Below is an extract from A POCKET FULL OF CHANGE - The House of Representatives Standing Committee on Finance and Public Administration - Banking and Deregulation - Nov 1991:

|

|

Insert one of the two enclosed CDs into a Windows computer to auto-open this page. Left click on it and then left click on the welter of embedded URLs in Blue Text, Red Text or Black to open associated files. To leave a page and return to the previous page, click on the arrow at top left of your screen/monitor.

If this page accidentally closes when you leave another page, right click on

your CD Drive icon and left click on 'Open Auto Play'. If using a MAC, or the enclosed USB stick, or the enclosed CDs do not auto-open this letter, then navigate to CreditCards/Comms/Letter_to_Jim_Chalmers_7-Sept-22.htm

Evidence Facts Sheet Thirty-Two Questions Directed at Three Financial Services Regulators and Supporting Evidence Two Exceedingly Costly Interest Charging Practices Defined Terms and Documents Unit 5, 13-15 Stokes StLane Cove North NSW 2066 scribepj@bigpond.com 0434 715.861 7 September 2022

Hon. Dr. Jim Chalmers jim.chalmers.mp@aph.gov.auFederal Treasurer, Australian Labor Party

PO Box 6022,

House of Representatives,

Parliament House

PO Box 349 Dear Dr. Chalmers

Review of the Reserve Bank Three Questions to the Federal Treasurer regarding Australia's Principal Regulator of the Payments System adherence to its statutory obligations to "best contribute to.......... the economic prosperity and welfare of (ALL) the people of Australia" regarding Credit Card Products, in particular application of the User Pays Principle

"3. The Review will exclude the RBA's payments, financial infrastructure, banking, and banknotes functions". ==========================

========================== If the Writer does not receive an adequate written response from the Federal Treasurer to his above THREE QUESTIONS within two weeks and two days of the date of this letter, the Writer will post this letter to some of the interested parties that have expressed concerns (listed in Annexure A) under covering letter (on CD, USB and A4). Annexure B is his prepared letter to three concerned journalists and the CEO of CHOICE. The welter of the embedded URL files (will be accessible) that date back to the Writer's Extensive Submission to the RBA dated 8 Dec 2011 which sought application of the User Pays Principle to Credit Card Products, principally by re-introducing an interest rate Cap on each of Purchases and Cash Advances. The Writer's concern is that the User Pays Principle has to date not applied on the Retail Supply Side because the diversity of Credit Cards are exceedingly complex financial products, beyond the mental capacity of all but a few, which is why the Writer has thousands embedded threads to many thousands of pertinent files and expended an abundance of hours research since mid-2011. However, pricing arrangement within the Wholesale Supply Side are reasonably equitable because the 'parties' under the Four-Party Schemes and Three-Party Schemes (except Credit Cardholders) had powerful lobby groups to Argy Bargy reasonably equitable pricing for inter alia Merchant Service Fees. The Writer expects that many parties (that have written about Credit Card wroughts over the last 25+ years, listed in Annexure A) will be surprised that a Labor Govt opted to abandon its 'rusted on' Labor voters, as many have been or still are Persistent Revolvers, by not holding Australia's Principal Regulator of the Payments System to account -

========================== The RBA, the Principal Regulator of the Payments System, is obligated "....to ensure that the monetary and banking policy of the Bank .... is directed to the greatest advantage of the people of Australia and that the powers of the Bank ... are exercised in such a manner as, in the opinion of the Reserve Bank Board, will best contribute to ...... the economic prosperity and welfare of the people of Australia.'’ Prior to the Campbell Report circa early 1980's, the RBA regulated all Australian bank interest rates with an Iron Fist dating back to the failure of banks in the 19th century - "... when de-regulation resulted in adverse consequences, re-regulation ensued...".

