Writer's CD submission to RBA Intro Letter to Maurice Blackburn Submission Letter to Maurice Blackburn Second Letter to Maurice Blackburn Maurice Blackburn response letter Intro Letter to Nick Xenophon Submission Letter to Nick Xenophon ResponseFromXenophonTeam Defined Terms & Documents

1305, 12 Glen Street 'The

Pavilion'

Milsons Point NSW 2061

0434 715.861

15 September 2017

Insert

one of the two enclosed DVDs in a Windows PC

which will open at this LetterToExecutiveProducersFourCorners_15-Sept-17.htm

If using a MAC or the enclosed USB

stick drive,

or the enclosed two DVDs do not open automatically in a Windows computer, open this letter at CreditCards\ABC\LetterToExecutiveProducersFourCorners_15-Sept-17.htm

Executive Producers

Four Corners

Refer: Sam

Lipski

and Robert

Raymond

ABC Ultimo Centre

700 Harris Street

Ultimo NSW 2007

Dear Sam and Robert - (click on any of the embedded URLs in light blue text or Bold black text in the headings)

Proposed Four Corners programme titled "Nobody Cares in a Christian Country" that would chronicle/detail the ineptitude of Two of Australia's Three Financial Services Regulators to the detriment of almost half a million Persistent Revolvers.

Almost one million (945,706 - cell B36) Credit Cardholders have been identified by the Reserve Bank as Persistent Revolvers.

Four Types of Revolvers estimates that approx. half of that 945,000 Credit Cardholders, namely 473,000 circa Credit Cardholders are Financially Uneducated And Vulnerable Australians that possess only Level 1 or Level 2 Financial Literacy Capacity that -

* suffer Extreme Financial And Emotional Distress; and

* contribute 40% circa of

Interest and Penalty Fees Revenue

to Credit

Card Issuers, even though there are 7.515 million Credit Cardholders

in Aust.

Persistent Revolvers

pay over $5b in

Interest And Penalty Fees Revenue annually to

Credit Card Issuers.

Ipso facto, Persistent Revolvers that are Financially Uneducated And Vulnerable Australians, namely 473,000 Credit Cardholders circa pay over $2.5b in Interest And Penalty Fees Revenue annually.

Each Financially Uneducated And Vulnerable Persistent Revolver pays over $5,000 circa on average in Interest And Penalty Fees annually, because of -

A. the ineptitude of the Reserve Bank of Australia, and to a lesser extent ASIC, collectively Two of Australia's Three Financial Services Regulators, due to -

