Writer's CD submission to RBA sent 8 Dec 2011 Defined Terms and Documents

5 Ronald Ave

Freshwater NSW 2096

0434 715.861

8 May 2017

Insert

one of the two enclosed DVDs in a Windows PC

which will open at this IntroLetterToMauriceBlackburn_8-May-17.htm

If using a MAC or the enclosed USB

stick drive,

open this letter at Senex\CreditCards\MauriceBlackburn\IntroLetterToMauriceBlackburn_8-May-17.htm

Mr. Andrew Watson

National Head of

Class Actions

Maurice Blackburn

Level 10, 456 Lonsdale Street

Melbourne VIC 3000

(03) 9605.2735

Dear

Andrew

- (click on any of the zillion embedded URLs in this

Intro Letter)

Class Action representing 400,000 circa Eligible Persistent Revolver Plaintiffs that possess Financial Literacy Capacity of only Level 1 (or less) and some Level 2 (Financially Uneducated And Vulnerable Australians) against Two Of Australia's Three Financial Services Regulators for breach of their respective Statutory Duty and Fiduciary Duty due to Negligence under Common Law by failing a Duty of Care "to act in the public interest" to inform the Commonwealth Government (obligated under Section 11 of the Reserve Bank Act 1959) that the PSB wanted** to adopt the User Pays Principle to Credit Cards (obligated under Section 8 of the Payments System Regulation Act 1998 and other rights/duties/obligations listed in Extensive Powers of RBA and ASIC - Our Powers) due to the 'eight items of evidence' listed in the heading/title of my Submission Letter to Maurice Blackburn

** Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001 evidences that Reserve Bank advocated a move ".....towards a 'user pays' approach to credit card payment services....” which never crystallised

Prior to retiring in 2007, the Writer worked for CBA for 37 years commencing in 1970 where he initially worked in four branches 'til 1974 when bank interest rates were rigidly controlled by the Reserve Bank and uncontrolled within the NBFIs. He worked the latter 18 years in infrastructure finance which was particularly satisfying working with talented people from the top legal, accounting firms and construction companies. He holds an Undergraduate Degree in Economics and a Master’s Degree in Applied Finance – both from Macquarie University.

In late 2011, the Writer commenced emails with Ms. Sharon van Etten, Public Relations Officer, Media & Public Relations Office, Reserve Bank of Australia regarding Credit Cards. After expending about 40 hours reading Reserve Bank Copious Publications On Credit Cards, he posted a comprehensive submission (on a CD ROM) dated 8 Dec 2011 to Ms. Sharon van Etten at the RBA which behoved the RBA to implement the User Pays Principle to Credit Card Products. The RBA did not respond.

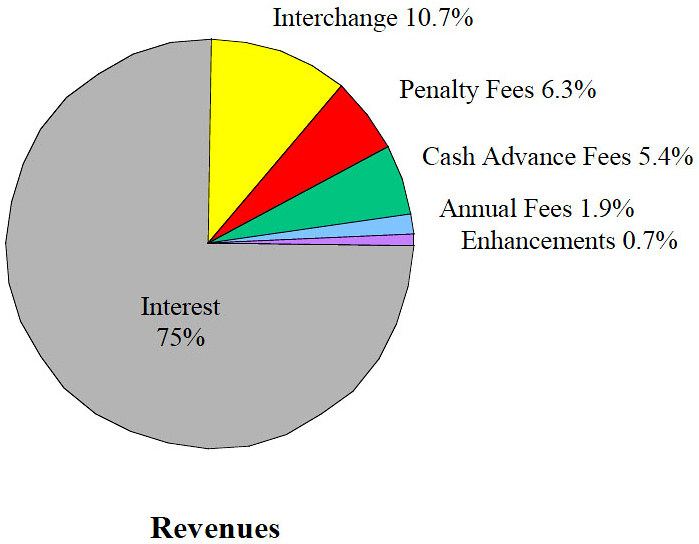

Credit Card Products are both ubiquitous and unique. Almost all goods and services purchased in the market place have a dollar price which is the same no matter if you are wealthy or poor - Financially Savvy or not. A loaf of bread, a carton of beer, a gallon of petrol command a price that the purchaser, rich or poor, pays. 67% circa of Credit Cardholders, those that are Financially Educated with level 3, 4 and 5 Financial Literacy Capacity, referred to by the RBA as Transactors, make almost no payment for enjoying a Line/s of Credit for up to 55 days. The remaining 33% circa, Revolvers, who are Financially Uneducated And Vulnerable Australians, with level 1 or 2 Financial Literacy, contribute 80% of the Credit Card Issuers' Revenues in Interest And Penalty Fees Revenue, of Credit Card Issuers. Hence, one third of Credit Cardholders pay the cost of two thirds of Credit Cardholders to enjoy a Line of Credit for an ave. $2,923 per month (per card) for up to 55 days.

{kind=link}

This inequitable pricing structure exists because of Unconscionable Conduct by too many Credit Card Issuers as evidenced in the 'Nine Examples' in a Labyrinth of Concealed Spiders in marketing a highly differentiated*** lending product, accompanied by a 70+ pages circa of fine print 'Terms & Conditions' booklets - too often with -

* loss of Interest Free Period for up to three months for failing to pay the Closing Balance in full by the Payment Due Date,

* luring Rewards Points, with Usurious Unsecured Personal Loan Interest Rates Charged On Many Credit Cards); and

* an inept, conflicted financial regulator with "Extensive Powers And Responsibilities" to "...gather (ANY) information from a payment system or from individual participants" under statutory authority to ensure "....the economic prosperity and welfare of (ALL) the people of Australia.

