|

|

Thirty Two Written Questions - most directed at Governor of the RBA Defined Terms and Documents 1305, 12 Glen St -

The Pavilion on the Harbour' scribepj@bigpond.com 0434 715.861

Insert

one of the enclosed two DVDs in a Windows PC

to auto-open this

Letter_to_Adele_Ferguson_5-Oct-19.htm

To navigate

this letter,

click on the countless

blue embedded threads herein 5 October 2019 Ms. Adele Ferguson PO BOX 4,

Dear Ms. FergusonThe

Writer herewith

provides a welter of evidence

for a Second Wave of the Royal Commission into Financial Services: * one week of cross examination of the Council of Financial Regulators, in particular its Chair (explained in Section 5 below) 12.58% circa of Credit Cardholders (categorised by the RBA as Persistent Revolvers) that possess low Financial Literacy Capacity and are Financially Uneducated And Vulnerable Australians contribute a whopping 80% circa of all Interest And Penalty Fees Revenue generated from Credit Card Products ostensibly due to Numeracy And Literacy Targeting from Unconscionable Credit Card Advertising. Labyrinth of ‘Concealed Spiders’ exposes 'nine examples' of Unconscionable Conduct from Predatory Advertising of some Credit Cards Credit Card Products evidences that the most widely used retail credit borrowing instrument in Australia is the most differentiated product (in both 'variety of types' and 'quantum of providers') in the entire Western World - by a country mile If the 2018 Royal Commission into Financial Services had kicked-off by investigating Unconscionable Conduct by many Credit Card Issuers that manifested over the last 20 years, Commissioner Hayne could have expended all of 2018 cleaning up only one banking product, albeit the most prolifically used, such is the breadth and depth of Unconscionable Conduct ostensibly targeted at Financially Uneducated And Vulnerable Australians; Credit Cardholders With Low Financial Literacy Capacity Unconscionable Credit Card Interest Charging focuses on a significant change in interest charging for Credit Cards that a Red Faced ABA, under a parachuted in, Anna Bligh, has regulated on ALL Credit Card Issuers in Aust. to implement no latter than 1 July 2019 under the ABA's 'Banking Code of Practice'. These regulated changes followed years of deceit perpetrated voracity fostered under Ms. Bligh's two predecessors, David Bell and then Steven Münchenberg Australia's Principal Regulator of the Payments System should have regulated the changes in the ABA's 'Banking Code of Practice', pertinent to Credit Cards, over 25 years ago when the Bank Interest Rate Margin between the Overnight Cash Rate and the average Purchase interest rate exceeded 16% - back in June 1992. In not doing so, the - * RBA breached its Statutory Duty to "best contribute to.......... the economic prosperity and welfare of ALL the people of Australia"; and * Payments Systems Board abrogated its responsibility to always Act in the Public Interest,

by not

informing the Commonwealth Govt required under

under

Section

11(1) of the Reserve Bank Act 1959

to

"

....inform the Government, from time to time,

of the Bank's monetary and banking

policy"

having regard to its obligations under

Section 10(2)

' If the SMH shares the Writer's belief that Australia's Principal Regulator of the Payments System failed in its Statutory Duty to inter alia re-impose a maximum interest rate on Credit Cards when the spread between to Overnight Cash Rate and the maximum interest rate for Purchases increased from less than 1% (April 1985) to 28% (March 2019) (for a Cash Advance) to the Extreme Financial And Emotional Distress of Persistent Revolvers, then the SMH should read inter alia the Writer's 3rd letter to Dr. Peter Brandson, Bank Reform Now dated 2 Aug 2019 (that seeks a second wave of the Royal Commission - a mere two weeks of hearings and cross examination) which inter alia provides -* Thirty Two Written Questions - most directed at the Governor of the Reserve Bank; and * extensive Supporting Documented Evidence to justify each of the Thirty Two Written Questions

