Insert one of the three enclosed CDs into a Windows PC to auto-open this page.

About 15 seconds after inserting a CD, left click on the Windows prompt on lower RHS of your monitor.

Then left click on the file titled

Left click on it and then left click on the welter of embedded URLs in Blue Text or Red Text or BLACK underlined Bold Text to open associated files.

To leave a page and return to the previous page, click on the arrow at top left of your screen/monitor.

If this page accidentally closes when you leave another page, right click on

your CD Drive icon and left click on 'Open Auto Play'.

If using a MAC, or one of the enclosed two USB sticks, or the enclosed

CDs do not auto-open at this letter, then navigate to CreditCards/Comms/Letter_to_Paul_Keating_28-Oct-20.htmEvidence Facts Sheet Thirty-Two Questions Directed at Three Financial Services Regulators and Supporting Evidence Two Exceedingly Costly Interest Charging Practices Defined Terms and Documents

1305, 12 Glen St -

The Pavilion on the Harbour'

Milsons Point NSW 2061

scribepj@bigpond.com 0434 715.861

CONFIDENTIAL CONFIDENTIAL CONFIDENTIAL

28 October 2020

The Honourable PJ Keating

PO Box 1265

Potts Point NSW 1335

Australia

Dear Mr. Keating

Section 10(2)

'

The

Reserve Bank

breached its

Statutory Duty

and

Fiduciary Duty

to

Credit Cardholders

with poor

Financial Literacy Capacity

(400,000 circa of them) for inter alia

not informing the Federal Govt. as far back as late 1992

(obligated under

Section 11(1) of the Reserve Bank Act 1959)

that it (the RBA)

needed to re-impose

a

maximum interest rate

cap (limit)

on

Credit Cards

because the

spread between the

Overnight Cash Rate

and the

Purchase

Interest Rate

exceeded 16% (in

June 1992).

Whereas when the 18% interest rate cap on all Credit Cards was

removed by the RBA in April 1985, the spread was less than 1%, which is why that 18% cap

was removed,

although pursuant to

Section 10(2)

'

The Writer's Submission to Maurice Blackburn (on CD) sought it to run a Class Action against the RBA on behalf of 400,000 circa Eligible Persistent Revolver Plaintiffs, that are Financially Uneducated And Vulnerable Australian Credit Cardholders with poor Financial Literacy Capacity that had been preyed upon by Predatory Advertising. Each of the 400,000 circa (that I estimated) had paid in excess of $20,000 in Interest and Penalty Fees, too often enduring Unconscionable Credit Card Interest Charging at Usurious Interest Rates. Evidence Of Unfair Credit Card Practices Which Prey Upon Financially Uneducated And Vulnerable Australians by Numeracy And Literacy Discrimination contains a veritable welter of proof, across a variety of platforms, of inter alia Extreme Financial And Emotional Distress Suffered by the 400,000 circa Eligible Persistent Revolver Plaintiffs

Maurice Blackburn response letter dated 14 July 2017 (two full pages) included:

Conclusion"

In our view there would be legal risks associated with a claim in relation to the circumstances outlined in your letter and for this reason the proposed claim does not meet our criteria for the pursuit of a class action.

Although it may be the case that financially vulnerable consumers are at risk when it comes to credit card products, we think that the concerns outlined in your letter would be best addressed by legislative or regulatory change that is designed to protect the interests of these consumers. In this regard, we suggest that you contact your local Member of Parliament to continue your advocacy on behalf of vulnerable consumers."

Meanwhile the Parliamentary appointed Gatekeeper with a charter to inter alia "best contribute to.......... the economic prosperity and welfare of (ALL) the people of Australia", had remained asleep at the wheel. Prior to the Campbell Report circa early 1980's, the same 'central bank' regulated all Australian bank interest rates with an Iron Fist. The Principal Regulator of the Payments System has been complicit in some Credit Card Providers targeting Australians with poor numeracy and literacy skills - detailed in Labyrinth of ‘Concealed Spiders’. 67% circa of Credit Cardholders, referred to by the RBA as Transactors, receive their Lines of Credit at virtually no cost, with some receiving Reward Points

