Chapter 1

Productivity Commission and the ABS rank Australians as

having between Level 1 (low) and Level 5 (high) for

Numeracy and Literacy Skills.

A person assessed at Level 5 possess up to five times the skills within the

particular domain (eg Numeracy, Literacy, Prose etc) than a person assessed at Level

1.

Level 3 or above is required

"to meet the complex demands of

everyday life and work in the emerging knowledge-based economy"

ASIC

2010 report notes

"These findings

have implications for our regulatory regime, which relies upon disclosure as

a critical element of our consumer protection system."

St. George and Westpac test Credit Cardholders with even Level 5

Numeracy and Literacy Skills

by expecting all their Credit Cardholders to read/comprehend voluminous

Conditions of Use

in a tiny font.

These results, when considered together with Australian Bureau of

Statistics‘ research into Australians‘ general document literacy and

numeracy,15

in particular

their ability to meet the complex demands of a knowledge-based economy,

suggest that about one in two Australians do not have the skills required to

make informed choices in their interactions with the financial services

sector.16 There is also

an identifiable age link, with document proficiency tending to decrease with

age.

14 For

example the 2008 ANZ study of financial literacy found that ‗67% of

respondents said that they understood the principle of compound interest,

but only 28% were

rated with a good level‘ of comprehension when they solved the problem‘,

ANZ Banking Group Limited,

ANZ survey of adult financial literacy in Australia, (The Social Research Centre) ANZ Banking Group, Melbourne, 2008, p. 19.

15

As part of an

international study, the ABS measured skills in document literacy, prose

literacy, numeracy and problem solving and found that approximately 7

million (46%) of Australians (and 7.9 million (53%) of Australians aged 15

to 74) had proficiency less than the minimum required for individuals to

meet the complex demands of everyday life and work emerging in the

knowledge-based economy‘ for document literacy and numeracy respectively‘,

Australian Bureau of Statistics,

Adult literacy and life

skills survey results, cat. no. 4228.0, ABS, Canberra, 2006, p.

5.

16

These findings

have implications for our regulatory regime, which relies upon disclosure as

a critical element of our consumer protection system.

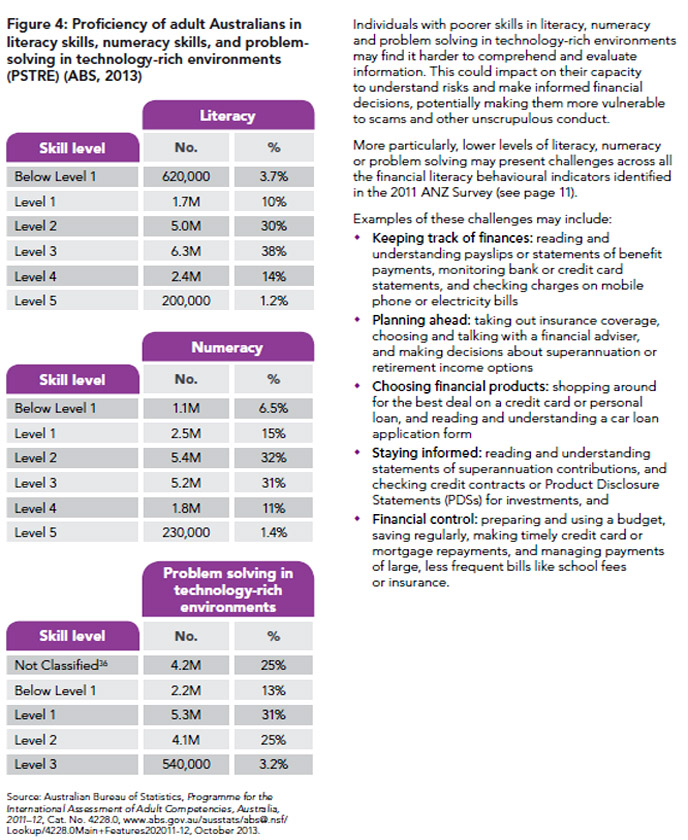

"The ABS research groups literacy and numeracy

into six skill levels (where below Level 1 is lowest and Level 5 is

highest), and problem solving in technology-rich environments (PSTRE) into

four skill levels (where Below Level 1 is lowest and Level 3 is highest).33

The Productivity Commission’s analysis of these results highlights that many

Australians have relatively low literacy and numeracy skills and this limits

the range and type of tasks that they can do in comparison with those with

relatively higher skills.34

Groups with relatively low literacy and numeracy skills include:

‘people

with low levels of education; older persons; people not working; and

immigrants with a non-English speaking background’.

35

Behavioural indicators

Research tells us that

Australians have differing attitudes to money and varying levels of

financial knowledge and proficiency.22 People may perform well on some

aspects of financial literacy, but poorly on others.23

The latest report on

Australians’ financial literacy, the 2011 ANZ Survey of Adult Financial

Literacy in Australia (ANZ Survey), is the fourth in a series of

national snapshots conducted by the ANZ Banking Group since 2003.24

Many people underestimate the

extent of their own knowledge gaps. So their behaviour, even in simple

day-to-day money management, may not be consistent with how confident they

are in their abilities. As discussed on page 8, individual financial

decision-making behaviour may also be influenced by personal or

environmental circumstances.

The 2011 ANZ Survey also highlighted a number

of areas of behavioural vulnerability, particularly in keeping track of

finances and planning ahead:

one third (36%) found dealing with money

stressful, even when things were going well

Results of the 2011 ANZ Survey confirm the complex and variable nature of

individual financial decision-making. A range of factors were found that may

help explain differences in financial literacy levels, such as financial

attitudes, age, financial knowledge and numeracy, household income, and

education and occupation.29

The Productivity Commission’s analysis of these results highlights that

many Australians have relatively low literacy and numeracy skills and this

limits the range and type of tasks that they can do in comparison with those

with relatively higher skills.34 Groups with relatively low

literacy and numeracy skills include: ‘people with low levels of education;

older persons; people not working; and immigrants with a non-English

speaking background’.35

Research shows that

Australian women typically have lower numeracy levels, find dealing with

money stressful or overwhelming and have more difficulty with

retirement-related investment decisions than men.63"

The above

extract of page 13 of the

National Financial Literacy Strategy

2014–17

notes that according to the ABS 21.5% of the Australian population do not

posses the Numeracy Skills to "shopping around

for the best deal on a credit card"

or

making timely credit card or

mortgage repayments.

"A necessary part of financial literacy is

knowing how to track your expenses and live within your means.

Data from

Roy Morgan Research in 2012 shows that, within the 16–24 age group, one in

10 carry forward more than $2,000 in credit card debt each month, suggesting

difficulties in managing money.49"

"Feedback from the 2013 Consultation also

identified the need for a mechanism to share relevant findings from existing

national surveys (for example, focusing on the savings and credit card

behaviour of Australians)."

These results, when considered together with Australian Bureau of

Statistics‘ research into Australians‘ general document literacy and

numeracy,

15

in particular their

ability to meet the complex demands of a knowledge-based economy, suggest

that about one in two Australians do not have the skills required to make

informed choices in their interactions with the financial services sector.16

There is also an identifiable age link, with document

proficiency tending to decrease with age.

The above published reports from the

Productivity Commission, ABS and ASIC is patent evidence that a

“community service

obligation” has existed for at least 20 years for

the (small 'g') government to take stringent action because during that

post-deregulation era Credit Card Issuershave -

Relying upon the Productivity Commission and the

further ABS above rankings for the

domains/categories of

Numeracy and Literacy Skills, less than half of the top Level 5

Credit Cardholders (approx 5% of

Credit Cardholders) could

read and comprehend the follow three Conditions of Use booklets from St. George,

ANZ and Westpac:

'Introduction' "The credit card

contract governs the operation of the credit card account and your use of a

credit card. It is important that you read and understand the credit card

contract. The credit card contract is set out in your Letter of Offer and Parts

A and B of this booklet."

"The

following summary is designed to highlight some of the important information

about your credit card account and to help you identify where to find further

details within this booklet. The summary is not a substitute for the terms of

Parts A and B of this booklet, which

you should still read and understand."

Part A of the booklet has 51 pages. Part B has 22 pages.

Further in 'Introduction' is:

"Finally, you should also read the notice ‘Things

you should know about your proposed credit contract’,

which is included in this booklet following Parts A and B." '

'Things you should know about

your proposed credit contract’ is 7 pages. Hence, ANZ tells its

Credit Cardholders to read the entire 97 pages of its booklet.

Clause (4) 'Allowing

use by others' includes:

"(b) The account holder is responsible to ANZ for the operation

by an additional cardholder of the credit card account and any

other account linked to the credit card account. If an

additional cardholder does not comply with the credit card

contract, the account holder will be liable to ANZ. The account

holder should therefore ensure that each additional cardholder

receives a copy of the credit card contract and reads and

understands it."

The word "interest' appears 216 times in the booklet. The word 'fee' or

'fees' appears 104 times.

Westpac has two

separate Credit Card booklets both "Effective as at 28 Oct 2016":

- "Combined

Conditions of Use and Credit Guide' for Credit Cards"

in Arial 11 font:

The word 'interest' appears in the 'Contents' once and 98 more times throughout

the 63 pages. The word 'fee' or 'fees' appears 90 times. The word

'Contract' appears 81 times.

Sub

clause (c) of clause 1.1 'Introduction' notes:

"These Conditions of Use do not, on

their own, contain all the terms applying to your Credit Card, so it

is important that you read all of the documents comprising the

Credit Card Contract carefully and retain them for future

reference."

Clause 17. 'Do I have any other rights and obligations?':

"Yes. The law will give you other

rights and obligations. You should also READ YOUR CONTRACT

carefully."

- "Ignite

by Westpac - Consumer Credit Card Conditions of Use"in

HelveticaNeue-Light 9 font.

The

word 'interest' appears in the 'Contents' once and 92 more times throughout

the 43 pages. The word 'fee' or 'fees' appears in the

'Contents' once and 74 more times throughout the 43 pages. The below statement appears on the front cover of "Ignite

by Westpac - Consumer Credit Card Conditions of Use": "This User

Guide forms part of your Credit Card Contract, along with the information

set out on the reverse of your welcome letter which advises you of your credit

limit and other prescribed information we are required to give you by law."

Clause 17 is "Do I have any other rights and obligations? Yes.

The law will give you other rights and obligations. You should also READ YOUR

CONTRACT carefully."

