|

| |

Grounds/Reasons for

the Written Questions

Chapter

10. The CEO's of the Four Pillars were questioned by a

House of Representatives Standing Committee on Economics

in Oct 2016

Three

CEO's, and likely several Senate Committee members, are unaware of the Reserve Bank's

above noted

'extensive powers' to gather information from a

payment system or from individual participants

CEOs would like you to believe that Credit Card Products have very high

bad debt write-offs, but do they? What annual write-off amount is high for

a Pillar Bank?

Below are extracts

from SMH reports of

questions asked of some of the four CEO's by the

House of Representatives Standing Committee on Economics - Review of Australia's

Four Major Banks in

Oct 2016:

LNP's Scott

Buchholz asked how much revenue Westpac's credit card business

generates.

"Where would you

allocate the profit to?"

"We don't have a credit card business,"

Westpac's CEO, Mr Hartzer responded that credit

cards fell within multiple business units.

After a brief

circular exchange Committee Chair David Coleman intervened by asking Mr Hartzer

to confirm he wasn't answering the question.

"What I'm saying is

that we're not able to

answer that question because we don't have a credit card business per se,"

Mr Hartzer said.

David Coleman

noted the Committee might be in-touch about this issue.

Labor’s

Matt Keogh is curious about the profitability of credit cards and asked ANZ

CEO , Shane

Elliot, who responded:

“I’m not sure that we disclose that,

but I’ll give you a rough idea. It would be, after tax, a couple of hundred

million dollars,”

Elliott acknowledged that it is a large amount of money,

albeit a small share of the banks’ overall earnings.

The Australian - 6 Oct 2016 reported that Commonwealth Bank's chief

executive, Ian Narev, resisted providing returns across products, claiming

these are commercially sensitive for competitive reasons.

A

CEO commented that the Credit Card Product has

"high risk debt" and did not encourage customers "to take on high amounts of

high-risk debt":

"Commonwealth Bank boss, Ian Narev, has defended the

bank’s exorbitant credit card interest rates, insisting it’s high-risk debt, AAP writes.

Mr. Narev was grilled today over credit card rates. He was asked why the cash advance rate on the

bank’s low rate card was more than 21 per cent, when the official cash rate is

just 1.5 per cent. “To me, that’s gouging, that’s excessive,” coalition

backbencher Scott Buchholz said. “It is a highly profitable part of the business,

how is that fair?”

Mr. Narev said he understood the concerns, but

argued the bank did not encourage its customers to take on high amounts of

high-risk debt.

“I said we came in here with a spirit of openness

and listen to suggestions and we will,” Mr. Narev replied."

CBA CEO, Ian Narev, deflected questions on the profitability of Credit Cards:

*

"We don’t disclose the returns on equity by individual products,” he said in

response to questioning from Labor MP Pat Conroy.

*

“In highly competitive markets, you don’t want these individual aspects of

product profitability disclosed to your competitors.”

Below are extracts

from SMH reports of

questions asked of some of the four CEO's by the

House of Representatives Standing Committee on Economics - Review of Australia's

Four Major Banks in

Oct 2016 which provides a 'ball park' brake-up of the Credit Card business by

the ANZ CEO,

Shane Elliot:

Shane Elliot has given Liberal MP Scott Buchholz an

illustrative breakdown of costs in the credit cards business (re

the pie chart on RHS "Costs" in

Chapter 8 above):

"If the credit card

section were a stand-alone business, he says -

*

25 per cent of the cost would be the cost of funds.

*

another quarter would be features - insurance, reward points etc

*

while about a third are the administrative systems needed.

*

the balance, slightly less than 20 per cent, is lost through bad debts and

fraud."

ANZ CEO, Shane Elliot, responded to a question about

the profitability of credit cards,

“I’m not sure that we disclose that, but I’ll give you a rough idea. It would

be, after tax, a couple of hundred million dollars,”

Elliott says, acknowledging it is a large amount of money

albeit a small share of the banks’ overall earnings.

ANZ

to consider slicing credit card rates: ANZ Banking Group will consider

cutting interest rates on its credit cards and introducing a pricing regime

based on "borrower risk".

Shane Elliott, CEO ANZ said:

The bank is currently looking at

changing the parameters for credit cards to ensure people can avoid

financial hardship.

“It’s the right thing for us as well ... It’s not in our

interest to have customers with products they can’t service,”

he says.

Pressed by Liberal MP Scott Buchholz whether there was

“ample opportunity”

for card rates to be lower, Mr. Elliott said:

“As a general proposition, I think you’re right.”

“I think there’s an opportunity for us frankly

to take a bit of leadership on this and do something better on not just the

interest rate but also the fee structure on cards,”

Shane Elliott said.

He also said ANZ would look to

harness big data to discover low-risk customers that could be offered lower

interest rates.

Andrew Thorburn, CEO NAB said

"The credit

card business has some of the 'highest losses in our portfolio' and one third of

their customers were on a 13.99 per cent 'low rate' card."