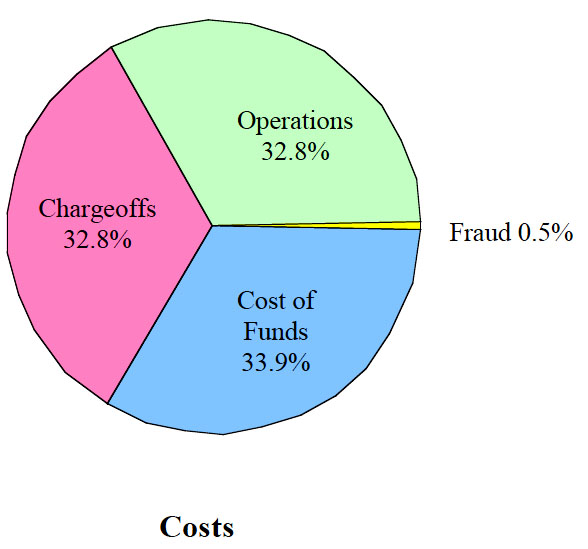

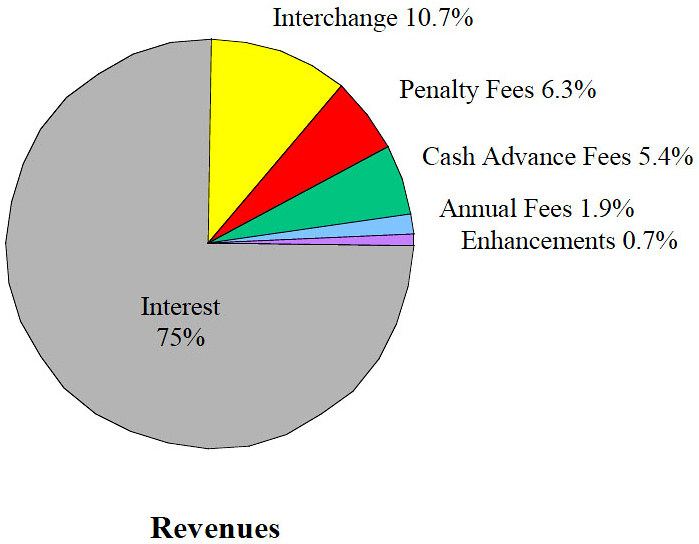

(i) not regulating adoption of the ubiquitous User Pays Principle to Credit Cards usage after the Reserve Bank advocated its adoption in a Consultation Document in 2001, so that Transactors also contribute to the pie chart of Costs and the pie chart for Revenues, and not merely Revolvers 'forking-out for other Christians';

{kind=link}

{kind=link}

(ii) the Reserve Bank not drawing upon its unique Extensive Powers and Responsibilities to ALL Australians to require Credit Card Issuers to provide regular financial information of Credit Card Indebtedness on a demographic socio-economic basis to identify which cohorts of Credit Cardholders are being unfairly burdened due to their poor Financial Literacy Capacity; and

(ii) the Reserve Bank being too slow to ban some types of Unconscionable Conduct and only after earlier action by the then UK Regulator, BIS - it took the Reserve Bank over 10 years to commence the steps to ban the Unconscionable 'Order of Payments' Allocation Practice;

(iv) the Reserve Bank should have Determined Standards (obligated upon it under Section 8 of the Payments System Regulation Act 1998) and other rights/duties/obligations listed in Extensive Powers and Responsibilities of the RBA) to re-introduce a cap on Credit Card Purchase and Cash Advance interest rates (18% max interest rate cap on Credit Cards was removed in 1985), pursuant to Section 11 of the Reserve Bank Act 1959, any time after the Reserve Bank published LOAN RATE STICKINESS: THEORY AND EVIDENCE in June 1992; and

B. Predatory Advertising and Numeracy And Literacy Targeting by many Credit Card Issuers whereupon many Financially Uneducated And Vulnerable Australians have paid Usurious Interest Rates with no Interest Free Period and usually incurring Late Payment Fees (some also incurring OverLimit Fees), whilst 67% circa of Credit Cardholders, referred to by the Reserve Bank as Transactors, pay nothing, or very little, for enjoying a Line/s of Credit for up to 55 days - many Transactors are Free Riders

Section 2 and Section 3 of 'Extensive Powers and Responsibilities of the RBA' evidences that the Reserve Bank has explicit obligations/responsibilities to Persistent Revolvers, whereas the U.S. Federal Reserve and the Bank of England do not

ASIC website - Our Role provides a succinct definition on Unconscionable Conduct and sets out its obligations (see also ASIC and Australian Securities and Investments Commission)

1. The age old 'Survival of the fittest' adage

'Survival of the fittest' has prevailed throughout the 125,000 years that Homo sapiens has walked 'terra firma'. It continues to triumph today. However, the fittest are no longer the bodily strongest dominating the physically weaker. Or the fittest that for over 100,000 years ran down faster animals due to possessing greater physical endurance. Very little hunting involved throwing a spear or firing an arrow. Hunting was normally more primitive where a human on two legs chased a smaller animal on four legs; eventually breaking its spirit (due to greater physical endurance) and then its spine.