{kind=link}

It took the threat to Brand Name of inter alios the Four Pillars from a Royal Commission into Misconduct in Banking for a Red Faced ABA, under a parachuted in, Anna Bligh, to urgently prohibit some Unconscionable Credit Card Practices by regulating ALL Credit Card Issuers in Aust. to implement, no later than 1 July 2019, the ABA's 'Banking Code of Practice' that inter alia Outlawed the Unconscionable Practice of charging interest on all Purchases made during the previous month unless every dollar of those Purchases was repaid by the Payment Due Date - that existed in Example 1 - Unconscionable Conduct - St George Visa Card. The RBA should have outlawed what the ABA, under Anna Bligh, banned under the the ABA's 'Banking Code of Practice' on 1 July 2019 at least 20 years earlier. Outlawing the Unconscionable practice explained in Example 1 - Unconscionable Conduct - St George Visa Card has materially reduced Credit Card Issuers' profitability and substantially alleviated Credit Cardholders with poor Financial Literacy Capacity

Would you send one CD, one USB Stick, and one of the A4 hardcopy of key information, to two different 'constitutional lawyers' to opine on my -

A. allegations against the RBA in this letter;

B. Thirty-Two Questions Directed at Three Financial Services Regulators, or a Royal Commissioner, and Supporting Evidence that warrant each question being asked in a Second Wave of the Royal Commission into Financial Services; and

C. my easy to appraise Evidence Facts Sheet?

Some people like using a CD which auto opens at this page (in a Windows Operating System), whereas others prefer to use a USB Stick and navigate to open this page.

By following the written instructions at the top of this page, the two 'constitutional lawyers' will be able to appraise the veracity of my allegations and questions to regulators herein.

1. Overview

In May 2020, Choice CEO, Alan Kirkland, asserted that Credit Card Providers have stolen $6.3 billion from customers “by failing to pass rate cuts on for credit cards, banks have effectively stolen $6.3 billion from the pockets of Australians,” Mr Kirkland said.

* "The 10 costliest credit cards in Australia – and why you should avoid them like the plague" - CHOICE

Paul Keating recently spurned the RBA to follow the 'long lead' of several 'central banks' to increase their fiscal pot, by buying long dated Govt. bonds from new electronically created money sourced 'out of the ether' - QE. In light of the below assertion, the former Labor Prime Minister should be concerned about the plight of hundreds of thousands of Persistent Revolvers that represent a mere 12.58% circa of all Credit Cardholders, yet contribute a whopping 80% circa of all Interest And Penalty Fees Revenue generated from Credit Card Products, often suffering Extreme Financial And Emotional Distress:

"No one in Australian public life had done more to lift up the Reserve Bank while giving it a singular discretion over interest rates than I did. And no one carried a greater cost of it."

Persistent Revolvers that account for a mere 12.58% circa of Credit Cardholders contributed a whopping 80% circa of that $6.3 billion Interest And Penalty Fees Revenue due to Credit Card Issuers not passing on falls in the Overnight Cash Rate. The remaining 20% of that $6.3 billion was paid by other Revolvers that account for 20.42% circa of all Credit Cardholders. The remaining 67% circa of all Credit Cardholders, described by the RBA as Transactors, contributed zilch of that $6.3 billion Interest And Penalty Fees Revenue. Hardly, an example of the User Pays Principle that "RBA's Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001 advocated the application to Credit Card Products. But its Board never adopted its own published policy document.

Back in 2011, after sharing emails with Ms. Sharon van Etten, Public Relations Officer, Media & Public Relations Office, RBA, the Writer posted his extensive submission (on 3 CDs and A4) to the RBA on 8 Dec 2011 seeking application of the User Pays Principle to Credit Card Products. Section 8 of his submission accords with recommendations within "RBA's Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001. "A movement towards a “user pays” approach to credit card payment services would be consistent with the approach adopted by Australian financial institutions in pricing other payment instruments under their control."

Following receipt of the Writer's comprehensive letter to the RBA dated 8 Dec 2011 in 3 identical CDs, the RBA should then have re-imposed a maximum interest rate on all Credit Cards of -

1. 850 basis points circa for Purchases; and

2.