The incumbent Federal Labor Govt has opted to omit reviewing a vital responsibility of the Principal Regulator of the Payments System, from the much heralded, long overdue review of Australia's banking regulator. Despite during the last 25+ years, the Principal Regulator of the Payments System overlooked many hundreds of thousands of Persistent Revolvers that represent a mere 12.58% circa of all Credit Cardholders, yet contributed a whopping 80% circa of Credit Cardholders' Contribution To Credit Card Issuers Gross Revenue, too often suffering Extreme Financial And Emotional Distress. Whilst 67% circa of Credit Cardholders, labeled by the RBA as Transactors, ".... normally pay an annual fee, they pay no transactions fees, enjoy the benefit of an interest-free period and in many cases earn loyalty points for each transaction." Finder reports that there were 13,161,440 credit cards in Australia as of June 2022, carrying a national debt accruing interest of $18.2 billion. A mere 13.58% circa of all Credit Cardholders (issued in Aust), those identified by the RBA as Persistent Revolvers incurred $14.56 billion of that $18.2 billion interest debt last year. Two thirds of Credit Cardholders paid none of that huge interest burden; Transactors effectively enjoy their Line/s of Credit for FREE. In 2015 the principal solicitor with the Financial Rights Legal Centre, Alexandra Kelly, reported to the SMH that the biggest debt she had seen on a single Credit Card was $90,000, while clients with multiple cards can end up owing hundreds of thousands of dollars. "We have had cases of people who have accrued debts of $100,000 or $200,000 on multiple cards - that is the worst case scenario," she said. Quotes from reputable Credit Card Distress Authorities about unconscionable advertising of Credit Cards by Credit Card Issuers resulting in some indebted Credit Cardholders being issued multiple Credit Cards. The Journal of Economic Psychology contends that "The underlying premise is that people with high numeracy accumulate more wealth than people with low numeracy. Previous findings are consistent with the hypothesis that numeracy is related to wealth and wealth growth." Since the early 1990s hundreds of thousands on Labor's loyal to the core 'rusted on' voters too often with low Financial Literacy Capacity generally through no fault of their own have paid over $20,000 each in Interest and Penalty Fees on Credit Card Products because the Reserve Bank Board overlooked Credit Card Issuers explicitly Targeting Credit Cardholders With Low Financial Literacy Capacity through Predatory Advertising that Federal Parliament had entrusted it (back in 1959 under Nugget Coombs) to inter alia "....best contribute to.......... the economic prosperity and welfare of (ALL) the people of Australia". Labyrinth of ‘Concealed Spiders’ exposes 'n ine examples' of Unconscionable Conduct from Predatory Advertising of some Credit Cards.Below is an extract from Reform of Credit Card Schemes in Australia: RBA's "A Consultation Document" – Dec 2001 - Executive Summary where the RBA acknowledged that - A. Revolvers "... pay interest rates significantly above rates on other forms of unsecured lending"; and B. a much larger cohort, described as Transactors, did not pay for their Lines Of Credit that they benefited from, with many ..... earning loyalty points for each transaction:

In 2001 the RBA undertook to adopt "A movement towards a “user pays” approach to credit card payment services would be consistent with the approach adopted by Australian financial institutions in pricing other payment instruments under their control." But the RBA never actioned the blinkin obvious by recommending to the Federal Treasurer to re-impose a Cap on the maximum credit card interest rate able to be charged that was lifted in April 1985 during an era of unprecedented high interest rates. Below is an extract from Credit card interest rates 'inexplicably high': Choice - Rachel Browne - SMH - 1 June 2015:

Persistent Revolvers (12.58% circa of Credit Cardholders) invariably possess low Financial Literacy Capacity have paid 80% circa of Credit Card Issuers Interest And Penalty Fees Revenues. A portion of Credit Card Issuers operating costs is funding Rewards Schemes that many of the Financially Educated Transactors enjoy a Free Ride - at no material cost and income tax free Rewards Schemes. Interchange Fees levied upon Merchants funded the remainder of Rewards Schemes. Hardly, an example of the User Pays Principle.. Since the early '90s some Credit Card Issuers brazenly lured Financially Uneducated And Vulnerable Australian Credit Cardholders with low Financial Literacy Capacity by marketing Balance Transfer offers intent upon snaring (from other Credit Card Issuers) the most lucrative payers of Interest and Penalty Fees.

Over the last 25+ years in the region of one million Financially Uneducated And Vulnerable Australian Credit Cardholders with low Financial Literacy Capacity, identified by the RBA as Persistent Revolvers, have been preyed upon by Predatory Advertising. Around three quarters of a million Financially Uneducated And Vulnerable Australian Credit Cardholders have paid in excess of $20,000 in Interest and Penalty Fees, too often enduring Unconscionable Credit Card Interest Charging at Usurious Interest Rates. Evidence Of Unfair Credit Card Practices Which Prey Upon Financially Uneducated And Vulnerable Australians by Numeracy And Literacy Discrimination contains a veritable welter of proof, across a variety of platforms, of inter alia Extreme Financial And Emotional Distress Suffered by the 400,000 circa (as at 2017) Eligible Persistent Revolver Plaintiffs that had paid in excess of $20,000 in Interest and Penalty Fees, too often enduring Unconscionable Credit Card Interest Charging at Usurious Interest Rates that the Writer identified in his Submission to Maurice Blackburn (on CD) dated 25 June 2017 that sought Maurice Blackburn to run a Class Action against the RBA. The Writer's Submission to Maurice Blackburn contended that 400,000 circa Eligible Persistent Revolver Plaintiffs that were Financially Uneducated And Vulnerable Australian Credit Cardholders with low Financial Literacy Capacity had been overtly preyed upon by Predatory Advertising. Julian Schimmel, Principal Lawyer in Maurice Blackburn's class actions department wrote a two page response dated 14 July 2017. Australia's Principal Regulator of the Payments System breached its Statutory Duty and its Fiduciary Duty to "best contribute to.......... the economic prosperity and welfare of (ALL) the people of Australia" by not recommending to the Commonwealth Govt (under Section 11(1) of the Reserve Bank Act 1959) that it (RBA) be authorised to re-impose a maximum interest rate Cap on Credit Cards when as far back as June 1992, the spread between the Overnight Cash Rate and the average Purchase interest rate exceeded 16%. That Cap had stood at 18% until it was removed in April 1985 when the spread/margin between Overnight Cash Rate and that 18% interest rate Cap was less than 1%. By not recommending (from 1992) that the Commonwealth Govt. regulate a maximum Purchase Interest Rate and a maximum Cash Advance Interest Rate when the spread between the Overnight Cash Rate and the average Purchase interest rate exceeded 16%, Australia's Principal Regulator of the Payments System breached its Statutory Duty and its Fiduciary Duty to the enormous detriment of several hundred thousand Persistent Revolvers that through no fault of their own possessed low Financial Literacy Capacity and were easy prey to Predatory Advertising. In Aug 2021 the difference between the Overnight Cash Rate of 0.10% and the Standard credit card Purchase interest rate of 19.94 was 19.84%. 22 years ago (Aug 2000) the spread between the standard Purchase interest rate and the Overnight Cash Rate was a mere 10.39% (16.64% - 6.25%).

