|

Thirty-Two Written Questions and

Supporting

Documented Evidence (as at 10 Feb '19)

Directed to a Financial Services Regulator or a Royal Commissioner |

|

CLICK ON BELOW

QUESTION

NUMBERS |

Question

Recipient |

Issue/Problem/Negligence/Predatory/Discrimination/Deceit/Unconscionable

'et al' |

Click

on Number of Supporting

Evidence

Documents |

|

|

1st |

Royal

Commissioner |

Will the Royal Commission request financial data from the primary six

Credit Card Issuers

(Four Pillars,

Citibank and

Latitude Financial

nee G.E. Capital)

that identifies the contributors of

Interest And Penalty Fees Revenue

to test the

Writer's

calculation that

Persistent Revolvers account for

12.58%

circa of 7,515,000 Credit Cardholders

- June 2016), yet contribute 80% circa of all

Interest And Penalty Fees Revenue? |

12 |

|

|

2nd |

Governor of the Reserve Bank |

Why

did the

Reserve Bank published

LOAN RATE STICKINESS: THEORY AND EVIDENCE in June 1992

and never act upon its 'sticky' findings re the plummeting

Overnight Cash Rate, in particular of the need to

determine a new

Standard to re-regulate

a maximum interest rate for -

* each Credit Card

Purchase; and

*

each Credit Card

Cash Advance,

as the

Writer recommended in

Section 8

of his

Submission to the RBA dated 25 Oct 2011? |

12 |

|

|

3rd |

Governor of the Reserve Bank |

What

did the

Reserve Bank hope to achieve from publishing

Reform of Credit Card Schemes in Aust: "A Consultation Document"

in March 2001?

Why hasn't

the

RBA over the subsequent 17 years informed the Commonwealth government, as

obligated under

Reserve Bank Act 1959 - Section 11, 'Differences

of opinion with Government on questions of policy' of the

need to

determine in the

Public Interest new

Standards

to apply the

User Pays Principle

to the

Retail Supply Side

of

Credit Card Products?

|

3 |

|

|

4th |

Governor of the Reserve Bank |

Will the

Reserve Bank set a new

Standard, pursuant to

Division 4 Section 18,

to replace

the debt 'lure' of an

Interest Free Period

with

a

-

*

Concessional Interest Rate Period;

and

*

Purchase Usage Fee,

for each

Purchase

with a

Credit Card,

so that each user pays

for the benefits of their

Revolving Line/s of Credit?

Because the

Merchant is funded within 24 hours by the

Credit Card Issuer, but the

Cardholder does not pay for

each

Purchase

or

Cash Advance

for up to 55 days later?

|

2 |

|

|

5th |

Governor of the Reserve Bank |

Does the Governor of the

Reserve Bank agree with the former Assistant Commissioner, Dr. Malcolm Edey's,

below response to a question from the Acting Chair of the

Senate Economics Legislation Committee

on 1 June 2015?

"... we do not have an interest rate regulator in

Australia...............

What we do have is

an ACCC that can investigate uncompetitive conduct if they see it, but they

clearly have not seen it in this market."

|

3 |

|

|

6th |

Governor of the Reserve Bank |

Does the Governor of the

Reserve Bank

concur with the

1st paragraph on page 3 of

Senate 'Economics Reference Committee' summary report titled

Interest

rates and informed choice in the Australian credit card market dated

Dec. 2015 which justified Dr. Edey's

response (listed in

Question

5) which asserted that the ACCC is responsible to monitor and

regulate credit card interest rates, even after the

RBA had

Designated,

established an

Access Regime and

Determined a Standard/s? |

3 |

|

|

7th |

Governor of the Reserve Bank |

Does the Governor of the

Reserve Bank

agree with Dr. Malcolm Edey's

below responses to the

Senate 'Economics Reference Committee'

on 1 June 2015 because it is contrary to the findings in

LOAN RATE STICKINESS: THEORY AND EVIDENCE in June 1992

and empirical evidence in the USA, the UK and Australia over the

subsequent 26 years?