950 basis points circa for Cash Advances,above the RBA official interest rate (Overnight Cash Rate) as the Writer's comprehensive letter implored. But it should have re-imposed a maximum interest rate almost 19 years earlier when the spread between the Overnight Cash Rate and the Standard Purchase Interest Rate exceeded 16% - back in June 1992. The Writer emailed Ms. Sharon van Etten that he had posted those CDs and A4 hardcopies (and two updated versions - 9 CDs in toto). He received no response to his letter on 9 CDs dated 8 Dec 2011.

Inaction by APRA and ASIC has been attributed to some scandals exposed in the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry. Puzzlingly Australia's Principal Regulator of the Payments System came out of the Royal Commission unscathed. It should not have because of the Extensive Powers bestowed upon the Reserve Bank, in particular under the Payment Systems (Regulation) Act 1998, conferred an obligation upon the RBA, pursuant to Section 11(1) of the Reserve Bank Act 1959, to inform the Commonwealth Govt. that it (RBA) needed to re-impose a maximum Credit Card interest rate limit/cap as far back as late 1992 by -

-

setting new Standards that "are in the public interest" relying (from July 1998) on Division 4, Section 18 of the Payments System Regulation Act 1998,

-

for a previously Designated Payments System (under Division 2—Section 11 of the Payment Systems (Regulation) Act 1998 - eventually Designated on 12 April 2001 ,

-

after having also previously imposed an Access Regime under Division 3 Section 12 - imposed on 23 Feb 2004.

Below is an extract from Designated and Regulated Payment Systems that evidenced that the RBA had actioned all the 'conditions precedent' in order to re-impose a maximum interest chargeable by Credit Card Issuers relying upon the Payments System Regulation Act 1998:

"The RBA -

'Designated' Credit Card Schemes in Australia on 12 April 2001, relying on Division 2, Section 11 of the Payment Systems (Regulation) Act 1998. The RBA overtly stressed when it opted to 'Designate' "...credit card schemes in Australia under its regulatory oversight."... that ...."the standards will not cover the setting of credit card fees and charges to cardholders and merchants, or interest rates on credit card borrowings"

Imposed an 'Access Regime' on 23 Feb 2004 on each of the three designated credit card schemes in Australia (Visa, MasterCard and Bankcard) relying upon Division 3 - Access to designated systems, Subdivision A - Access regimes of the Payment Systems (Regulation) Act 1998; and

Determined 'Standards' pursuant to Division 4, Section 18 of the Payments System Regulation Act 1998 that "are in the public interest" on 1 Sept 2016 and 1 July 2017.

Failure to notify successive Commonwealth Govt’s, obligated under pursuant to Section 11(1) of the Reserve Bank Act 1959, that the Principal Regulator of the Payments System needed to re-impose a maximum interest rate to "best contribute to.......... the economic prosperity and welfare of the people of Australia"; specifically to protect in alios Credit Cardholders with poor Numeracy and Literacy Capacity, constitutes gross negligence and willful misconduct of its regulator obligations under civil law because –

1) RBA’s paper "Reform of Credit Card Schemes in Aust: "A Consultation Document" in Dec 2001 argued for greater application of the User Pays Principle. Transactors do not pay the real economic cost of their Lines of Credit that they enjoy, because they meticulously pay for their Purchases up to 45 days in arrears; and

2) Six Pivotal Credit Card Publications during the last 26 years, three of which were written by the RBA, identified that interest rates on Credit Card Products against reductions in the Overnight Cash Rate, were most sticky, "...The rate on credit cards is found to be the most sticky, followed by personal loan rates, the housing loan rate and the small business overdraft rate"; and

3) 12.58% circa of all Credit Cardholders, described by the RBA as Persistent Revolvers had paid 80% circa of all Interest and Penalty Fees Revenue.

Section 2 B. of Extensive Powers and Responsibilities evidence that the RBA's powers and obligations to 'inter alia' "best contribute to.......... the economic prosperity and welfare of the people of Australia" are "unique among central banks" and exceed the obligations upon the USA and UK 'central banks', U.S. Federal Reserve and The Bank of England respectively, to their peoples' economic prosperity and welfare.

