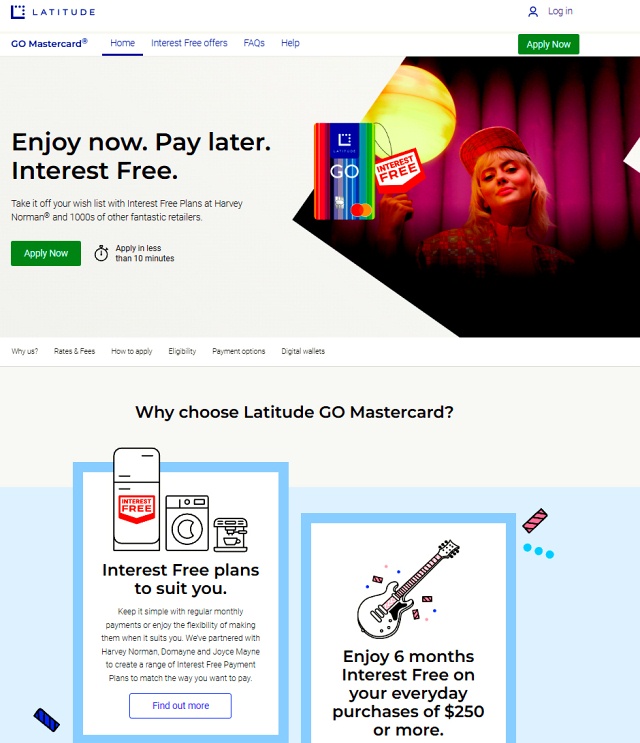

In April 1985 the 18% interest rate Cap on Credit Cards was removed when the Overnight Cash Rate was 17.2% circa - spread was less than 1%. Less than two years ago the spread between the Overnight Cash Rate of 0.10% and the highest Cash Advance interest rate (Latitude Financial's Go Mastercard) was over 28%. Latitude Financial's Go MasterCard had a Cash Advance interest rate of 29.49% until March 2019. Presently it is 25.9%, but now incorporates a Cash Advance Fee of $3 or 3% of the cash advance, whichever is greater = 28.9%. It also charges an explicit 'Late fee' of $35. Little wonder that Credit Cardholders with low Financial Literacy get lured into applying for a Latitude Financial GO Mastercard because of deceptively offering 'Enjoy now. Pay later. Interest Free'.

{kind=link}

See Numeracy And Literacy Range Of The Australian Population

Australian Social Trends - 2008 Article: Adult literacy

Mapping adult literacy performance - written by Michelle Circelli, David D Curtis and Kate Perkins

Project Team That Produced AUSTRALIAN CORE SKILLS FRAMEWORK

AUSTRALIAN CORE SKILLS FRAMEWORK

Numeracy And Literacy Authorities

Financial Literacy among Marginalised Women

Financial Literacy among Marginalised Women - On-line version

Australian Securities and Investments Commission (ASIC) "National Financial Literacy Strategy"

Financial literacy in the Australian context - ANZ Survey 2011

Numeracy And Literacy Authorities

Numeracy And Literacy Discrimination

Numeracy And Literacy Targeting

Numeracy And Literacy Range Of Australians or Numeracy And Literacy Skills

Numeracy And Literacy Skills or Skills Numeracy And Literacy Range Of Australians