If credit card

scheme restrictions were to remain largely unchanged, the main beneficiaries

of the arrangements would continue to be:

(i)

credit card Transactors who settle their credit card account in full each

month; and

(ii) credit card

Scheme Members and the

Schemes

themselves.

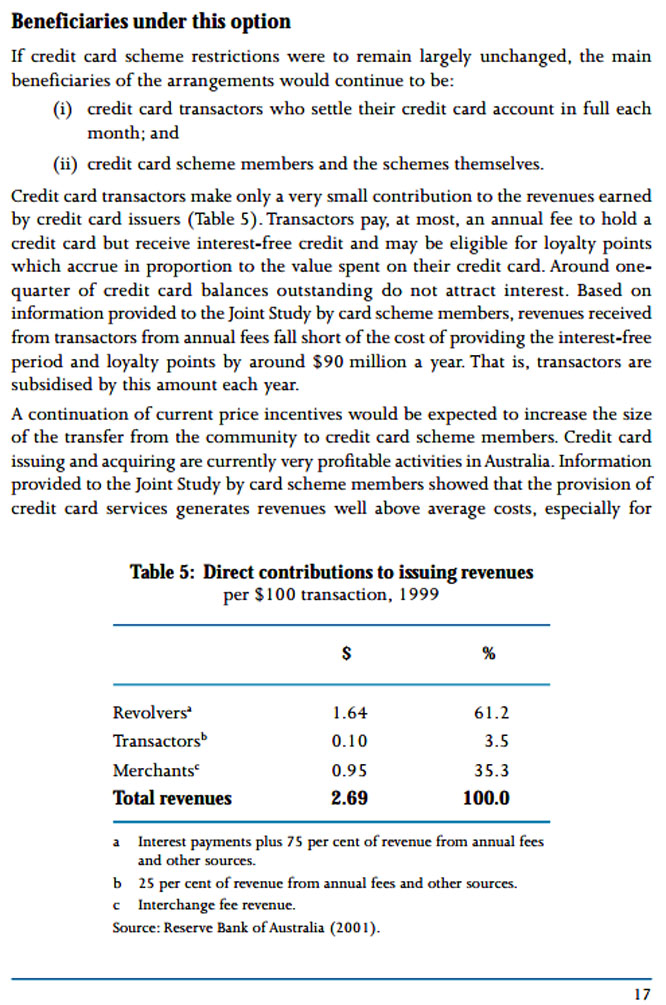

Credit card Transactors make

only a very small contribution to the revenues earned by credit card issuers

(Table 5 below). Transactors pay, at most, an annual fee to hold a

credit card, but receive interest-free credit and may be eligible for

loyalty points which accrue in proportion to the value spent on their credit

card. Around one quarter of credit card balances outstanding do not

attract interest.