Recommendation 30 (page 254) of the Australian Govt Financial System Inquiry - Final Report - Nov 2014 recommended Strengthening the focus on competition in the financial system by reviewing "the state of 'competition' in the financial system every three years":

Recommendation 30

Review the state of competition in the sector every three years, improve reporting of how regulators balance competition against their core objectives, identify barriers to cross-border provision of financial services and include consideration of competition in the Australian Securities and Investments Commission’s mandate.

"As an immediate first step, regulators should examine their rules and procedures to assess whether those that create inappropriate barriers to competition can be modified or removed, or whether alternative and more pro-competitive approaches can be identified.42 Each regulator should report back to Government prior to the first external review of the state of competition.

Government should update ASIC’s mandate to include a specific requirement to take competition issues into account as part of its core regulatory role.43

These proposals are in addition to the recommendations in this report addressing sectoral issues in banking, payments and financial markets."

Both ASIC and Australian Treasury are members of the Council of Financial Regulators. The abovementioned Financial System Inquiry Final Report sits on the Australian Treasury website. Notwithstanding the need to "Review the state of competition in the sector every three years", seemingly, neither ASIC, nor Australian Treasury, has nudged the RBA to re-impose a maximum interest rate on Credit Cards or indeed encouraged Credit Card Issuers to reduce interest rates on their existing Credit Card Products. Apart from the ACCC, our financial regulators are too adept at keeping a chair warm.

2. Australia's Central Bank previously regulated all bank interest rates

Prior to the Campbell Report circa early 1980's, the RBA had imposed an 18% maximum interest rate upon all Credit Card Issuers. Australia's banking history evidences that "... when de-regulation resulted in adverse consequences, re-regulation ensued...". Due to failures of banks in the 19th century, Australian banks had been highly regulated. Particulars of deregulations and subsequent re-regulations are well chronicled. That 18% cap on the maximum interest rate on all Credit Cards was withdrawn in April 1985 when the Overnight Cash Rate was a smidgeon over 17% during an era of very high inflation.

Until 1980 banks could not offer more than 3¾% on a passbook account. "From 1966, when personal loans were introduced, the maximum rate that banks could charge was set by the Reserve Bank."

Four Economic Reasons for the Campbell Committee Report – Sept 1981 notes inter alia that the Campbell Report recommended removal of the caps on all bank products in an era when commercial interest rates skyrocketed and building societies, credit unions and finance companies had been progressively poaching traditional national and state bank’s depositors’ balances (accounts) since the late ‘70s. “.. by the early 1980s the banks’ share of savings had fallen to 40 per cent, compared with 70 per cent in the early 1950s.” The Overnight Cash Rate peaked at over 20% in June 1984.