CBA's Credit

Cards 'Conditions

of Use' booklet in Arial 9 font is only 21 pages.

The word 'interest' appears 44 times. The word 'fee' or 'fees' appears 20

times.

Clause 1.

of the booklet titled 'Your contract with us" notes:

"Please read both these Conditions of Use and the Schedule of Credit

Card Particulars in your letter of offer, which together make up

your contract and include the information we must give you."

Chapter

2. 'User Pays Principle' is evident in the price of every commodity in the

market place, except Credit Cards

'Supply and Demand' is arguably

the most fundamental concept in economics and the foundation of any free

enterprise market economy. The 'User Pays Principle' is

the omnipresent pricing mechanism to achieve the most equitable distribution of resources in

any such market economy. It

promotes responsibility and accountability and encourages 'Supply'. 'User Pays' occurs when consumers pay the 'full

cost' of

the goods or services that they consume - if

you want to acquire a good or service in the market place, you pay the market

price be it petrol, alcohol, groceries, paying the rent, engaging a plumber or

visiting the GP.

This deep-seated

fundamental of the 'User' paying the market price for a 'good' or 'service'

applies in all sectors of any open market

economy, even in the banking

sector

(eg. housing loan, personal loan, corporate loan, syndicated infrastructure

loan, overdraft, buying a bank cheque,

issuing a personal cheque, buying a money box etc.). But

the 'User Pays Principle'

does not Credit Cards.

Chapter

3. Basic Credit Card of

55+ years ago now includes 'Sweets', 'Sours'

and

'Spiders'

The ubiquitous Credit Card is

the solitary 'service' instrument omnipresent throughout the industrialised world that has morphed -

* from a simple Charge Card

some 65

years ago where the monthly Total Amount Owing

had to be repaid in full at the end of each month in order to be allowed to

continue using the

Charge Card

Product

Differentiation is a fundamental of micro-economics - making a homologous

product (low barriers to entry) different from your competitors' similar

homologous product to attract sales. (c) to (g) above is a shining example

of Product Differentiation for the 'core purpose' of the humble plastic namely a quick swipe

to

establishes the Purchaser's 'ability-to-pay' to pay.

The term, Grace

Period, is used in North America and Europe to describe what Australians call

the Interest Free

Period.

The first universalCredit Card,

which could be used at a variety of establishments, was introduced by the

Diners' Club Inc., in 1950. Another majorCredit

Cardof

this type, known as a travel and entertainmentcard,

was established by the American Express Company in 1958. Diners Club and American Express' decision to provide a

Grace Periodas an inducement/lurewhen mass marketing their 'new fangled' Credit

Cards in the early 1960's has proven to be a marketing 'master stroke'.

A lot ofArgy Bargy

periodicallyamongst the following

lobby groups oversupply/demand impacts

and cost-based benchmarking of services/funding costs have contributed to

"competitiveness and efficiency

in pricing" on the Wholesale Supply Side of the

Debit Card and

Credit Card Systems in Australia:

* Visa,

MasterCard, Amex, Diners Club

* eftpos

*

ePal - part-owned by the Four

Pillars and also Coles and Woolworths

* Australian

Payments Clearing Association

*

AMA,

The

Pharmacy Guild, Retail Traders Association,Australian Newsagents Federation,

other Merchant

special interest groups *

TYRO Payments Limited

(b) does not

contain a powerful lobby

group to represent the interests of

Credit Cardholders (unlike the Wholesale Supply Side)to ensure equitable 'User Pay' pricing.

A Credit Card is

the only style unsecured personal loan that does not charge the customer a 'loan limit fee'

and a usage fee based on the loan

outstanding unilaterally for each usage.

the Bank’s payments

system policy

is

directed to the greatest advantage of the

people of Australia; and

the powers of the Bank

under the

Payment Systems (Regulation) Act 1998 and the Payment

Systems and Netting Act 1998 are

exercised in a way that, in the Board's

opinion, will best contribute to:

promoting competition in the market for

payment services, consistent with the

overall stability of the financial

system.

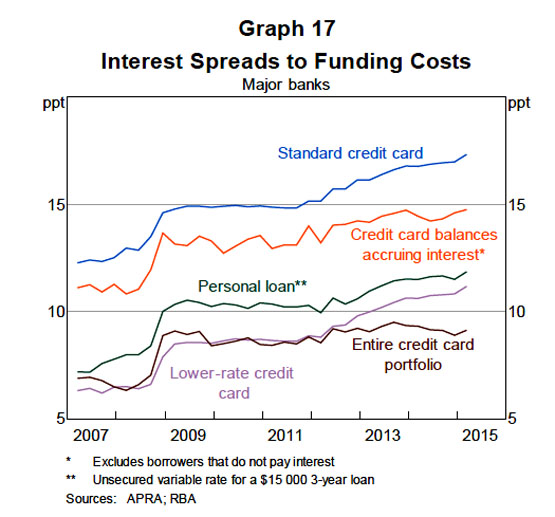

"Based on estimates of the overall cost of funds for banks, it is

possible to calculate the spreads on different lending rates (Graph 17).11 The

data indicate that the interest rate on bank credit card portfolios is around 9

percentage points above the cost of funds, while the spread for those borrowers

who are paying interest is about 14¾ percentage points. These spreads rose

significantly in the global financial crisis (when funding rates fell

significantly but credit card rates fell by much less) and have remained at that

level or drifted modestly higher since.

The observation that issuers compete

actively for customers yet credit card interest rates are high and do not

closely follow changes in funding costs is consistent with international

experience and has been studied by academics. The most well-known paper

addressing this issue is a study by Ausubel (1991) for the United States. The

study notes the apparent paradox that a market with few barriers to entry and

the presence of 4 000 competitors could be characterised by very sticky interest

rates and card issuers making much higher rates of return on their credit card

lending than on other lines of business. Based on the work of Ausubel and

others, it seems reasonable to explain

the apparent paradox as resulting to a large extent from the existence of a

significant number of consumers who are either not well informed or (for various

behavioural reasons) are reluctant to switch banks or seek a lower rate.

At the same time, banks may have little incentive to lower interest rates, given

that rates are not a determining factor for many individuals who may (possibly

mistakenly) not expect to build up significant balances, while in the case of

other individuals, banks may worry that lower rates may attract lower-quality

borrowers.

Below is an

extract from 'Summary' in THE OFFICE OF REGULATION REVIEW dated mid-1990s which

commented that should bank fees and charges change in the future

the most efficient approach would be to

provide specific groups of customers with fee-free basic banking services, with

the Commonwealth Government reimbursing the banks for the costs of doing so:

"The structure of

bank fees and charges could change in the future. In that case, the argument

for government intervention may become stronger. However, any such

intervention would not be without cost. On balance, the ORR considers that,

if the

government chose to intervene, the most efficient approach would take the

form of a “community service obligation” on banks to provide specific groups

of customers with fee-free basic banking services, with the Commonwealth

Government reimbursing the banks for the costs of doing so."

"The Inquiry noted that there is currently no process for regularly assessing

the state of competition in the financial system, nor a requirement for

regulators to demonstrate that they have given consideration to the trade-offs

between competition and their other objectives, creating the risk that

competition issues may be ignored.

The Inquiry recommended reviewing the state of competition in the financial

system, as well as improving the way in which regulators report how they balance

competition against their core objectives and to include explicit consideration

of competition in ASIC’s mandate. The review would examine and report on whether

there are barriers which are inappropriately limiting competition or imposing

barriers to foreign or domestic market entrants. "

Five extracts that evidence that Financially Savvy Users Don't Pay - some Are Paid

"Within the latter group, there is

a third group which directly contributes very

little to the costs of credit card schemes –

these are the

Credit Cardholders

(known as ‘Transactors’) who settle their credit card

account in full each month. Although they

normally pay an annual fee, they pay no

transactions fees, enjoy the benefit of an

interest-free period and in many cases earn

loyalty points for each transaction."

"As an aside it is necessary to deal with so-called travel and

entertainment charge-card schemes branded Amex and Diners. The affront to the

community inherent in these schemes should be dealt with resolutely.

The

distinguishing practical function of these schemes is to convert inflated

business expenses into untaxed personal income, delivered to the card holders as

flyer points to use at their discretion personally. Both these schemes would

cease to exist if and when the ATO required recipients of the flyer-point

income-in-kind to declare it as income and pay tax on it.

That is all that needs to be said about these rackets – never get intrigued

into debates about 3-party and 4-party schemes."

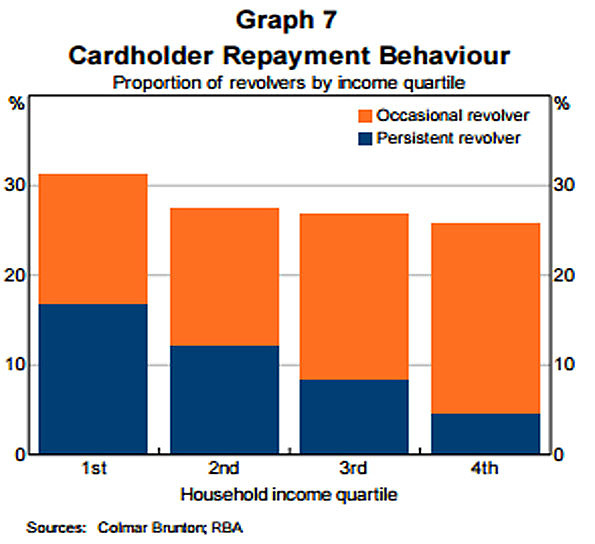

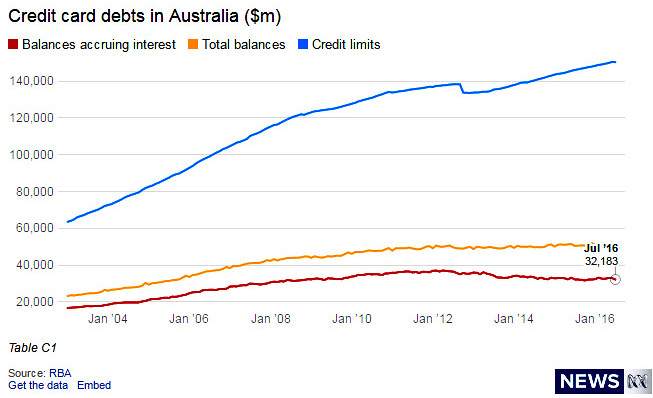

This disparity between 30% and two thirds indicates that a small portion of

Credit Cardholders are carrying very high

Credit Card Debt Accruing Interest.