1. Pertinent events since mid-2010 by the Writer re Credit Card Products: (a) Has undertaken well over a thousand hours gathering evidence of Unconscionable Conduct by some Credit Card Issuers of Credit Card Products that have mislead and deceived using Predatory Advertising, charging Usurious Interest Rates Targeted At Credit Cardholders With Low Financial Literacy Capacity - evident in the embedded URL threads in his 570 circa Defined Terms and Documents, in particular Labyrinth of ‘Concealed Spiders’. (b) Posted on CDs to the Reserve Bank his Submission dated 8 Dec 2011 that beseeched the RBA to rely upon its Extensive Powers to require Credit Card Issuers in Australia to adopt the User Pays Principle because Transactors enjoy their Lines of Credit at virtually no cost and Persistent Revolvers that regularly possess poor Financial Literacy Skills and account for only 12.58% circa of Credit Cardholders contribute a whopping 80% circa of all Interest And Penalty Fees Revenue generated from Credit Card Products. Section 8 of his submission to the RBA accords with recommendations within "RBA's Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001 in particular "A movement towards a “user pays” approach to credit card payment services would be consistent with the approach adopted by Australian financial institutions in pricing other payment instruments under their control."(c) Posted a Submission to Maurice Blackburn on 25 June 2017 (on DVD) asking it to run a Class Action representing 400,000 circa Eligible Persistent Revolver Plaintiffs against the Reserve Bank for breach of its Statutory Duty and Fiduciary Duty to the material detriment of those Eligible Persistent Revolver Plaintiffs. (d) Maurice Blackburn response letter dated 14 July 2017 included:

(e) Emailed his Public Submission sent 22 April 18 to the Royal Commission which was deemed ineligible because this Writer had not personally suffered a financial loss.

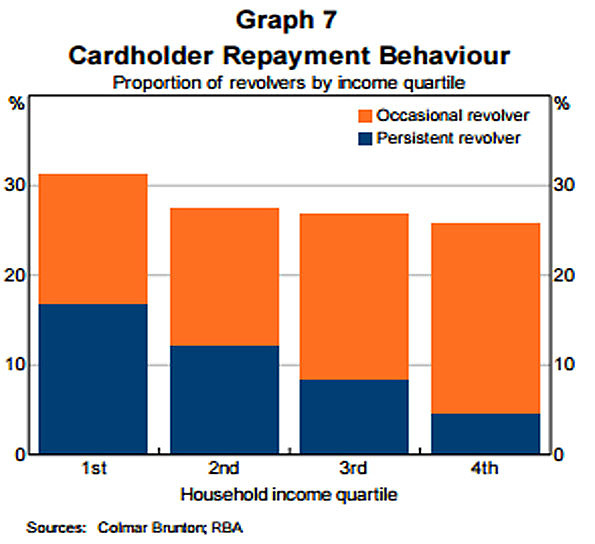

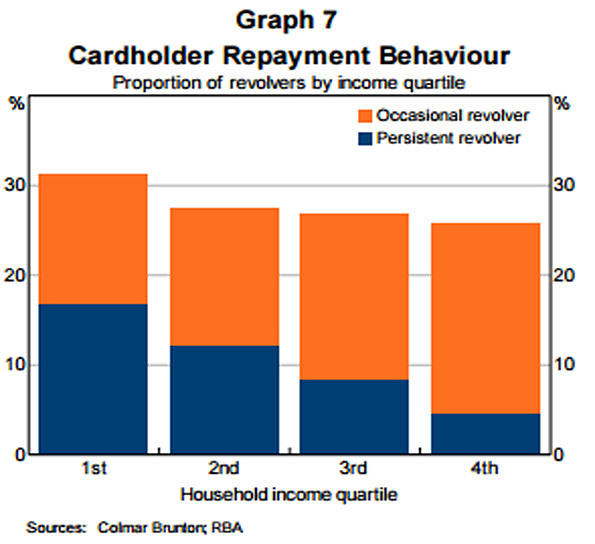

(f) Posted all requisite information to Dr. Peter Brandson, CEO, Bank Reform Now, PO Box 497, Batemans Bay NSW to justify a second wave of the Royal Commission (only two weeks of hearings and cross examination), specifically to address an alleged breach of Statutory Duty by Australia's Principal Regulator of the Payments System that has cost 400,000 circa Credit Cardholders across Australia (first identified as Persistent Revolvers by the Reserve Bank of Australia in its Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - Aug 2015 in Graph 7 titled ''Cardholder Payment Behaviour") because 400,000 circa Credit Cardholders -