"Yes, the

financial system works through competition. The

basic wholesale interest rate is the cash rate,

which we set, and then competitive forces will

cause other interest rates to move up and down

with the cash rate. That is the way the effect

of policy is transmitted to the wider economy."

|

5 |

|

|

8th |

Governor of the Reserve Bank |

Is

the Governor

of the

Reserve Bank

in

possession of empirical evidence that supports Dr. Malcolm Edey's

contention (in Dr. Edey's responses to the Acting Chair of the

Senate 'Economics Reference Committee'

on 1 June 2017)

that a viable opportunity exists for

Credit Cardholders that have

managed to 'chalk up' considerable debit, often across several

Credit Cards, to

consolidate those debts in a zero or introductory low interest rate

Credit Card to

".... pay off their loans more

quickly"?

Because

Credit Card Issuers

that offer

Balance Transfer Interest-Free Period Offers

are not Benevolent Bankers, they seek to poach profitable

Credit Cardholders from other

Issuers

evident in

Balance Transfer Offers.

|

4 |

|

|

9th |

Chair

of

APRA

|

APRA

Chairman

responded to

a Senator Hearing in Canberra on 3 June 2017

"....the margins on credit card business look very high , certainly

to any other form of credit, and certainly I can't sit here today

with an explanation of why that is,"............ and ............

"Informing us all about that is probably a useful piece of work".

What did APRA

seek post 3

June 2017 to understand why Credit Card interest rates were so high, when

the

Cash Rate is

at an all time low of 1.5%? |

9 |

|

|

10th |

Governor of the Reserve Bank |

Has the

Governor of the

Reserve Bank who is the

Chair of the

Council

of Financial Regulators,

and co-wrote

LOAN RATE STICKINESS: THEORY AND EVIDENCE in June 1992,

ever discussed with the other two members of that Council, namely

APRA

and

ASIC, the

RBA informing the Government, pursuant to

section 11(1) of the Reserve Bank Act 1959,

of the need for the

RBA, pursuant to

section 50 of the Banking Act 1959, to re-regulate a maximum interest rate for

Purchases and

for

Cash Advances due to the burgeoning gap between the

Overnight Cash Rate of 1.5% and interest rates charged on low interest and on high

interest Credit Cards that peak at 29.49% for a

Cash Advance using a

Latitude Financial

"Go MasterCard"?

|

9 |

|

|

11th |

Royal

Commissioner |

Will

the Royal Commission recommend to the Chair of the

Three Financial Regulators

to provide Minutes of their quarterly meetings?

|

2 |

|

|

12th |

Governor of the Reserve Bank |

Is the Board of the

Reserve Bank

which is chartered under

Section 10(2) 'Functions of Reserve Bank

Board' of the

Reserve Bank Act 1959

to

"best

contribute to.......... the

economic prosperity and welfare of the

people of Australia"

aware of the primary findings of the reports (published

from 2005) from the

Productivity Commission, the ABS and ASIC that

classify and quantify the Financial Literacy Capacity of Australians that are

ranked as low as less than Level 1 up to Level 5?

In particular that

"For nearly half of the

population were assessed at either levels 1 (the lowest level) or 2, both of

which are below the minimum level deemed necessary to participate in a

knowledge-based economy (level 3)." |

3 |

|

|

12(a)th |

Chair of APRA |

Is the Chair of APRA,

Wayne Byres,

aware of the primary findings of the reports (published

from 2005) from the

Productivity Commission, the ABS and ASIC that

classify and quantify the Financial Literacy Capacity of Australians that are

ranked as low as less than Level 1 up to Level 5?