3. Australia's Central Bank's obligation to the Australian people

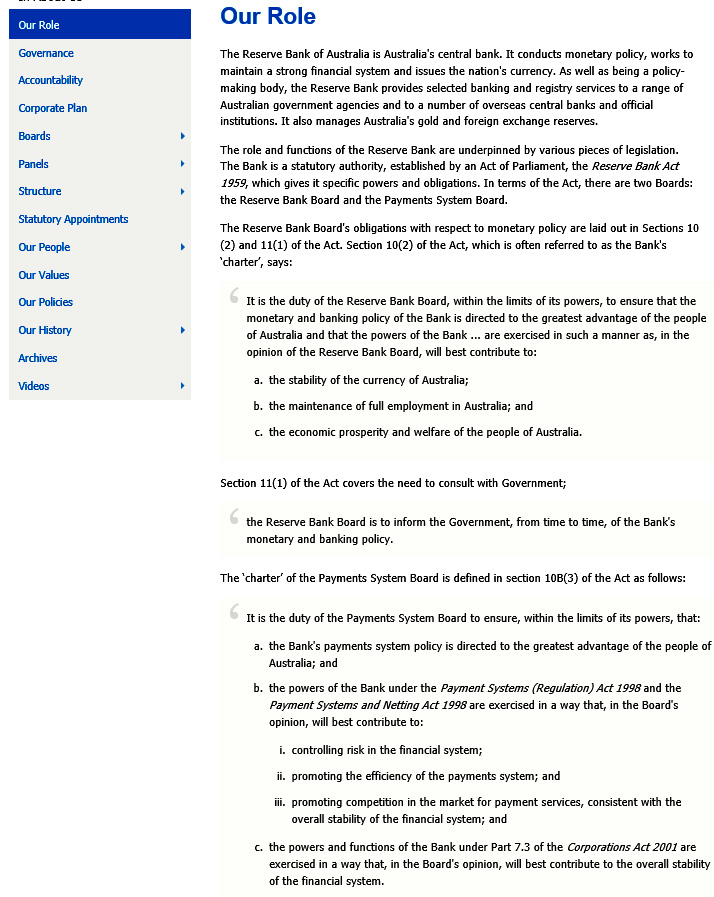

The RBA, Australia's 'central bank', has professed itself to be Australia's Principal Regulator of the Payments System.

The RBA's "Our Role" represents to "

best contribute to.......... the economic prosperity and welfare of (ALL) the people of Australia". That obligation to "the people of Australia" far exceeds the obligations upon the USA and UK 'central banks', U.S. Federal Reserve and The Bank of England respectively, to their peoples.{kind=link}

The Payment Systems (Regulation) Act 1998 obligates the Payments Systems Board to always Act in the Public Interest. The Act "allows it to undertake more direct regulation of ‘Designated’ payments systems when it judges it to be "in the public interest". This may involve the imposition of access rules or operating standards (under Division 4, Section 18 of the Payments System Regulation Act 1998) for participants in such systems."

but the Board's legislative responsibility and powers to promote efficiency and competition in the payments system are unique. This responsibility has broadened the Bank's traditional focus on the high-value wholesale payment systems which underpin stability, to encompass the retail and commercial systems where large transaction volumes provide scope for efficiency gains."

Below are extracts from Reserve Bank of Australia Bulletin - July 1998 - Australia’s New Financial Regulatory Framework that chronicles the Reserve Bank's powers, set out in the Payment Systems (Regulation) Act 1998, that allow the Reserve Bank to undertake more direct regulation of ‘designated’ payments systems to –

"... promote competition in the market for payments services, consistent with the overall stability of the financial system..." when it judges it to be "in the public interest" which may involve the imposition of access rules or operating standards for participants in such systems:

"The new Payments System Board is responsible for the Bank’s payments system policy, the objectives of which are:

• controlling risk in the financial system arising from the operation of the payments system;

• promoting the efficiency of payments systems; and

• promoting competition in the market for payments services, consistent with the overall stability of the financial system.

The Bank’s powers in this area, set out in the

Payment Systems (Regulation) Act 1998, allow it to undertake more direct regulation of ‘designated’ payments systems when it judges it to be in the public interest. This may involve the imposition of access rules or operating standards for participants in such systems. The Act also provides a framework for regulation of purchased payment facilities, such as travellers cheques and stored-value cards."Below is an extract from the Writer's page titled Australia's Principal Regulator of the Payments System:

998 for a Payments System that it Designated on 12 April 2001 (under Division 2—Section 11 of the Payment Systems (Regulation) Act 1998; and"The Reserve Bank of Australia -

A. has powers to gather financial information from ADIs under Part 5—Miscellaneous, Section 26 of the Payment Systems (Regulation) Act 1998; and

B. has responsibilities to 'inter alia' "best contribute to.......... the economic prosperity and welfare of the people of Australia" in terms of Section 10(2) 'Functions of Reserve Bank Board' of Reserve Bank Act 1959 which includes -

" ....inform the Government, from time to time, of the Bank's monetary and banking policy" under Section 11(1) of the Reserve Bank Act 1959;to set Standards that "are in the public interest" relying on Division 4, Section 18 of the Payments System Regulation Act 1

to re-regulate commercial bank interest rates relying on Section 50 of the Banking Act 1959 that "are in the public interest",

that are more extensive/inflexible/onerous than the -

1. Bank of England, that was not nationalised as Britain's central bank until 1946, which is a corporation wholly owned by the UK government - the 'Corporate governance: Board responsibilities' – SS5/16 (Short form) focus on the Corporates it regulates with no apparent obligation to best contribute to the peoples of Britain; and

2. U.S. Federal Reserve that was established as the United States' central bank until 1913, although the below item 7. "Promoting Consumer Protection and Community Development." obligates the U.S. Fed to research the impact of financial services practices on consumers and communities:

"The Federal Reserve advances supervision, community reinvestment, and research to increase understanding of the impacts of financial services policies and practices on consumers and communities."