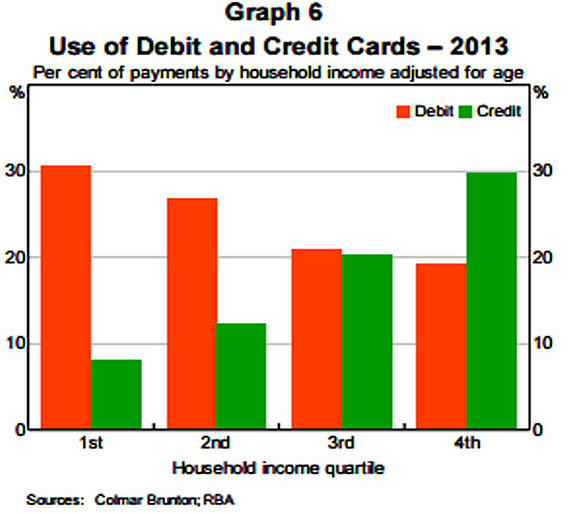

Graph 6 below evidences that

higher-income households use credit cards much

more frequently that debit cards; however debit card use is more common for

lower-income households.

The above Australian

calc of

AUD$6,095 average debt is per Credit Card of the 5,280,000 (33% of all Credit Cards)

held by

Revolvers

of the 16.09 million Credit Cards owned by Australians. The above ave of

USD$7,453

from the

McKinsey Report

represents agg. debt per

Credit Cardholder

amongst the

'Financially stressed'.

"Recommendation 9

- The government should consider expanding financial literacy programs

such as the Australian Securities and Investments Commission's MoneySmart

Schools Program."

·"The

rate on credit cards is found to be the most sticky, followed by personal loan

rates, the housing loan rate and the small business overdraft rate.

·In

contrast, the rates on personal loans and credit cards do not appear to be more

flexible in the deregulated period."

The RBA would likely

retort that it de-regulated loan and deposit interest rates following the

recommendations in the Campbell Report. Chapter 17 below notes:

"The tide of utilitarianism rose

slowly, and a lengthy campaign was necessary before the financial

deregulation of 1854, which abolished the British interest rate cap.

However, one act of deregulation cannot quell an argument that has been going on for millennia. Over the following century the tide gradually turned towards re-regulation, culminating with detailed requirements imposed on the financial sector (particularly the banks) during and immediately after the Second World War. We now trace the gradual lead-up to this second phase of regulation."

"Obviously this is a pretty radical

act, and it will be fought," he replied. "But I think the American people

are disgusted with the financial industry. They want change.

You could argue that an interest rate of 15% or 18% is more than enough to

accommodate any amount of risk on the lender's part.

If a loan appears

riskier than that, don't make it.

What we have to ask as a nation is

whether it's ethical to charge people 30% interest rates," Sanders said.

"This is loan sharking. Let's call it what it is."

Hence, the above

"Recommendation 9

- The government should consider expanding financial literacy programs

such as the Australian Securities and Investments Commission's

MoneySmart

Schools Program" totally ignores

assisting the

33% of

Credit Cardholders that are

Revolvers'

that carry 100% of the

$33.1 billion

of interest bearing

debt.

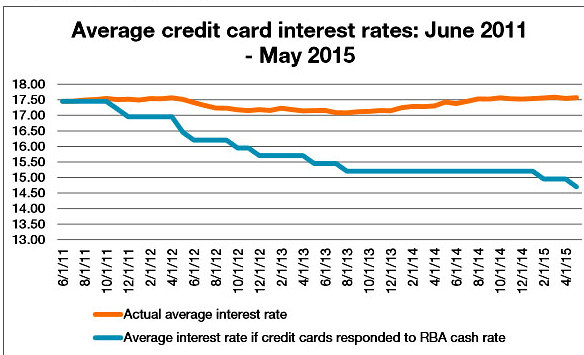

The average credit card interest rate at 31 May 2015 was 17.61%. Instead

of falling in line with the cash rate, the average credit card interest

rate has risen by 0.2% over the last four

years from 17.41% in June 2011.

1

1

Based on an analysis

by Mozo of interest rate changes of over 170 credit cards between 2011

and 2015. Unless otherwise noted, all data in section oneis based on

figures supplied by Mozo.

The graph above compares the average credit card interest rate on all

cards to the interest rate if cards responded to RBA announcements. If

credit card interest rates had moved in line with RBA cash rate

announcements, as they largely had before 2011, the expected average

interest rate in May 2015 would have been 14.70%.

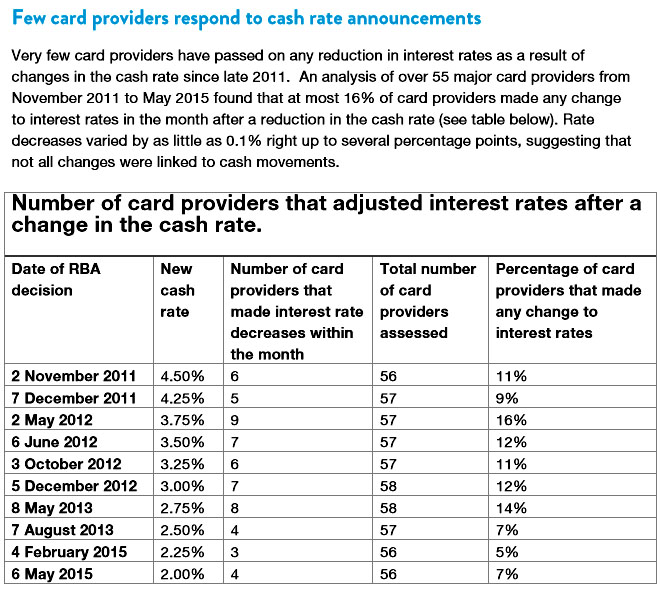

Few card providers respond to cash rate announcements

Very few card providers have passed on any reduction in interest rates

as a result of changes in the cash rate since late 2011. An analysis of

over 55 major card providers from November 2011 to May 2015 found that

at most 16% of card providers made any change to interest rates in the

month after a reduction in the cash rate (see table below). Rate

decreases varied by as little as 0.1% right up to several percentage

points, suggesting that not all changes were linked to cash movements."

The spread between the wholesale

cost of funds and Standard Credit Card

"For example, at the end of June 1985

interest rates were in the range 17.25% to 19%."

* December 1987 - spread

2½%

Based on the immediately below two Light Blue RBA graphs titled "Simple

Measures Of Bank Margins" that appear in RBA's "Bank Interest Rate Margins

dated 1992,

that 2½

years after "the jail door was thrown

open in April 1985 and the money lenders were released", namely in Dec 1987, the variance between the then

overnight cash rate and the Standard Credit

Card Purchase

Interest Rate

was 2½% (13½%

minus 11%).

The

Interactive hover

mouse on that RBA webpageCash Rate displays the

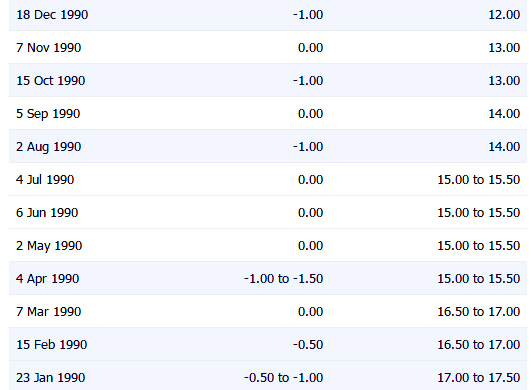

Cash Rate at 15.5% in July 1990.

The below RBA Graph 6 'Credit Card Interest Rates' (sourced from

Developments in the Card Payments Market - Mar 2015)

shows the Standard Credit Cards

Purchase

Interest Rate @ 23.5%

on 1 July 1992 and spread of

12.5% (23.5% minus 15.5% = 8%).

*

Sept 1990 - spread 9.5%

The

Interactive hover

mouse on that RBA webpageCash Rate displays the

Cash Rate at 14% in Sept 1990.

The below RBA Graph 6 'Credit Card Interest Rates' (sourced from

Developments in the Card Payments Market - Mar 2015)

shows the Standard Credit Cards

Purchase

Interest Rate @ 23.5%

on 1 Sept. 1992 and spread of

12.5% (23.5% minus 14% = 9.5%).

*

January 1991 - spread 11.5%

The

Interactive hover

mouse on that RBA webpageCash Rate displays the

Cash Rate at 12% in Jan 1991.

The below RBA Graph 6 'Credit Card Interest Rates' (sourced from

Developments in the Card Payments Market - Mar 2015)

shows the Standard Credit Cards

Purchase

Interest Rate @ 23.5%

on 1 Jan 1991 and spread of

12.5% (23.5% minus 12% = 11.5%).

When Messrs.

Lowe and Rohling wrote their Discussion

Paper,

LOAN RATE STICKINESS: THEORY AND EVIDENCE

in June 1992 - seemingly on a topic of some significance -

the Interactive hover

mouse on that RBA webpageCash Rate displays the

Cash Rate at

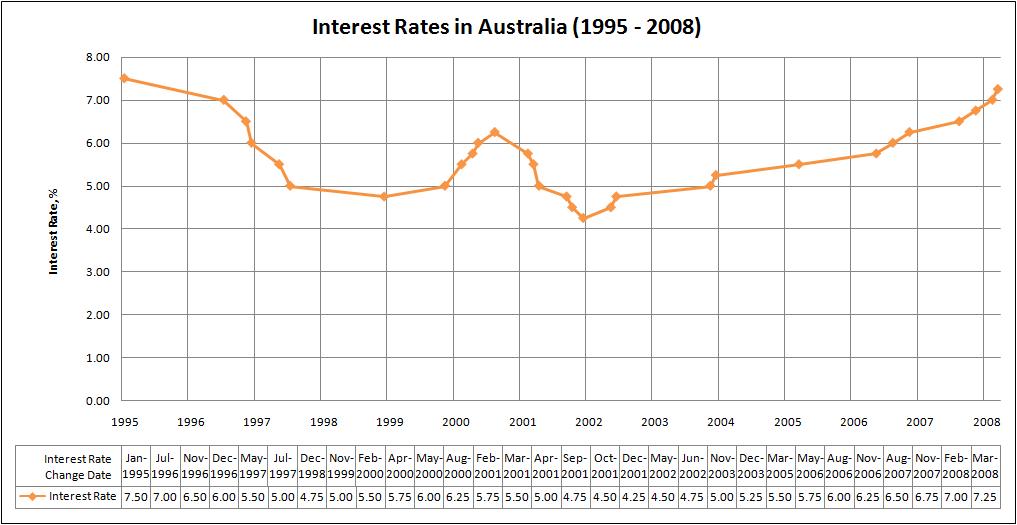

6.5% in June 1992.