2. Earlier this year, the Writer provided all necessary evidence to Bank Reform Now for it to lobby for a second wave of the Royal Commission focusing on a breach of Statutory Duty by the Principal Regulator of the Payments System

The Bank Reform Now website proclaims:

It attests -Bank Reform Now's Facebook and Twitter make similar representations. The Writer posted his initial submission to Dr. Peter Brandson, Bank Reform Now dated 16 March 2019 in A4 hardcopy, USB Flash Drive and 2 DVDs under the following title/headings:

The Writer posted Version 2 of his original submission to Dr. Peter Brandson, Bank Reform Now dated 9 April 2019. The Writer posted his 3rd letter (also in DVDs, USB Stick and A4) to Dr. Peter Brandson, Bank Reform Now dated 2 Aug 2019. Below is a sentence from that 3rd letter: ''The Writer welcomes discussing with you his above work, after you have sought a lawyer, versed in “statutory interpretation”, to appraise the above referenced sections of legislation that govern the RBA's statutory obligations.'' Notwithstanding the above claims on the Bank Reform Now website, the Writer never received any response from Dr. Peter Brandson. Click on Thirty Two Questions and Supporting Evidence for a second wave of the Royal Commission to consider asking - A. "the principal regulator of the payments system through the PSB", and Chair of the Council of Financial Regulators, that -

B. the Chair of ACCC as to whether particular aspects of Credit Card Issuers' marketing representations fall within the ACCC's definition of Unconscionable Conduct; C. the Chair of APRA regarding his undertaking to a Senate Enquiry on 3 June 2017 that included: "....the margins on credit card business look very high, certainly to any other form of credit, and certainly I can't sit here today with an explanation of why that is,"............ and ............ "Informing us all about that is probably a useful piece of work"? D. the Chair of ASIC to inform what action ASIC took to protect Financially Uneducated And Vulnerable Credit Cardholders that have poor Financial Literacy Capacity, after ASIC published Report 224 "Access to financial advice in Australia" in Dec 2010 that included:

The UK Guardian article 'The interest-free credit card trap snaring unwitting borrowers' is rife with examples of UK Credit Card Issuers' Predatory Marketing directed at Financially Uneducated And Vulnerable Credit Cardholders that Lack Financial Acumen. There is a welter of evidence that U.S. Credit Card Issuers are not immune from similar Unconscionable Credit Card Advertising. One could presuppose: "Well why shouldn't it be any different in Australia?" It SHOULD be different in Australia, because Australia's 'central bank' has unique powers and exceptional responsibilities "...to.......... the economic prosperity and welfare of the people of Australia" and for its Payments Systems Board to always Act in the Public Interest, not held by the 'central bank' of the UK or the USA. Below is an extract from the Writer's page titled Australia's Principal Regulator of the Payments System:

Australia's 'central bank' has never exercised its rights - * under Part 5—Miscellaneous, Section 26 of the Payment Systems (Regulation) Act 1998 to ask for financial data from the major Credit Card Issuers of Interest & Penalty Fees revenue for each of their Credit Cardholders for all Credit Card Products for a minimum of 12 months in order to establish if the User Pays Principle applies, notwithstanding that the RBA argued for greater application of the User Pays Principle in its paper "Reform of Credit Card Schemes in Aust: "A Consultation Document" in Dec 2001; or

* under

Section

11(1) of the Reserve Bank Act 1959

to

"

....inform the Government, from time to time,

of the Bank's monetary and banking

policy"

having regard to its obligations under

Section 10(2) ' * the RBA recommended in Dec 2001; and * the Writer recommended in Section 8 of his letter (on CD) to the RBA dated 8 Dec. 2011 - explained in Point 9 of Supporting Evidence re 1st Question.

