Persistent Revolvers (discussed in Chapter 5 and Chapter 20) generally Lack Financial Acumen and possess low Financial Literacy Capacity *** -

(i) in 2017 paid a 17.22% interest rate (average based on ASIC Money Smart) on 100% of their Credit Card Debt on an average of 5½ Credit Cards per Persistent Revolver (up to 20 Credit Cards could be held by a single Persistent Revolver) - refer Chapter 7, occasionally on aggregate Total Amount Owing that exceeds $100,000 according to anecdotal evidence from 'Credit Card Distress' Authorities in Quotes from reputable Credit Card Distress Authorities about unconscionable advertising;

(ii) forfeit their Interest Free Period;

(iii) pay Late Payment Fees and may also pay Over-the-Limit Fees;

(iv) experience Extreme Financial And Emotional Distress;

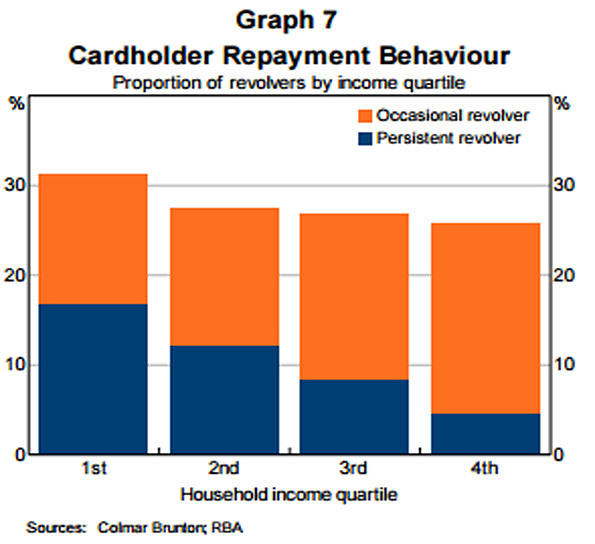

(v) account for 38.13% circa of all Revolvers (Graph 7 below and table thereunder);

(vi) account for 12.58% circa of Credit Cardholders (Revolvers = 33% of Credit Cardholders. Persistent Revolvers = 38.13% circa of Revolvers. 38.13% of 33% = 12.58% circa)

(vii) pay 80% circa of all Interest and Penalty Fees Revenue generated from Credit Card Products which amounted to a whopping $14.56 billion in Credit Card interest last financial year, whilst 67% of Credit Cardholders described by the RBA as Transactors, paid no interest costs for the Line/s of Credit that the benefited from,

(viii) hold 5,201,380 Credit Cards circa of the 16.699 million current Credit Cards in Australia;

(ix) paid in the previous year $5,471,110,000 in agg. Credit Card interest annually on 5,201,380 Credit Cards owned by Persistent Revolvers

(x) pay on ave. $5,159.80 circa of interest and penalty fees annually;

(xi) account for 12.58% circa of the 7,515,000 Credit Cardholders, namely 945,000 [cell b36] Credit Cardholders (ASIC 'Credit card debt clock' 27-Apr-17) that pay a whopping 80% circa of Interest And Penalty Fees Revenue levied by Credit Card Issuers annually; and

(xii) "13 per cent of people pay only the minimum repayment off their account each month. Australians have a collective credit card debt of almost $1,500 for every man, woman and child" infochoice May 2017.

*** The above information is drawn from calculations in Excel file 'Credit Card Statistics' based on -

(a) the below Commonwealth Treasury and RBA quotations that Revolvers account for 33% circa of Credit Cardholders;

(b) anecdotal evidence from 'Credit Card Distress' Authorities, in particular Financial Counsellors, regarding the magnitude of Credit Card Debt Accruing Interest (and the number of Credit Cards owned) held by many of the Credit Cardholders that seek their counsel; and

(c) the below RBA Graph 7 and table thereunder.

The term, Persistent Revolvers, was identified by the Reserve Bank in its Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - Aug 2015 - Submission 20. It appears in the below Graph 7 titled "Cardholder Payment Behaviour" on page 6. The explanation of (v) to (xii) [listed above] is set out below.

