|

|

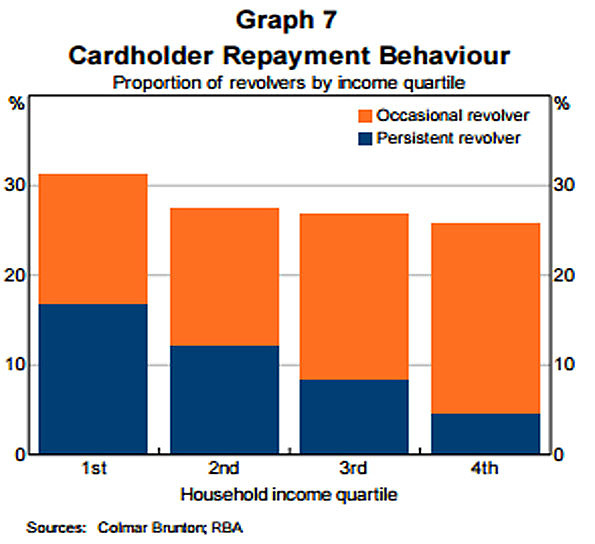

Eligible Persistent Revolver Plaintiffs: (1.) 400,000 circa Credit Cardholders across Australia, first identified as Persistent Revolvers by the Reserve Bank of Australia in RBA Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - Aug 2015 in Graph 7 titled ''Cardholder Payment Behaviour" (2.) are drawn from those Persistent Revolvers that - a) have been issued with four or more Credit Cards by Credit Card Issuers singularly (or five or more Credit Cards if a couple that are in a 'living together' relationship); b) have paid in excess of $20,000 in Interest and Penalty Fees (that were charged at Usurious Interest Rates) to Credit Card Issuers over a continuous nine years period at an average Comparison Rate Over 18% Per Annum; c) were misled by Predatory Advertising Targeted At Credit Cardholders With Low Financial Literacy Capacity where such Predatory Advertisements constitute Unconscionable Conduct; d) have suffered Extreme Financial And Emotional Distress; and e) possess poor Financial Literacy Capacity (predominantly Level 1 or below, and some Level 2) as - (i) identified and quantified by the Productivity Commission, the ABS and ASIC separate written reports (Chapter 1); and (ii) evidenced on a daily basis by 500 circa Financial Counsellors employed by 44 charities/community organisations that collectively receive $43 million annually from the Commonwealth Govt. ($20m) and the State Govts ($23m) via Financial Counselling Australia (Chapter 7). Of the Four Types of Revolvers, the initial two types would be candidates to be Eligible Persistent Revolver Plaintiffs. It would be necessary to 'Test/Measure' potential Eligible Persistent Revolver Plaintiffs to ensure that each met the requirements in (2.) above. Relying upon Low Interest Rate Credit Cards - at March 2017, each Eligible Persistent Revolver Plaintiff seeks refund of all afore-mentioned - * Interest paid beyond 9% above the pertinent Overnight Cash Rate (eg. as at April 2017 it would be say at 20.99% Purchase interest rate, less 9%, less 1.5% Overnight Cash Rate = 10.49% of all interest on all Purchases made at 20.99% over a continuous nine year period), and * 50% of all Late Payment Fees and OverLimit Fees, as determined by 'Independent Scrutineers', to be refunded by - * Reserve Bank of Australia - 95%; and * ASIC - 5%.

The majority of potential Eligible Persistent Revolver Plaintiffs would not have paper copies of all pertinent Monthly Credit Card Statement. Research would have to be undertaken on scope to source old monthly statements under 'freedom of information'. Other issues:

See: |

|

|

|

{kind=link}