|

|

Thirty Two Questions and Supporting Evidence Submission Letter to Royal Commission April-2018 Defined Terms & Documents

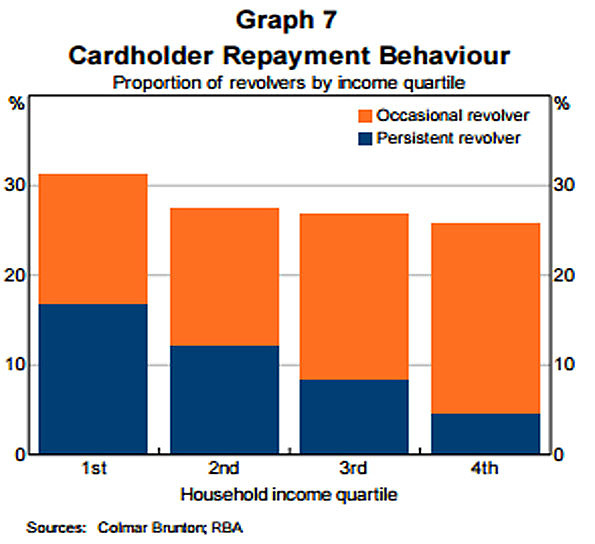

1st Question Will the Royal Commission delve where - * the Reserve Bank, the principal regulator of the Payments System through the PSB, that has 'extensive powers' to gather information from a payment system or from individual participants; and * no other member of the Council of Financial Regulators, have not been prepared "to go there"; namely the RBA has not requested data to empirically quantify the financial burden falling upon the minority of Credit Cardholders, described by the RBA as Revolvers, that possess poor Financial Literacy Capacity often paying Usurious Interest Rates, ostensibly due to Predatory Marketing Practices, and until recently also endured Unconscionable Credit Card Interest Charging (as defined by the ACCC)? Specifically, will the Royal Commission obtain financial data from the primary six Credit Card Issuers (Four Pillars, Citibank and Latitude Financial nee G.E. Capital), in order to determine if the Writer's below calculations (detailed in Chapter 5) based on the RBA's 'Landmark' third publication Submission 20 to the Senate Inquiry into Matters Relating to Credit Card Interest Rates dated Aug 2015 are correct? (A) Revolvers - 33% approx of all Credit Cardholders pay over 95% of all Interest And Penalty Fees Revenue annually. (B) Persistent Revolvers - 12.58% circa of the 7,515,000 Credit Cardholders (June 2016), namely 945,000 [cell b36] Credit Cardholders pay 80% circa of all Interest And Penalty Fees Revenue. (C) Transactors - 67% approx of all Credit Cardholders - * enjoy the convenience of their Revolving Line/s of Credit (often not paying for Purchases for up to 55 days after receipt of goods and services); and * often receive Rewards Programs, without materially contributing to Credit Card Issuers' operating costs and profits which are primarily generated by Interest And Penalty Fees Revenue paid by Revolvers, of which Persistent Revolvers account for 38.13% circa of all Revolvers (Graph 7 and table thereunder).