3. In April 1985 the RBA

removed an 18%

interest rate cap on Credit Cards when the

Overnight Cash Rate was 17.2%.

The RBA capped the maximum interest rate on Credit Cards in Australia at 18% until April 1985. The cap was withdrawn when the Overnight Cash Rate was a smidgeon over 17% during an era of very high inflation and associated interest rates. Australia's Principal Regulator of the Payments System, the RBA, should have re-imposed a maximum interest rate on Credit Cards over 25 years ago when the spread between the Overnight Cash Rate and the average Purchase interest rate exceeded 16% - back in June 1992.

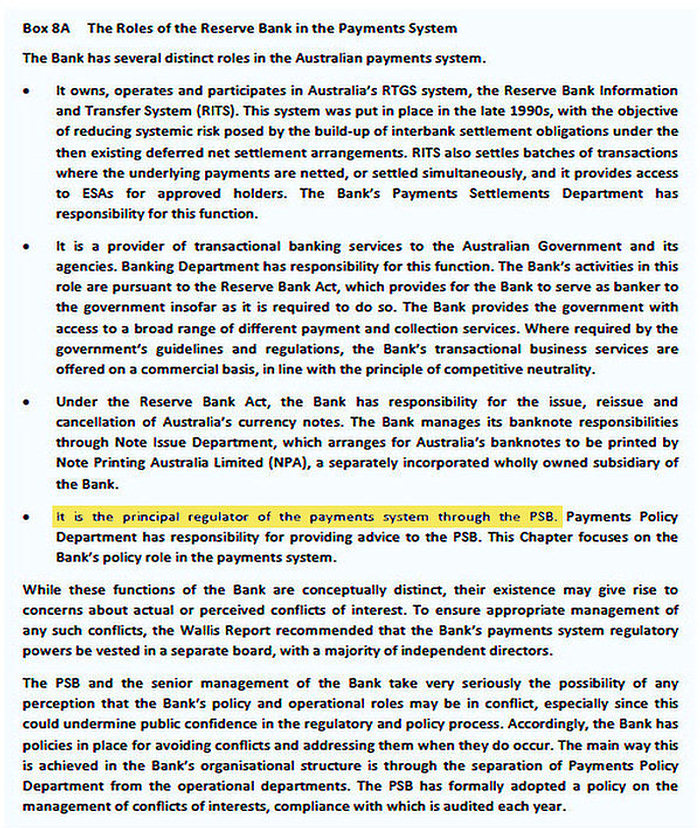

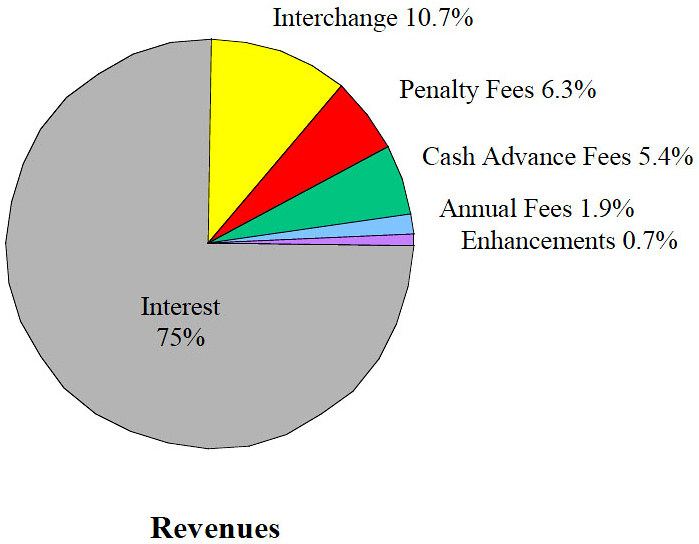

Significantly, prior to the Campbell Report circa early 1980's, the RBA regulated all Australian bank interest rates with an Iron Fist - "... when de-regulation resulted in adverse consequences, re-regulation ensued...". Prior to The Campbell Committee recommendations Australian banks had been highly regulated - dating back to the failure of banks in the 19th century. The particulars of deregulation are well covered by: * "Overview of Financial Services Post-Deregulation - 2002 - Dr. Diana Beal * "CHANGES IN THE BEHAVIOUR OF BANKS AND THEIR IMPLICATIONS FOR FINANCIAL AGGREGATES - July 1989" - Battellino and McMillan* Consumer Affairs Victoria - Regulating the cost of credit - Research Paper No. 6 2006* The Unpleasant Truth About Australian Banking - bankinfoline.com By its own admission in Box 8A of the Reserve Bank's Submission to the Financial System Inquiry - March 2014, "The Reserve Bank is the principal regulator of the payments system through the PSB." The payments system includes control over Credit Card Products. Persistent Revolvers, as identified by the RBA in Graph 7 'Cardholder repayment behaviour' invariably possess only Level 1 or Level 2 Financial Literacy Capacity (as measured by the Productivity Commission and the ABS). Persistent Revolvers have paid a horrible price since the 18% cap on Credit Card interest rates was removed by the RBA in April 1985 – Latitude Financial's Money Go MasterCard credit card had a Cash Advance interest rate of 29.49% until last March . It is now 25.9%, but now incorporates a Cash Advance Fee of $3 or 3% of the cash advance, whichever is greater = 28.9%. There are over 16 million Credit Cards in Australia. Persistent Revolvers hold 12.58% of those 16 mil Credit Cards. Persistent Revolvers pay 80% circa of the Interest, Penalty Fees and Cash Advance Fees shown in the Credit Card Revenue pie chart. Chapter 5 and Chapter 17 note inter alia that between 1960 and 1980 the Reserve Bank diligently regulated Australian commercial bank interest rates relying on Section 50 of the Banking Act 1959 as amended. Until 1980 banks could not offer more than 3¾% on a passbook account and 6½% interest on a Savings Investment Account (minimum account balance of $500, deposits and withdrawals must be $100 or greater, and 7 days written notice had to be given to the bank for all withdrawals). "......... to achieve monetary policy, public sector financing and sectoral assistance objectives.....", as well as safeguarding against further bank collapses (chronicled in Chapter 17). Chapter 5 notes:

Prior to Aug 1993, Credit Card Issuers were restricted from charging an Annual Fee on Credit Cards as the various State Credit Acts prohibited most Credit Card Issuers from charging annual fees if they charged interest on credit card purchases (e.g. Credit Act 1984 (NSW) s 54). Following a recommendation from the Prices Surveillance Authority’s 1992 ' Inquiry Into Credit Card Interest Rates', State legislatures issued exemption orders which allowed all financial institutions to charge both interest and fees on credit cards from 1 August 1993.Below is an extract from Consumer Affairs Victoria - Regulating the cost of credit which evidences that in the past if de-regulation did not achieve the desired results, then re-regulation followed.

"the principal regulator of the payments system through the PSB", and Chair of the Council of Financial Regulators -

(1) has extensive powers to, inter alia, request information from payment system participants and operators regarding Credit Cards under, amongst other clauses, Part 5—Miscellaneous, Section 26 of the Payment Systems (Regulation) Act 1998; (2) is bound to " ....inform the Government, from time to time, of the Bank's monetary and banking policy" under Section 11(1) of the Reserve Bank Act 1959 having regard to its obligations under Section 10(2) 'Functions of Reserve Bank Board' of Reserve Bank Act 1959 to "best contribute to.......... the economic prosperity and welfare of the people of Australia"; (3) holds authority under Division 4, Section 18 of the Payments System Regulation Act 1998 to set Standards that "are in the public interest" for a previously 'designated Payments System (under Division 2—Section 11 of the Payment Systems (Regulation) Act 1998 after having also imposed an Access Regime under Section 12. Re (2) above, sub clause (xiii) of Section 51 of the Australian Constitution behoves the Australian Parliament to place serious weight on any recommendation by the RBA re "banking".After sharing emails with Ms. Sharon van Etten, Public Relations Officer, Media & Public Relations Office, Reserve Bank of Australia, the Writer posted his extensive submission (on 3 CDs and A4) to the RBA in Dec 2011 seeking application of the User Pays Principle. Section 8 of his submission accords with recommendations within "RBA's Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001. " A movement towards a “user pays” approach to credit card payment services would be consistent with the approach adopted by Australian financial institutions in pricing other payment instruments under their control."