The fittest today continue to survive at the expense of the weak. However, in the last scintilla of human existence (the last 20 or so years) the fittest are humans who -

(i) know the tax laws to avoid paying any capital gains tax, even owning a dozen or more investment properties, by occupying each of their investment properties for a minimum of three months within each six years period; or

(ii) are adept at reading the fine print (in 9 font grey) to avoid the pitfalls dissected in Labyrinth of ‘Concealed Spiders’ and enjoy Lines of Credit where they take receipt of goods and services, on a daily basis, and not pay for those goods and services for up to 55 days later - many are Free Riders; or

(iii) are adept at reading the fine print (in 9 font grey), so as to not get scammed on a mobile phone plan; or

(iv) know the rudimentaries about getting their car serviced, so they are not 'taken for a costly ride' by an unscrupulous motor mechanic wanting to change half the components under the bonnet; or

(v) are aware that when you negotiate say 22% off electricity and 12% off gas on a 12 months energy plan with AGL, Origin Energy 'et al', that you need to re-negotiate a new 12 months contract in 12 months time, because those attractive and material discounts fall away at the end of a 12 months' contract and you will pay 100 cents in the dollar from then on unless you argy bargy with the providers or use iSelect 'et al'.

The Writer worked for the Commonwealth Bank for 37 years until retiring in 2007. It was owned by the Australian Govt until privatised in 1991. Being the Govt. owned bank, Australians trusted its staff. The Writer worked at four suburban branches until moving to H.O. departments 1974. In his early branch years, when assisting customers to open a Passbook Account, Savings Investment Account, an IBD, cheque account or purchase travellers cheques, CBA staff always acted in the best interests of their customers. Unfortunately, post privatisation, some senior CBA staff (blow-ins) overtly exploited that trust which had been built up over 30 years since 1959. That betrayal has angered retired staff who had fostered that trust. The Writer worked under five MDs, starting with Sir. Bede Callaghan and ending with Ralph Norris. David Murray started at CBA Lindfield in 1996 and retired as M.D. in 2006. He was an exceptional M.D. who knew banking "from the grass roots upwards".

Incumbent CEO, Ian Narev, had less than five years experience in banking when appointed CEO in 2011, after coming from McKinsey Consulting in 2007. Alas, Mr. Narev's commercial banking experience was not in Risk Management (the core of commercial banking) or Relationship Banking (endeavouring to gain, or retain, Corporate accounts, by dealing with CFOs and CEOs re loan facilities). Rather Ian Narev worked in strategic planning at CBA from 2007. The chap who can "talk under wet concrete with a mouthful of marbles" was appointed CEO in 2011, by the Board of the Commonwealth Bank that was negligent by not undertaking requisite due diligence re Mr. Narev's performance at CBA.

CBA staff are now remunerated on sales which are prominent in KPIs. Ian Narev received $12.3m in remuneration for the 12 months to 30 June 2016. Hence, staff are conflicted into promoting products that -

* contain Spiders in the fine print of voluminous Terms and Conditions documents; and/or

* provide 'kick-backs' to CBA or directly to a financial adviser.

Fortunately for Australians, but not CBA shareholders, some of the outcomes of a Board appointing a non-commercial banker as CEO of Australia's largest bank, have received public prominence.

There has never been a period in the history of Homo sapiens where courageous, emboldened regulators are more required. Why? Because in the case of Australia's largest bank, under Ian Narev's watch since 2011, unconscionable behaviour by Commonwealth Bank employees has flourished (financial planning scandal, insurance claim denials, failing to report (to AUSTRAC) money laundering through ATMs and cash accepting machines by drug dealing 'et al') due to exploiting and abusing a mindset of public trust that had been built up over generations. That could not have occurred under David Murray's leadership, because he knew the responsibilities of his Department Heads, better than they did. Alas, it often takes extraordinary courage by the likes of Kate McClymont, Rachel Olding and journalists at Four Corners to embarrass regulators into action.