The below RBA Graph 6 'Credit Card Interest Rates' (sourced from

Developments in the Card Payments Market - Mar 2015) displays the

Standard Credit Cards

Purchase

Interest Rate @ 23% in

June 1992 with a spread of 16.5%.

Little wonder Messrs Lowe/Rohling

wrote their Discussion Paper highlighting that the Credit

Cards

Purchase

Interest Rate had been markedly

sticky or stucky, because the spread had blown

out from 12.5% to 16.5% in 11 months because credit card interest rates

were 'stuck'.

* July 2001 - spread 11.5%

The

Interactive hover

mouse on that RBA webpageCash Rate

displays the Cash Rate at 5% in July 2001.

According

to a 2013 RBA survey, only around 30 per cent of credit card users reported that

they pay interest on their credit card balances (the ‘Revolvers’)."

"Within the latter group, there is

a third group which directly contributes very

little to the costs of credit card schemes –

these are the

Credit Cardholders

(known as ‘Transactors’)

who settle their credit card

account in full each month. Although they

normally pay an annual fee,they pay no

transactions fees, enjoy the benefit of an

interest-free period and in many cases earn

loyalty points for each transaction."

[Above two extracts sourced from

"Five extracts that evidence that Financially Savvy Users Don't Pay - some Are Paid"

above in this Chapter 5].

The Board has been given the backing

of strong regulatory powers,

unique

among central banks."

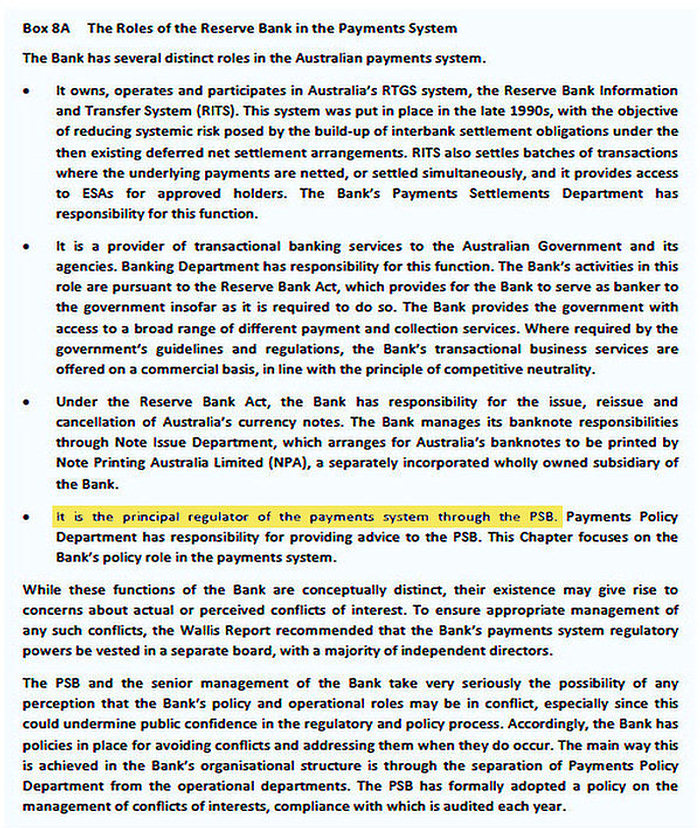

*

"The Reserve Bank

is the principal regulator of

the payments system

through the PSB."

A.

powers to gather financial

information from ADIs; and

B.

responsibilities to

'inter alia'

"best

contribute to.......... the

economic prosperity and welfare of the

people of Australia",

are more

extensive/inflexible

than the -

1.

Bank of England,

that was not

nationalized as

Britain's central bank

until 1946, which is a

corporation wholly owned

by the UK government -

the 'Corporate governance: Board responsibilities' –

SS5/16 (Short form) and the (Long

form)focus on the Corporates it

regulates with no

apparent obligation to

best contribute to the

peoples of Britain; and

"The Federal Reserve

advances supervision,

community reinvestment,

and research to increase

understanding of the

impacts of financial

services policies and

practices on consumers

and communities."

One can only ponder whether "Loan

Rate Stickiness" is still

a concern of the Reserve Bank, but it was in 1992 - at least to the two

authors:

The '16.5% Differential'

[between the

Overnight Cash Rate of 1.5% (as at 27 Dec 2016) and the 18% 'Cap On Credit CardInterest Rates'

(forPurchases and Cash Advances)] could be

'locked in'. Whereupon if the

Overnight Cash Rateincreased to say 3%, the 'Cap On Credit CardInterest Rates' would increase to 19.5%

('16.5% Differential' + 3%).

If credit card

scheme restrictions were to remain largely unchanged, the main beneficiaries

of the arrangements would continue to be:

(i)

credit card Transactors who settle their credit card account in full each

month; and

(ii) credit card

Scheme Members and the

Schemes

themselves.

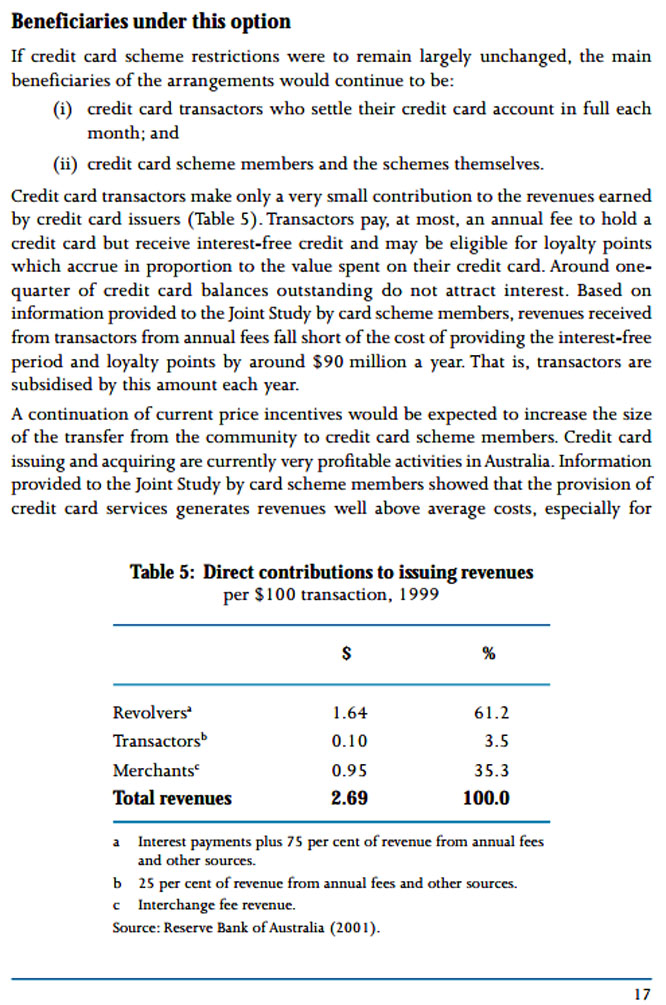

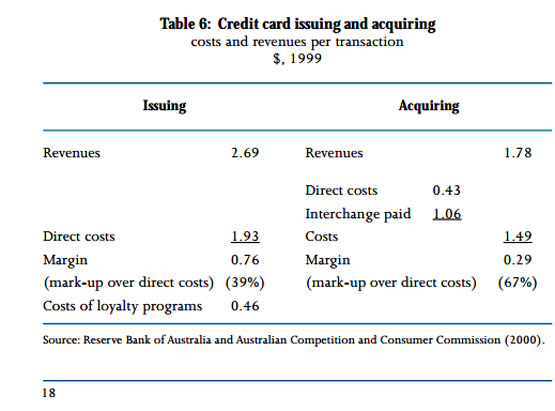

Credit card Transactors make

only a very small contribution to the revenues earned by credit card issuers

(Table 5 below). Transactors pay, at most, an annual fee to hold a

credit card, but receive interest-free credit and may be eligible for

loyalty points which accrue in proportion to the value spent on their credit

card. Around one quarter of credit card balances outstanding do not

attract interest.

Based on information provided to the Joint Study by

card Scheme Members,

revenues received from Transactors from annual fees fall short of the cost

of providing the interest-free period and loyalty points by around $90

million a year. That is, Transactors are subsidised by this amount

each year.

A continuation of current price

incentives would be expected to increase the size of the transfer from the

community to credit card

Scheme Members. Credit card 'Issuing' and 'Acquiring' are

currently very profitable activities in Australia. Information

provided to the Joint Study by card scheme members showed that the provision

of credit card services

generates

revenues well above average costs, especially for financial institutions

which are both significant card issuers and acquirers.The margins are

particularly wide in credit card acquiring (Table 6). Although card

scheme members were generally unable to supply suitable capital data,

indicative figuring by the Reserve Bank – based on the main risks against

which capital would be held – suggested that the margins in credit card

issuing and acquiring were well above what would be required to provide a

competitive rate of return on capital.

The

designated credit card schemes would also continue to benefit from current

arrangements. MasterCard and Visa earn revenue from credit card activities

in Australia through their operational role in providing switching

facilities to participants. The schemes typically charge their members a

flat fee per transaction for processing transactions through their switch, a

source of income which has risen significantly over recent years in line

with the strong growth in the number of credit card transactions."

"the

worst financial scams and unscrupulous market conduct in the country"

(Predatory

Advertising) on a daily basis

within some web and newspaper

advertisements for

Credit Card Products that have patently

proved very costly for

Credit Cardholders with poorFinancial Literacy

Skills.

Federal and State Govt's that fund $43m annually

-

* should obtain from senior Financial Counsellors descriptions of

misleading, deceptive or

Unconscionable

Credit Card

advertisements; and

* pass those descriptions onto

Australia's Three Financial Regulatorsthat should ensure that those offending Credit Card

Issuersareharshly fined

Ms Katherine Temple, a policy officer with the Consumer

Action Law Centre in Melbourne, provided the

Senate

Economics

References Committee

with some insight into

its work with people struggling with

Credit Card DebtAccruing Interest, and by extension the

scale and severity of the problem in the community:

"Queensland is the host

state and custodian of the national consumer credit regulatory regime.It is also the home

base of some of the worst financial scams and unscrupulous market conduct in

the country. Many of these scams spread south and west much faster than the

cane toad has so far been able."