The RBA should then have imposed a maximum interest rate on all Credit Cards - 1. for all Purchases a maximum interest rate of 850 basis points; and 2. for all Cash Advances of 950 basis points, above the RBA official interest rate (Overnight Cash Rate). But it should have re-imposed a maximum interest rate over 25 years ago when the spread between the Overnight Cash Rate and the average Purchase interest rate exceeded 16% - back in June 1992.

4. 400,000 circa Credit Cardholders with Poor Numeracy and Literacy Capacity, often through no fault of their own, have paid a frightful price because of Unconscionable Credit Card interest rates, Predatory Marketing and Numeracy And Literacy Targeting

As detailed in the Writer's Submission to Maurice Blackburn dated 25 June 2017 seeking a Class Action against the RBA for breach of its Statutory Duty and Fiduciary Duty, 400,000 circa Credit Cardholders across Australia - a) have paid in excess of $20,000 each in Interest and Penalty Fees (charged at Usurious Interest Rates) during up to a continuous nine years period at an average Comparison Rate Over 18% Per Annum; b) were misled by Predatory Advertising Targeted At Credit Cardholders With Low Financial Literacy Capacity that constitutes Unconscionable Conduct; c) have suffered Extreme Financial And Emotional Distress; and d) posses poor Financial Literacy Capacity (predominantly Level 1 or below, and some Level 2) as - (i) identified and quantified by the Productivity Commission, the ABS and ASIC separate written reports (Chapter 1); and (ii) evidenced on a daily basis by 500 circa Financial Counsellors employed by 44 charities/community organisations that collectively receive $43 million annually from the Commonwealth Govt. ($20m) and the State Govts ($23m) via Financial Counselling Australia (Chapter 7). Hardly a month goes by without another newspaper article, or report by ASIC, the Reserve Bank or a plea from a Credit Card Distress Authority, regarding the debt burden born by a small number of Credit Cardholders, invariably with Poor Numeracy and Literacy Skills that the RBA has referred to as Persistent Revolvers. Meanwhile two thirds of Credit Cardholders, described by the RBA as Transactors, enjoy their Lines of Credit a virtually no cost, because Annual Cardholder Fees account for only 2% of Interest And Penalty Fees Revenue.

Is Australia really an egalitarian country? Five Prime Ministers have talked it, but our Federal Govt hasn't walked it, obligated under Section 51 (xiii) of the Australian Constitution, to the detriment of Financially Uneducated And Vulnerable Australians that possess, through no fault of their own, poor Financial Literacy Skills; some Credit Card Issuers have deployed Predatory Advertising and charged Usurious Interest Rates and Penalty Fees, Targeted At Credit Cardholders With Low Financial Literacy Capacity.