Four Types of Revolvers informs that not all Persistent Revolvers are on low incomes with poor Financial Literacy Capacity.

|

|

|

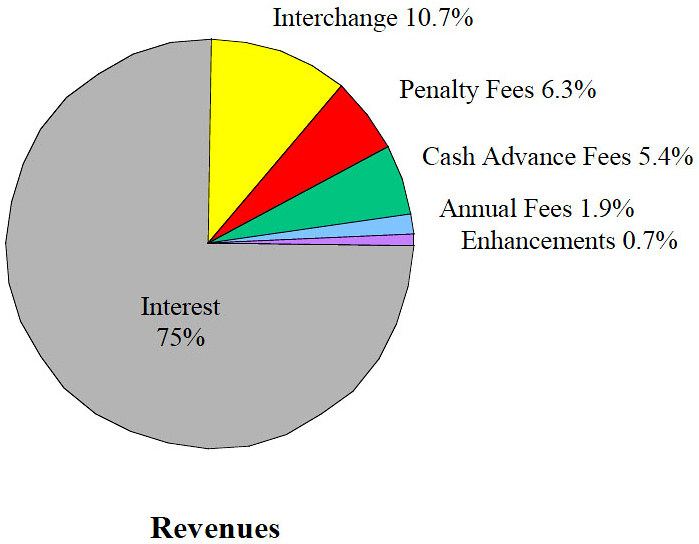

The above 'pie chart' (on RHS) appears in a journal report titled "Who Pays for Credit Cards?"

(presented by the Federal Reserve Bank of Chicago dated 2001). It displays a break-up of Card Issuers' Revenues for the aggregate of Visa, MasterCard and Discover cards in the USA. It shows that net U.S. Interest Revenues of 75% and associated Penalty Fees Revenue (Late Payment Fees and Overlimit Fees) of 6.3% and Cash Advance Fees of 5.4% aggregate to 86.7% of U.S. Card Issuers' Annual Revenue. Interchange Fees charged to the Merchant are only 10.7%.Chapter 2 - "Overview of the Australian credit card market" notes:

2.16 The RBA advised that the proportion of revolvers is higher among low-income households and when high-income households do fall into the revolver category, they are more likely to be 'occasional revolvers' as opposed to 'persistent revolvers'.[18]

McKinsey Report - May 2014 categorizes 'Five Segments' of Credit Cardholders in the USA. Below is an extract from the 'Third Segment', namely 'Financially stressed':

"Carry heavy credit card debt—nearly four times the average, at USD$7,453.

|

Below are two an extracts from RBA Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - Aug 2015:

Revolvers (Occasional Revolvers + Persistent Revolvers) account for 33% circa of Credit Cardholders based on -

Casual empiricism of the above (Graph 7) as calculated in the immediately above table suggests that - * almost two thirds of Revolvers, referred to by the RBA as Occasional Revolvers, pay interest occasionally. * over one third of Revolvers, referred to by the RBA as Persistent Revolvers, pay a 17.22% Interest Rate (average) on 100% of their Credit Card Debt. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

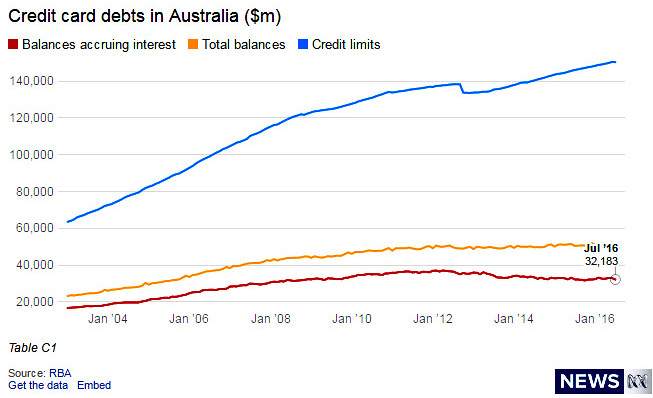

Revolvers represent 33% of Credit Cardholders transactions. Revolvers carried $32.183 billion (see above graph as at July '16) of interest accruing Credit Card debt at an average per Credit Card debt of $6,095 paying interest @ an ave. 17% p.a. = $1,036 pa. interest on average per Credit Card used. This $1,036.20 pa. circa takes no account of Late Payment Fees.