================================================= Supporting Documented Evidence re 1st Question The Reserve Bank has never requested financial data from the primary six or seven Credit Card Issuers as sought in Question 1, notwithstanding that - to meet the complex demands of everyday life and work in the emerging knowledge-based economy".ASIC 2010 report notes "These findings have implications for our regulatory regime, which relies upon disclosure as a critical element of our consumer protection system. " St. George and Westpac test Credit Cardholders, even those possessing Level 5 Numeracy and Literacy Skills, by expecting all their Credit Cardholders to read/comprehend voluminous Conditions of Use printed in a tiny font; 2. Federal and State Govt's allocated $43.38 million in 2014 to 44 Australian charities to provide 500 circa financial counsellors to Australians, over the subsequent year, that are experiencing Extreme Financial And Emotional Distress. The vast majority of those counselled are Credit Cardholders with poor Financial Literacy Capacity (Chapter 7); 3. Credit Card Products are the most differentiated product (in both 'types' and 'providers') in the entire Western World because the 'money lenders' in the 21st Century, as likely around the 30th year in the 1st Century, focus on one or more promoted benefits, but often misrepresent the material hidden cost/s to possibly procure that benefit/s, where losers result; 4. The majority of Credit Card Issuers in Australia have engaged in Predatory Marketing Practices, and until recently Unconscionable Credit Card Interest Charging, targeted at Credit Cardholders with poor Financial Literacy Capacity which falls within the ACCC definition of Unconscionable Conduct; 5. Submission 20 to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - Aug 2015 (Reference A listed at top of this page - 3rd Publication) evidenced the RBA introduce a new nomenclature, Persistent Revolvers, in Aug 2015 to describe Credit Cardholders that were hopelessly in debt: * Graph 7 titled ''Cardholder Payment Behaviour" quantified the magnitude of the gross interest burden falling upon Persistent Revolvers that often possess low Financial Literacy Capacity that are often Financially Uneducated And Vulnerable Australians and have paid Usurious Interest Rates. The Writer calculates that Persistent Revolvers accounted for 12.58% circa of the 7,515,000 Credit Cardholders (June 2016), namely 945,000 [cell b36] Credit Cardholders (ASIC 'Credit card debt clock' 27-Apr-17) paid an Unconscionable 80% circa of Interest And Penalty Fees Revenue levied by Credit Card Issuers; and * Noted that "..... In addition, many credit card holders take advantage of interest-free periods such that they do not pay interest on their card balances " identified by the RBA as Transactors. 6. Extensive Powers and Responsibilities of the RBA notes - * (in Section 2 therein) Part 5—Miscellaneous, Section 26 'Persons to give Reserve Bank information' of the Payment Systems (Regulation) Act 1998 gives the Reserve Bank 'extensive powers' to gather information from a payment system or from individual participants. "The Payments System Board was established by the Commonwealth Govt. in 1998 so as to best contribute to: .......... and promoting competition in the market for payment services." Red Book 2011 "Payment, clearing and settlement systems in Australia - 2011" notes: "The Payment Systems (Regulation) Act 1998 also gives the RBA extensive powers "....to gather information from payment system participants and operators." * (in Section 3 therein) that - * the Reserve Bank has significantly greater powers/responsibilities to "...the economic prosperity and welfare of the people of Australia", than the Bank of England or the U.S. Federal Reserve has to the economic prosperity and welfare of the U.K. and U.S. citizens respectively. * "the PSB has been given the backing of strong regulatory powers, unique among central banks" * (2) It is the duty of the Reserve Bank Board, within the limits of its powers, to ensure that the monetary and banking policy of the Bank is directed to the greatest advantage of the people of Australia and that the powers of the Bank under this Act and any other Act, other than the Payment Systems (Regulation) Act 1998, the Payment Systems and Netting Act 1998 and Part 7.3 of the Corporations Act 2001, are exercised in such a manner as, in the opinion of the Reserve Bank Board, will best contribute to: (a) the stability of the currency of Australia; (b) the maintenance of full employment in Australia; and (c) the economic prosperity and welfare of the people of Australia. 2nd paragraph in Chapter 9 and Attachment D notes that Part 5—Miscellaneous, Section 26 'Persons to give Reserve Bank information' of the Payment Systems (Regulation) Act 1998 gives the Reserve Bank 'extensive powers' to gather information from a payment system or from individual participants provides further explanation of the RBA's authority to seek any financial information that it wants to from any/all Credit Card Issuers. Dr. Malcolm Edey, the then Assistant Governor (Financial System) in a Speech at the Cards & Payments Conference on 21 May 2015 noted: * RBA's key areas of focus included capacity for richer information with payments. * "On current scheduling the New Payments Platform will deliver a fast payments service with rich information and addressing capabilities in the second half of 2017. Where is the rich information regarding the financial burden that fall upon Revolvers, in particular Persistent Revolvers? 7. The Reserve Bank and its then predecessor, the Govt. owned Commonwealth Bank, had increasingly regulated 'with an iron fist in a velvet glove' the commercial banks since 1911. Historically when de-regulation resulted in adverse consequences, re-regulation by Australia's 'central bank' ensued.The Unpleasant Truth About Australian Banking notes: "Before 1981, activities of major Australian banks, including the manner they dealt with customers, were subject to detailed regulations imposed by the Federal Government. Following the 1981 Campbell Committee Report, banking regulations were significantly reduced." 8. "Prior to 1985 the maximum rate that could be charged on credit cards had been set at 18% pa by the Reserve Bank of Australia. In April 1985, this rate was deregulated." - see bottom of page 7 of a University of Wollongong paper dated January 2012; 9. On 25 Oct 2011, the Writer spoke to Ms. Sharon van Etten by 'phone at RBAInfo and then emailed her 'Subject: Seeking data on the percentage of credit card users who repay their outstanding indebtedness in a particular month, and a break-up of those who do not'. Ms van Etten responded on Thurs, 10 Nov 2011 by providing useful summary information from Strategic Review of Innovation in the Payments System: Results of the Reserve Bank of Australia’s 2010 Consumer Payments Use Study - June 2011.

10. In order to test the Writer's calculations listed at (A), (B) and (C) in this 1st Question, it would be necessary for the Royal Commission to request Australia's largest six or seven Credit Card Issuers, that included Citibank and Latitude Financial, to provide Credit Card data over at least 12 months that lists the - * 16 digit account number for each of the Credit Card Issuers' Credit Card Products; * Outstanding Indebtedness the day after the Payment Due Date each month * the Interest Rate Charged and the Interest Amount Charged each month * the postcode of the Credit Cardholder; and * Credit Cardholder Fees each month, excluding the Annual Cardholder Fee, to enable an .I.T. Coder to write a programme to calc the agg. Interest And Penalty Fees Revenue for the Four Types of Revolvers which included those Persistent Revolvers on low income with poor Financial Literacy Capacity.

11. Below is and extract from page 2 of ASIC's "Check Against Delivery" dated 6 March 2018 for the Productivity Commission Inquiry into competition in the Australian financial system: Hearings on draft report:

12. Below is an extract from TREASURY SUBMISSION TO THE SENATE ECONOMICS REFERENCES COMMITTEE INQUIRY INTO MATTERS RELATING TO CREDIT CARD INTEREST RATES - 11 Aug 2015:

Data from the household, income and labour dynamics survey in Australia (HILDA), the household expenditure survey and the survey of housing and income shows households in the lowest income quintile have more credit card debt relative to their incomes and pay more in credit card interest relative to their incomes than higher income households, though overall differences in interest payments between quintiles are small (Figure 1).1 These surveys also show households in the bottom two quintiles by net worth also pay the most in credit card interest relative to their income (Figure 2). |

|

|

|

{kind=link}