|

|

Evidence Facts Sheet Click on the myriad of blue or black underlined embedded threads beneath The Writer has conducted research into Predatory Advertising and Unconscionable Credit Card Interest Charging at Usurious Interest Rates Targeted at Credit Cardholders with low Financial Literacy Capacity.1st Fact: Australia's Principal Regulator of the Payments System is aware that many Australians have inadequate Financial Literacy Capacity to use Credit Card Products without incurring very high Interest Costs and Penalty Fees. In Dec 2010 ASIC Report 224 (pg 16) "53% of Australians (aged 15 to 74) had proficiency less than the minimum required for individuals to meet the complex demands of everyday life and work emerging in the knowledge-based economy, for document literacy and numeracy respectively". informs that the Productivity Commission, ASIC the ABS have separately published detailed reports that rank Australians as having between Level 1 (low) and Level 5 (high) for Numeracy and Literacy Skills. A person assessed at Level 5 possesses up to five times the skills within the particular domain (eg Numeracy, Literacy, Prose etc) than a person assessed at Level 1. Level 3 is regarded by the survey developers as the ‘minimum required for individuals to meet the complex demands of everyday life and work in the emerging knowledge-based economy’ (ABS 2006, p. 5).ASIC Report 224 "Access to financial advice in Australia" - Dec 2010 includes:

Re Footnotes 15 and 16 above, ASIC has ignored its acknowledgement in 2010 that:

2nd Fact: Australia's Principal Regulator of the Payments System is aware from the multitude of information sources in the below URL thread that Credit Cardholders with poor Financial Literacy Capacity have collectively paid many billions of dollars in Interest and Penalty Fees on their Credit Cards often at Usurious Interest Rates:

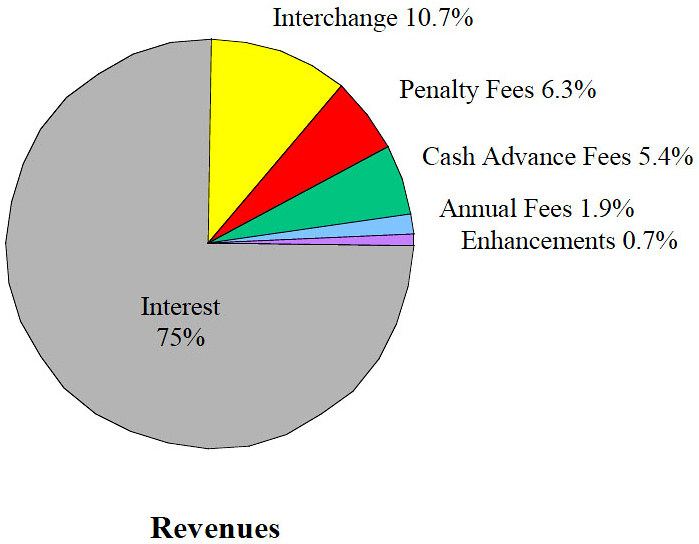

3rd Fact: The RBA and its Payment System Board enjoy authority to obtain financial information and powers to regulate Credit Cards 'unique among central banks', that exceed the Bank of England and the U.S. Federal Reserve. The RBA is the principal regulator of the Payments System through its PSB. Below is an extract from a Reserve Bank publication titled The Board's powers to promote efficiency and competition in the payments system are unique:

"The Reserve Bank is the principal regulator of the payments system through the PSB." As chronicled in the following paragraph, Australia's 'central bank' has unique powers and exceptional responsibilities "...to.......... the economic prosperity and welfare of (ALL) the people of Australia" and for its Payments Systems Board to always Act in the Public Interest; unique powers of the PSB not obligated upon the 'central bank' of the UK or the USA. The Reserve Bank of Australia has - A. powers to gather financial information from ADIs under Part 5—Miscellaneous, Section 26 of the Payment Systems (Regulation) Act 1998; andB. responsibilities to 'inter alia' "best contribute to.......... the economic prosperity and welfare of the people of Australia" in terms of Section 10(2) 'Functions of Reserve Bank Board' of Reserve Bank Act 1959 which includes - " ....inform the Government, from time to time, of the Bank's monetary and banking policy" under Section 11(1) of the Reserve Bank Act 1959; to set Standards that "are in the public interest" relying on Division 4, Section 18 of the Payments System Regulation Act 1998 for a Payments System that it Designated on 12 April 2001 (under Division 2—Section 11 of the Payment Systems (Regulation) Act 1998; and to re-regulate commercial bank interest rates, in particular a maximum interest rate for Credit Card Purchases and a maximum interest rate for Credit Card Cash Advances relying on Section 50 of the Banking Act 1959 that "are in the public interest", that are more extensive/inflexible/onerous than the - 1. Bank of England, that was not nationalised as Britain's central bank until 1946, which is a corporation wholly owned by the UK government - the 'Corporate governance: Board responsibilities' – SS5/16 (Short form) focus on the Corporates it regulates with no apparent obligation to best contribute to the peoples of Britain; and2. U.S. Federal Reserve that was established as the United States' central bank until 1913 , although the below item 7. "Promoting Consumer Protection and Community Development." obligates the U.S. Fed to research the impact of financial services practices on consumers and communities:"The Federal Reserve advances supervision, community reinvestment, and research to increase understanding of the impacts of financial services policies and practices on consumers and communities." The above is explained in The Reserve Bank had previously 'lined up all the requisite wooden ducks' to set Standards for Credit Cards to 'inter alia' re-impose a maximum Purchase interest rate and a maximum Cash Advance interest rate for 'public interest issues' (To Act In The Public Interest).NB: The Bank of England has been sued previously. 4th Fact:The 'central bank' responsibilities were withdrawn from the Commonwealth Bank in 1959. Ensuring the economic prosperity and welfare of the people of Australia has been an obligation of the RBA since 14 January 1960 Below are extracts from the RESERVE BANK BILL 1959 - Second Reading on 8 April 1959 which iterate that the economic prosperity and welfare of the people of Australia has always been an obligation of the RBA: "We charge it with the responsibility for the stability of the currency of Australia, the maintenance of full employment in Australia, and the economic prosperity and welfare of the people of Australia." "Mind you, the responsibility to maintain the stability of the currency, full employment, economic prosperity, and to care for the welfare of the people of this country has shifted to the Reserve Bank." 5th Fact:Does a former Labor Prime Minister give a tinkers cuss about the plight of over one million fellow Australians with poor Financial and Literacy Capacity, who through no fault of their own (identified by the RBA as Persistent Revolvers) have paid 80% circa of the Interest, Penalty Fees and Cash Advance Fees evident in the Credit Card Revenue pie chart due to Predatory Advertising and Unconscionable Credit Card Interest Charging at Usurious Interest Rates Targeted at Credit Cardholders with low Financial Literacy Capacity? 6th Fact: The RBA regulated all bank interest rates until rampant inflation and accompanying high interest rates in the late 1970s, when unregulated building societies/finance companies/credit unions were poaching banks deposits, caused inter alia the 18% Cap on Credit Cards to be removed in April 1985 When the 18% interest rate cap on all Credit Cards was removed by the RBA in April 1985, the spread was less than 1%, which is why that 18% cap was removed. With the Overnight Cash Rate fell to 0.25% in March 2020, that spread was asa high as 28% on a few Credit Cards for a Cash Advance. Latitude Financial's Go MasterCard credit card had a Cash Advance interest rate of 29.49% until March 2019. It is now 25.9%, but now incorporates a Cash Advance Fee of $3 or 3% of the cash advance, whichever is greater = 28.9%. There are over 16 million Credit Cards in Australia. Persistent Revolvers hold 12.58% circa of those 16 mil Credit Cards. Persistent Revolvers pay 80% circa of the Interest, Penalty Fees and Cash Advance Fees shown in the Credit Card Revenue pie chart. In May of this year, Choice CEO, Alan Kirkland, asserted that Credit Card Providers have stolen $6.3 billion from customers “by failing to pass rate cuts on for credit cards, banks have effectively stolen $6.3 billion from the pockets of Australians,” Mr Kirkland said. "The 10 worst credit cards in Australia – and why you should avoid them like the plague" Persistent Revolvers that account for a mere 12.58% circa of Credit Cardholders contributed a whopping 80% circa of that $6.3 billion Interest And Penalty Fees Revenue due inter alia to Credit Card Issuers not passing on falls in the Overnight Cash Rate. The remaining 20% of that $6.3 billion was paid by other Revolvers that account for 20.42% circa of all Credit Cardholders. The remaining 67% circa of all Credit Cardholders, described by the RBA as Transactors, contributed zilch of that $6.3 billion. Hardly, an example of the User Pays Principle that "RBA's Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001 advocated the application to Credit Card Products. "A movement towards a 'user pays' approach to credit card payment services would be consistent with the approach adopted by Australian financial institutions in pricing other payment instruments under their control." But its Board never adopted its own published policy document. Quantitative, Qualitative, Credit Card Distress Authorities, Numeracy And Literacy Authorities, And Newspaper Article - Evidence Of Unfair Credit Card Practices Which Prey Upon Financially Uneducated And Vulnerable Australians by Numeracy And Literacy Discrimination details a veritable welter of evidence of the Interest and Penalty Fees paid by Persistent Revolvers. The Principal Regulator of the Payments System should have re-imposed a maximum interest rate cap (limit) on Credit Cards as far back as June 1992 when the spread between the Overnight Cash Rate and the Purchase Interest Rate exceeded 16%, because of the RBA’s – A. obligations to “the economic prosperity and welfare of (ALL) the people of Australia” because its Payment System Board’s “has been given the backing of strong regulatory powers that are unique amongst central banks; and B. obligations to “inform the Government, from time to time, of the Bank’s monetary and banking policy”; and C. its Payments Systems Board needs to always Act in the Public Interest; unique powers of the PSB not obligated upon the 'central bank' of the UK or the USA. 7th Fact: The RBA has ignored the findings in Six Pivotal Credit Card Publications in the last 20 years (three of them were published by the RBA) that - * Credit Card interest rates were far too high; and * Revolvers, in particular Persistent Revolvers, were paying the costs of Transactors' Lines of Credit Failure to notify successive Commonwealth Govt’s that the Principal Regulator of the Payments System needed to re-impose a maximum interest rate to protect in alios Credit Cardholders with poor Numeracy and Literacy Capacity constitutes gross negligence and willful misconduct of its regulator obligations under civil law because – 1) RBA’s paper "Reform of Credit Card Schemes in Aust: "A Consultation Document" in Dec 2001 argued for greater application of the User Pays Principle; and 2) Six Pivotal Credit Card Publications during the last 26 years, three of which were written by the RBA, identified that interest rates on Credit Cards against reductions in the Overnight Cash Rate, were most sticky, "...The rate on credit cards is found to be the most sticky, followed by personal loan rates, the housing loan rate and the small business overdraft rate"; and 3) 12.58% circa of all Credit Cardholders, described by the RBA as Persistent Revolvers have paid 80% circa of all Interest and Penalty Fees Revenue. Section 2 B. of Extensive Powers and Responsibilities evidence that the RBA's powers and obligations to 'inter alia' "best contribute to.......... the economic prosperity and welfare of the people of Australia" are "unique among central banks" and exceed the obligations upon the USA and UK 'central banks', U.S. Federal Reserve and The Bank of England respectively, to the " ... economic prosperity and welfare.... " of their peoples. The below Recommendation 30 (page 254) of the Australian Govt Financial System Inquiry - Final Report - Nov 2014 recommended "Strengthening the focus on competition in the financial system" by reviewing "the state of 'competition' in the financial system every three years":