1. Overview Back in 2011, after sharing emails with Ms. Sharon van Etten, Public Relations Officer, Media & Public Relations Office, RBA, the Writer posted his extensive submission (on 3 CDs and A4) to the RBA on 8 Dec 2011 seeking application of the User Pays Principle to Credit Card Products. His follow up email to Ms. van Etten sent 16 Dec 2011 and 20 Dec 2011 were not answered. Section 8 of his submission accords with recommendations within "RBA's Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001. "A movement towards a “user pays” approach to credit card payment services would be consistent with the approach adopted by Australian financial institutions in pricing other payment instruments under their control."

Below is an extract from the Writer's email to Ian Chua, Senior Communications Officer, Media and Communications, RBA sent 16 March, 2017 3:19PM: Those four former RBA colleagues epitomised the prevailing culture that the Reserve Bank was chartered under Parliamentary legislation to watch over the behaviour of the commercial banks. In May 2020, Choice CEO, Alan Kirkland, asserted that Credit Card Providers have stolen $6.3 billion from customers “by failing to pass rate cuts on for credit cards, banks have effectively stolen $6.3 billion from the pockets of Australians,” Mr Kirkland said. * "The 10 costliest credit cards in Australia – and why you should avoid them like the plague" - CHOICE

* "CHOICE

is calling on banks to cap interest rates at 10% to stop the spread of

long-term credit card debt" "Payments group SmartWayToPay is urging the federal government to put a 10 per cent limit on credit card interest rates to help people claw their way out of persistent debt........ Cutting credit card interest rates could make an important difference to those struggling financially. A 20 per cent rate on a card with $5000 debt would cost a total of $24,345 if just minimum repayments were made, compared to $8116 on a 10 per cent rate." The Writer telephoned Paul Keating's PA, Susan Grusovin, in mid-Oct 2020 and explained that he was keen to present evidence to Paul Keating that the RBA should have re-imposed a Cap on Credit Card interest rates to protect Australians with low Financial Literacy Skills because Revolvers (33% of Credit Cardholders) were paying all of Credit Cardholders' Contribution To Credit Card Issuers Gross Revenue. And 67% of all Credit Cardholders, namely Transactors did not contribute to the cost of the Credit Card System, although enjoying substantial benefits recognised by the RBA "Although they normally pay an annual fee, they pay no transactions fees, enjoy the benefit of an interest-free period and in many cases earn loyalty points for each transaction." On 28 Oct 2020 the Writer posted his detailed Submission letter to Paul Keating dated 28 Oct 2020 (on 2 @ DVD, 2 @ USB and 3 @ A4) hopeful that Paul Keating would similarly trumpet criticism of the RBA for not having re-imposed a maximum interest rate Cap on Credit Cards (as far back as June 1992 when the spread between the Overnight Cash Rate and the average Purchase interest rate exceeded 16%). The Writer emailed Paul Keating's PA, Susan Grusovin, on 29 Oct 20 and on 4 Nov 20 explaining his letter to Paul Keating dated 28 Oct 20 that include several attached files. Seemingly the former Labor Prime Minister wasn't overly concerned about the plight of hundreds of thousands of Persistent Revolvers that represent a mere 12.58% circa of all Credit Cardholders, the majority likely 'rusted on' Labor voters, yet contribute a whopping 80% circa of all Interest And Penalty Fees Revenue generated from Credit Card Products, often suffering Extreme Financial And Emotional Distress.Inaction by APRA and ASIC was attributed to some scandals exposed in the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry. Puzzlingly Australia's Principal Regulator of the Payments System came out of that Royal Commission relatively unscathed. It should not have because of the Extensive Powers bestowed upon the Reserve Bank, in particular under the Payment Systems (Regulation) Act 1998, conferred an obligation upon the RBA, pursuant to Section 11(1) of the Reserve Bank Act 1959, to inform the Commonwealth Govt. that it (RBA) needed to re-impose a maximum Credit Card interest rate limit/cap as far back as mid-1992 by -

Below is an extract from Designated and Regulated Payment Systems that evidenced that the RBA had actioned all the 'conditions precedent' in order to re-impose a maximum interest chargeable by Credit Card Issuers relying upon the Payments System Regulation Act 1998:

T he Writer believes that the Principal Regulator of the Payments System failed to notify successive Commonwealth Govt’s (obligated under Section 11(1) of the Reserve Bank Act 1959) that a maximum interest rate Cap (removed in April 1985 during hyper-inflation) needed to be re-imposed because the Overnight Cash Rate had plummeted and Credit Card interest rates were Sticky. The Principal Regulator of the Payments System failure to "best contribute to.......... the economic prosperity and welfare of (ALL) the people of Australia" that includes protecting in alios Credit Cardholders with poor Numeracy and Literacy Capacity, by so notifying the Federal Treasurer constitutes negligence and misconduct of its regulator obligations under civil law because –1) RBA’s paper "Reform of Credit Card Schemes in Aust: "A Consultation Document" in Dec 2001 argued for greater application of the User Pays Principle. As acknowledged by the RBA, Transactors do not pay the real economic cost of their Lines of Credit that they enjoy, because they meticulously pay for their Purchases up to 45 days in arrears; and2) Six Pivotal Credit Card Publications during the last 26 years, three of which were written by the RBA, identified that interest rates on Credit Card Products against reductions in the Overnight Cash Rate, were most sticky, "...The rate on credit cards is found to be the most sticky, followed by personal loan rates, the housing loan rate and the small business overdraft rate"; and 3) 12.58% circa of all Credit Cardholders, described by the RBA as Persistent Revolvers have paid 80% circa of all Interest and Penalty Fees Revenue amounting to many billions of dollars, whilst 67% circa of all Credit Cardholders, described by the RBA as Transactors, contributed zilch of that $6.3 billion of Interest And Penalty Fees Revenue quantified by CHOICE in June 2020. Hardly, an example of the User Pays Principle. Section 2 B. of Extensive Powers and Responsibilities evidence that the RBA's powers and obligations to 'inter alia' "best contribute to.......... the economic prosperity and welfare of the people of Australia" are "unique among central banks" and exceed the obligations upon the U.S. Federal Reserve and The Bank of England, to their peoples' economic prosperity and welfare - explained in The RBA has greater obligations to its people than the Bank of England or the US Federal Reserve.2. Australia's Central Bank previously regulated all bank interest rates Prior to the Campbell Report circa early 1980's, the RBA had imposed an 18% maximum interest rate upon all Credit Card Issuers. Australia's banking history evidences that "... when de-regulation resulted in adverse consequences, re-regulation ensued...". Due to failures of banks in the 19th century, Australian banks had been highly regulated. Particulars of deregulations and subsequent re-regulations are well chronicled. That 18% cap on the maximum interest rate on all Credit Cards was withdrawn in April 1985 when the Overnight Cash Rate was a smidgeon over 17% during an era of very high inflation. Until 1980 banks could not offer more than 3¾% on a passbook account. "From 1966, when personal loans were introduced, the maximum rate that banks could charge was set by the Reserve Bank." Ric Battellino, Deputy Governor, RBA acknowledged in his address to China Australia Governance Program in Melbourne (16 July 2007) that in the mid-1970s when the NBFIs were offering much higher deposit interest rates and thereby stealing depositors balances from the traditional banks, that bringing those NBFIs under the Banking Act 1959 was the initial solution:

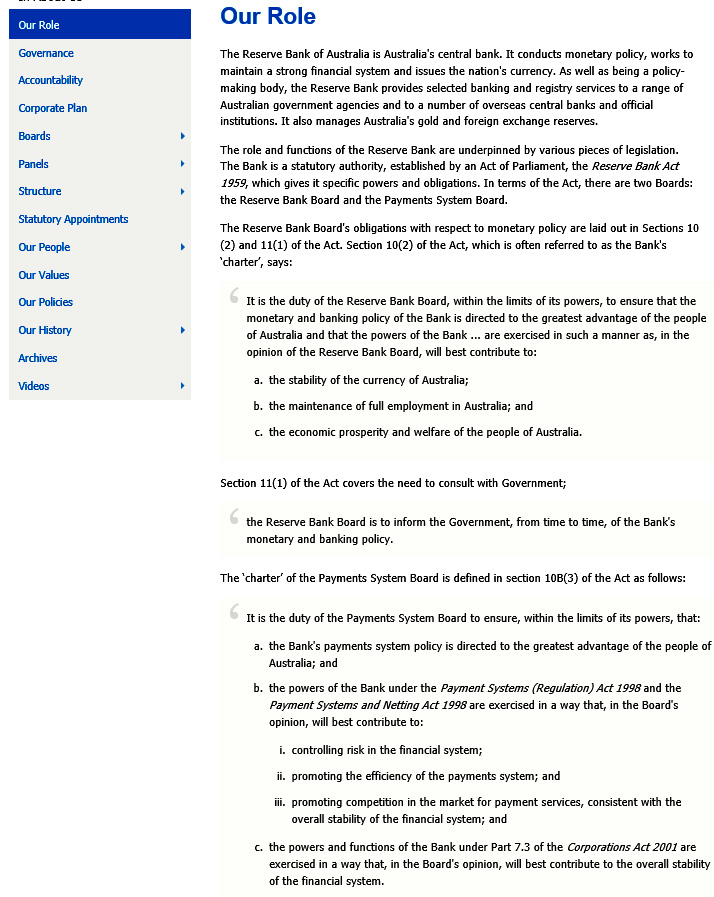

Below is an extract from A POCKET FULL OF CHANGE - The House of Representatives Standing Committee on Finance and Public Administration - Banking and Deregulation - Nov 1991: "2.59 The last move to reinforce the regulatory system was the passing of the Financial Corporations Act, 1974. It was becoming increasingly apparent that a system of implementing monetary policy through tightly regulated banks while there were relatively free non-bank financial intermediaries was leading to the banks losing business to their competitors. This was not only viewed as unfair to the banks but was weakening monetary policy. Many economists saw the solution in deregulating the banks and moving to a more market-based monetary policy. The logical alternative was to attempt to bring the non-banks within the regulatory net. This the Act could have done. However, it was decided to limit its operation to the collection of statistics and the sections covering the regulation of non-banks bas never been proclaimed. "Four Economic Reasons for the Campbell Committee Report – Sept 1981 notes inter alia that the Campbell Report recommended removal of the caps on all bank products in an era when commercial interest rates skyrocketed and building societies, credit unions and finance companies had been progressively poaching traditional national and state bank’s depositors’ balances (accounts) since the late ‘70s. “.. by the early 1980s the banks’ share of savings had fallen to 40 per cent, compared with 70 per cent in the early 1950s.” The Overnight Cash Rate peaked at over 20% in June 1984. It is doubtful that the Campbell Committee ever thought that the Overnight Cash Rate could fall to 0.1% and remain there for 18 months. 3. Australia's Central Bank's obligations to the Australian people The RBA professes itself to be the Principal Regulator of the Payments System. The RBA's "Our Role" represents to " best contribute to.......... the economic prosperity and welfare of (ALL) the people of Australia". That obligation to "the people of Australia" far exceeds the obligations upon the USA and UK 'central banks', U.S. Federal Reserve and The Bank of England respectively, to their peoples.The Payment Systems (Regulation) Act 1998 obligates the Payments Systems Board to always Act in the Public Interest. The Act "allows it to undertake more direct regulation of ‘Designated’ payments systems when it judges it to be "in the public interest". This may involve the imposition of access rules or operating standards (under Division 4, Section 18 of the Payments System Regulation Act 1998) for participants in such systems."

Below are extracts from Reserve Bank of Australia Bulletin - July 1998 - Australia’s New Financial Regulatory Framework that chronicles the Reserve Bank's powers, set out in the Payment Systems (Regulation) Act 1998, that allow the Reserve Bank to undertake more direct regulation of ‘designated’ payments systems to – "... promote competition in the market for payments services, consistent with the overall stability of the financial system..." when it judges it to be "in the public interest" which may involve the imposition of access rules or operating standards for participants in such systems: "The new Payments System Board is responsible for the Bank’s payments system policy, the objectives of which are: • controlling risk in the financial system arising from the operation of the payments system; • promoting the efficiency of payments systems; and • promoting competition in the market for payments services, consistent with the overall stability of the financial system. The Bank’s powers in this area, set out in the Payment Systems (Regulation) Act 1998, allow it to undertake more direct regulation of ‘designated’ payments systems when it judges it to be in the public interest. This may involve the imposition of access rules or operating standards for participants in such systems. The Act also provides a framework for regulation of purchased payment facilities, such as travellers cheques and stored-value cards." Below is an extract from the Writer's page titled Australia's Principal Regulator of the Payments System:

Below is a brief extract from a description of the Reserve Bank of Australia (RBA) by Clayton Utz:

4. Australia's Central Bank has failed in its obligations to "best contribute to.......... the economic prosperity and welfare of the people of Australia" To the Writer's knowledge, Australia's 'central bank' has not exercised its rights - * under Part 5—Miscellaneous, Section 26 of the Payment Systems (Regulation) Act 1998 to ask for financial data from the major Credit Card Issuers of Interest & Penalty Fees revenue for each of their Credit Cardholders for all Credit Card Products for a minimum of 12 months, or even 6 months, in order to establish if the User Pays Principle applies, notwithstanding that the RBA argued for greater application of the User Pays Principle in its paper "Reform of Credit Card Schemes in Aust: "A Consultation Document" in Dec 2001; or

* under

Section

11(1) of the Reserve Bank Act 1959

to

"

....inform the Government, from time to time,

of the Bank's monetary and banking

policy"

having regard to its obligations under

Section 10(2)