In particular that

"For nearly half of the

population were assessed at either levels 1 (the lowest level) or 2, both of

which are below the minimum level deemed necessary to participate in a

knowledge-based economy (level 3)." |

5 |

|

|

13th |

Chair of ASIC |

Will the Royal

Commission ask the Chair of ASIC that is bound by

Part 1-Preliminary Division 1 Objects

of

the

ASIC Act 2001 to -

* "improve

the performance of the financial system and entities in it;

and

*

" receive,

process and store, efficiently and quickly, information that is given to us",

to inform what action ASIC took to

protect

Financially Uneducated And Vulnerable

Credit Cardholders

that have poor

Financial Literacy Capacity,

after it published

ASIC Report 224 "Access

to financial advice in Australia"

in Dec 2010?

|

5 |

|

|

14th |

Chair of

Council

of Financial Regulators |

Will the Chair of the

Council

of Financial Regulators

provide to the

Royal Commission a schedule of the respective responsibilities of the

RBA, APRA and

ASIC (and the clauses relied upon in their respective

Acts listed at the top of this letter), that satisfy the 'Terms of Reference' and

'Statement of Expectations'

required under the

PGPA Act, that obligates each regulator to ensure

competition amongst

Credit Card Products which involves seeking information

to establish that

Credit Card Issuers

are not

engaging in

Numeracy And Literacy Discrimination

through

Unconscionable Credit Card Advertising

targeted at

Credit Cardholders with low

Numeracy and Literacy Skills? |

5 |

|

|

15th |

Governor of the Reserve Bank |

Will the Governor of the

Reserve Bank inform why its

Payments System

Board's 'Responsibilities and Powers

webpage

does not also list the

Banking Act 1959

under legislation that

governs the Payment Systems Board's

responsibilities and

powers?

|

1 |

|

|

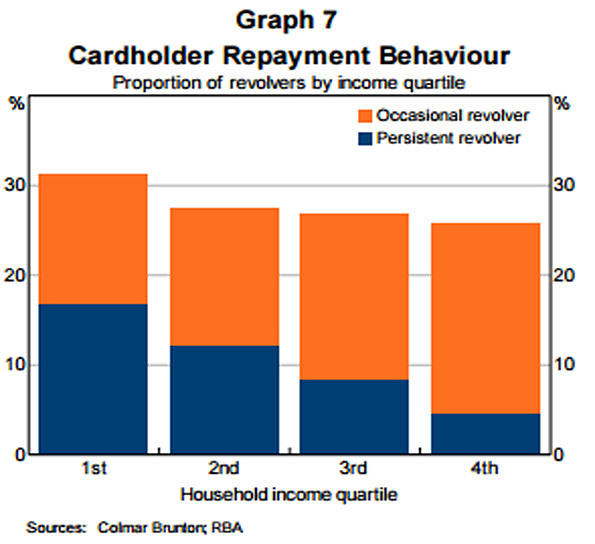

16th |

Chair of

Council

of Financial Regulators |

Will the

Chair of the

Council

of Financial Regulators

inform

if it sought

financial data from the primary six

Credit Card Issuers

(Four

Pillars,

Citibank and

Latitude Financial

nee G.E. Capital) that identifies the number,

Outstanding Indebtedness

and demography of

Credit Cardholders that are

Persistent Revolvers

after the

RBA quantified in

Graph 7 of

RBA Submission

to the Senate Inquiry into Matters Relating to Credit Card Interest Rates -

Aug 2015

the indebtedness borne by

Persistent Revolvers? |

3 |

|

|

17th |

CEO of the ABA that issued the

regulatory binding

Banking Code of Practice from 1 July 2019 |

Will the Royal Commission

ask the CEO of the ABA -

*

if

Example 1 -

Unconscionable Conduct - St George Visa Card of the

Nine Examples

within

Labyrinth of

‘Concealed Spiders’

constitutes

Unconscionable Conduct

(based in the ACCC's definition of

Unconscionable Conduct).

AND

* did St.

George Bank by charging interest @ 20% from the date of each

Purchase

for the subsequent two months constitute an illegal

penalty under the common law equitable penalty doctrine, because that

interest charge was collateral to the main obligation

(to pay the

Closing Balance

by the

Payment Due Date)

and the withdrawal of the

Interest Free Period

was intended to

be in terrorem of the other party (the Cardholder).