"A key responsibility the financial counselling community shoulders in

responding to its client base is to ensure the experiences those people

report are recorded and appropriately considered in service design and policy, social action

and law reform activities. Sadly, the otherwise rich data pool that the

450 odd financial counsellors working around Australia have access to, is also

fragmented. Representatives from the Commonwealth Financial Counselling Program

are here today. I congratulate them on evolving efforts to collect and produce

more useful data. The conversation around data collection and usage does require

greater engagement with and of the financial counselling community and all of

the various funding sources around the country."

7th

extract:

SMH article "Middle class hit by debt"

notes thatTony Devlin, a senior

Financial Counsellor at

Salvation Army's

"Moneycare" service, has

interviewed hundreds of level 1 and level 2 Australians who have incurred huge

debts on multiple credit cards. "There are far more middle-income earners seeking a way out of the desperate

cycle of huge mortgage repayments and mounting credit card debt.........And

people try to keep the ship afloat by using more credit cards."

The Writerspoke to Tony Devlin on Wed 7 Dec '11. Tony told

him

"It is not uncommon to meet

people in financial trouble who had significant debts on between

6 and 10 credit cards."

A. assist agencies

(charities/not-for-profits/community

organisations) that

offer

financial counselling services to provide a high quality of service; and

B. set out the essential requirements an agency

should meet if it wishes to offer financial counselling services.

Below are

extracts from the above FCA booklet which relate to

Financial Counsellors

maintaining records whereby useful data/information can be provided back to their 'funders':

1. Financial counsellors

also work to prevent financial difficulty through community education and by

providing input to government and industry policy development processes.

2. The agency

keeps

complete and legible records in relation to each matter where it provides

financial counselling services.

3.

The agency submits reports to its

funders in the required format and within the required time frames.

4. The agency

collects and

analyses data concerning:

(a) Demographic information about the

clients who use the service.

(b) Systemic issues that are identified in

the course of service delivery.

5. The agency participates

in evaluation concerning the effectiveness of its financial counselling

services.

A shocker of misrepresentation and deceit was that some Credit Card Issuers were offering a Zero Balance Transfer

(for say one or two years) and then -

i) applying monthly repayments of

Purchases

to

reduce the Zero Balance

Transfer amount; and

ii) charging 20% circa on those

Purchases

from date of each Purchase

and in some cases, withdrawing the Interest free Period for one or two months.

(A.) descriptions

of

misleading, deceptive or unconscionable

web and newspaper Credit Card advertisements (Predatory

Advertising)

and pass those advertisements

onto

Australia' Three Financial Regulators

that should ensure that offending

Credit Card

Issuersare

prosecuted,

with ASIC (or another) imposing hefty monetary fines and public exposing

the practice; and

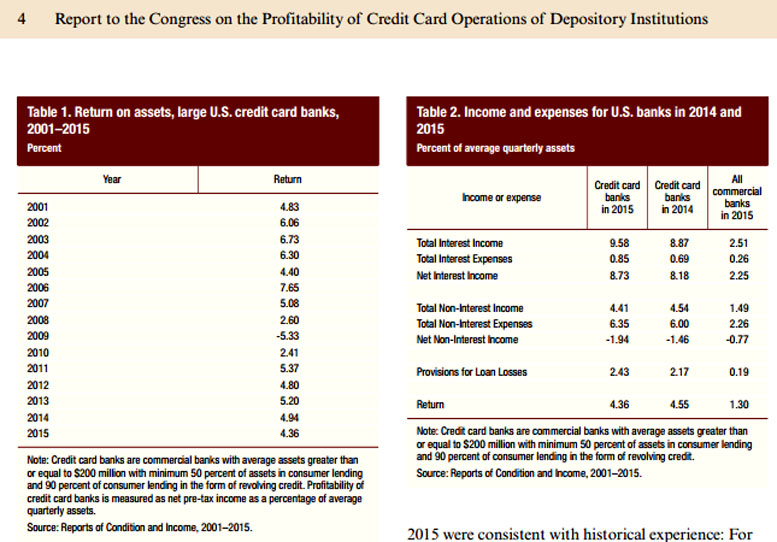

The U.S. Federal Reserve's annualReport to the Congress

on the Profitability of Credit Card Operations of Depository Institutions - June 2016

includes the below Table 2 which

shows that 'USA Credit Card Banks' in 2015 had Net Interest Income of 8.73% and

Net Non-Interest Income of -1.94% of average quarterly assets.

USA Credit Card Banks are defined as commercial

banks with average assets greater than or equal to $200 million with minimum 50

percent of assets in consumer lending and 90 percent of consumer lending in the

form of revolving credit.

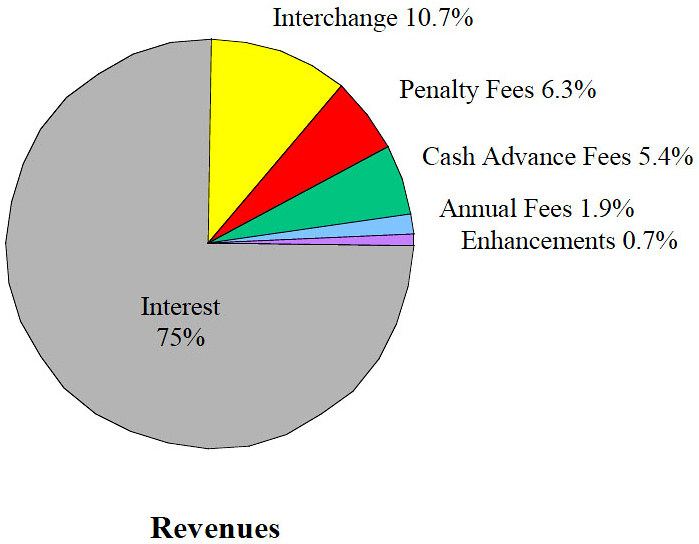

The below two 'pie charts' appears in a journal report titled

"Who Pays for Credit Cards?"dated 2001 which displays a break-up of

Card Issuers'

Revenues for the

aggregate of Visa, MasterCard and Discover Credit Cards in the USA. It shows

that U.S. Interest Revenues of 75% and associated Penalty Fees Revenue (Late

Payment Fees and Overlimit Fees)

of 6.3% and Cash Advance Fees of 5.4% aggregate to 86.7% of U.S. Card Issuers' Annual Revenue.

Interchange Fees charged to Merchants were only 10.7%.

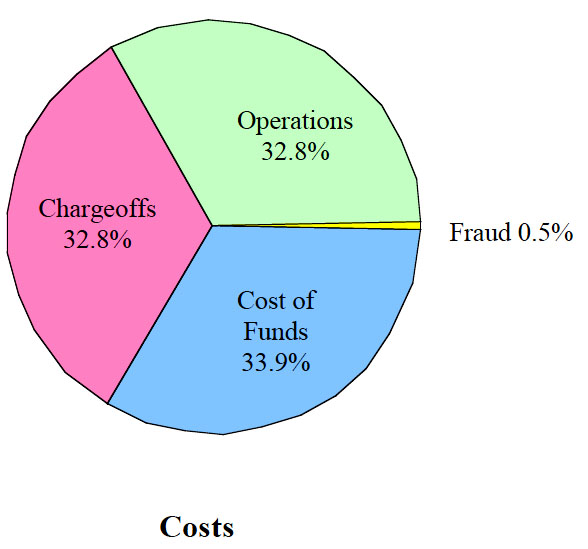

'Chargeoffs' are bad debts written-off or

sold to a collections agency.

It is a sad reflection of any unsecured personal loan lending product

that almost one third of operating 'Costs' is debt written off annually.

No other lending

product could survive with writing off one third of lent money annually.

This lending product can only be maintained because of the extraordinary

quantum of interest/fees based revenue stream evident in below

Revenues

'pie chart'.

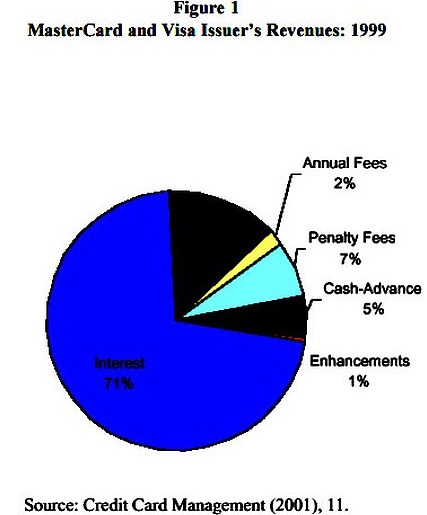

Below are extracts from 'Estimating

the Volume of Payments-Driven Revenues' dated 2003 published by

POLICY STUDIES presented by

Federal Reserve Bank of Chicago which relate to Figure 1 on LHS that breaks up

the revenues from US Banks that issued Visa and MasterCards in 1999:

The pie chart shows that net U.S. Interest Revenues from Credit Cards of 71%, Penalty

Fees Revenue (Late

Payment Fees and Overlimit Fees)

of 7% and Cash Advance Fees of 5% aggregate to 84% of U.S.

Card Issuers' Annual Revenue. Interchange Fees

charged to Merchants are only 14. Notwithstanding that

Interchange Fees are levied at a materially

higher amount in the USA,

Interchange Fees account for

less than 11% of aggregate U.S. Card Issuers' Revenue in the first above

pie-chart.

"A

third of Americans do not own a credit card, according to our

survey. Of those who use them, here's how much money they owe"

The disturbing disclosure from the above two 'Revenue' pie

charts is that the aggregate of Interest, Cash Advance Fees, and Penalty Fees

(Late Payment and Overlimit) aggregate from a high of 86.7% down to 84% of aggregate

Credit Card Issuers 'Revenue'.

Annual Fees do not exceed 2% of 'Revenue' in either above pie chart.

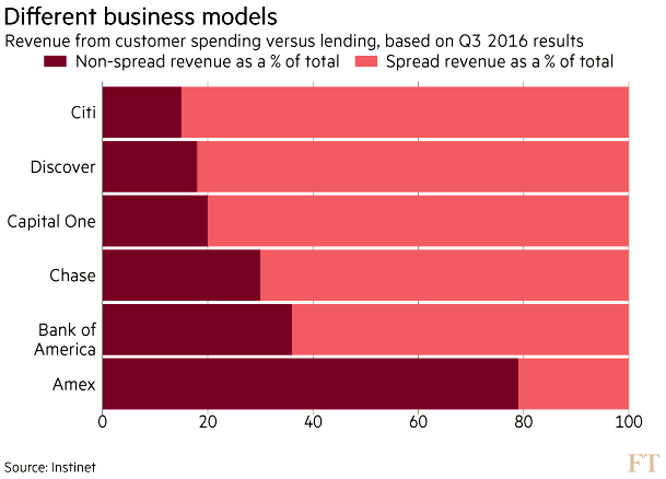

The above graph appeared in the USA

Financial Times on Dec. 23, 2016 article discussing credit cards. One of the

charts (“Different business models”) shows a breakdown of spread revenue vs.

non-spread revenue for six major Credit Card Issuers in the USA.

Patently the top five Credit Card Issuers are deriving "The Lion's Share" of Revenue from the implicit

interest margin between "where they borrow money and the interest rates they

charge out" on Purchases and Cash Advances on some credit cards.

Fee

income is relatively minor, except for Amex, BoA and perhaps Capital One.”

Section 8 of the Fair Credit and Charge Card Disclosure Act of 1988 directs the

U.S. Federal Reserve Board to transmit annually to the U.S. Congress a written

report about the profitability of credit card operations of depository

institutions. Last August the

Board of Governors of the

Federal Reserve System presented its 26th "Report

to the Congress on the Profitability of Credit Card Operations of Depository

Institutions".

The Reserve Bank's webpage "Accountability"

provides a section titled 'Accountability to Parliament' which notes that the

Governor of the Reserve Bank has provided every few years since 1998 to the Commonwealth Parliament a Statement on the

Conduct of Monetary Policy.

A precedent is therefore in place with the U.S. Federal Reserve reporting

annually in writing to the U.S. Congress on various aspects of Credit Cards

Profitability, for the Reserve Bank to similarly report annually to the

Commonwealth Parliament on various aspects of Credit Cards profitability which

would include Credit Card Issuers complying with

Section 3.4.8

Changes to benchmark compliance.

"The

Reserve Bank’s policy-making role is one of the four different roles of the Bank in the

payments system (see ‘Box 8A: The Roles of the Reserve Bank in the Payments

System’).

The Reserve Bank is the principal

regulator of the payments system through the PSB. Payments Policy

Department has responsibility for providing advice to the PSB."

"The Payment Systems (Regulation) Act 1998 gives the Reserve Bank of Australia

'extensive powers' to gather information from a

payment system or from individual participants."

"The Payments

System Board was established by the Commonwealth

Govt. in 1998 so as to best contribute to:

.......... and

promoting competition in the market for payment

services."

(i) same

style 'pie charts' for "Card Issuers'

Revenue" [that quantifies at least seven revenue sources] and "Card Issuers'

Costs" [that quantifies at least five costs, which include Rewards Programs] that is displayed in

Chapter 8;

CEOs would like you to believe that Credit Card Products have very high

bad debt write-offs, but do they? What annual write-off amount is high for

a Pillar Bank?

LNP's Scott

Buchholz asked how much revenue Westpac's credit card business

generates.

"Where would you

allocate the profit to?"

"We don't have a credit card business,"

Westpac's CEO, Mr Hartzer responded that credit

cards fell within multiple business units.

After a brief

circular exchange Committee Chair David Coleman intervened by asking Mr Hartzer

to confirm he wasn't answering the question.

"What I'm saying is

that we're not able to

answer that question because we don't have a credit card business per se,"

Mr Hartzer said.

David Coleman

noted the Committee might be in-touch about this issue.

Labor’s

Matt Keogh is curious about the profitability of credit cards and asked ANZ

CEO

, Shane

Elliot, who responded:

“I’m not sure that we disclose that,

but I’ll give you a rough idea. It would be, after tax, a couple of hundred

million dollars,”

Elliott acknowledged that it is a large amount of money,

albeit a small share of the banks’ overall earnings.

The Australian - 6 Oct 2016 reported that Commonwealth Bank's chief

executive, Ian Narev, resisted providing returns across products, claiming

these are commercially sensitive for competitive reasons.

"Commonwealth Bank boss, Ian Narev, has defended the

bank’s exorbitant credit card interest rates, insisting it’s high-risk debt, AAP writes.

Mr. Narev was grilled today over credit card rates. He was asked why the cash advance rate on the

bank’s low rate card was more than 21 per cent, when the official cash rate is

just 1.5 per cent. “To me, that’s gouging, that’s excessive,” coalition

backbencher Scott Buchholz said. “It is a highly profitable part of the business,

how is that fair?”

Mr. Narev said he understood the concerns, but

argued the bank did not encourage its customers to take on high amounts of

high-risk debt.

“I said we came in here with a spirit of openness

and listen to suggestions and we will,” Mr. Narev replied."

Shane Elliot has given Liberal MP Scott Buchholz an

illustrative breakdown of costs in the credit cards business (re

the pie chart on RHS "Costs" in Chapter 8 above):

"If the credit card

section were a stand-alone business, he says -

*

25 per cent of the cost would be the cost of funds.

*

another quarter would be features - insurance, reward points etc

*

while about a third are the administrative systems needed.

*

the balance, slightly less than 20 per cent, is lost through bad debts and

fraud."

ANZ CEO, Shane Elliot, responded to a question about

the profitability of credit cards,

“I’m not sure that we disclose that, but I’ll give you a rough idea. It would

be, after tax, a couple of hundred million dollars,”

Elliott says, acknowledging it is a large amount of money

albeit a small share of the banks’ overall earnings.

ANZ

to consider slicing credit card rates: ANZ Banking Group will consider

cutting interest rates on its credit cards and introducing a pricing regime

based on "borrower risk".

Shane Elliott, CEO ANZ said:

The bank is currently looking at

changing the parameters for credit cards to ensure people can avoid

financial hardship.

“It’s the right thing for us as well ... It’s not in our

interest to have customers with products they can’t service,”

he says.

Pressed by Liberal MP Scott Buchholz whether there was

“ample opportunity”

for card rates to be lower, Mr. Elliott said:

“As a general proposition, I think you’re right.”

“I think there’s an opportunity for us frankly

to take a bit of leadership on this and do something better on not just the

interest rate but also the fee structure on cards,”

Shane Elliott said.

He also said ANZ would look to

harness big data to discover low-risk customers that could be offered lower

interest rates.

Andrew Thorburn, CEO NAB said

"The credit

card business has some of the 'highest losses in our portfolio' and one third of

their customers were on a 13.99 per cent 'low rate' card."

The Four Pillars

bad debt

write-off rates would be lower and discourage

"its customers to take on high amounts of high-risk debt", if

all Credit Card Issuers in

Australia were regulated to -

A) limit school leavers

from 18 years

to a Charge Card for the initial six months,

thereby necessitating the Total Amount Owing

to be repaid at the end of each monthly cycle, in order to establish/improve their

Credit Rating;

C) require all

Credit Cardholders to pay a minimum of

25% of the Total Amount Owing

each month,

wherebyCardholders could contact their

Credit Card Issuer and request their Credit Card Issuer to reduce the monthly

limit to 5% for up to two years dependant upon the normal parameters governing

an Unsecured Personal Loan

application.

"Value simplicity and transparency in fees, rates and terms, but their

biggest need is for something that NO credit card offers: a mechanism

allowing them to impose their own spending limits which would enable them to

carry a credit card for larger purchases that take time to pay off, without

fearing they might be tempted to use it for non-essentials."

The

below three graphs seek to identify write-offs on Credit Cards by the major

Australian Credit Card Issuers.

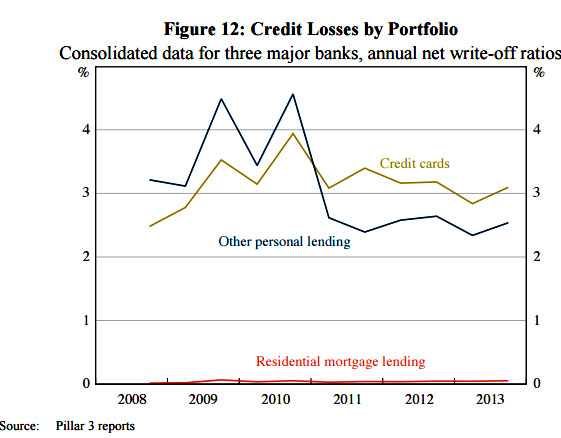

The above graph from

Reserve Bank's Credit

Losses at Australian Banks: 1980–2013 shows annual net write-offs for

Credit Cards for three of the Four Pillars

in 2013 was 3.1% of Debt Outstanding.

The above RBA graph seems to infer that

for every $100 funded by a Credit Card Issuer to a Credit Cardholder, the Credit

Card Issuer will not get $3.10 back in 2013. But are Credit Card Issuers

making 17% on ave. before costs on the remaining 96.9% Credit Cardholders?

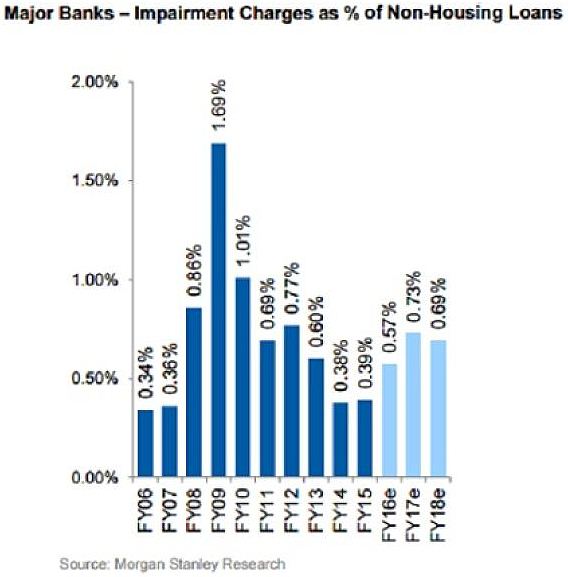

The above Morgan Stanley Research graph estimates that 'Impairment Charges as %

of Non-Housing Loans' will increase -

*

from 0.39 per cent of total non-mortgage loan books in 2015

*

to 0.57 per cent upwards to 0.73 per cent in 2017.

The above

Morgan Stanley graph

seems to infer that for every $100 funded by a Credit Card Issuer to a Credit

Cardholder, the Credit Card Issuer will not get back $0.73 in 2017.

Chapter

11. The

Four Pillars announces large profits year after year. CEO's of the

Four

Pillars are paid 'phone number salaries'

whereas 20 years earlier they were not

"Ponder the consequences of banks, mainly the

Four Pillars, now holding

some $1,000 billion -- that’s one trillion dollars – in transaction deposit

accounts on which no interest of material consequence is paid to depositors but

which, invested by banks, returns market-rate revenue to banks."

Based on stats in Reserve Bank reports and information from some of the 44

charities/community organisations that provide

Financial Counselling(Chapter 7 above), over half a million Australian

Credit Cardholdersare suffering Extreme Financial And Emotional Distress

due to Credit Cards Debt sometimes exceeding $150,000

(across a dozen or so Credit Cards) that also may affect their family and close friends, causing

diminished productivity and creating a further burden on social welfare budgets,

as appraised by the Productivity Commission

and Dept. of Social Services.

A costly flaw in the judgment by Australia's

Three Regulators for Financial Services and

Senate Committees is the assumption/belief that all

"... individuals

are

expected to assume personal responsibility for the financial decisions they

make,....."

;namely that

all individuals possess the capacity

to "assume personal

responsibility for the financial decisions they make."

"Though individuals are expected

to assume personal responsibility for the financial decisions they make,

evidence received in this inquiry indicates that the credit card market is

structured in such a way as to make it extremely difficult for individuals to

makeinformeddecisions

about credit card debt."

The above extract

says that "...individuals

are expected to assume personal responsibility for the financial decisions they

make, ...".

Then it says "the

credit card market is structured in such a way as to make it extremely difficult

for individuals to makeinformeddecisions

about credit card debt."

These two parts of the above extracted single sentence

are incongruous, contradictory and paradoxical. How can all individuals

".... assume

personal responsibility ...."

and then

"... the

credit card market is structured in such a way as to make it extremely difficult

for individuals to makeinformeddecisions......"when

the range of those skills are separated into five 'skills' quintiles?

Individuals identified by theProductivity Commission and the ABS as possessing only

Level 1 and Level 2 Financial Literacy Skills are unskilled ...to makeinformeddecisions

about credit card debt that is structured in such a way as to make it extremely

difficult for individuals to makeinformeddecisions."

The current arrangement of Credit Card Issuers seeking data from one or two of

Three Credit

Rating Agencies is not working as the credit data is not complete,

unless data from all three

Credit Reporting Agencies is sourced

* RBA's key areas

of focus included capacity for richer

information with payments.

On

current scheduling the New Payments Platform will deliver a fast payments

service with rich information and addressing capabilities in the second

half of 2017

* Chapter Five: 'Philosophy of Financial Regulation'

"Third, regulation can help achieve social

objectives such as, for example, 'community service obligations' which typically

take the form of price controls."

* Chapter Nine: 'Stability and Payments'

"There is scope for increased competition in the payments system which will help

to lower its costs of operation. However, this must be balanced against

the need to maintain stability in the financial system. The payments system provides one central

way in which instability can be generated. The RBA should retain overall

responsibility for the stability of the financial system, the provision of

emergency liquidity assistance and for regulating the payments system."

* Chapter Eleven: Promoting Increased Efficiency

"Cross-subsidies are derived from

historical product bundling [evident in (a) to (g) of

Chapter 3 above], earlier

difficulties with apportioning costs, and community expectations that

institutions should meet community service obligations. The unwinding of

such cross-subsidies can increase efficiency in the financial system."

* the Reserve Bank Board’s

obligations with respect to monetary policy are laid

out in Sections 10(2) and 11(1) of the Act. Section

10(2) of the Act, which is often referred to as the

Bank’s ‘charter’, says:

(A) report annually

to the Australian Parliament on each of the

Four Pillars

Net Revenue and Net Costs break-up of their cumulative

Credit Card Products;

and

(B) report annually

to the Australian Parliament whether any Credit Card

Issuer/s is -

Chapter 17. Reserve Bank possessed and exercised 'extensive powers'

under

Section 50

of the

Banking Act 1959

to regulate/cap bank

deposit/investment interest rates from 1969 to 1980.

Reserve Bank must regulate interest rates and fees according to

User Pays Principle

to bring Credit Card Products into line with

all other 'goods' and 'services, incl. other

banking lending products because Australians with low Financial Literacy

Capacity have been exploited by some Credit Card

Issuers

The below four quotes from "Overview

of Financial Services Post-Deregulation"by (Dr) Diana

Beal, Director, Centre for Australian Financial Institutions, University of

Southern Queensland,

evidence that the Reserve Bank

rigorously regulated bank deposit rates until 1980 when restrictions on interest rates

were dismantled after adopting Campbell Committee recommendations:

"Interest-rate

ceilings on deposit accounts restricted the banks’ ability to attract funds

particularly during the 1970s when inflation was rampant. In the June

quarter of 1975, inflation rose to 16.9% pa. At the same time, interest

payable on amounts held in savings accounts offered by savings banks, for

example, was restricted to 3.75% from 1969 to 1980 (Foster, 1996). In contrast, the

interest rates offered by non-bank financial institutions (NBFIs) were not

controlled and they were able to pay around 10% on passbook accounts."

"Banks in 1980 still operated in a highly regulated environment which was an

artefact of previous economic and social conditions. Indeed, an extensive

collection of controls remained from regulation introduced under the

National Security Regulations in 1941."

"Interest rate ceilings on trading bank and savings bank deposits were

dismantled from 1980; some limits on minimum and maximum terms on fixed

deposits remained."

"The maximum interest rate payable on small

balances in savings accounts was fixed by regulation at 3.75% from 1969

to 1980."

The

Writerworked for CBA for 37 years

commencing in 1970 where he worked in four branches 'til 1974 whence bank

interest rates were rigidly controlled by the Reserve Bank and uncontrolled upon

the NBFIs.

"Looking

back in time, Australian banks collapsed in almost every decade of the 19th

century. In 1893 after the failure of fraudulent land banks in Victoria

triggered a wholesale run on banks. In the space of six weeks, 12 banks closed

their doors. Those banks accounted for two-thirds of the total banking assets in

Australia. That crisis increased pressure - which had been building for some time - for the

formation of a central bank. The Commonwealth Bank was formed by the Federal

Government in 1911 to issue notes which would be backed by the resources of the

nation.Banking became more tightly controlled during World War II, with the central

bank dictating overdraft rates and, later, statutory reserve deposit ratios and

liquid asset ratios.To avoid a patent conflict of interest, the Commonwealth Bank's 'central banking

powers' were transferred to the newly formed Reserve Bank of Australia in 1959."

Between 1960 and

1980 the Reserve Bank diligently regulated commercial Australian bank interest

rates relying on

thebelow Section 50

of the

Banking Act 1959 as amended:

(1) The Reserve Bank may, with

the approval of the Treasurer, make regulations:

(a) making provision for

or in relation to the control of

rates of interest payable to or by ADIs,

or toor by

other persons in the course of any banking business carried on by them;

(b) making provision for

or in relation to the control of rates of discount chargeable by ADIs, or by

other persons in the course of any banking business carried on by them;

(c) providing that

interest shall not be payable in respect of an amount deposited with an ADI,

or with another person in the course of banking business carried on by the

person, and repayable on demand or after the end of a period specified in

the regulations; and

(d) prescribing

penalties, for offences against the regulations, not exceeding:

(i) if

the offender is a natural person--a fine of $5,000; or

(ii) if

the offender is a body corporate--a fine of $25,000.

Until 1980, banks could not

offer more than 3¾% on a passbook account and 6½% interest on a Savings Investment Account (minimum account

balance of $500, deposits and withdrawals must be $100 or greater, and 7 days

written notice had to be given to the bank for all withdrawals). Leading up

to 1980, building societies (unregulated) were offering materially higher interest rates and attracting bank customers

'in droves'.

"the RBA should retain overall

responsibility for the stability of the financial system, the provision of

emergency liquidity assistance and for regulating the payments system."

A). The 'iron

fist control' that the Reserve Bank had over commercial bank interest rates,

both deposit and lending, until deregulation in 1980, whereupon when the jail

gate was no longer locked; and

B). It was apparent

to the Reserve Bank as early as 1992 that deregulation wasn't going to evidence

banks lowering loan rates when the cost of funds fell.

"April 1985.

In the case of overdrafts the maximum rate on all overdrafts was set by the Reserve Bank prior to February 1972". At that

time interest rates on overdrafts drawn on limits over $50,000 became

a matter for negotiation between the banks and their customers while

those drawn under limits less than $50,000 remained regulated. In February

1976 the threshold level was increased to $100,000 and in April 1985 all regulations were lifted.

From 1966, when personal loans were introduced, the maximum rate

that banks could charge was set by the Reserve Bank. Once again, in

April 1985, the controls were removed.

At the same time, the maximum interest rate that could be charged on credit cards was

deregulated. Prior to this time the maximum rate had been set at 18 per cent per

annum.

The period of housing loan rate regulation extended beyond that

for the other lending rates. Until 1973, the maximum rate that could be

charged on housing loans was the same as that on overdrafts although

banks typically charged a

lower rate. In October 1973 banks agreed to a "consultative maximum" on housing loans which was below the overdraft rate. This was formalised in December 1980 when the maximum rate that could be charged on owner-occupied housing was

set one percent below the maximum overdraft rate. The ceiling on new owner-occupied housing loans was finally removed in April 1986.

In the deregulated period, data on certain

actual lending rates is readily available. For example, the actual rate charged on credit card

loans is directly observable and is the same for all classes of

borrowers.

In contrast,

the rates on personal loans and credit cards do not appear to be

more flexible in the deregulated period.

For credit cards, personal loans, owner-occupied housing loans and the standard overdraft rate, changes in the banks' marginal cost of funds have not been translated one for

one into the contemporaneous lending rates."

Prior to Aug 1993, Credit Card Issuers were restricted from

charging an Annual Fee on Credit Cards as the various State Credit Acts

prohibited most Credit Card Issuers from charging annual fees if they charged

interest on credit card purchases (e.g. Credit Act 1984 (NSW) s 54).

Following a recommendation from the Prices Surveillance Authority’s 1992 'Inquiry

Into Credit Card Interest Rates', State legislatures issued exemption orders

which allowed all financial institutions to charge both interest and fees on

credit cards from 1 August 1993.

"But of course the PSB does have a regulatory mandate,

and it has used its powers

to regulate a number of aspects of card payments where it judged that there was

a public interest case to do so. Probably the aspects of this regulation that

have attracted the most attention have been those related to interchange and surcharging....."

There is a patent

"... public interest case to ..."

re-introduce interest rate caps on credit card interest rates that applied until 1985 -

as called for in Chapter 5.

"1.8 Dr Edey quite

rightly made the point that Australia does not

regulate interest rates, and, as such, there is no

interest rate regulator.He told the committee that Australia

does have 'an ACCC [Australian Competition and Consumer Commission] that can

investigate uncompetitive conduct if they see it, but they clearly have not

seen it in this market'.3 It was put to Dr Edey that the issue

was not so much whether there was uncompetitive conduct in the market, but

whether regulatory settings were conducive to the promotion of sufficient

competition to put downward pressure on credit card interest rates.4

In part, the committee's inquiry has been directed at understanding whether

existing regulatory settings in relation to credit cards are appropriate in

this respect. More broadly, the committee has sought to determine what

might be done to improve competition in the credit card market or otherwise

put downward pressure on credit card interest rates."

"Increasingly, central banks are being given

explicit authority for payments system safety and

stability, but the Board's legislative responsibility and

powers to promote efficiency and competition in the

payments system are unique.

This responsibility has broadened the Bank's

traditional focus on the high-value wholesale

payment systems which underpin stability, to

encompass the retail and commercial systems where

large transaction volumes provide scope for

efficiency gains."

"Regulation of all markets for goods and services can be

categorised according to three broad purposes. First, regulation is to help

ensure that markets work efficiently and competitively, and thus to overcome

sources of market failure. Second, regulation can prescribe particular

standards or qualities of service, especially where the consumption of goods

and services carries risks, so that safety is a focus of concern.

Third, regulation can

help achieve social objectives such as, for example, 'community service obligations' which typically take the form of price controls."

The Reserve Bank retains the same 'extensive powers' that it relied upon from 1969 to

1980, to again cap interest rates on Australian Credit Card Issuers. The Reserve Bank presently regulates the

Overnight Cash Rate. If the

Reserve Bank no longer has such regulatory powers, then those

'extensive powers' must have been

transferred to APRA, ASIC or possibly ACCC. If that is the case, then the

Reserve Bank would be able to provide a written explanation of the particular

legislation/s and legislative process for transfer of the interest rate

regulating powers and the MOI with the other regulator that accepted and

acknowledged subrogation of interest rate regulation to it.

The Campbell Committee recommended

deregulating interest rates. It did not recommend reducing the

'extensive powers'

bestowed upon the Reserve Bank by Parliamentary Acts.

Below is a quotation from Westpac's submission to the Wallis

Inquiry, submitted by the then CEO, Bob Joss,

that may have anticipated that after deregulation several Credit Card Issuers

wouldrun amuck:

The contents of this report are confidential. Data relating to

the business of the Australian Retailers Association (ARA) or its members and

contained within this submission is confidential

and is not to be released into the

public domain."

"Executive Summary

The thrust of this paper by the

Australian Retailers Association (ARA) can be summarised by a quotation from the

RBA / ACCC paper ‘Debit And Credit Card Schemes in Australia – A Study of

Interchange Fees And Access’; Page 52 states:

“ Simple economics shows that when a service is under priced, it tends to be

over-used”.

This statement in our view distills the essence of credit card

pricing and use both here and internationally. From inception, the Merchant

community has been paying a disproportionate share of the cost of credit cards.

Consumers have been paying less than the true cost of services provided to them

by

Credit Card Issuers. This we believe

was the result of credit cards at inception not having a viable economic

rationale for the consumer and Credit Card Issuers and

Acquirers structuring the

product economics in order to enhance take up. Had credit cards been priced in a

competitive environment, then it is highly likely that they would not have

gained such a major global presence.

1. interchange

between Card Issuers and

Card Acquirers

should be completely abolished and replaced with activity bases fees or fees for

service;

2. credit card

interchange is passed on to Merchants via the

Merchant Service Fee. Our own

experiences have seen interchange put to us as a ‘floor’ to the Merchant service

fee rate advanced by Acquirers;

3.

Merchant Service Fees should be

completely abolished and replaced with market negotiated activity based fees;

4.

the current credit card scheme no surcharging or non-discrimination rule be

abolished across all card types, and that Merchants

and the market not be

restricted (subject to competition law) from setting their own pricing policies.

We would encourage the RBA to take this opportunity to address a

major inequity in the Australian payments environment."

Below are pertinent arguments:

Argument 1 - The risk of extending credit to cardholders:

"The magnitude of credit card

annual percentage rates (APR) is well above other unsecured lending

rates."

Argument 2 - The cost of the

Issuerprocessing the transaction

"It is therefore reasonable for the

Issuer

to seek cost recovery and a competitive margin for this service – from the cardholder with whom a

relationship exists and for whom a service is being performed. Such a

fee for service should reflect the exact nature of the services offered

by the Issuer

to the cardholder.

The fee should be ‘internal’ to that relationship.

We would therefore argue that the cost of the

Issuer processing

a credit card transaction does not warrant an

Cardholder

who is seeking to effect payment to the

Merchant via a credit card. It is at the

Cardholder's

discretion to

select a payment method. The

Cardholder

initiates the entire credit card processing cycle

and should bear the costs of the party (the

Issuer) acting directly

on their behalf;"

Argument 3 - Costs associated with the interest free period

attached to credit cards

"We agree that the interest free period encourages potential

Cardholders

to take up card products and existing cardholders to utilise their

cards. It is very useful and beneficial for consumers to delay payment for goods

and services for some 55 days.

We would point

out that certain credit cards have zero interest free days, yet still attract identical interchange and

Merchant Service Feelevels.

The interest free period is again, a

Card Issuer / card holder

relationship cost.

The introduction and length of interest free periods was

determined by credit

Card Issuers to facilitate credit card take up and usage – both

revenue generating activities for themselves. We find it implausible

that

Issuers sought to introduce interest free periods for any reason other than to

increase their own income levels."

Argument 4 - The cost associated with providing a payment

guarantee to merchants

"We would expressly reject that any credit losses resulting to

the

Issuer from this process (card holders lodging bogus charge backs and then

not paying when proof of purchase is provided), should be passed back to

the

AnInterchange Feeis charged by the Card Issuer to the Merchant for putting the Merchant in

funds 'same day' of a

Purchase by a Credit Cardholder or a Debit Cardholder.

Credit Cards that offer the highest Rewards Programs charge the highest

Interchange Fees and

charge the highest Annual Fees which are attractive to small and large

companies, as well as sole traders, that can charge Annual Fees

as a legitimate tax deduction. Rewards under

Rewards Programsare not assessed as taxable income by the ATO.

"The tendency for interchange rates to rise to high levels is most apparent in unregulated

jurisdictions like the United States

where credit card interchange rates in the MasterCard system are as high as 3.25 per cent plus

10 cents, implying that – after scheme fees and acquirer margin – some merchants may pay over 3½

per cent in merchant service fees for high rewards cards."

"The

new interchange standards will result in a reduction in payment costs to

merchants, which will place downward pressure on the costs of goods and

services for all consumers, regardless of the payment method they use.The

weighted-average benchmark for credit cards has been maintained at 0.50 per

cent, while the benchmark for debit cards has been reduced

from 12 cents to 8 cents. The weighted-average benchmarks will

be supplemented by ceilings on individual interchange rates which will

reduce payment costs for smaller merchants.Commercial

cards will continue to be included in the benchmarks, but the Board has

decided for the present against making transactions on foreign-issued cards

subject to the same regulation as domestic cards. Schemes will be required

to comply with the benchmarks on a quarterly frequency, based on

weighted-average interchange fees over the most recent four-quarter period.

These tighter compliance requirements will ensure that the regulatory

benchmarks are an effective cap on average interchange rates. The new

interchange standards will largely take effect from 1 July 2017."

Regulation is needed to limit

interchange fees because competitive forces in the payments card market do

not have the usual effect of bringing costs down. Where merchants feel

unable to decline particular cards (because consumers expect to be able to

pay with that card and may take their business elsewhere if they cannot),

card schemes tend to have strong incentives to raise interchange rates.

Evidence from a range of countries suggests that competition between

well-established payment card schemes can lead to the perverse result of

increasing the price of payment services to merchants (and therefore to

higher retail prices for consumers). The conclusion of the Reserve Bank in

Australia, and by other regulators internationally, is that regulation is

needed to contain the upward pressure on interchange fees. Previous attempts

at self-regulatory responses to this issue have not proved feasible."

"Option 3

:

Regulatory

– modifying the regulatory regime, retaining the existing

weighted-average interchange benchmark for credit cards but enforcing it

more effectively with more frequently observed (quarterly) compliance, and

supplementing it with maximum caps on interchange rates. Companion cards

would be regulated in the same way as cards in the four-party schemes. The

weighted-average benchmark for debit cards would be reduced, consistent with

changes in average transaction values, and maximum caps would also apply to

debit card rates. Prepaid cards would be brought formally into line with

debit card interchange regulation. Permitted surcharge levels would be

defined more narrowly to ensure more effective enforcement against excessive

surcharging. Payments card acquirers would have to provide periodic

statements with more detailed costs of acceptance to merchants."

the

(RBA's

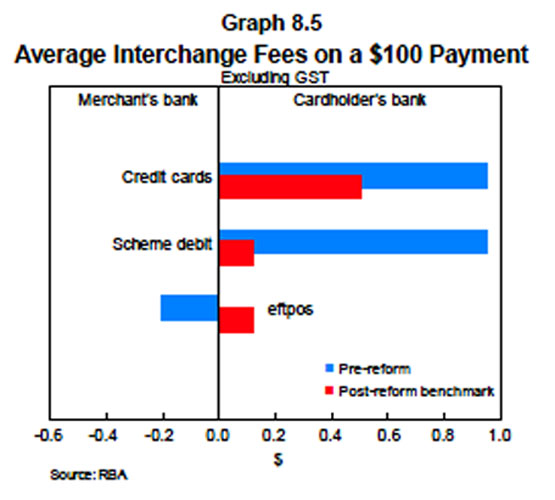

"interchange fee reforms have brought down the average

interchange fees paid in the international systems and have

reduced the gap between interchange fees in the credit card,

scheme debit card and eftpos systems (Graph 8.5). The broader