St Vincent de Paul, Salvos, Anglicare et al provide a welter of Financial Counsellors where Credit Card Debt Accruing Interest, often spread over several Credit Cards, is invariably the root of Extreme Financial And Emotional Distress. Australian Governments allocate $43.38 million annually to 44 Australian charities to provide financial counselling to Australians that are experiencing Extreme Financial And Emotional Distress. National Debt Helpline is a not-for-profit service that provides professional counsellors to help Australians tackle their debt problems. 5. A brief second wave of the Royal Commission to right the wrongs within the most differentiated Product in the entire Western World, because - * 12.58% of all Credit Cardholders, invariable with low Finan cial Literacy Capacity, have paid 80% circa of all Interest and Penalty Fees Revenue; and* five former Prime Minister's have attested that Australia is an egalitarian country The Interim Report from the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry found faults in the regulatory performance of ASIC and APRA. Alas it did not investigate patent Unconscionable Conduct amidst the most widely used lending product in Australia, namely Credit Card Products - the antithesis of the User Pays Principle with 67% circa of Credit Cardholders, known as Transactors, enjoying a Free Ride, whilst 12.54% circa of Credit Cardholders, identified by the Reserve Bank as Persistent Revolver, contribute 80% circa of all Interest and Penalty Fees Revenue. The complexity and massive differentiation within Credit Card Products is conceivably the reason that Commissioner Hayne avoided investigating the marketing and pricing by some Credit Card Issuers. The Royal Commission into Financial Services in 2018 failed to recognise an alleged manifest breach of Statutory Duty by the Reserve Bank (summarised in Extensive Powers and Parliamentary Bestowed Mandate) by not recommending to the Federal Govt., as far back as July 1992, to reintroduce a maximum interest rate on Credit Cards, pursuant to under Section 11(1) of the Reserve Bank Act 1959 and the various Federal Govts for not invoking sub clause (xiii) of Section 51 of the Australian Constitution to pursue a maximum interest rate on Credit Cards. Pursuant to the Royal Commissions Act 1902 (Cth) and clauses (g), (h) and (j) of the Terms of Reference of the 2018 Royal Commission into misconduct in the Banking, Superannuation and Financial Services Industry, the Writer seeks by 1 April 2020 a second wave (two weeks of hearings/cross examination) that - 1. investigates the Writer's alleged systemic failings of the non-statutory Council of Financial Regulators performance over the Credit Cards Payments System and the highly differentiated Credit Card Products; and 2. seeks the Council of Financial Regulators to account for the alleged inept behaviour identified in this letter, not limited to requiring the Principal Regulator of the Payments System to - (i) elucidate on the RBA's Extensive Powers and shoulders Responsibilities to All Australians and for its Payments Systems Board to always Act in the Public Interest; responsibilities not held by the 'central bank' of the UK or the USA, namely the US Federal Reserve and the Bank of England to - (a) request any financial information from ADIs that it wants to examine; or (b) responsibilities to "........best contribute to........the economic prosperity and welfare of (ALL) the people of Australia". (ii) explain why it did not recommend to the Federal Govt to reintroduce a maximum interest rate on Credit Cards when the Bank Interest Rate Margin exceeded 16% - back in June 1992, pursuant to Section 11(1) of the Reserve Bank Act 1959, mindful of sub clause (xiii) of Section 51 of the Australian Constitution. (iii) recommend to the Federal Govt under Section 11(1) of the Reserve Bank Act 1959 a maximum interest rate for all Purchases and a slightly higher maximum interest rate for all Cash Advances; and (iv) reflect, with the value of hindsight, if the below concern expressed by the then Westpac CEO, Bob Joss, (previously Wells Fargo) to the Wallis Inquiry in 1997 was prophetic: "Also relevant is the Inquiry’s concern with fairness, or the equitable treatment of the various users of the financial system." "Protection of consumers On-going monitoring of credit card pricing in anticipation of a substantial inquiry into the effects on consumers of the deregulation of credit card interest rates" (v) comment whether "A movement towards a “user pays” approach to credit card payment services would be consistent with the approach adopted by Australian financial institutions in pricing other payment instruments under their control." ("RBA's Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001) was every effectively implemented on the Retail Supply Side of Credit Cards?(vi) opine on the seven other recommendations (in Section 8 of the Writer's Submission to the RBA dated 8 Dec 2011) re changes to Credit Cards, many to better protect Australians with poor Financial Literacy Skills. Yours sincerely Philip Johnston - the Writer ================================== Synopsis Format of this Letter ==================================

|

|

|

|

{kind=link}

{kind=link}

{kind=link}

{kind=link}