|

Table 'A' |

||

| Agg Credit Card debt - July '16 | $32,183,000,000 | |

| Total number of Credit Cards | $16,000,000 | |

| Revolvers |

33% |

$5,280,000.00 |

| Ave debt per Card per Revolver | $6,095.27 | |

| Ave. interest rate |

17% |

|

| Ave. interest per Card per Revolver | $1,036.20 | |

|

Table 'B' |

||

| Total Revolvers | 33% | of all Credit Cards |

| Persistent Revolvers | 38% | of all Revolvers |

| Total Persistent Revolvers | 12.58% | of all Credit Cards |

| Total Persistent Revolvers hold |

2,006,400 |

Credit Cards |

The immediate above 'Table B' evidences that 12.58% of Credit Cards are held by Persistent Revolvers (Revolvers = 33% of Credit Cardholders. Persistent Revolvers = 38% of Revolvers. 38% of 33% = 12.58%)

InfoChoice.com.au notes in

'Low income families are spending on credit cards':

"13 per cent of people pay only the minimum repayment off their account each month. Australians have a collective credit card debt of almost $1500 for every man, woman and child"

"Regulatory tricks, to their credit, in our interest" - SMH, Clancy Yeates - Jan 6, 2014 includes:

"According to an ANZ survey quoted by the academics, 13 per cent of people pay only the minimum repayment."

Australia's nomenclature for

USA McKinsey's 'Financially stressed' Credit Cardholders is Persistent Revolvers that "Carry heavy credit card debt—nearly four times the average with unpaid debt.

Occasional Revolvers therefore contribute approx one fifth (20% circa) of Interest and Penalty Fees Revenue.

The above Australian calc of AUD$6,095 average debt is per Credit Card held of the 5,280,000 (33% of all Credit Cards) held by Revolvers of the 16.09 million Credit Cards owned by Australians. The above ave of USD$7,453 from the McKinsey Report represents agg. debt per Credit Cardholder amongst the 'Financially stressed'.

67% circa of all Credit Cardholders, being Transactors, enjoy a Free Ride. Those Free Riders' Revolving Lines of Credit are paid for by 33% circa of Credit Cardholders that are Revolvers of which 38% of Revolvers are Persistent Revolvers that -

* hold 12.58% circa of the 16.1 million Credit Cards in Australia; and

* pay 80% circa of Interest and Penalty Fees Revenue - displayed in Figure 3 and Figure 1 above and also in Chapter 8.

The Pareto Principle, colloquially known as the '80-20 Rule', is that 20% of customers generate 80% of the revenue for a particular business. The Pareto Principle has been 'blown away' by Credit Card Issuers because 12.58% of Credit Cardholders (not 20%), namely Australia's Persistent Revolvers (referred to by McKinsey in the USA as 'Financially stressed'), identified in the above RBA Graph 7 "Cardholder Payment Behaviour" (in RBA report RBA Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - Aug 2015), pay 80% of Interest and Penalty Fees Revenue.

Mindful that the highest -

* Purchase interest rate is 25.9% from "

Lombard Visa Card Classic; and* Cash Advance interest rate is 29.49% from G.E. Money's "Go MasterCard",

one ponders whether LOAN RATE STICKINESS: THEORY AND EVIDENCE - June 1992 is still a concern of the Reserve Bank, but it was in 1992 - at least to the two authors:"

The RBA would likely retort that it de-regulated loan and deposit interest rates from 1980 following the recommendations in the Campbell Committee Report. Chapter 17 below notes:

"The Campbell Committee was established in 1979 and reported in 1981. The recommendations of the inquiry were targeted at ..... the abolition of direct interest rate and portfolio controls on financial institutions. Campbell did not recommend removal of any powers held by the Reserve Bank to regulate interest rates or demand financial information. The Campbell recommendations were made following an extended period of high interest rates. High deposit interest rates by NBFIs existent circa 1980 are no longer an impediment to regulating credit card interest rates. The abovementioned reference to Chapter Nine (in Chapter 15 above): 'Stability and Payments' of the Wallis Enquiry noted "the RBA should retain overall responsibility for the stability of the financial system, the provision of emergency liquidity assistance and for regulating the payments system." .."The ACCC and the PSB should monitor the delivery fees charged on credit and debit cards while the ACCC should monitor the rules of international credit card associations to ensure they are not overly restrictive."

