Four Economic Reasons for the Campbell Committee Report – Sept 1981

"Reasons

for Change

Why did Australia move away from this system? I think there are four broad

reasons.

·

First, being heavily focused on banks, the controls were

weakening the position of banks and hampering their ability to respond to

customer needs. Banks were rapidly losing market share in the financial system;

by the early 1980s their share had fallen to 40 per cent, compared with 70 per

cent in the early 1950s.

·

Second, the controls were becoming ineffective,

as new, unregulated, intermediaries sprung up to provide finance.

·

Third, the increase in international capital flows

following the breakdown of the Bretton Woods arrangements began to

put pressure on the Australian dollar exchange rate.

The authorities could stabilise the exchange rate only by engaging in large

foreign exchange transactions, which in turn made it difficult to manage

domestic liquidity and domestic financial conditions more generally.

·

Fourth,

the financial system was quite inefficient, with wide interest spreads, little

innovation and many creditworthy potential borrowers unable to get access to

credit.

The Deregulation Process

·

virtually all controls on banks had been removed,

·

foreign banks had been allowed to enter the market; and

· the exchange rate had been floated."

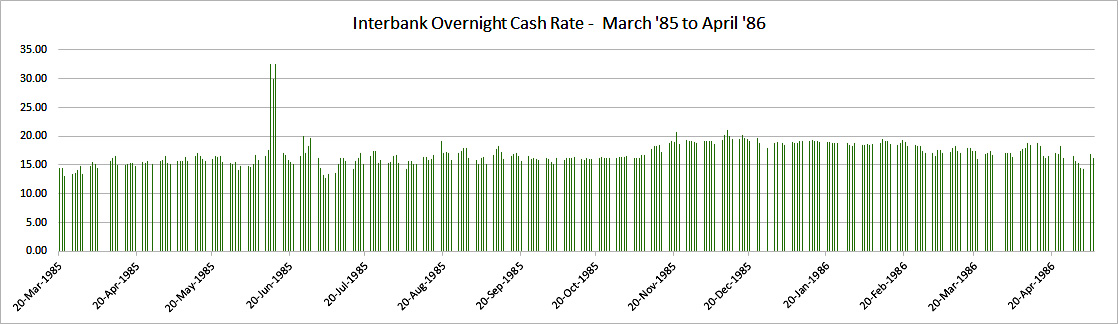

The RBA

removed the 18% cap in April 1985. Shortly after the Overnight Cash Rate

spiked fleetingly to 30% as evident in

RBA Excel file

that enabled the below graph.

Short term

rates since back in the olden days of 1900

Graph 6

The

Overnight Cash Rate is now 0.25%, but the RBA, that ruled all commercial bank

interest rates with an Iron Fist from 1959 ‘til the early 1980s, failed

to re-impose a cap in early 1990 when the difference between the Standard

Purchase Interest Rate Card and the Overnight Cash Rate

exceeded

16% in June 1992.

Refer attached Graph 6 sourced from

http://www.rba.gov.au/payments-and-infrastructure/review-of-card-payments-regulation/developments-card-payments-mkt.html

That

spread between the Standard Purchase Interest Rate Card

and the Overnight Cash Rate is now over 19%.

However,

there are several Credit Cards with a Purchase interest rate well above 20% and

a Cash Advance interest rate a lot higher still.

Latitude’s

‘Go MasterCard’ has a Purchase rate of 22.74% and a Cash Advance interest rate

of 25.90%, with an additional 3% Cash Advance fee

= 28.90%

to enjoy a Cash Advance and an annual fee of $71.40.