The

Four Pillars

bad debt

write-off rates would be lower and discourage

"its customers to take on high amounts of high-risk debt", if

all Credit Card Issuers in

Australia were regulated to -

A) limit school leavers

from 18 years

to a

Charge Card for the initial six months,

thereby necessitating the

Total Amount Owing

to be repaid at the end of each monthly cycle, in order to establish/improve their

Credit Rating;

B) then

(after six months of repaying the

Total Amount Owing

each month in arrears)

replace their

Charge Card

with a Credit Card

with a prudent

Card Limit which could be increased no more than once a year according to the

Credit Cardholders'

Credit Rating;

and

C) require all

Credit Cardholders to pay a minimum of

25% of the

Total Amount Owing

each month,

whereby

Cardholders could contact their

Credit Card Issuer and request their Credit Card Issuer to reduce the monthly

limit to 5% for up to two years dependant upon the normal parameters governing

an

Unsecured Personal Loan

application.

Re C) above,

McKinsey Report -

May 2014 categorizes 'Five Segments' of Credit Cardholders in the USA.

Below is an extract from the 'Third Segment' of

USA Credit Cardholders,

namely 'Financially

stressed' Credit Cardholders:

"Value simplicity and transparency in fees, rates and terms, but their

biggest need is for something that NO credit card offers: a mechanism

allowing them to impose their own spending limits which would enable them to

carry a credit card for larger purchases that take time to pay off, without

fearing they might be tempted to use it for non-essentials."

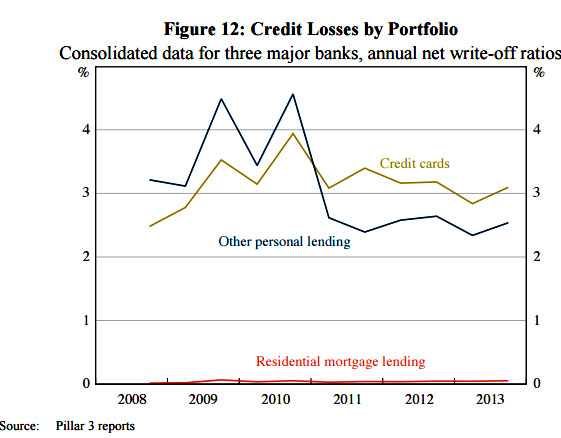

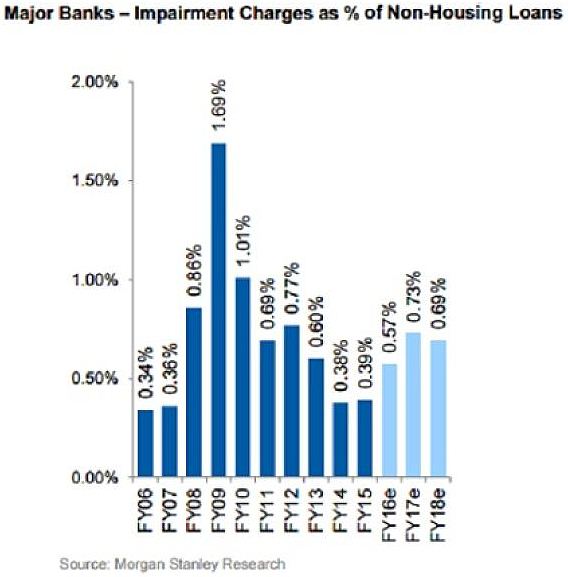

The

below three graphs seek to identify write-offs on Credit Cards by the major

Australian Credit Card Issuers.

|

The above graph from

Reserve Bank's

Credit

Losses at Australian Banks: 1980–2013 shows annual net write-offs for

Credit Cards for three of the Four Pillars

in 2013 was 3.1% of Debt Outstanding.

The above RBA graph seems to infer that

for every $100 funded by a Credit Card Issuer to a Credit Cardholder, the Credit

Card Issuer will not get $3.10 back in 2013. But are Credit Card Issuers

making 17% on ave. before costs on the remaining 96.9% Credit Cardholders?

|

|

The above Morgan Stanley Research graph estimates that 'Impairment Charges as %

of Non-Housing Loans' will increase -

*

from 0.39 per cent of total non-mortgage loan books in 2015

*

to 0.57 per cent upwards to 0.73 per cent in 2017.

The above

Morgan Stanley graph

seems to infer that for every $100 funded by a Credit Card Issuer to a Credit

Cardholder, the Credit Card Issuer will not get back $0.73 in 2017.

|

|

The above graph taken from

Submission

to the Financial System Inquiry - RBA - March 2014

surprisingly shows that non-housing lending losses -

* were less than $0.45 per $100 in

July 2009 (immediately after GFC); and

* were about $1.10 per $100 in

mid-2013.

|

=====================================================================================

Refer:

Chapter

11.

Summary Page re Written Questions and the Grounds/Reasons

Grounds/Reasons

(one document with 21 Chapters)

Grounds/Reasons

(21 separate Chapters)

Written Questions

(one document with Written Questions)

Written Questions

(Individual Written Questions)

| |

|