' * the RBA recommended in Dec 2001; and * the Writer recommended in Section 8 of his letter (on CD) to the RBA dated 8 Dec. 2011 - explained in Point 9 of Supporting Documentary Evidence re 1st Question. 5. ABA's Banking Code of Practice set new stringent standards of practice for banks, their staff and their representatives to take effect on or before 1 July 2019. Australia's Central Bank should have recommend to the Federal Treasurer that it regulate most of the nine ABA imposed changes at least 15 years earlier than 1 July 2019 Australia's Principal Regulator of the Payments System breached its Statutory Duty to "best contribute to.......... the economic prosperity and welfare of (ALL) the people of Australia". Its Payments Systems Board abrogated its responsibility to always Act in the Public Interest by failing to "..undertake more direct regulation of ‘designated’ payments systems when it judges it to be in the public interest" due to condoning Two Exceedingly Costly Monthly Interest Charging Practices by many Credit Card Issuers that Targeted Credit Cardholders With Low Financial Literacy Capacity, whereupon Financially Uneducated And Vulnerable Australians have suffered Extreme Financial And Emotional Distress.Two Exceedingly Costly Monthly Interest Charging Practices evidences that the Reserve Bank breached its Statutory Duty and Fiduciary Duty to Credit Cardholders with low Financial Literacy Capacity. Persistent Revolvers that account for a mere 12.58% circa of Credit Cardholders have contributed a whopping 80% circa of all Interest And Penalty Fees Revenue annually generated from Credit Card Products. The numeric dollar magnitude of those losses is explained in the Writer's Submission to Maurice Blackburn lawyers.RBA's LOAN RATE STICKINESS: THEORY AND EVIDENCE written by Philip Lowe and Thomas Rohling - Research Discussion Paper - 9206 - June 1992 recognised that Credit Card Issuers were not passing on reductions in the cost of funds, but the RBA Board did zilch about the Commonwealth Govt. regulating Credit Card Issuers to lower interest rates on their Credit Card Products, yet it possessed the Extensive Regulatory Powers to do so. Below is an extract from RBA's LOAN RATE STICKINESS: THEORY AND EVIDENCE: For credit cards, personal loans, owner-occupied housing loans and the standard overdraft rate, changes in the banks' marginal cost of funds have not been translated one for one into the contemporaneous lending rates." Unconscionable Credit Card Interest Charging focuses on a significant change in interest charging for Credit Cards that a Red Faced Australian Bankers Association, under a parachuted in, Anna Bligh, regulated ALL Credit Card Issuers in Aust. (implement by 1 July 2019) under the ABA's 'Banking Code of Practice'. These regulated changes followed years of deceit perpetrated voracity fostered under Ms. Bligh's two predecessors, David Bell and Steven Münchenberg. Below is a crucial extract from Unconscionable Credit Card Interest Charging:"ABC News article, Banks revamp code of practice in face of scandals, royal commission - (A). informed that the current CEO of the ABA, Anna Bligh, announced in late Dec 2017 that the ABA had just lodged a 'Banking Code of Practice' with the Australian Securities and Investments Commission (ASIC) for approval; and (B). listed several changes that will be legally binding on all 'member banks' of the ABA which includes: "Customers only paying interest on what remains on a credit card and not the full amount of purchase if a loan is being paid down."

Below is an extract from page 40 of Australian Banking Association Banking Code of Practice - 1 March 2020 Release:

The fact that the ABA made it mandatory in its lodged Banking Code of Practice that its members charge interest on ONLY any unpaid portion of the Closing Balance from the Payment Due Date is patent evidence that the previous long-running practice (explained in Unconscionable Credit Card Interest Charging) was Unconscionable Conduct Targeted At Credit Cardholders With Low Financial Literacy Capacity." and unfortunately countenanced by Australia's Principal Regulator of the Payments System, 6. Have reviews of the state of competition in the financial system that have been recommended by inter alios the Australian Govt been carried out?Recommendation 30 (page 254) of the Australian Govt Financial System Inquiry - Final Report - Nov 2014 recommended Strengthening the focus on competition in the financial system by reviewing "the state of 'competition' in the financial system every three years":

Government should update ASIC’s mandate to include a specific requirement to take competition issues into account as part of its core regulatory role.43 These proposals are in addition to the recommendations in this report addressing sectoral issues in banking, payments and financial markets." Both ASIC and Australian Treasury are members of the Council of Financial Regulators. The abovementioned Financial System Inquiry Final Report sits on the Australian Treasury website. Notwithstanding the need to "Review the state of competition in the sector every three years", seemingly, neither ASIC, nor Australian Treasury, nudged the RBA to re-impose a maximum interest rate on Credit Cards or indeed encouraged Credit Card Issuers to reduce interest rates on their existing Credit Card Products. Below is a quotation from Westpac's submission to the Wallis Inquiry 1996, submitted by the then CEO, Bob Joss, that may have anticipated that after deregulation several Credit Card Issuers would run amuck:7. High annual cost to the State and Territory budgets of providing Financial Counselling Financial Counselling Australia publication dated Jan 2014 reported -

Dept of Families and Social Services reported in March 2019 an agg. of $64.1 million (annually) was expended over the previous financial year on Financial Counselling across Federal, six States and the ACT governments:

This appears to be a 47.7% (($64.1m - $43.38m)/$43.38m) increase in funding of Financial Counsellors over only five years.How much of this annual funding of Financial Counsellors could have been reduced had the Principal Regulator of the Payments System treated the CAUSE rather than condoned the EFFECT?