Below is a brief extract from description of the Reserve Bank of Australia (RBA) by Clayton Utz:

"The RBA’s monetary policy is primarily directed at maintaining inflation rates at the level most conducive to sustainable growth. The RBA’s financial stability policy aims to prevent excessive risks in the financial system and to limit the effects of financial disturbances when they occur. Within this role, the RBA has a particular responsibility for maintaining the efficiency of the payments system. The RBA is governed by the Reserve Bank Board and the Payments System Board."

4. Australia's Central Bank has failed its obligations to the Australian people

To the Writer's knowledge, Australia's 'central bank' has not exercised its rights -

* under Part 5—Miscellaneous, Section 26 of the Payment Systems (Regulation) Act 1998 to ask for financial data from the major Credit Card Issuers of Interest & Penalty Fees revenue for each of their Credit Cardholders for all Credit Card Products for a minimum of 12 months, or even 6 months, in order to establish if the User Pays Principle applies, notwithstanding that the RBA argued for greater application of the User Pays Principle in its paper "Reform of Credit Card Schemes in Aust: "A Consultation Document" in Dec 2001; or

* under Section 11(1) of the Reserve Bank Act 1959 to " ....inform the Government, from time to time, of the Bank's monetary and banking policy"

having regard to its obligations under Section 10(2) '* the RBA recommended in Dec 2001; and

* the Writer recommended in Section 8 of his letter (on CD) to the RBA dated 8 Dec. 2011 - explained in Point 9 of Supporting Documentary Evidence re 1st Question.

5. Australia's Central Bank should have regulated most of the changes pronounced in the ABA's 'Banking Code of Practice at least twenty years earlier

In view of the above noted obligations, at least from the Payment Systems (Regulation) Act 1998, if not several years beforehand, -

* Australia's Principal Regulator of the Payments System has breached its Statutory Duty to "best contribute to.......... the economic prosperity and welfare of (ALL) the people of Australia"; and

* its Payments Systems Board has abrogated its responsibility to always Act in the Public Interest by failing to "..undertake more direct regulation of ‘designated’ payments systems when it judges it to be in the public interest",

due to condoning Two Exceedingly Costly Monthly Interest Charging Practices by many Credit Card Issuers that Targeted Credit Cardholders With Low Financial Literacy Capacity, whereupon Financially Uneducated And Vulnerable Australians have suffered Extreme Financial And Emotional Distress.

Please read Two Exceedingly Costly Monthly Interest Charging Practices carefully because it explicitly evidences that the Reserve Bank has breached its Statutory Duty and Fiduciary Duty to Credit Cardholders with poor Financial Literacy Capacity. Persistent Revolvers that account for a mere 12.58% circa of Credit Cardholders contribute a whopping 80% circa of all Interest And Penalty Fees Revenue generated from Credit Card Products. The numeric dollar magnitude of those losses is explained in the Writer's Submission to Maurice Blackburn lawyers.

Why is the Writer so adamant that the RBA has patently failed is parliamentary responsibilities? Answer: Because LOAN RATE STICKINESS: THEORY AND EVIDENCE (June 1992) recognised that Credit Card Issuers were not passing on reductions in the cost of funds, but did zilch about regulating them to lower interest rates on their Credit Cards, yet it possessed the Extensive Regulatory Powers to do so:

This paper examines the degree of price stickiness in the market for bank loans. In the classical world of perfect competition, changes in marginal costs are translated into similar changes in the price of the product. We find that complete pass-through of changes in banks' marginal cost of funds only occurs with the base or reference overdraft rates to large and small business borrowers. For credit cards, personal loans, owner-occupied housing loans and the standard overdraft rate, changes in the banks' marginal cost of funds have not been translated one for one into the contemporaneous lending rates."

