Writer's CD submission to RBA sent 8 Dec 2011 Defined Terms and Documents

5 Ronald Ave

Freshwater NSW 2096

0434 715.861

8 May 2017

Mr. Andrew Watson

National Head of

Class Actions

Maurice Blackburn

Level 10, 456 Lonsdale Street

Melbourne VIC 3000

(03) 9605.2735

Dear

Andrew

- (click on the zillion embedded URLs in this

Submission Letter)

Class Action representing 400,000 circa Eligible Persistent Revolver Plaintiffs that possess Financial Literacy Capacity of only Level 1 or less and some Level 2 (Financially Uneducated And Vulnerable Australians) against Two Of Australia's Three Financial Services Regulators for breach of their respective Statutory Duty and Fiduciary Duty due to Negligence under Common Law by failing a Duty of Care - in the case of -

* the Reserve Bank "to act in the public interest" to inform the Commonwealth Government (obligated under Section 11 of the Reserve Bank Act 1959) that the PSB sought [in 2.(ii) below] to adopt the User Pays Principle to Credit Cards (obligated under Section 8 of the Payments System Regulation Act 1998 and other rights/duties/obligations listed in Extensive Powers and Responsibilities of the RBA to All Australians); and

* ASIC for failing to draw upon 'Our powers' in ASIC - Our Role due to -

1. some Credit Card Issuers engaging in Numeracy And Literacy Targeting of 'Eligible Persistent Revolver Plaintiffs, with Predatory Advertising of some Credit Card Products (occasionally involving Unconscionable Conduct) that regularly charge Usurious Interest Rates, whereupon the ubiquitous User Pays Pricing Principle is uniquely absent -

* Persistent Revolvers that hold only 12.58% circa of the 16.686 million Credit Cards (held by Credit Cardholders) have suffered Extreme Financial And Emotional Distress and have contributed 80% circa of Interest and Penalty Fees Revenue to Credit Card Issuers; and

* Transactors that hold 67% circa of Credit Cards receive a Free Ride enjoying their Revolving Lines of Credit to take receipt, but not pay for their Purchases, for up to 55 days later, many enjoy Rewards Programs tax free

2. Reserve Bank published LOAN RATE STICKINESS: THEORY AND EVIDENCE in June 1992; yet incongruously over the subsequent 25 years the RBA has failed (as obligated under Section 11 of the Reserve Bank Act 1959) to inform the Commonwealth Government that -

A. the spread between Credit Card Issuers' Wholesale Cost Of Funds has increased from less than 1% in April 1985 (when the Reserve Bank removed the 18% cap on the maximum Credit Card interest rate) to the current spread of 18.5% (Overnight Cash Rate of 1.5% and the Credit Card Purchase Interest Rate of 20%) [max Cash Advance interest rate in April 2017 is 29.49% representing a spread of 26.49% after Latitude Financial's cost of funds]; and

B. the Reserve Bank deems it necessary to re-introduce a cap on the maximum -

* Purchase Interest Rate of 12% circa above the Overnight Cash Rate; and

* Cash Advance interest rate of 15% circa above the Overnight Cash Rate - refer Low Interest Rate Credit Cards - at March 2017,

because of the RBA's findings in -

(i) LOAN RATE STICKINESS: THEORY AND EVIDENCE - June 1992 that noted that credit card interest rates did not reduce in line with the Overnight Cash Rate

(ii) Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001 evidences that Reserve Bank wanted to move ".....towards a 'user pays' approach to credit card payment services....”

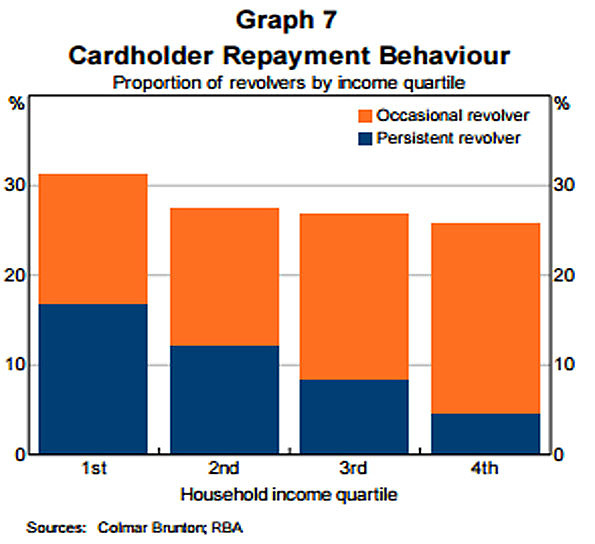

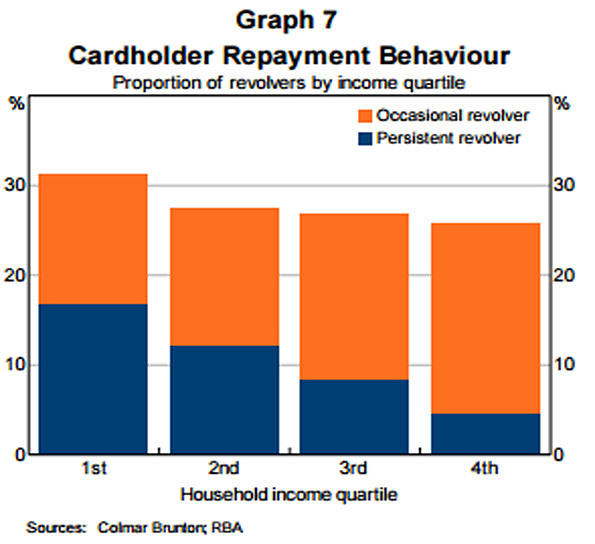

(iii) Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - Aug 2015 in Graph 7 titled ''Cardholder Payment Behaviour" re the gross interest burden upon Persistent Revolvers [and earlier similar RBA findings noted in Persistent Revolvers and Revolvers] that possess very low Financial Literacy Capacity and fall within Financially Uneducated And Vulnerable Australians