2. Will Four Corners present a programme titled 'Nobody Cares in a Christian Country'?

This letter seeks Four Corners to present a programme titled 'Nobody Cares in a Christian Country' focusing on (ii) above only.

As noted at the bottom of this letter, should one of the two Executive Producers read this letter, and one of his delegates also read my other recommended documents to -

* Australia's principal and oldest financial services regulator;

* the leading Class Action law firm in Australia; and

the Writer will provide 'Written Questions' (that he has prepared) to the Executive Producers for a Four Corners' interviewer to ask -

* Phillip Lowe, Governor of the Reserve Bank; and

* separately to ask Greg Medcraft, Chairman of ASIC,

that evidence, in the opinion of the Writer, gross negligence by these Two Financial Services Regulators for not having regulated "yonks ago" to protect Financially Uneducated And Vulnerable Australians against Numeracy And Literacy Targeting (refer A.(i) to A.(iv) in the above titles/headings) as evidenced in Nine Examples Of Predatory Advertising.

Why have these Two Regulators been negligent when the same unscrupulous behaviour re Credit Cards continues to exist in the UK and the USA? Because, as explained in (iv) C. and D. below, and detailed in Section 2 and Section 3 of Extensive Powers and Responsibilities of the RBA (and ASIC), the Reserve Bank's and ASIC powers and obligations are far stronger and more obligatory than upon the central banks in the USA and Great Britain, namely the U.S. Federal Reserve and the Bank of England.

3. Our penchant for plastic

Most of us delight in paying for goods and services with a piece of plastic because it is easier than cash and overcomes having to receive change in coins. Some prudent consumers will pay with a Debit Card where the payment is withdrawn from the Purchaser's bank account instantaneously and arrives at the Merchant's bank account usually overnight. The associated EFTPOS fee is relatively low as explained in Merchant Service Fee and Fees Levied On The Wholesale Supply Side.

A much larger group of Credit Cardholders will happily Tap&Go (PayPass), referred to as Contactless Payments, for purchases up to $100, because they receive Rewards Programs, and enjoy up to 55 days Interest Free Period, even though the Merchant may pay a hefty Interchange Fee depending on the benefits offered by the Credit Card Issuer to the Credit Cardholder.

4. Evidence that Credit Cardholders with poor Financial Literacy Capacity have been Targeted by some Credit Card Issuers and have endured Extreme Financial And Emotional Distress

Read Chapter 1 and the Reserve Bank did not recognise vulnerable Credit Cardholders with the diligence/swiftness that UK regulator, BIS, did.

Chapter 7 explains that Australian Governments allocate $43.38 million annually to 44 circa charities to provide financial counselling to predominantly Persistent Revolvers that pay 80% circa of all Interest and Penalty Fees Revenue generated from Credit Card Products.

5. The User Pays Principle is ubiquitous across the laissez faire market place for pricing goods and services, that includes the Financial Services Industry, except puzzlingly the most 'differentiated' product in the market place, namely Credit Card Products which are a minefield for Credit Cardholders with poor Financial Literacy Capacity as measured by the Productivity Commission and the ABS

User Pays Principle notes that every commercial bank lending product, except Credit Card Products, is priced on the User Pays Principle. Below is an extract of from RESERVE BANK OF AUSTRALIA - REFORM OF CREDIT CARD SCHEMES IN AUST - A Consultation Document - Dec 2001 (CHAPTER 5: PROMOTING EFFICIENCY AND COMPETITION - page 118):

"............movement towards a 'user pays' approach to credit card payment services would be consistent with the approach adopted by Australian financial institutions in pricing other payment instruments under their control. It is also fairer and efficient, because consumers only pay for what they use.”

Alas, Chapter 5 evidences that the Reserve Bank submissively abandoned its above 2001 aspirations for greater application of the User Pays Principle by Credit Cardholders' actual usage of Credit Cards.