*** extract from the Summary of Productivity Commission's Staff Working Paper Links Between Literacy and Numeracy Skills and Labour Market Outcomes dated Aug 2010 included a bullet point summary titled "Key Points" which includes:

for nearly half of the population were assessed at either levels 1 (the lowest level) or 2, both of which are below the minimum level deemed necessary to participate in a knowledge-based economy (level 3). For example, level 3 is regarded by the survey developers as the ‘minimum required for individuals to meet the complex demands of everyday life and work in the emerging knowledge-based economy’ (ABS 2006, p. 5).

Transactors enjoy 'up to 55 days' Interest Free Period on their Line/s of Credit for a mode Card Limit of say $10,000 at virtually no annual cost because they pay their previous month's Closing Balance by the Payment Due Date. Line of Credit explains that the vast majority of these Credit Cardholders make multiple Purchases each month, sometimes several Purchases in a day, and do not pay a solitary cent on those Purchases for 'up to 55 days'.

Revolvers (with only level 1 and level 2 Financial Literacy skills) are paying the Transactors (with level 3, 4 and 5 Financial Literacy) usage costs for their Line/s of Credit which is contrary to -

(A) the RBA's mandate to ensure "...the economic prosperity and welfare of (all of) the people of Australia";

(B) the Wallis Report on the Australian Financial System: Summary and Critique June 1997 that support 'price controls' and unbundling the 'Sweets', Sours & Spiders' within Credit Cards to deliver a 'Vanilla' Revolving Line of Credit:

* Chapter Five: 'Philosophy of Financial Regulation' includes "Third, regulation can help achieve social objectives such as, for example, 'community service obligations' which typically take the form of price controls."

* Chapter Nine: 'Stability and Payments' "There is scope for increased competition in the payments system which will help to lower its costs of operation.................The RBA should retain overall responsibility for the stability of the financial system, the provision of emergency liquidity assistance and for regulating the payments system."

* Chapter Eleven: Promoting Increased Efficiency "Cross-subsidies are derived from historical product bundling [evident in (a) to (g) of Chapter 3 above], earlier difficulties with apportioning costs, and community expectations that institutions should meet community service obligations. The unwinding of such cross-subsidies can increase efficiency in the financial system."; and

(C) several Reserve Bank statements extracted in User Pays Principle.

The 12.58% circa Persistent Revolvers are subjected to Numeracy And Literacy Targeting with Predatory Advertising often paying Usurious Interest Rates with no Interest Free Period and usually incurring Late Payment Fees (some also incurring OverLimit Fees).

As noted in Section 1.B. of my Submission Letter to Maurice Blackburn dated 8 May 2017, on 17 July 2015 the Writer posted two CDs to Slater & Gordon which auto opened at his Introductory Letter to Slater and Gordon dated 17 July 2015 which asked James Higgins to review the Writer's Submission Letter to Slater and Gordon dated 17 July 2015 which sought S&G to launch a Class Action on behalf of Eligible Plaintiffs (not to be confused with the now Eligible Persistent Revolver Plaintiffs).

The Writer's Introductory Letter to Slater and Gordon dated 17 July 2015 and his more comprehensive Submission Letter to S & G also dated 17 July 2015 contained about 15% of the evidence that my Submission Letter to Maurice Blackburn dated 8 May 2017 contains, as evidenced by Additional Humdinger Evidence of Breach of Statutory Duty and Fiduciary Duty that the Writer has garnered in last three months to early May 2017.

If you have any doubts as to whether the Writer has undertaken requisite due diligence for this submission, click on the -

* 24 Chapters in Grounds/Reasons explain why the Shadow Minister for Revenue and Financial Services should submit Written Questions (re credit card products) to the Minister for Revenue and Financial Services during Question Time in the Lower House of Federal Parliament and read the 24 Chapter titles; and

* 13 Written Questions (re Credit Card Products) that the Shadow Minister for Revenue and Financial Services could submit to the Minister for Revenue and Financial Services during Question Time in the Lower House of Federal Parliament and the specific Grounds/Reasons for each Question which ask several questions and requests specific new financial information that the RBA should have been asking and seeking from Credit Card Issuers for several years to understand -

(A) how profitable Credit Card Products are; and

(B) which cohort/s of Credit Cardholders are funding that profit/revenue.

Should Maurice Blackburn wish to commence a Class Action against the Reserve Bank and ASIC (or only the Reserve Bank), the Writer would sell the I.P. in this DVD addressed to Maurice Blackburn dated 8 May 2017 for a Peppercorn Fee of $1.

The Writer's offer to sell the I.P. in this DVD (that opens at this Intro Letter to Maurice Blackburn) to Maurice Blackburn, and/or a litigation funder such as IMF Bentham, is conditional upon the legal counsel that represented Eligible Persistent Revolver Plaintiffs filing a statement of claim (or comparable claims document) upon the appropriate court which substantially includes the evidence contained in the following documents, so that evidence is then in the public domain, so that journalists/politicians have ready access to it:

-

Written Questions (re Credit Card Products) that the Shadow Minister for Revenue and Financial Services could submit to the Minister for Revenue and Financial Services during Question Time in the Lower House of Federal Parliament

-

Grounds/Reasons explain why the Shadow Minister for Revenue and Financial Services should submit Written Questions (re credit card products) to the Minister for Revenue and Financial Services during Question Time in the Lower House of Federal Parliament

The purpose of the above paragraph is to avoid the Defendant/s seeking an out-of-court confidential settlement that Maurice Blackburn, and/or a litigation funder, was attracted to accept prior to the afore-mentioned evidence entering the public domain.

Yours sincerely