{kind=link}

2. Reserve Bank has failed to draw upon its Extensive Powers and Responsibilities to (All) Australians to require major Credit Card Issuers (Four Pillars ) to provide financial information for Credit Card Products that identify cohort/s of Credit Cardholders that have paid an excessive burden of Interest And Late Payments Fees (Chapter 9 and Question 9), even after the Reserve Bank identified the material Outstanding Indebtedness carried by Persistent Revolvers (in Aug 2015), whilst 67% circa of Credit Cardholders Transactors enjoy a Free Ride with their Revolving Lines of Credit

3. Reserve Bank has abrogated its charter/mandate/role to "........best contribute to........the economic prosperity and welfare of ALL the people of Australia"

4. Australia's "... principal regulator of the payments system ..." has failed to impose a 'Standard', pursuant to Division 4, Section 18 of the Payments System Regulation Act 1998, upon Credit Card Issuers to ensure some Credit Cardholders that are suffering Extreme Financial And Emotional Distress are not issued additional Credit Cards evident in Quotes from reputable authorities about unconscionable advertising of Credit Cards by Credit Card Issuers resulting in some indebted Credit Cardholders being issued multiple Credit Cards?

5. ASIC Has Ignored Its Acknowledgement Made in 2010 "That these findings [re Financial Literacy Capacity levels identified by the Productivity Commission and the ABS] "....have implications for our regulatory regime..."

6. Labyrinth of ‘Concealed Spiders' provides nine examples of Unconscionable Conduct by Credit Card Issuers in Predatory Advertising their various Credit Card Products to extricate maximum Interest and Penalty Fees Revenue from Financially Uneducated Credit Cardholders which constitutes Numeracy And Literacy Targeting - also acknowledged in Quotes from reputable Credit Card Distress Authorities about unconscionable advertising of some Credit Cards by some Credit Card Issuers resulting in some indebted Credit Cardholders being issued multiple Credit Cards

RBA's Copious Publications on Credit Cards are bereft of any mention whatsoever of protecting "vulnerable consumers" or "at risk consumers", whereas the UK regulator regularly makes specific mention of providing "real help for vulnerable consumers" (and similar) in its published reports

Does the Reserve Bank consider that all Credit Cardholders possess the same Numeracy and Literacy Capacity?

Or does it assume 'caveat emptor'?

Other contributing Australian interested parties recognise protecting

'vulnerable consumers', but not the RBA

Productivity Commission and ABS have published several detailed reports about the divergent Numeracy and Literacy Capacity across the Australian population (Chapter 1)

Reserve Bank continually failing to recognise (in its Copious Publications on Credit Cards) 'vulnerable' or 'at risk' Credit Cardholders (with only low Financial Literacy Capacity) evidences breach of its Statutory Duty and Fiduciary Duty to Persistent Revolvers

Joint Media Release "Getting a Better Deal on Credit Cards and Mortgages" issued on 5 July 2011 evidences that RBA plagiarized (from UK BIS) the metaphor "Getting a Better Deal" - first used in BIS report (to the UK Parliament) dated 5 July 2009 titled "A Better Deal for Consumers - Delivering Real Help Now and Change for the Future"

7(a). RBA breached it Extensive Responsibilities to Persistent Revolvers by taking 12 years circa to 'stamp out' five ploys of Unconscionable Conduct listed in Joint Media Release "Getting a Better Deal on Credit Cards and Mortgages" that initially surfaced in the USA, migrated to the UK and onto Australia - 18 months slower than the UK Regulator

8. Credit Card Issuers have since conjured up more Predatory Advertising to Target Credit Cardholders With Low Financial Literacy Capacity that continued unchecked by Two Of Australia's Three Financial Services Regulators

User Pays Principle notes that every commercial bank lending product, except Credit Card Products, is priced on the User Pays Principle as the Reserve Bank acknowledged in 2001 "movement towards a 'user pays' approach to credit card payment services would be consistent with the approach adopted by Australian financial institutions in pricing other payment instruments under their control. It is also fairer and efficient, because consumers only pay for what they use.”

The definition of User Pays Principle notes that -

* every commercial bank lending product, except Credit Card Products, is priced on the User Pays Principle

* in 2001, the Reserve Bank released "RBA's Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001 that announced:

towards a 'user pays' approach to credit card payment services would be consistent with the approach adopted by Australian financial institutions in pricing other payment instruments under their control. It is also fairer and efficient, because consumers only pay for what they use.”"Reform of credit card schemes will also have a direct impact on credit cardholders and is likely to result in some re-pricing of credit card payment services. However, this is the means by which the price mechanism is to be given greater rein in the credit card market. A movement

* Chapter 5 evidences that the Reserve Bank abandoned its 2001 aspirations for the User Pays Principle -

° detriment of Persistent Revolvers; and

° benefit of Transactors who enjoy a Free Ride

* Reserve Bank of Australia - 'Our Role' notes: "To that end, it recommended the establishment of the Payments System Board at the Reserve Bank with the responsibility and powers to promote greater competition, efficiency and stability in the payments system."