6. The Writer has taken his concerns about the Unconscionable exploitation of a Vulnerable Cohort "to all the usual suspects", but alas nobody cares in this Christian Country

After reading SMH article

"Middle class hit by debt.....

credit cards bills are taking their toll"

(i) has subsequently expended six years, on-and-off (mainly off) researching Credit Card Products and creating a catalogue of over 500 Defined Terms and Documents - the major source has been the myriad of publications and statistics on the RBA website;

(ii) R&D'd a comprehensive Grounds/Reasons why the Shadow Minister for Revenue and Financial Services should submit Written Questions (re credit card products) to the Minister for Revenue and Financial Services during Question Time in the Lower House of Federal Parliament;

(iv) posted submissions on CDs to:

A. Reserve Bank dated 8 December 2011 imploring it to apply the User Pays Principle for using the Line/s of Credit provided by Credit Cards.

B. Submission Letter to Slater & Gordon dated 17 July 2015 B.1. (Slater & Gordon response letter dated 21 Sept 2015)

C. Intro Letter to Maurice Blackburn dated 8 May 2017

D. Submission Letter to Maurice Blackburn dated 8 May 2017

E. Second Letter to Maurice Blackburn dated 25 June 2017 E. 1. (Maurice Blackburn response letter dated 14 July 2017 ***)

F. Intro Letter to Nick Xenophon dated 17 August 2017

G. Submission Letter to Nick Xenophon dated 17 August 2017 G.1. (Response email from Nick Xenophon Team sent 1 Sept 2017)

The ten letters in (iv) above evidences why the proposed Four Corners programme is titled 'Nobody Cares in a Christian Country' because the Writer initially approached Australia's primary Financial Services regulator/Principal Regulator of the Payments System, then two Class Action law firms, then an esteemed Senator, about the unfortunate plight of many Australian Credit Cardholders with inadequate Financial Literacy Capacity that experience Numeracy And Literacy Targeting through Predatory Advertising. But the Writer "drew up blanks".

7. Labor's sought-after Royal Commission into the Financial Services Industry is bereft of any 'terms of reference'. Yet Labor asserts that the Royal Commissioners would deliver a robust written report to the Lower House of Federal Parliament within two years at a cost of $53 million - No terms of reference, yet an undertaking to deliver in two years @ $53m a robust written report from the Royal Commissioners into the Financial Services Industry is an unfortunate indictment of the capacity of the Party in Opposition, under our Two Party System, to be able to obtain requisite information

A Royal Commission into many facets of the Financial Services Industry as proposed by the Federal Labor Party, would take at least four years to table to Federal Parliament and cost several multiples of the forecast $53 million, as the Commissioners investigated 300 circa Products and Services delivered by 130 approx. large companies that employ 500,000 staff circa in the Financial Services Industry, many of which, particularly within Credit Card Products, are highly differentiated. There would be very little of 'comparing apples with apples' to determine what is "...illegal and unethical behaviour and how the financial services industry institutions understood and gave effect to their duty of care to consumers."

Merely considering the banks, there are 37 Australian-owned banks, nine foreign-owned subsidiary banks and another 35 circa branches of foreign banks that collectively provide 200 circa banking Products and Services in Australia. Looking in isolation at only one of the Four Pillars, ANZ Bank with 50,152 employees (in 2015), under 7 Divisions, delivers approx. 200 Products and Services.

Australia has had 133 Royal Commissions since 1902, but none previously with the broad scope and density of matters to examine than that announced by the Federal Labor Party in April 2016. Previous Royal Commissions have been granted both time and budget extensions. The more complexity in the warranted terms of reference, the less likely that the Royal Commission will -

(i) be cost-effective; and

(ii) achieve material improvement in 'banking behaviour' in the 'shorter term'.