It was intended to scare the

Cardholder

(Mr. McK_nn) into paying his

Closing Balance

on time and the 20% interest rate was

a

Usurious Interest Rate

and therefore an unconscionable

penalty because 20% from the date of each

Purchase

did

not reflect the losses St. George Bank incurred as a result of the

Cardholder's

failure to pay the shortfall of $40 (2.06%) by the

Payment Due Date,

particularly as he was charged 20% on all his

Purchases

of

$1,936.92,

even though he had repaid

97.94% of his

Closing Balance

10 days prior to the

Payment Due Date.

==========================

(Example 1

notes that

St George

Credit Cardholder,

Peter

McK_nn,

had a

Closing Balance

of $1,936.92

of his Visa Gold Credit Card and

paid $1,896.92 (97.94%, of his

Closing Balance)

to

St. George Bank

on 22 May '14 (10 days prior to his monthly

Payment Due Date)

which was a shortfall of $40 on the

Closing Balance

of $1,936.92

of his Visa Gold Card. Peter was charged interest @ 20% by

St. George Bank on

$1,936.92

(his total

Purchases

for the previous month) even though he

had repaid

97.94% of his

Closing Balance

10 days prior to the

Payment Due Date.

He

then forfeited his

Interest Free Period

for two subsequent months, whereby being charged @ 20% interest from the date of

each

Purchase.) |

2 |

|

|

17(a)th |

Chairman

of ACCC |

Will the Royal Commission

ask the

Chairman of the ACCC, Mr. Rod Sims,

to

examine the information regarding advertisements for Credit Cards

(explained in the

Nine Examples

within

Labyrinth of

‘Concealed Spiders’),

with

particular regard to obligations under the

National Consumer Credit

Protection Amendment (Home Loans and Credit Cards) Act 2011,

to determine if any represent

Predatory Advertising,

ipso facto

Unconscionable Conduct

(based in the ACCC's description of

Unconscionable Conduct)? |

2 |

|

|

18th |

Chairman

of ACCC |

Will the Royal Commission ask the

Chairman of the ACCC, Mr. Rod Sims, if the 'Conditions

of use' booklets issued by St. George Bank, ANZ and

Westpac (summarised

in table in

Chapter 1)

and listed in

18th

with text

in small fonts

on innumerable page constitute

Unconscionable Conduct? |

3 |

|

|

19th |

Royal

Commissioner |

Will the Royal Commission recommend to the

Three Financial Services Regulators that they use their existing

regulatory powers to require all

Credit Card Issuers to simplify their

Credit Card Products

so that their Credit Cards 'Conditions of Use' booklet,

together with any Schedule/s referred to therein, -

(a) do

not exceed

50 pages in text no smaller than Arial 10 font;

and

(b) the existing height and width

of the booklet is retained?

|

4 |

|

|

20th |

Royal

Commissioner |

Does each of the

Four Pillars reducing their low interest credit card by

5% circa amidst the prospect of a Royal \ Commission,

evidence that the

Four Pillars

that issue 80% of Credit Cards used in

Australia, were uncompetitive during the

Council

of Financial Regulators 'watch', when each of the

RBA,

ASIC

and

APRA

have regulatory obligations to the Australian public

to ensure real competition amongst

Credit Card Issuers,

in particular the RBA

under

Section 10(2) 'Functions

of Reserve Bank Board' of Reserve Bank Act 1959 to

"best

contribute to.......... the

economic prosperity and welfare of the

people of Australia"

and for the

Payments Systems Board

to always

Act

in the Public Interest? |

5 |

|

|

21st |

Royal

Commissioner |

Will the Royal Commission recommend to the

Three Financial Regulators that they use their existing

regulatory powers to ban

Reward Programs?

|

6 |

|

|

22nd |

Royal

Commissioner |

Will the Royal Commission recommend to the

Three Financial Regulators that they use their existing

regulatory powers to ban

Credit Card Issuers

paying third party credit

card websites (finder.com,

canstar.com.au,

iselect.com.au

'et al')

to market/advertise/promote/recommend in any way, shape or form their

Credit Card Products

because such advertisements are conflicted, often misleading and deceptive and targeted at