8. Financial Counsellors evidence first-hand "the worst financial scams and unscrupulous market conduct in the country" (Predatory Advertising) on a daily basis within some web and newspaper advertisements for Credit Card Products that have patently proven very costly for Credit Cardholders with low Financial Literacy Skills

The immediately above embedded thread provides access to a welter of evidence of the distress upon many Australians with low Financial Literacy Capacity incurring huge Credit Card indebtedness not only for the Credit Cardholders, but also for Financial Counsellors. Below are a few extracts from the above title heading:

9. Journalists and consumer groups have been vocal for decades in their criticism of some Credit Card Issuers engaging in Numeracy And Literacy Targeting to the enormous financial detriment of Persistent Revolvers who have paid 80% circa of the cost of the Lines of Credit enjoyed by Transactors, with the remaining 20% circa contributed by Occasional Revolvers Below are extracts from "Ross Greenwood, David Koch and Paul Clitheroe slam banks over ‘unconscionable’ credit card lending" – news.com.au. The three finance journalists were questioned by Economic References Committee chairman, Labor’s Sam Dastyari, and Liberal Sean Edwards, at the Senate Inquiry into credit cards at the Sofitel Wentworth in Sydney on Sept 1, 2015:"FINANCE experts Ross Greenwood, David Koch and Paul Clitheroe don’t always agree — but they’ve just united to slam the banks over ‘unconscionable’ credit card lending.

Below are three extracts from Helping Australians avoid the credit card debt trap - Chapter 5 - 16 Dec 2015: 18 Interest payments made by these consumers help subsidise the rewards programs offered to Transactors, who tend to be wealthier and attracted to high-interest cards that offer redeemable points as prizes for frequent usage". Interest would be 260% of the initial $5,000 indebtedness.

10. References to the Writer's earlier approaches on CDs concerning Australia's Central Bank's failure to observe its Parliamentary Bestowed Mandate to "best contribute to.......... the economic prosperity and welfare of (ALL) the people of Australia" that includes Credit Cardholders, through no fault of their own, possess low Financial Literacy Capacity

The Writer's letter on CDs to 5, 6 and 7 above -a) recommended a very brief second wave of the Royal Commission; and b) provided Thirty-Two Written Questions directed at Financial Services Regulators, and a Royal Commissioner, and my Supporting Evidence that warrant these questions to right the wrongs within the most differentiated product in the entire Western World, because -* 12.58% circa of all Credit Cardholders, identified by the RBA as Persistent Revolvers, invariable with low Financial Literacy Capacity, have paid 80% circa of all Interest and Penalty Fees Revenue; and* five former Prime Ministers have attested that Australia is an egalitarian country, yet it is not. Extensive Supporting Documented Evidence to warrant each of the Thirty-Two Written Questions is accessible by clicking on each Question number. So complex, that if the 2018 Royal Commission into Financial Services had kicked-off by investigating Unconscionable Conduct by many Credit Card Issuers that manifested over the last 20 years, Commissioner Hayne could have expended all of 2018 cleaning up only one banking product, albeit the most prolifically used, such is the breadth and depth of Unconscionable Conduct primarily targeted at Financially Uneducated And Vulnerable Australian Credit Cardholders with Low Financial Literacy Capacity. 11. Postscript The RBA needs to be held to account for the Extreme Financial And Emotional Distress that the Financially Uneducated And Vulnerable Persistent Revolvers, the majority of whom would likely be rusted on Labor voters, have suffered during the last 25+ years. The vast majority received their first Credit Card in their late teens or very early adulthood, with rarely a skerrick of money management understanding, but rather were confronted by Predatory Advertising.Prior to the Campbell Report circa early 1980's, the RBA regulated all Australian bank interest rates with an Iron Fist dating back to the failure of banks in the 19th century - "... when de-regulation resulted in adverse consequences, re-regulation ensued...". Many Credit Card Issuers have engaged in Predatory Advertising charging Usurious Unsecured Personal Loan Interest Rates overtly Targeting Credit Cardholders with Low Financial Literacy Capacity Financially - Uneducated And Vulnerable Australians suffering Extreme Financial And Emotional Distress for over 25 years, whilst 67% of Credit Cardholders, identified by the RBA as Transactors, have enjoyed their Lines of Credit from regularly using their Credit Cards at virtually no cost, even though the RBA has previously written that the User Pays Principle should apply to Credit Card Products. Inaction by APRA and ASIC was attributed to some scandals exposed in the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry. ABCNews Business Editor, Ian Verrender, article (26 Nov 2018) Is it time for corporate watchdog ASIC to be put down? includes "It is this cosy relationship that forms the nub of the problem".Yet far more consequentially, Australia's Principal Regulator of the Payments System has been complicit with Credit Card Issuers that engaged in Predatory Advertising even though the Commonwealth Govt had enacted legislation for the Principal Regulator of the Payments System to act upon Unconscionable Conduct from Predatory Marketing, in particular concealed interest penalties in 9 font Arial dark grey in 98 pages T&Cs, of some Credit Cards. Post the 2018 Royal Commission, "ASIC and APRA, in addition to the Royal Commission recommendations addressed to them specifically, are now working with the Federal Government to assist the development of legislative reform":