Since the above-mentioned RBA publication in 2001, the Reserve Bank has not used its Extensive Powers and Responsibilities to ALL Australians to move "towards a 'user pays' approach to credit card payment services and promote greater competition and efficiency in the pricing structure that Credit Card Issuers apply to recoup their costs and achieve a profit for providing Credit Card Products because -

(i) the margin between the cost of funds and the maximum Cash Advance interest rate has increased from less than 1% when Reserve Bank removed the 18% cap on Credit Card interest rates in April 1985 up to 18.5% [Cash Rate of 1.5% and the RBA's nominated ave. Credit Card Purchase Interest Rate of 20%] whilst the "principal regulator of the payments system" has 'sat on its hands'; and

(ii) Reserve Bank has ignored its own published evidence -

(a) of the huge interest burden upon Revolvers provided in Persistent Revolvers; and

(b) that "the main regulations established by the credit card schemes in Australia do not meet the public interest test" - extracted in User Pays Principle

The Reserve Bank has failed (as obligated under Section 11 of the Reserve Bank Act 1959) to inform the Commonwealth Government that -

(A) RBA has failed to Determine Standards to ensure that the User Pays Principle had been applied to Credit Card Products; and

(B) as a result the 12.58% circa of Credit Cards owned by Persistent Revolvers have paid 80% circa of all Interest and Penalty Fees Revenue paid to Credit Card Issuers, with Occasional Revolvers paying the remaining 20%, whilst Transactors (that own 67% circa of the 16.686 million Credit Cards on issue in Australia) enjoy a Free Ride.

The Reserve Bank published a 'Research Discussion Paper' LOAN RATE STICKINESS: THEORY AND EVIDENCE in June 1992 that the current Governor of the Reserve Bank, Phillip Lowe, and colleague, Thomas Rohling, wrote. It investigated whether movements in the Cash Rate were reflected in commensurate movements in loan and investment rates. It found that:

A. Increases in the Cash Rate were passed on relatively quickly (un-sticky).

B. Reductions in the Cash Rate were not passed on with lower Credit Card interest rates (sticky).

Mid way down Chapter 5 notes that:

* Seven years after the 18% interest rate cap was removed, namely in June 1992 when Phillip Lowe co-wrote LOAN RATE STICKINESS: THEORY AND EVIDENCE, the spread between the then Cash Rate of 6.50% and the Credit Card Purchase Interest Rate of 23% was 16.5% (Cash Advance interest rates are often appreciably higher).

* 32 years after 1985, in April 2017, the spread between the Cash Rate of 1.5% and the Credit Card Purchase Interest Rate of 20% is 18.5%. (As at April 2017, the highest Purchase interest rate is 25.9% from "Lombard Visa Card Classic". The highest Cash Advance interest rate is 29.49% from G.E. Money's "Go MasterCard").

The Reserve Bank has failed to re-regulate a max Credit Card interest rate/s during the 25 years since LOAN RATE STICKINESS: THEORY AND EVIDENCE was published in June 1992, notwithstanding that -

(a)

Persistent Revolvers

(discussed in

Chapter 5

and

Chapter 20)

that hold

12.58% circa of the

16.686 million Credit Cards held by

Credit

Cardholders)

[which includes 400,000

circa

Eligible Persistent Revolver Plaintiffs with Level 1 or less

Financial Literacy

Capacity]

that are

Financially Uneducated And Vulnerable Australians

and

have suffered

Extreme Financial And Emotional Distress

and contributed 80% circa of

Interest and Penalty Fees Revenue

to

Credit

Card Issuers

of which 80% of all

Revenues

to

Credit

Card Issuers

from

Credit

Card Products

is

Interest and Penalty Fees Revenue, while

Transactors

continue to enjoy

a

Free Ride

for their

Revolving Lines of Credit

- not 'physically' pay for their

Purchases for

up to 55 days after receipt.

{kind=link}

Section 5.2 'Scheme regulations and competition benchmarks' of "RBA's Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001 (Chapter 5) merited the User Pays Principle: - page 116 to "...meet the public interest test ...." because "It is also fairer and efficient, because consumers only pay for what they use” as explained in User Pays Principle;