8th Fact: The pivotal matter for constitutional lawyers to opine on The RBA breached its Statutory Duty and Fiduciary Duty to Credit Cardholders with poor Financial Literacy Capacity by inter alia not informing the Federal Govt. as far back as late 1992 (obligated under Section 11(1) of the Reserve Bank Act 1959) that Section 10(2) 'Functions of Reserve Bank Board' of Reserve Bank Act 1959 obligated it (the RBA) to re-impose a maximum interest rate cap (limit) on Credit Cards because the spread between the Overnight Cash Rate and the Purchase Interest Rate exceeded 16% (in June 1992). Whereas when the 18% interest rate cap on all Credit Cards was removed by the RBA in April 1985, the spread was less than 1%, which is why that 18% cap was removed.The Payments System Regulation Act 1998 obligates the RBA's Payment System Board to act in the public interest.

Section 10(2) 'Functions of Reserve Bank Board' of Reserve Bank Act 1959 includes

responsibilities

'inter alia'

to

"best

contribute to.......... the economic prosperity and welfare of the people of

Australia"

The Parliamentary Acts that govern the responsibilities and authority of the Bank of England, or the U.S. Federal Reserve System, do not include: * to act in the public interest * to "best contribute to.......... the economic prosperity and welfare of the people of Australia" The definition of User Pays Principle provides other pertinent information concerning the obligations upon the Reserve Bank and its Payments System Board. As does Payments System Board’s Mandate and Objectives. 9th Fact: The definition of Unconscionable Conduct includes: is 62 pages written in tiny Arial 10 font or smaller "We strongly recommend that you read this booklet carefully and retain it for your future reference." 10th Fact: Annexure A is Two Exceedingly Costly Interest Charging Practices that the RBA failed to rectify at least 15 years ago to the material detriment of Credit Cardholders with poor Financial Literacy Capacity, invariably through no fault of their own. The ABA outlawed the second unconscionable interest charging practice on or before 1 July 2019. 11th Fact: A very brief second wave of the Royal Commission to right the wrongs within the most differentiated Product in the entire Western World, because - * 12.58% circa of all Credit Cardholders (identified by the RBA as Persistent Revolvers), invariable with low Financial Literacy Capacity , have paid 80% circa of all Interest and Penalty Fees Revenue; and* five former Prime Ministers have attested that Australia is an egalitarian country Thirty-Two Written Questions for one of three Financial Regulators - most are directed at the Governor of the Reserve Bank. Extensive Supporting Documented Evidence (under CLICK ON BELOW QUESTION NUMBERS on LHS) to justify each of the Thirty-Two Written Questions.

Credit Card Products are the most differentiated product (in both 'variety of types' and 'quantum of providers') in the entire Western World - by a country mile. And the legislation that governs the RBA's obligations and rights is manifold and complex. So multifarious that if the 2018 Royal Commission into Financial Services had kicked-off by investigating Unconscionable Conduct by many Credit Card Issuers that manifested over the last 20 or more years, Commissioner Hayne could have expended all of 2018 cleaning up only one banking product, albeit the most prolifically used, such is the breadth and depth of Unconscionable Conduct ostensibly targeted at Financially Uneducated And Vulnerable Australian Credit Cardholders with low Financial Literacy Capacity.

|

|

|

|

{kind=link}