Convenient Free Ride or Free Riders means 67% circa of Credit Cardholders are Transactors that Enjoy The Three Purchase Benefits of Tap and Go reliant upon costly electronic infrastructure under Four Party Schemes and Three-Party Schemes using one or more Revolving Lines Of Credit to make 264 on average Purchases per Credit Cardholder p.a. that aggregate to approx. $27,000 pa. (cell I31) with no, or an immaterial, Annual Cardholder Fee.

Transactors enjoy a Line/s Of Credit by paying for goods and services up to 55 days after receipt, rather than visiting an ATM to draw cash and then carry cash the way we all did 20 or more years ago is a material convenience and security benefit. Paying Tap and Go with a Credit Card is a highly sought after and convenient payment method for many millions of Australians. Yet one third of Credit Cardholders (Revolvers) pay the provisioning costs of the other two thirds of Credit Cardholders (Transactors).

Many Transactors earn in excess of $100 annually in Rewards Programs that are income tax and FBT free.

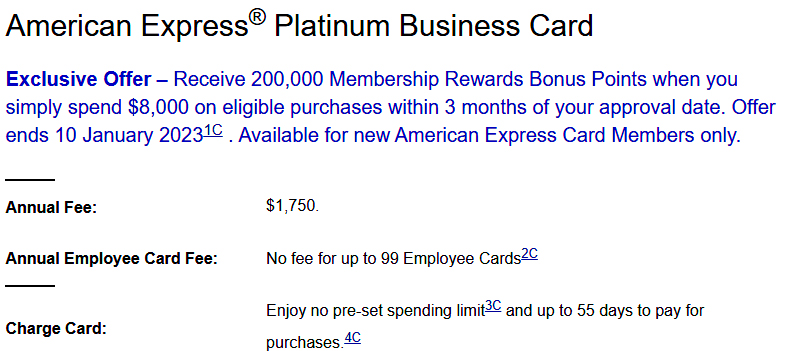

Some Transactors pay as high as $1,750 pa. Annual Charge Card Fee that is tax deductible to increase their Rewards Programs benefits that are non-taxable.

The American Express Platinum Business Card has an Annual Fee of $1,750 (usually tax deductible) and provides copious untaxed personal income.

Credit Cardholders of Credit Cards such as the 'Citi Select Credit Card' usually treat their an annual fee of $700 as a 'company tax write-off', and the $600 to $800 in flight tickets, luxury items or cash that they receive annually as 'tax free income'.

If Rewards Programmes 'Reward Points' are converted to flight tickets, luxury items or cash and the Credit Cardholder of the 'Citi Select Credit Card' (or comparable) is -

(a) an employee and the Credit Card is provided by the employer, then the ATO should deem such receipts as a fringe benefit and therefore income taxable; and

(b) not an employee, then the ATO should deem such receipts as taxable income in the same manner that the ATO deems bank interests receipts as taxable income.