(b) for most of the 55+ years existence of Credit Cards, the Credit Cardholder paid Interest on that part of the Total Amount Owing that was not repaid by the Payment Due Date. If the Total Amount Owing was $500 and the Credit Cardholder repaid $400 by the Payment Due Date, the Credit Cardholder paid Interest on the $100 until the remaining $100 was repaid. And then the Interest Free Period was re-instated. Almost all Credit Card Issuers have moved from the former interest charging model of charging interest on any shortfall until repaid, to charging Interest on all Purchases if the Total Amount Owing is not repaid by the Payment Due Date, even if the payment was 'a dollar short or a day late'. Some Credit Cards also cancel the Interest Free Period for up to two subsequent months, if the Total Amount Owing is not paid by the Payment Due Date, which means that if a Credit Cardholder failed to pay the Total Amount Owing in the third month, he/she could forfeit their Interest Free Period for five months; many Financially Uneducated And Vulnerable Credit Cardholders have so forfeited - see Example 1. Credit Cardholders with poor Financial Literacy Capacity are much more prone to Forfeit Interest Free Period And Pay Interest On Each Purchase From The Purchase Date which can spiral into accelerating Outstanding Indebtedness and Extreme Financial And Emotional Distress; this Spider is invariably not noted in advertisements, nor included in the Key Facts Sheet, rather concealed in the Terms & Conditions document up to 90 pages in tiny 9 font in dark grey text - see Example 1:

(c) the Reserve Bank is aware -

(i) of detailed written reports by the Productivity Commission, ABS and ASIC (that date back to 2006) re the material disparity in Financial Literacy Capacity across Credit Cardholders (Chapter 1);

(ii) that Federal and State Govt's allocate $43.38 million annually to 44 Australian charities to provide 500 circa financial counselling to Australians that are experiencing Extreme Financial And Emotional Distress where the vast majority of those counseled are Credit Cardholders with poor Financial Literacy Capacity (Chapter 7);

(iv) Newspaper articles re Credit Card debt, Usurious Interest Rates and Compulsive Buying Disorder.

Persistent Revolvers Extreme Financial And Emotional Distress and foregone productivity is -

(A) seen by Credit Card Distress Authorities day-in and day-out (Chapter 7); and

(B) felt by the Dept of Social Services that pays fortnightly pension support for Credit Cardholders that are no longer capable of "going to work" which according to the Federal Minister for Social Services, Christian Porter, at an address to the National Press Gallery on 20 Sept 2016 are often funded for many, many years

ASIC Has Ignored Its Acknowledgement Made in 2010 "That these findings [re financial literacy 5 levels] "....have implications for our regulatory regime,... "....which relies upon disclosure as a critical element of our consumer protection system."

Over recent months, the Writer has assembled a welter of evidence in software files (in a structured file index) of:

* Reserve Bank's stringent regulation of commercial bank lending and deposit interest rates prior to the 1980s - relying on Section 50 of the Banking Act 1959 (Chapter 17)

*

Reserve Bank's

Payment Systems

Board enjoys 'extensive powers'

(Chapter 9)

and (Chapter

16) to -

- request any financial information from

Australia's commercial banks - relying on the

Payment Systems (Regulation)

Act 1998; or

-

set caps on deposit and loan interest rates - relying on

Clause (1)(a) of

Section 50

of the

Banking Act 1959

* annual financial reporting for last 26 years by the U.S. Fed. Reserve to the U.S. Congress on 'Profitability of Credit Card Operations of large U.S. Credit Card banks'

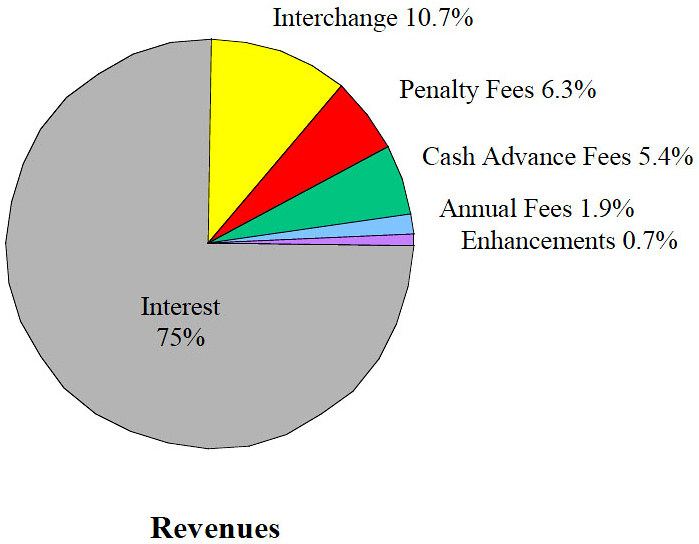

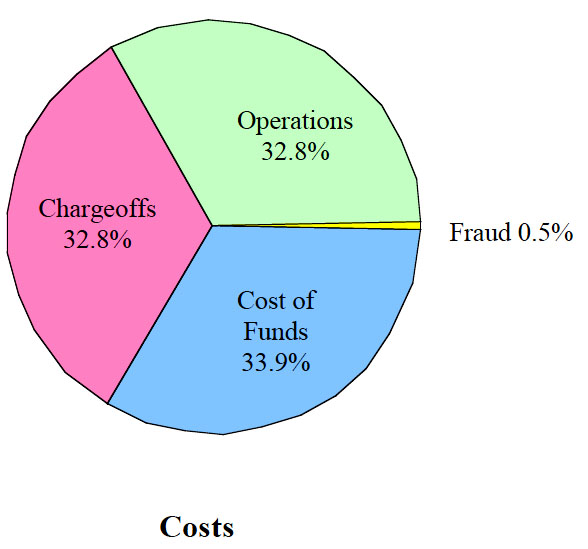

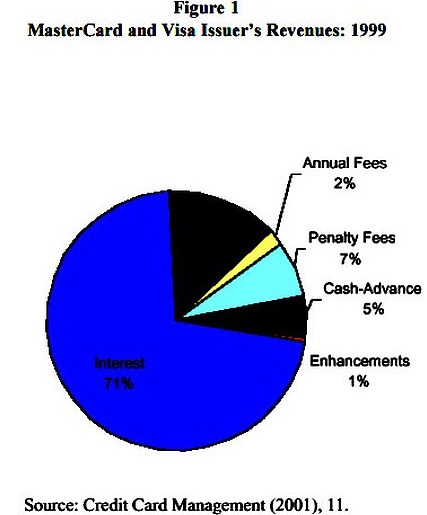

* a

pie chart

for 'Costs' and a

pie chart for Revenues of U.S. MasterCard and Visa

Credit

Card Issuers (in

Chapter 8) that display:

-

Interest And Penalty Fees Revenue exceed 80%

of 'Revenues';

{kind=link}

-

Interchange Fees (charged on every

Credit Card transaction to

Merchants) accrue only 10.7% of 'Revenues'; and

-

Annual Cardholder Fees accounts for

less than 2% of 'Revenues'

{kind=link}

* Unconscionable Conduct (misleading and deceptive conduct, Predatory Advertising) by some Credit Card Issuers - Chapter 3, Chapter 7 and Chapter 20

The Writer has prepared 1. and 2. below which evidence that the Reserve Bank has breached its Statutory Duty and Fiduciary Duty through Negligence under Common Law by failing a Duty of Care "to act in the public interest" by drawing upon its extensive powers to seek meaningful financial information to establish, inter alia, which cohorts of Credit Cardholders are paying "The Lion's Share" of Interest And Penalty Fees Revenue:

1. Written Questions (re Credit Card Products) that the Shadow Minister for Revenue and Financial Services could submit to the Minister for Revenue and Financial Services during Question Time in the Lower House of Federal Parliament - that evidences negligence by the Reserve Bank not relying upon its extensive powers under the Payment Systems Regulation Act 1998 to ask commercial banks for a broad range of financial information to identify -

(A) how much of Interest And Penalty Fees Revenue is being born by Persistent Revolvers; and

(B) what percentage of the 16.686 million Credit Cards are held by Persistent Revolvers.

2. Grounds/Reasons explain why the Shadow Minister for Revenue and Financial Services should submit Written Questions (re credit card products) to the Minister for Revenue and Financial Services during Question Time in the Lower House of Federal Parliament - contains many graphs and tables primarily draw from RBA website - which expose the Reserve Bank for maintaining the below statistical information 'of no material use' re Credit Cards and Charge Cards, but it fails to seek financial information from Credit Card Issuers that establishes that Revolvers -

(A) are paying 100% circa of all Interest And Penalty Fees Revenue; and

(B) the 37.25% of Revolvers that are Persistent Revolvers are paying 89% of Credit Cardholders' Contribution To Credit Card Issuers' Gross Revenue:

Determine Standards to 'inter alia' re-cap Credit Card interest rates for 'public interest issues' debunks Ms. van Etten's Media & Public relations, RBA, email sent 10 Nov 2011 to the Writer that noted: "The Payments System Board of the Reserve Bank has no regulatory power over these aspects of credit cards", because the Reserve Bank could have determined Standards (obligated under Section 8 of the Payments System Regulation Act 1998 and other rights/duties/obligations listed in Extensive Powers and Responsibilities of the RBA) to re-introduce a cap/s over Credit Card interest rates, by according with Section 11 of the Reserve Bank Act 1959, any time it wanted to since the Reserve Bank published LOAN RATE STICKINESS: THEORY AND EVIDENCE in June 1992.

Below is an extract from Media Release "Designation of Credit Card Schemes in Australia" issued 12 April 2001:

"The Bank will now proceed to establish, in the public interest, standards for the setting of interchange fees and a regime for access to the credit card systems. However, the standards will not cover the setting of credit card fees and charges to cardholders and merchants, or interest rates on credit card borrowings."

Australia's central bank, with a Board that has been given the backing of strong regulatory powers, unique among central banks, could have Determined Standards to re-impose a maximum interest rate on Credit Cards, or a maximum interest rate for Purchases and a maximum interest rate for Cash Advance, at any time that it wanted to.

===========================================

1. Earlier correspondence with the RBA - emails and the Writer's Letter to RBA dated 8 Dec 2011:

A.

After a few civil emails with

Sharon van Etten

The Writer's letter to the RBA dated 8 Dec 2011 -

(A) provided 'Print Screen' evidence of Numeracy And Literacy Targeting in Credit Card web advertisements of Predatory Advertising; and

(B) implored (in his Section 8) that the RBA take stringent action to ensure that Credit Card Products follow the User Pays Principle by introducing new usage fees (for all users) because 'Unlucky' Revolvers (very low Financial Literacy Capacity as measured by the Productivity Commission, ABS and ASIC) [described in RBA Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - Aug 2015 as Persistent Revolvers], were paying for the Revolving Line/s Of Credit of 'Lucky' Transactors' (high Financial Literacy Skills) that incongruously enjoy a Free Ride because no other product or service, either provided by the Financial Services sector, or the broader 'supply market', provides their goods or service 'gratis' to some, but not others.

Section 8 of the Writer's letter to the RBA dated 8 Dec 2011 set out eight specific actions for the RBA to employ the User Pays Principle to Credit Card Products. The Writer posted a further 3 CDs on 16 Dec '11 and a final 3 CDs on 20 Dec '11 which contained minor embellishments/clarifications to his initial letter to the RBA dated 8 Dec 2011. He confirmed posting his two additional sets of 3 CDs on 16 Dec '11 and 21 Dec '11 to Sharon van Etten in his emails to with RBAInfo sent 16 Dec 2011 and 20 Dec '11.

ASIC website says:

"You should report misconduct to the relevant government agency that is primarily responsible for the conduct."

The RBA did not respond to his above letter (on CD) or his emails. But the RBA was informed (by the Writer) of the need to regulate to apply the User Pays Principle because of the material financial detriment to the 12.58% circa of Credit Cardholders that are Persistent Revolvers that are contributing 80% circa of all Interest And Penalty Fees Revenue.

B. On 17 July 2015, the Writer posted a couple of CDs to Slater & Gordon which auto opened at his Introductory Letter to Slater and Gordon dated 17 July 2015 which asked James Higgins to review the Writer's Submission Letter to Slater and Gordon dated 17 July 2015 which sought S&G to launch a Class Action on behalf of Eligible Plaintiffs:

* Financially Uneducated And Vulnerable Australians with poor Financial Literacy Skills - identified in Productivity Commission and ABS published reports; and

* Suffered Numeracy And Literacy Discrimination and paid Material Interest And Fees (ie. more than $5,000 in any continuous three year period).

Slater & Gordon's Response Letter dated 21 Sept 2015 (9 week's later) declined my invitation to launch a Class Action on behalf of Eligible Plaintiffs.

The Writer's Introductory Letter to Slater and Gordon dated 17 July 2015 and his more comprehensive Submission Letter to S & G also dated 17 July 2015 contained about 20% of the evidence that this Submission Letter to Maurice Blackburn contains, as evidenced by Additional Humdinger Evidence of breach of Statutory Duty and Fiduciary Duty that the Writer has garnered in last three months to May 2017.

============================================

2. Issues to warrant/justify a Class Action against the Reserve Bank and ASIC for breach of their respective Statutory Duty and Fiduciary Duty to Persistent Revolvers, that represent a majority portion of Financially Uneducated And Vulnerable Australians, with, through no fault of their own, possess very low Financial Literacy Capacity ("nearly half of the population were assessed at either levels 1 (the lowest level) or 2, both of which are below the minimum level deemed necessary to participate in a knowledge-based economy (level 3)" - Level 5 is the highest level

A. Reasons for de-regulation of the commercial banks from 1980 - after over 100 years of regulation due to regular commercial bank collapses

In the 1970s, the NBFIs stared attracting large depositors' balances away from the banks due to NBFIs not being capped at 3¾% on savings accounts and 6½% on savings investment accounts. The commercial banks started whinging to the Reserve Bank that NBFIs should be similarly regulated.

The Initial Reaction by the Reserve Bank and other regulators was to seek to impose (upon the NBFIs) the same interest rate caps that were regulated upon the commercial banks because of -

(i) the long history of financial collapses in the 19th Century and early 20th century; and

(ii) the collapses of Mainline, Cambridge Credit and Associated Securities, plus ANZ bailing out FCA by taking over Associated Securities.

Between 1983 and 1985 Treasurer, Paul Keating, deregulated the financial system by -

(a) floating the Australian dollar in December 1983;

(b) granting 40 new foreign exchange licences in June 1984; and

(c) granting 16 banking licences to 16 foreign banks in February 1985.

The Campbell Committee's recommendation to de-regulate (from 1980) interest rates imposed upon Australia's commercial banks, due to stiff (higher deposit interest rate) competition from the NBFIs, was heavily influenced by powerful bank lobbying seeking to better compete against the burgeoning NBFIs.

Below is an extract from RBA has done naught to require Credit Card Issuers to lower interest rates in line with the fall in the Cash Rate:

"Below is a quotation from Westpac's submission to the Wallis Inquiry, submitted by former CEO, Bob Joss. The Writer's investigations suggest that the Wallis Inquiry did not adopt Westpac's prudent recommendation in either its Discussion Paper - Released Nov 1996. Or its Final Report - Released March 1997):

"Protection of consumers

On-going monitoring of credit card pricing in anticipation of a substantial inquiry into the effects on consumers of the deregulation of credit card interest rates."

The RBA seems to have ignored then Westpac CEO, Bob Joss' above recommendation to the Wallis Inquiry for "On-going monitoring of credit card pricing in anticipation of a substantial inquiry into the effects on consumers of the deregulation of credit card interest rates".

The below extract from Summary of Part Two: Key Issues in Regulatory Reform from The Wallis Report on the Australian Financial System: Summary and Critique 'sugar coats' the reasons:

Below is an extract from 'Overview of Financial Services Post-Deregulation' by (Dr) Diana Beal, Director, Centre for Australian Financial Institutions, University of Southern Queensland, Toowoomba:

"Interest-rate ceilings on deposit accounts restricted the banks’ ability to attract funds particularly during the 1970s when inflation was rampant. In the June quarter of 1975, inflation rose to 16.9% pa. At the same time, interest payable on amounts held in savings accounts offered by savings banks, for example, was restricted to 3.75% (by RBA regulation) from 1969 to 1980 (Foster, 1996). In contrast, the interest rates offered by non-bank financial institutions (NBFIs) were not controlled and they were able to pay around 10% on passbook accounts."

"Banks in 1980 still operated in a highly regulated environment which was an artefact of previous economic and social conditions. Indeed, an extensive collection of controls remained from regulation introduced under the National Security Regulations in 1941."

Below are extracts from Eligible Plaintiffs Seek Compensatory Damages From RBA and ASIC:

"Between 1960 and 1980 the RBA took a pro-active role in regulating commercial bank interest rates. The purpose of regulation (until 1980) was "......... to achieve monetary policy, public sector financing and sectoral assistance objectives.....".

By regulation, the RBA fixed the maximum interest rate that Australian banks could pay on passbook savings account at 3.75% from 1969 until 1980**.

===========================================

B. Precedent to re-regulate after deregulation exposed flaws

Below is an extract from Consumer Affairs Victoria - Regulating the cost of credit which evidences that in the past if de-regulation did not achieve the desired results, then re-regulation followed. But not with regard to re-introducing a max interest rate cap/s on Credit Cards, notwithstanding that the spread between the current Cash Rate of 1.5% and the Credit Card Purchase Interest Rate of 20% is 18.5%. (As at April 2017, the highest Purchase interest rate is 25.9% from "Lombard Visa Card Classic

" and the highest Cash Advance interest rate is 29.49% from G.E. Money's "Go Mastercard"):"The tide of utilitarianism rose slowly, and a lengthy campaign was necessary before the financial deregulation of 1854, which abolished the British interest rate cap. However, one act of deregulation cannot quell an argument that has been going on for millennia. Over the following century the tide gradually turned towards re-regulation, culminating with detailed requirements imposed on the financial sector (particularly the banks) during and immediately after the Second World War. We now trace the gradual lead-up to this second phase of regulation."

===========================================

"Obviously this is a pretty radical act, and it will be fought," he replied. "But I think the American people are disgusted with the financial industry. They want change.

You could argue that an interest rate of 15% or 18% is more than enough to accommodate any amount of risk on the lender's part. If a loan appears riskier than that, don't make it.

What we have to ask as a nation is whether it's ethical to charge people 30% interest rates," Sanders said. "This is loan sharking. Let's call it what it is."

===========================================

C. What has Australia's "... principal regulator of the payments system ..." done about some Credit Cardholders that are suffering Extreme Financial And Emotional Distress being issued numerous Credit Cards as evidenced in:

* Credit Card Distress Authorities

Chapter 7 details Financial Counsellors evidence first-hand "the worst financial scams and unscrupulous market conduct in the country" (Predatory Advertising) on a daily basis within some web and newspaper advertisements for Credit Card Products that have patently proved very costly for Credit Cardholders with poor Financial Literacy Capacity.

"Typically, they may start with one card and when they reach the limit on that card, they get a second card and a third card and so on," she said. "They end up just shuffling the debts around while the interest compounds, leaving them in unmanageable debt."

"We have had cases of people who have accrued debts of $100,000 or $200,000 on multiple cards - that is the worst case scenario," she said.

Question 3 behoves Federal and State Govt's that fund $43m annually to 44 charities/community organisations across Australia to pay the salaries of 500 circa Financial Counsellors -

* to obtain from senior Financial Counsellors descriptions of misleading, deceptive or Unconscionable Credit Card advertisements (Labyrinth of ‘Concealed Spiders’); and

* pass those descriptions onto Australia's Three Financial Regulators that should ensure that those offending Credit Card Issuers are harshly fined.

===========================================

The Australian govt. website, "The strength of Australia’s financial sector" boasts that "The four major banks ........... are also some of the most profitable in the world." This submission presents one of the material reasons why the Four Pillars are so profitable ie. because two of Australia's Three Financial Services Regulators have abrogated their statutory appointed mandates to the detriment of many of those Australian people that are not shareholders.

{kind=link}

===========================================

D. Further evidence of RBA's Negligence under Common Law by failing a Duty of Care "to act in the public interest" to re-set a max Credit Card interest rate/s after it published in 1992 "LOAN RATE STICKINESS: THEORY AND EVIDENCE" that evidenced a material drop in the cost of funds, yet Credit Card Issuers had failed to lower Credit Card interest rates

Credit Cardholders' Contribution To Credit Card Issuers' Gross Revenue evidences that the Pareto Principle has been 'blown away' because 12.58% circa of Credit Cards (not 20%), are owned by Persistent Revolvers (identified in RBA Graph 7 "Cardholder Payment Behaviour" in RBA report RBA Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - Aug 2015) that pay 80% circa of Interest and Penalty Fees Revenue (remaining 20% is paid by Occasional Revolvers). Interest and Penalty Fees Revenue represent 80% of Credit Card Issuer Gross Revenue. After removing Merchant Service Fees from Credit Card Issuer Gross Revenue, Interest and Penalty Fees Revenue accounts for 89% circa of Credit Cardholders' Contribution To Credit Card Issuers' Gross Revenue. Hence, Persistent Revolvers contribute 89% circa of Credit Cardholders' Contribution To Credit Card Issuers' Gross Revenue.

{kind=link}

{kind=link}

===================

The present Governor of the Reserve Bank, Phillip Lowe, in LOAN RATE STICKINESS: THEORY AND EVIDENCE (June 1992) identified 25 years ago that:

-

"The rate on credit cards is found to be the most sticky, followed by personal loan rates, the housing loan rate and the small business overdraft rate.

-

In contrast, the rates on personal loans and credit cards do not appear to be more flexible in the deregulated period."

===================

The definition Extensive Powers and Responsibilities of the RBA notes at Section 2:

"The Board has been given the backing of strong regulatory powers, unique among central banks. At the same time, the Government has indicated its preference for a co-regulatory approach and it has balanced the Board's powers with safeguards for private-sector operators."

The Reserve Bank is the principal regulator of the payments system through the PSB."

Section 2 and Section 3 of 'Extensive Powers and Responsibilities of the RBA' evidences that the Reserve Bank of Australia has explicit obligations/responsibilities to Revolvers, whereas the U.S. Federal Reserve or the Bank of England does not.

===================

RBA's Copious Publications on Credit Cards are bereft of any mention whatsoever of protecting "vulnerable consumers" or "at risk consumers", whereas the UK regulator regularly makes specific mention of providing "real help for vulnerable consumers" (and similar) in its published reports

Does the Reserve Bank consider that all Credit Cardholders possess the same Numeracy and Literacy Capacity?

Or does it assume 'caveat emptor'?

Productivity Commission and ABS have published several detailed reports about the divergent Numeracy and Literacy Capacity across the Australian population (Chapter 1)

Reserve Bank continually failing to recognise in its Copious Publications on Credit Cards) 'vulnerable' or 'at risk' Credit Cardholders (with only low Financial Literacy Capacity) evidences breach of its Statutory Duty and Fiduciary Duty to Persistent Revolvers

Joint Media Release "Getting a Better Deal on Credit Cards and Mortgages" issued on 5 July 2011 evidences that RBA plagiarized (from UK BIS) the metaphor "Getting a Better Deal" - first used in BIS report (to the UK Parliament) dated 5 July 2009 titled "A Better Deal for Consumers - Delivering Real Help Now and Change for the Future"

RBA breached it Extensive Responsibilities to Persistent Revolvers by taking 12 years circa to 'stamp out' five ploys of Unconscionable Conduct listed in Joint Media Release "Getting a Better Deal on Credit Cards and Mortgages" that initially surfaced in the USA, migrated to the UK and onto Australia - 18 months slower than the UK Regulator

===================

Dr. H C "Nugget" Coombs below mentioned "friend" was a visionary because Nugget's below quote was made well prior to the maize of corporate and regulatory re-structures more recently sanctioned by Australia's senior banking regulator, the RBA, to defray its legislative responsibility considered in Parliamentary Bestowed Mandate, as evidenced in Question 4 and Grounds for Question 4 which challenges the -

(A) integrity of Dr. Malcolm Edey (now retired from the RBA); and

(B) the financial acumen of the Senate Economics Reference Committee:

"The brilliant, blunt Governor of the Reserve Bank of Australia between 1949-1968, Dr H.C. Coombs, famously recalled that, when he was trying to explain the complexities of central banking to a friend, the friend replied:

‘Come the Revolution, you will be hanged as high as the rest, but as they bear you off to the nearest lamp post, you will be crying plaintively, “But I am a CENTRAL banker!”

(quoted from Fast Money 2, Edna Carew, Allen & Unwin, 1985, page 46).

===========================================

E. RESERVE BANK ACT 1959 - SECT 11 sets out the 'modus operandi' that the Reserve Bank and the PSB must abide by to inform its financial policy to the Federal Govt. and that the Grosvenor General has the 'final call' on any Reserve Bank and the PSB 'financial policy' that the Federal Govt. does not believe "is directed to the greatest advantage of the people of Australia".

Monetary policy framework - Australian Treasury notes:

"Independence

The Reserve Bank Act 1959 provides for the independence of the Reserve Bank. This is restated in the Statement on the Conduct of Monetary Policy of August 1996.

Section 11 of the Reserve Bank Act 1959 (Differences of opinion with Government on questions of policy) prescribes procedures for the resolution of policy differences between the Reserve Bank and the Government. In the event of a material difference in opinion, these provisions allow the Government to determine policy. However, the procedures underlying such provisions are politically demanding and their nature is designed to reinforce the Reserve Bank's independence. These provisions have never been used.

In addressing the Reserve Bank's responsibility for monetary policy, the Reserve Bank Act 1959 also provides that the Reserve Bank Board shall, from time to time, inform the Government of the Bank's policy. Such arrangements are a common and valuable feature of institutional systems in other industrial countries with independent central banks and recognise the importance of macroeconomic policy coordination."

===========================================

F. Some Papers/Articles on Statutory Duty and litigation that do not seem to preclude this proposed Class Action.

===========================================

Should you approach IMF Bentham, or another litigation funder, please inform it of the existence of evidence II, III, IV and V (listed in the penultimate paragraph of the Intro Letter to Maurice Blackburn) that was not provided in the Submission Letter to Slater & Gordon dated 17 July 2015, because the Writer had not yet sourced that evidence.

Yours sincerely

Philip J. Johnston

aka

Bank

Teller