Below is an extract from Consumer Affairs Victoria - Regulating the cost of credit which evidences that in the past if de-regulation did not achieve the desired results, then re-regulation followed. But not with regard to re-introducing a max interest rate cap on Credit Card, notwithstanding that the spread between the current Cash Rate of 1.5% and the Credit Card Purchase Interest Rate of 20% is 18.5%. (As at April 2017, the highest Purchase interest rate is 25.9% from "Lombard Visa Card Classic" and the highest Cash Advance interest rate is 29.49% from G.E. Money's "Go Mastercard"):

"The tide of utilitarianism rose slowly, and a lengthy campaign was necessary before the financial deregulation of 1854, which abolished the British interest rate cap. However, one act of deregulation cannot quell an argument that has been going on for millennia. Over the following century the tide gradually turned towards re-regulation, culminating with detailed requirements imposed on the financial sector (particularly the banks) during and immediately after the Second World War. We now trace the gradual lead-up to this second phase of regulation."

The Productivity Commission's Staff Working Paper found that:

"Nearly half of the population were assessed at either levels 1 (the lowest level) or 2, both of which are below the minimum level deemed necessary to participate in a knowledge-based economy (level 3)."

An analysis of Numeracy and Literacy Skills of Australians is contained in Chapter 1.

Of the Four Types of Revolvers, the initial two types would be candidates to be Eligible Persistent Revolver Plaintiffs. It would be necessary to 'Test/Measure' potential Eligible Persistent Revolver Plaintiffs rigorously to ensure that each met the requirements in (2.) d) of Eligible Persistent Revolver Plaintiffs.

The Commonwealth Treasury noted in 2010 in its submission to National Credit Reform: Enhancing Confidence and Fairness in Australia’s Credit Law that

the Standing Committee on Economics found that ‘there was anecdotal evidence that in some cases at least the impost of high default fees is marginalising people who are already struggling to feel they belong in society.’22Below are extracts from

Smart cards. Dumb card holders? - 12th March 2014 - by Alan Thornhill:"ASIC says over half a million Australians carry more than $5,000 in credit card debt.

Yet, ASIC says, many of those card holders are middle income earners, managers and people with a degree.

It said research by Roy Morgan shows 22 per cent of Australians over the age of 18 earn more than $70,000 per year, and these people make up 42 per cent of those who carry credit card debt over $5,000.

In addition, the 12 per cent of the population are managers and managers make up 26 per cent of those with debt above $5,000.

And, while 42 per cent of Australians have a degree or diploma they represent 49 per cent of those carrying $5,000 or more in credit card debt.

“People might be excellent managers in the workplace, but they aren’t necessarily managing their finances in the best way possible.’

Around 2 million Australians do not pay off their personal credit card debt in full each month, rising from 24 per cent of personal credit card holders in 2009 to 27 per cent of personal credit card holders in 2013.

“Australians have over $34 billion owing on credit cards where interest is being charged and pay $6.2 billion a year in interest."

Below are extracts from

High incomes run up relatively less debt on major cards - Roy Morgan - Dec 12, 2016:"In the 12 months to October 2016, holders of major cards (VISA, MASTERCARD, AMEX) intended to carry forward to their next statement an average monthly debt of $19 billion between them. The main contributors to this were the lower-income card holders, who on average owed an amount equivalent to a much higher proportion of their incomes than the higher-income groups. These are the latest findings from Roy Morgan’s Single Source survey of over 50,000 consumers pa which includes detailed coverage of over 39,000 with major cards.

The proportion of cardholders who carry nothing or very little forward to their next statement increases with income."

See: