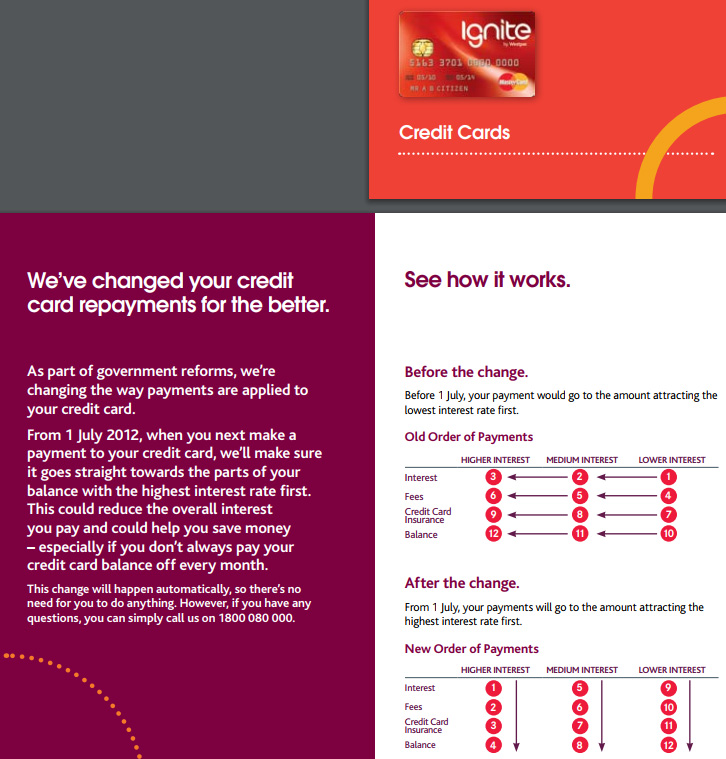

'Order of Payments' Allocation Practice eventually outlawed by the Reserve Bank

Chapter 7 of Grounds/Reasons for

the

13 Written Question is titled

|

Extracts that evidence that Financial Counsellors are familiar with Unconscionable advertisements and Predatory Lending that tempt many Revolvers with Low Financial Literacy Capacity into horrendous Credit Card Debt Accruing Interest

1s t extract:Financial Counselling Australia website notes: "Total funding from governments in Australia for financial counselling service delivery is $43 million per annum." of which 50% of assistance is to financially stricken Australians that earn less than $20,000 pa.

|

|

2nd extract: |

|

3rd extract:

|

|

4th extract: Ms Katherine Temple, a policy officer with the Consumer Action Law Centre in Melbourne, provided the Senate Economics References Committee with some insight into its work with people struggling with Credit Card Debt Accruing Interest, and by extension the scale and severity of the problem in the community: 85 " "..can lead to and exacerbate the marginalisation of struggling consumers. It can result in significant financial hardship and, in some cases, bankruptcy and the loss of the family home. At an acute level, credit card debt can lead to family violence, breakdown and a deterioration in health, including mental health. It can also have a long-term impact on the capacity to provide for health, retirement and education. These are serious and profound impacts. Taking appropriate steps, including regulation, should be an absolute priority for policymakers."[86] |

|

5th extract: |

|

6th extract:

|

|

7th extract:

SMH article "Middle class hit by debt"

notes that

Tony Devlin, a senior

Financial Counsellor at

Salvation Army's

"Moneycare" service, has

interviewed hundreds of level 1 and level 2 Australians who have incurred huge

debts on multiple credit cards.

"There are far more middle-income earners seeking a way out of the desperate

cycle of huge mortgage repayments and mounting credit card debt.........And

people try to keep the ship afloat by using more credit cards."

The Writer

spoke to Tony Devlin on Wed 7 Dec '11. Tony told

him

|

|

8 th extract:

"We had a client recently who owed $450,000 and was on a salary of $40,000. She had ten credit cards and was using one to pay off the other. By the time she came to us she was almost suicidal." "Lives can be destroyed by credit card debt, more couples break up over financial stress than infidelity," Ms Southon says. |

Financial Counselling Australia produced a booklet in 2015 titled Standards for agencies employing financial counsellors to establish standards that -

A. assist agencies (charities/not-for-profits/community organisations) that offer financial counselling services to provide a high quality of service; and

B. set out the essential requirements an agency should meet if it wishes to offer financial counselling services.

Below are extracts from the above FCA booklet which relate to Financial Counsellors maintaining records whereby useful data/information can be provided back to their 'funders':

1. Financial counsellors also work to prevent financial difficulty through community education and by providing input to government and industry policy development processes.

2. The agency keeps complete and legible records in relation to each matter where it provides financial counselling services.

3. The agency submits reports to its funders in the required format and within the required time frames.

4. The agency collects and analyses data concerning:

(a) Demographic information about the clients who use the service.

(b) Systemic issues that are identified in the course of service delivery.

5. The agency participates in evaluation concerning the effectiveness of its financial counselling services.

Financial Counsellors have evidenced first-hand the "the worst financial scams and unscrupulous market conduct in the country" on a daily basis in web and newspaper advertisements for Credit Card Products.

A shocker of misrepresentation and deceit was that some Credit Card Issuers were offering a Zero Balance Transfer (for say one or two years) and then -

i) applying monthly repayments of Purchases to reduce the Zero Balance Transfer amount; and

ii) charging 20% circa on those Purchases from date of each Purchase and in some cases, withdrawing the Interest free Period for one or two months.

National Consumer Credit Protection Amendment (Home Loans and Credit Cards) Act 2011 Unconscionable Conduct Credit Card Issuers are -

A. no longer able to apply the 'Order of Payments' provision; and

The Federal Dept. of Social Services provides a division called "Commonwealth Financial Counselling services that funds financial counselling that are provided by community and local government organisations to help people in personal financial difficulty to address their financial problems, managing the debt and make informed choices about their money in the future".

In order to better understand the social and fiscal costs of the Credit Card Product, Commonwealth Financial Counselling services and the State governments (that collectively fund $43 million annual for Financial Counselling at Australia's major charities/agencies) should obtain from the 10 largest charities/agencies that provide Financial Counselling -

(A.) descriptions of misleading, deceptive or unconscionable web and newspaper Credit Card advertisements (Predatory Advertising) and pass those advertisements onto Australia' Three Financial Regulators that should ensure that offending Credit Card Issuers are prosecuted, with ASIC (or another) imposing hefty monetary fines and public exposing the practice; and

(B.) numeric data of the number and demography of Credit Cardholders seen by Financial Counsellors that carry Credit Card Debt Accruing Interest >$10,000 >$25,000 >$50,000 and >$100,000 and the number of different credit cards held by each distressed Credit Cardholder in those debt categories.

As a start, the Federal Treasurer should request the relevant Regulator to -

(i) examine the information in advertisements for Credit Cards (explained in the Nine Examples in Labyrinth of ‘Concealed Spiders - referred to in Chapter 3 above) with particular regard to any breaches of the National Consumer Credit Protection Amendment (Home Loans and Credit Cards) Act 2011 'et al'; and

(ii) for ASIC to impose monetary penalties where Unconscionable Conduct is found to exist (based in the ACCC's description of (Unconscionable Conduct).