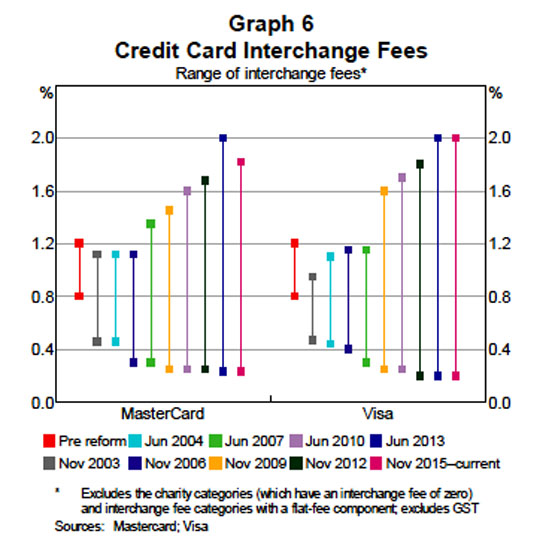

The Reserve Bank allows Credit Card Issuers to charge as low as 0.20% and as high as 2% (Graph No 6 below) for Credit Card Issuers to perform the same Interchange Fees Services

An Interchange Fee is charged by the Card Issuer to the Merchant for putting the Merchant in funds 'same day' of a Purchase by a Credit Cardholder or a Debit Cardholder.

(ii)

paid to the Card Issuer to cover -

a)

funding cost up to 55 days;

b)

electronic hardware and software handling costs;

c)

fraud and bad debt costs; and

d)

the risk involved in approving the payment.

Credit Cards that offer the highest Rewards Programs charge the highest Interchange Fees and charge the highest Annual Fees which are attractive to small and large companies, as well as sole traders, that can charge Annual Fees as a legitimate tax deduction. Rewards under Rewards Programs are not assessed as taxable income by the ATO.

An Interchange Fee is a fee for performing a) to d) above. Rewards Programmes are a lure to entice Credit Cardholders to make Purchases with their Credit Card/s.

Applying the User Pays Principle, the Interchange Fee is mutually exclusive of Rewards Programmes. They are as different as Chalk and Cheese.

"In four-party card schemes (such as MasterCard and Visa), rewards programs are, for the most part, funded by interchange fees."

The following statement is from the Reserve Bank's Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - August 2015

"The rewards programs offered by credit card issuers are due in large part to the existence of interchange fees."

"The Reserve Bank 'Standard' on interchange fees, came into effect in July 2003. In 2003, the Reserve Bank placed a cap on interchange fee arrangements in the major card schemes to address this – initially counterintuitive – result of competition driving prices up.

4"Looking at Reserve Bank reforms to reduce Interchange Fees, the Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - Aug 2015 noted "the Joint Study (RBA and ACCC 2000) found that there was very little transparency in the arrangements underlying card payment systems. It found that the card systems, exercising market power, tended to have arrangements that detracted from the efficiency and competitiveness of Australia's payments system:

The following two statements are from the Reserve Bank's Review of Card Payments Regulation dated May 2016 - Questions & Answers Card Payments Regulation:

"The tendency for interchange rates to rise to high levels is most apparent in unregulated jurisdictions like the United States where credit card interchange rates in the MasterCard system are as high as 3.25 per cent plus 10 cents, implying that – after scheme fees and acquirer margin – some merchants may pay over 3½ per cent in merchant service fees for high rewards cards."

"The new interchange standards will result in a reduction in payment costs to merchants, which will place downward pressure on the costs of goods and services for all consumers, regardless of the payment method they use. The weighted-average benchmark for credit cards has been maintained at 0.50 per cent, while the benchmark for debit cards has been reduced from 12 cents to 8 cents. The weighted-average benchmarks will be supplemented by ceilings on individual interchange rates which will reduce payment costs for smaller merchants. Commercial cards will continue to be included in the benchmarks, but the Board has decided for the present against making transactions on foreign-issued cards subject to the same regulation as domestic cards. Schemes will be required to comply with the benchmarks on a quarterly frequency, based on weighted-average interchange fees over the most recent four-quarter period. These tighter compliance requirements will ensure that the regulatory benchmarks are an effective cap on average interchange rates. The new interchange standards will largely take effect from 1 July 2017."

Review of Card Payments Regulation - Regulation Impact Statement - May 2016 includes:

"1.2 Why is government action needed?

Regulation is needed to limit interchange fees because competitive forces in the payments card market do not have the usual effect of bringing costs down. Where merchants feel unable to decline particular cards (because consumers expect to be able to pay with that card and may take their business elsewhere if they cannot), card schemes tend to have strong incentives to raise interchange rates. Evidence from a range of countries suggests that competition between well-established payment card schemes can lead to the perverse result of increasing the price of payment services to merchants (and therefore to higher retail prices for consumers). The conclusion of the Reserve Bank in Australia, and by other regulators internationally, is that regulation is needed to contain the upward pressure on interchange fees. Previous attempts at self-regulatory responses to this issue have not proved feasible."

"Option 3

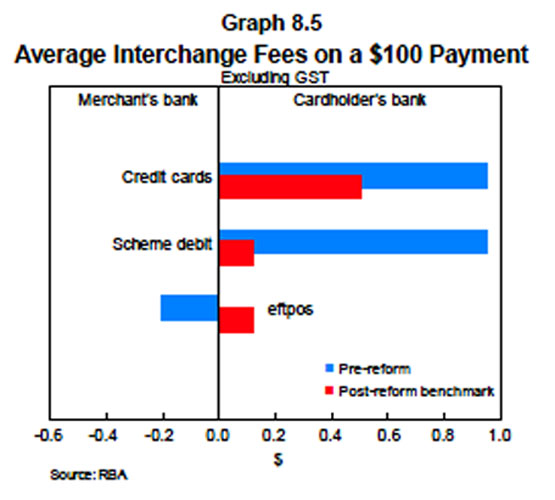

: Regulatory – modifying the regulatory regime, retaining the existing weighted-average interchange benchmark for credit cards but enforcing it more effectively with more frequently observed (quarterly) compliance, and supplementing it with maximum caps on interchange rates. Companion cards would be regulated in the same way as cards in the four-party schemes. The weighted-average benchmark for debit cards would be reduced, consistent with changes in average transaction values, and maximum caps would also apply to debit card rates. Prepaid cards would be brought formally into line with debit card interchange regulation. Permitted surcharge levels would be defined more narrowly to ensure more effective enforcement against excessive surcharging. Payments card acquirers would have to provide periodic statements with more detailed costs of acceptance to merchants."Below is Graph 8.5 from Submission to the Financial System Inquiry - RBA - March 2014 which notes:

the (RBA's "interchange fee reforms have brought down the average interchange fees paid in the international systems and have reduced the gap between interchange fees in the credit card, scheme debit card and eftpos systems (Graph 8.5). The broader effects of the interchange reforms are discussed below."

The Reserve Bank has followed the lead of the US central bank in regulating excessive Surcharging. Interchange Fees charged to Merchants have also been reduced, but seemingly more due to effective lobbying by merchant associations with the other three parties within the

Wholesale Supply Side.Post-reform benchmarks, the Credit Cardholder's bank now receives only about a $0.50c Interchange Fee on a $100 Merchant sale instead of $0.98c approx.. The Merchant's bank, known as the Card Acquirer, now receives nothing on a eftpos transaction where previously it received $0.20c.

"Issues Paper" dated March 2015 "Review of Card Payments Regulation 3. Developments in the Card Payments Market" includes 15 graphs which 'prima facie' evidences that the Reserve Bank enjoys virtually unlimited access to data from MasterCard and Visa Four Party Scheme Providers.

|

Below RBA Graph No 8 (as at March 2015) evidences the substantial range of Interchange Fees Categories: * MasterCard - 18 Categories * Visa - 23 Categories |

|

Below RBA Graph No 6 (as at March 2015) evidences the substantial increase in the range of Interchange Fees from Pre-2001 to 2015: * MasterCard in 2015 - from as low as a quarter of one percent up to 1.75 percent fee * Visa in 2015 - from as low as a fifth of one percent up to 2 percent fee |

|

Below

RBA Graph No 4 (as at March 2015) shows the

Market Share of Card Schemes: |

Below are pertinent extracts from Reserve Bank's Review of Card Payments Regulation - Conclusions Paper - May 2016 - Section 3.4.9 Implementation timeline:

"Conclusions: Interchange

The weighted-average credit benchmark of 0.50 per cent will be maintained.

The weighted-average interchange fee benchmark for debit cards will be reduced to 8 cents per transaction, which will apply jointly to debit and prepaid cards in each scheme.

Interchange fee caps will be supplemented by ceilings on individual interchange rates: 0.80 per cent for credit; and 15 cents, or 0.20 per cent if the interchange fee is specified in percentage terms, for debit and prepaid.

To prevent interchange fees drifting upwards in the manner that they have previously, compliance with the benchmark will be observed quarterly rather than every three years.

A scheme will be required to reset its interchange schedule in the event that its average interchange fee over the previous four-quarter period exceeds the benchmark.Commercial cards will continue to be included in the benchmark and will be subject to the ceilings above.

The new interchange benchmarks will take effect from 1 July 2017."

Below is a further extract from Reserve Bank's Review of Card Payments Regulation - Conclusions Paper - May 2016 - Section 3.4.

8 Changes to benchmark compliance:"When the benchmarks for credit card interchange fees were introduced in 2003, the Board’s aim was to limit the tendency for competition between schemes to drive up interchange fees. By setting the benchmarks in weighted average terms, the Bank allowed schemes significant flexibility to set different interchange fees for different transactions, some of which could be over the benchmark. Schemes have taken advantage of this, and of the current infrequent compliance arrangements, to develop commercial strategies that encourage issuers to maximise interchange revenue. The result has been that actual average interchange fees have tended to be higher than the regulatory benchmark and have drifted further above the benchmark between the three yearly compliance points. Accordingly, the benchmark has not represented an effective cap on average interchange fees."

=====================================================================================

Refer:

Summary Page re Written Questions and the Grounds/Reasons

Grounds/Reasons (one document with 21 Chapters)

Grounds/Reasons (21 separate Chapters)

Written Questions (one document with Written Questions)

Written Questions (Individual Written Questions)