Unconscionable Credit Card Interest Charging focuses on a significant change in interest charging for Credit Cards that a Red Faced ABA, under a parachuted in, Anna Bligh, regulated on ALL Credit Card Issuers in Aust. to implement by 1 July 2019 under the ABA's 'Banking Code of Practice'. These regulated changes followed years of deceit perpetrated voracity fostered under Ms. Bligh's two predecessors, David Bell and then Steven Münchenberg. Below is a critical extract from Unconscionable Credit Card Interest Charging:

"ABC News article, Banks revamp code of practice in face of scandals, royal commission -

(A). informed that the current CEO of the ABA, Anna Bligh, announced in late Dec 2017 that the ABA had just lodged a 'Banking Code of Practice' with the Australian Securities and Investments Commission (ASIC) for approval; and

(B). listed several changes that will be legally binding on all 'member banks' of the ABA which includes:

"Customers only paying interest on what remains on a credit card and not the full amount of purchase if a loan is being paid down."

The fact that the ABA has made it mandatory in its lodged Banking Code of Practice that its members charge interest on ONLY any unpaid portion of the Closing Balance after the Payment Due Date is patent evidence that the previous long-running practice (explained in Unconscionable Credit Card Interest Charging) was Unconscionable Conduct Targeted At Credit Cardholders With Low Financial Literacy Capacity."

6. References to the Writer's earlier approaches on CDs concerning Australia's Central Bank's failure to observe its Parliamentary Bestowed Mandate to "best contribute to.......... the economic prosperity and welfare of (ALL) the people of Australia" that includes Credit Cardholders, through no fault of their own, with Low Financial Literacy Capacity

Writer's letter to Ms. Sharon van Etten, Public Relations Officer, Media & Public Relations Office, Reserve Bank of Australia dated 8 Dec 2011 seeking application of the User Pays Principle to Credit Cards.

Writer's Submission to Maurice Blackburn dated 25 June 2017 and Maurice Blackburn's response letter dated 14 July 2017.

Writer's Submission to Adele Ferguson dated 5 Oct 2019 that provided evidence for a Second Wave of the Royal Commission into Financial Services

Writer's Submission to Ian Verrender dated 5 Feb 2020 that provided evidence for a Second Wave of the Royal Commission into Financial Services.

Writer's Submission to Michael West Media dated 10 July 2020 that alleged that the RBA had breached its Statutory Duty and Fiduciary Duty to Credit Cardholders with poor Financial Literacy Capacity

The

Writer's letter on CDs to 5, 6 and 7 above -a) recommended a very brief second wave of the Royal Commission; and

b) provided

Thirty-Two Written Questions directed at Financial Services Regulators, and a Royal Commissioner, and my Supporting Evidence that warrant these questions.to right the wrongs within the most differentiated product in the entire Western World, because -

* 12.58% circa of all Credit Cardholders, invariable with low Finan

cial Literacy Capacity, have paid 80% circa of all Interest and Penalty Fees Revenue; and* five former Prime Ministers have attested that Australia is an egalitarian country, yet it is not.

Thirty-Two Written Questions are directed at one of three Financial Regulators - most are intended for the Governor of the Reserve Bank. There are also a few questions to a Royal Commissioner.

Extensive Supporting Documented Evidence to warrant each of the Thirty-Two Written Questions is accessible by clicking on each Question number.

Neither Adele Ferguson, Ian Verrender or Michael West Media responded to the above written approaches. Perhaps because Credit Card Products are the most differentiated product (in both 'variety of types' and 'quantum of providers') in the entire Western World - by a country mile. And the legislation that governs the RBA's obligations and rights is manifold and complex.

So complex, that if the 2018 Royal Commission into Financial Services had kicked-off by investigating Unconscionable Conduct by many Credit Card Issuers that manifested over the last 20 years, Commissioner Hayne could have expended all of 2018 cleaning up only one banking product, albeit the most prolifically used, such is the breadth and depth of Unconscionable Conduct ostensibly targeted at Financially Uneducated And Vulnerable Australian Credit Cardholders with Low Financial Literacy Capacity.

7. Postscript

If the recent contrite behaviour by the Financial Services Sector, specifically the commercial banks, is to remain, the RBA must be held to account

for the Extreme Financial And Emotional Distress that the Financially Uneducated And Vulnerable Persistent Revolvers, have suffered during the last 20 years or so, where the vast majority received their first Credit Card in their late teens or very early adulthood, with not a skerrick of money management understanding, but rather were confronted by Predatory Advertisements.Yours sincerely

Philip Johnston - the Writer