Credit Cardholders with low

Financial Literacy Capacity as classified/quantified by the Productivity Commission and the ABS in

Chapter 1? |

2 |

|

|

23rd |

Royal

Commissioner |

Will the Royal Commission recommend to the

Three Financial Regulators that they use their existing

regulatory powers to ban any

Credit Card Issuer

offering

Balance Transfer Interest Free or Very Low interest introductory offers

which 'poach' profitable

Financially Uneducated And Vulnerable

other bank

Credit Cardholders

because

Persistent Revolvers

that

Lack Financial Acumen

contribute 80%

circa

of all

Interest and Penalty Fees Revenue generated from

Credit Card Products? |

6 |

|

|

24th |

Royal

Commissioner |

Will the Royal Commission ask the

ASIC

chairman, James Shipton, why

ASIC made

the following statement in

ASIC's Submission to the Productivity Commission Inquiry into competition in the

Australian financial system +- Sept 2017?

"A senate inquiry submission by Treasury noted

that in 2013 only 30% of surveyed users reported paying interest on their credit

card balance.98 .

Contrary to this self-reporting though, the share of balances attracting

interest at the time was in fact closer to two-thirds.99"

|

1 |

|

|

25th |

Royal

Commissioner |

Will

the Royal Commission recommend to the Governor of the

Reserve Bank that it provide to

the House of Representatives in the

Commonwealth Parliament an annual written

'Statement on the Conduct of Monetary Policy' which includes, inter alia -

A. an annual written 'Report on the

Profitability of Credit Cards'; and

B. certifies that Visa and MasterCard separately

complied with the two weighted-aver age

Interchange Fee benchmarks,

including 'companion cards',

during the relevant year,

namely 0.50% for Credit Cards and

8 cents

for Debit Cards?

|

4 |

|

|

26th |

Chair of Reserve Bank Board of Directors |

Will the

Royal Commission ask the Board of Directors of

RBA

to declare their aggregate -

*

Annual Cardholder Fees paid; and

*

Interest Costs

paid,

by

the eight members in

the 12 months to 30 June 2018 for enjoying the convenience of the

Lines of Credit provided by their personal Credit Cards?

|

1 |

|

|

27th |

Governor of the Reserve Bank |

Will the

Royal Commission ask the Governor of the Reserve Bank what investigations the Reserve Bank

has undertaken with Credit Card Issuers, the three

Credit Reporting Agencies,

Financial Counsellors

and

Credit Card Distress Authorities

to understand the number of

Credit Cardholders that are

experiencing

Extreme Financial And Emotional Distress

and the various financial quanta of that distress? |

8 |

|

|

28th |

Governor of the Reserve Bank |

Will the

Royal Commission ask the Governor of the

Reserve Bank

what the

Reserve Bank has done, and when it did it, to ensure that

Credit Card Issuers

do not issue further

Credit

Cards to applicants that are

experiencing

Extreme Financial And Emotional Distress

due to already having been issued

several Credit Cards?

|

2 |

|

|

29th |

Governor of the Reserve Bank |

Will the Royal Commission ask the

Reserve Bank to draw upon

its existing

Extensive Powers to establish a Standard for a 'Uniform Credit Evaluation Methodology' that all Credit Card Issuers must observe similar to

NAB's Microenterprise Loans

because too many Australian adults have obtained Credit Cards

with excessive interest rates which would be lower if the payment defaults were lower

due to a robust designated 'Uniform Credit Evaluation Methodology' that all

Credit Card Issuers

observed? |

8 |

|

|

30th |

Governor of the Reserve Bank |

Will the

Royal Commission recommend that the

Reserve

Bank

set a new Standard, pursuant to

Division 4, Section 18,

that requires all

Credit Card Issuers to issue a 'Provisional' Charge Card to any applicant

under the age of 21 that has not previously held a

Credit

Card? Any such applicant, predominantly school leavers, would need to

repay the entire

Closing Balance by the

Payment Due Date for a minimum of three months, prior to being issued with

a

Credit Card? |

2 |

|

{kind=link}