No one that the Writer has written re the injustices in Credit Card Products has demonstrated any capacity to understand even the Nine Examples Of Predatory Advertising. So how could Royal Commissioners review somewhere in the order of 300 circa Products and Services delivered by 130 approx. large companies that employ 500,000 staff circa in the Financial Services Industry and table a robust written report within two years @ $53m.

8. The Writer's letter to Nick Xenophon pointed the above-mentioned flaws in the Labor Party's delivery time, workload and cost calculations

Hence, receipt of (iv) G. 1. above -

* is testimony that the Extreme Financial And Emotional Distress suffered by almost half a million Credit Cardholders with from poor Financial Literacy Capacity, referred to by the Reserve Bank as Persistent Revolvers, is also beyond the comprehension of the Xenophon Team; and

* was "the final nail in the coffin", that 'nobody cares in a Christian Country' because the Writer's considers Senator Nick Xenophon to be the most capable politician in Australia, even though his bias towards his home state occasionally appears overtly compromised.

9. The hypocrisy of Christianity in Australia

The fundamental of Christianity is 'to love they neighbour'. But with regard to Credit Cards, if a Christian can benefit financially because of deficient Financial Literacy Capacity of their Christian neighbours, then "Christian love for those neighbours goes out the window" as evidenced in Section 6 (iv) above.

(iv) A to G above evidences that -

* the Writer researched Credit Card Products and exchanged emails with Ms. Sharon van Etten, Media & Public Relations Office, Reserve Bank of Australia in Nov 2011. But after he posted CDs to Ms Etten that sought the Reserve Bank to require Credit Card Issuers to apply the User Pays Principle to Credit Card Products (as set out in Section 8 of his letter to the Reserve Bank), Ms. Etten never responded;

* the Writer sent a comprehensive submission to Maurice Blackburn in May 2017 asking it to run a Class Action representing 400,000 circa Eligible Persistent Revolver Plaintiffs that possess Financial Literacy Capacity of only Level 1 (or less) and some Level 2 (Financially Uneducated And Vulnerable Australians) against Two Of Australia's Three Financial Services Regulators for breach of their respective Statutory Duty and Fiduciary Duty; and

* Maurice Blackburn's response letter dated 14 July 2017 -

1. noted:

2. cited the High Court's decision in July 2016 in the case of Paciocco & Anor v the ANZ Bank ("ANZ") to dismiss two appeals from the Full Court of the Federal Court of Australia. Below are extracts of commentary on Paciocco & Anor v the ANZ Bank:

"The majority (by 4 votes to one) of the High Court held in the first appeal that late payment fees charged by the respondent, ANZ, on consumer credit card accounts were not unenforceable as penalties, and in the second appeal that the imposition of late payment fees did not contravene statutory prohibitions against unconscionable conduct, unjust transactions and unfair contract terms. The first appellant, Mr Paciocco, held two consumer credit card accounts with the ANZ. The terms and conditions of the accounts required Mr Paciocco, following receipt of a monthly statement of account, to pay a minimum monthly repayment. If the minimum monthly repayment plus any amount due immediately was not paid within a specified time, a late payment fee was charged. The late payment fee was $35 before December 2009, and $20 thereafter. 26 late payment fees were charged to Mr Paciocco's accounts. The majority of the High Court held that the Full Court was correct to characterise the loss provision costs, regulatory capital costs and collection costs as affecting the legitimate interests of the ANZ.