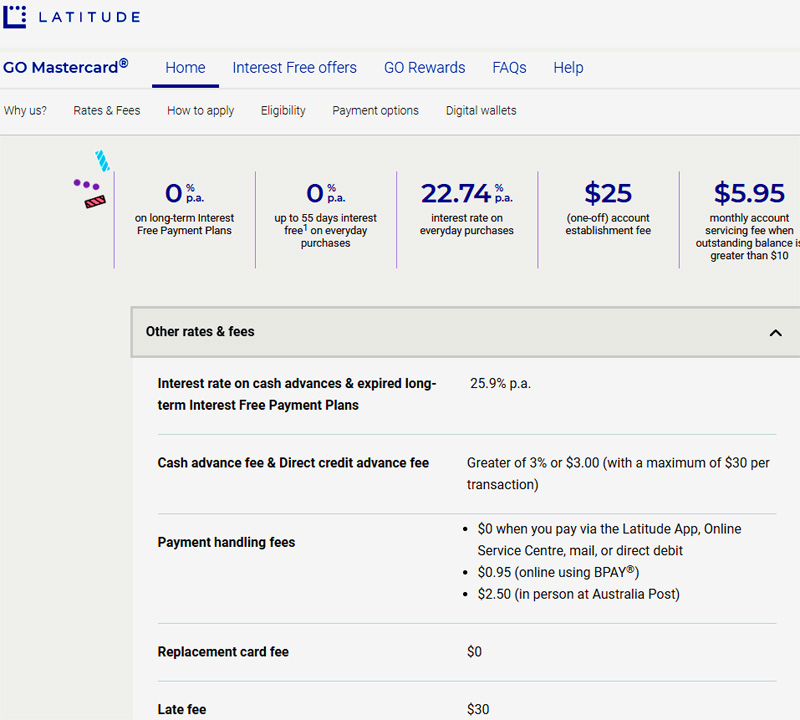

12. Summary - The central issue In April 1985 the 18% interest rate Cap on Credit Cards was removed when the Overnight Cash Rate was 17.2% circa - spread was less than 1%. Less than two years ago the spread between the Overnight Cash Rate of 0.10% and the highest Cash Advance interest rate. (Latitude Financial's Go Mastercard) was over 28%. Latitude Financial's Go MasterCard had a Cash Advance interest rate of 29.49% until March 2019. Presently it is 25.9%, but now incorporates a Cash Advance Fee of $3 or 3% of the cash advance, whichever is greater = 28.9%. It charges an explicit 'Late fee' of $35. $8.95 monthly account service fee when outstanding balance is greater than $10. Little wonder that Credit Cardholders with low Financial Literacy get lured into applying for a Latitude Financial GO Mastercard because of deceptively offering 'Enjoy now. Pay later. Interest Free'. Persistent Revolvers invariably with low Financial Literacy that account for a mere 12.58% circa of Credit Cardholders have contributed a whopping 80% circa of that $6.3 billion (asserted by Alan Kirkland of CHOICE in June 2022) in Interest And Penalty Fees Revenue due primarily to Credit Card Issuers not passing on falls in the Overnight Cash Rate. The remaining 20% of that $6.3 billion was paid by other Occasional Revolvers that account for 20.42% circa of all Credit Cardholders. The remaining 67% circa of all Credit Cardholders, described by the RBA as Transactors, contributed zilch of that $6.3 billion of Interest And Penalty Fees Revenue. Hardly, an example of the User Pays Principle that "RBA's Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001 advocated it apply to Credit Card Products "....consistent with the approach adopted by Australian financial institutions in pricing other payment instruments under their control." But its Board never adopted its own policy document.

Since the early 1990s hundreds of thousands of Credit Cardholders too often with low Financial Literacy Capacity generally through no fault of their own, the majority likely 'rusted on' Labor voters, have paid over $20,000 each in Interest and Penalty Fees on Credit Card Products because the Reserve Bank Board overlooked Credit Card Issuers explicitly Targeting Credit Cardholders With Low Financial Literacy Capacity, Predatory Advertising that Federal Parliament had entrusted it (back in 1959 under Nugget Coombs) to inter alia "....best contribute to.......... the economic prosperity and welfare of (ALL) the people of Australia".

"RBA Governor Philip Lowe says it’s ‘still plausible’ first rate rise won’t be before 2024" - Nov 16, 2021 address to Australian Business Economists. On 16 Nov 2021 the Cash Rate was 0.10%. RBA increased it to 2.35% on 6 Sept '22 even though the primary cause for recent inflation has been energy, fuel and food cost increases, primarily imported costs due to impacts of the Ukraine War - referred to as a 'supply shock'. These 'supply prices' have increased due to external impacts. Alas, the RBA increasing interest rates to reduce current inflation (caused by these external price increases) will also increase unemployment, thereby accentuating the adverse effects of the 'supply shock'. Whereas previous recent bouts of high inflation in Australia in the early '70s, late '80s and in 2000 were generally 'demand driven' due to wages growth, referred to as 'demand shock'. So the RBA increasing interest rates to reduce the available money supply was a logical treatment for those earlier instances.

‘They have to be held to account’: Future Fund chairman lashes RBA over rate rises.

Yours sincerely Philip J. Johnston ==================================

|

|

|

|

{kind=link}

{kind=link}

{kind=link}