"Nettle J, in dissent, would have allowed the appeal on the common law claim on the basis that the late fee was a penalty because it was grossly disproportionate to the greatest amount of damages that would be recoverable for the breach of the monthly payment obligation (Nettle J would have left the statutory appeal unadjudicated on the merits: see [375] and [376]). Contrary to the majority, Nettle J held the appropriate penalty test from Dunlop to have been of whether the agreed sum is ‘extravagant and unconscionable’ compared to the greatest loss that could conceivably be proved following a breach of the obligations (see [317]). Consequently, Nettle J saw the late fee as payable on a breach of the obligation to pay the monthly payment on time, and thus focused on the lateness of the payment rather than a failure to pay at all (at [338]). Following this approach, Nettle J held that the primary judge was correct to reject ANZ’s arguments that the late fee covered possible costs associated with bad or doubtful debts, increased regulatory capital and collections because to a very large extent those costs were not actually incurred (see at [349]–[369]). The total cost that might have been recoverable was at most $6.90 which was ‘extravagant or otherwise out of all proportion’ to the $35 (or the eventual $20 fee) that was charged, and thus the fee was a penalty (see at [371])."

* The Xenophon Team -

(A) supports a Royal Commission into the banks and will be considering a statutory compensation scheme for victims of bad financial advice, in the wake of scandals that have engulfed the financial services sector that has destroyed the financial security of thousands of Australians; and

(B) is not interested in the plight of almost half a million Persistent Revolvers, who through no fault of their own possess poor Financial Literacy Capacity, that have been paying 40% the Lines of Credit enjoyed by 67% of Credit Cardholders, known as Transactors, for at least three years and approaching 40% before then.

10. Does "Nobody Cares in a Christian Country" appeal as a Four Corners programme?

Are the Executive Producers of Four Corners interested in -

A). assisting the economic plight of almost half a million Australian Credit Cardholders, labelled Persistent Revolvers on low incomes with poor Financial Literacy Capacity, by exposing negligence in the performance of the Statutory Duties and Fiduciary Duties of the Reserve Bank and to a lesser extent, ASIC. As detailed in (iv) D. above, the Reserve Bank's statutory obligations to the people of Australia are far more onerous than those upon the central banks in the USA or the UK, as chronicled in Section 2 and Section 3 of Extensive Powers and Responsibilities of the RBA. The Reserve Bank enjoys "...extensive powers..." whereupon it could request financial data/information from Authorised Deposit-Taking Institutions ("ADIs") which would identify if Credit Cardholders with poor Financial Literacy Capacity are paying a grossly disproportionate share of all Interest and Penalty Fees Revenue;

B). reducing the

anxiety and frustration of some

Credit Card Distress Authorities

in particular Tony Devlin at

Salvation Army's

"Moneycare" service that featured in

SMH article "Middle class hit by debt.....

credit cards bills are taking their toll"

C).

reducing the $43

million annual burden upon the Commonwealth and State

D). exposing the

considerable excesses of some

Free Riders

- income that is tax free

E

If the Writer receives a response letter, email of 'phone call that informs that someone on behalf of Four Corners has read the above highlighted documents, he will post to the Executive Producers the 'Written Questions' that he has prepared to be presented separately to Phillip Lowe and Greg Medcraft that ostensibly relate to their predecessors' ineptitude in not implementing the prescribed steps to -

(1) re-introduce a maximum interest rate on Purchases and a maximum interest rate on Cash Advances. (The maximum interest rate allowed on Credit Cards was 18% until April 1985); and

(2) price Credit Cards in closer accordance with the User Pays Principle by introducing a 'Transaction Usage Fee' and a 'Lost Card Replacement Fee'; and

(3) require ADIs to provide regular data to the Reserve Bank that identifies the quantum of Interest and Penalty Fees Revenue paid by different socio-economic cohorts for the highly differentiated Credit Card Products that they use.

NB: The

Writer

would not have undertaken his research (evident in

Defined Terms & Documents)

if Section 2 and Section 3 of

Extensive

Powers and Responsibilities of the RBA

did not establish that the

Reserve Bank

has explicit

obligations/responsibilities to

Revolvers,

whereas the

U.S. Federal Reserve and the

Bank of England do not.

ASIC

has

ignored its acknowledgement made in 2010

"That these findings

[re Financial Literacy Capacity levels identified by the Productivity

Commission and the ABS]

"....have implications for our

regulatory regime..."

Yours sincerely