Additional Humdinger Evidence of Breach of Statutory Duty and Fiduciary Duty that the Writer has garnered in last three months to early May 2017

1.

Reserve Bank published a 'Research Discussion Paper' LOAN RATE STICKINESS: THEORY AND EVIDENCE in June 1992 that the current Governor of the Reserve Bank, Phillip Lowe, and colleague, Thomas Rohling, wrote. It investigated whether movements in the Cash Rate were reflected in commensurate movements in loan and investment rates. It found that:

A. Increases in the Cash Rate were passed on relatively quickly (un-sticky).

B. Reductions in the Cash Rate were not passed on with lower Credit Card interest rates (sticky).

Mid way down Chapter 5 notes that:

* Seven years after the 18% interest rate cap was removed, namely in June 1992 when Phillip Lowe co-wrote LOAN RATE STICKINESS: THEORY AND EVIDENCE, the spread between the then Cash Rate of 6.50% and the Credit Card Purchase Interest Rate of 23% was 16.5% (Cash Advance interest rates are often appreciably higher).

* 32 years from 1985, in April 2017, the spread between the Cash Rate of 1.5% and the Credit Card Purchase Interest Rate of 20% is 18.5%. (As at April 2017, the highest Purchase interest rate is 25.9% from "Lombard Visa Card Classic." The highest Cash Advance interest rate is 29.49% from G.E. Money's "Go MasterCard").

Why did the Reserve Bank publish LOAN RATE STICKINESS: THEORY AND EVIDENCE in June 1992 if it was not concerned about interest rates stickiness?

What has the Reserve Bank done about interest rates stickiness with Credit Cards over the 25 years since June 1992?

===========================================

2.

The definition of User Pays Principle notes that -

(i) in 2001, the Reserve Bank released "RBA's Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001 that announced a movement "towards a 'user pays' approach to credit card payment services would be consistent with the approach adopted by Australian financial institutions in pricing other payment instruments under their control. It is also fairer and efficient, because consumers only pay for what they use.” Chapter 5 evidences that the Reserve Bank abandoned its aspirations for the User Pays Principle.

(ii) Reserve Bank of Australia - 'Our Role' notes: "To that end, it recommended the establishment of the Payments System Board at the Reserve Bank with the responsibility and powers to promote greater competition, efficiency and stability in the payments system."

(iii) Reserve Bank has not used its Extensive Powers and Responsibilities to ALL Australians to move "towards a 'user pays' approach to credit card payment services and promote greater competition and efficiency in the pricing structure that Credit Card Issuers apply to recoup their costs and achieve a profit for providing Credit Card Products because -

(a) the margin between the cost of funds and the maximum Cash Advance interest rate has increased from less than 1% when Reserve Bank removed the 18% cap on Credit Card interest rates in April 1985 up to 18.5% [Cash Rate of 1.5% and the RBA's nominated ave. Credit Card Purchase Interest Rate of 20%] whilst the "principal regulator of the payments system" has 'sat on its hands'; and

(b) Reserve Bank has ignored its own published evidence of the Interest And Penalty Fees burden upon Revolvers explained in Persistent Revolvers that is recognised by the Reserve Bank.

===========================================

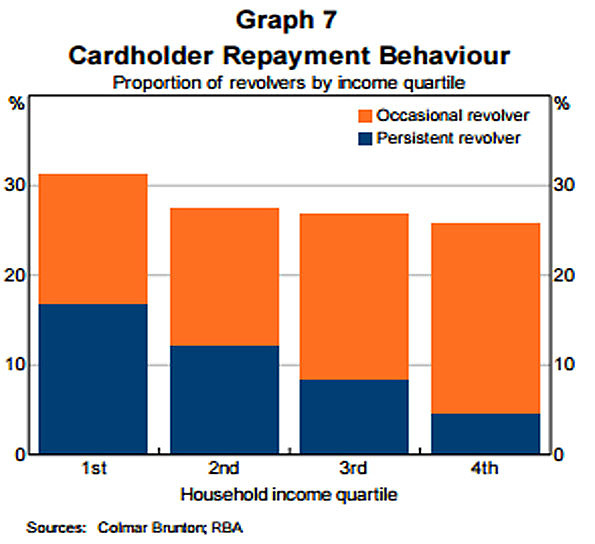

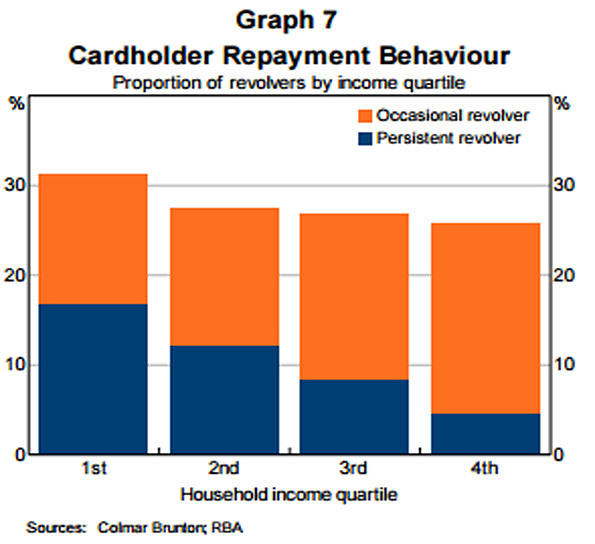

3.

Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - Aug 2015 in the below Graph 7 titled ''Cardholder Payment Behaviour" re the significant interest burden upon a new nomenclature in RBA documentation, namely Persistent Revolvers, [and earlier similar RBA findings noted in Persistent Revolvers and Revolvers]; such Persistent Revolvers possess very low Financial Literacy Capacity and fall within Financially Uneducated And Vulnerable Australians:

{kind=link}

In light of written representations by the Reserve Bank chronicled in User Pays Principle, what has the Reserve Bank done about reducing the interest burden upon Persistent Revolvers?

===========================================

4.

ASIC Has Ignored Its Acknowledgement Made in 2010 "That these findings [re Financial Literacy Capacity levels identified by the Productivity Commission and the ABS] "....have implications for our regulatory regime..."

===========================================

5.

The Writer's Introductory Letter to Slater and Gordon dated 17 July 2015 and his more comprehensive Submission Letter to S & G also dated 17 July 2015 referred to the RBA/PSB's 'extensive powers' (from the RBA page Payments System Board), but did not contain a Defined Term for Extensive Powers and Responsibilities of the RBA under 5 Sections therein which 'inter alia' notes:

*** The Reserve Bank of Australia's -

A. 'Powers' to gather financial information from ADIs; and

B. 'Responsibilities' to 'inter alia' "best contribute to.......... the economic prosperity and welfare of the people of Australia",

are "unique among central banks" and more extensive/inflexible than the -

1. Bank of England, that was not nationalised as Britain's central bank until 1946, which is a corporation wholly owned by the UK government - the 'Corporate governance: Board responsibilities' – SS5/16 (Short form) focus on the Corporates it regulates with no apparent obligation to best contribute to the peoples of Britain; and

2. U.S. Federal Reserve that was established as the United States' central bank in 1913 has the below obligation to " research .to increase understanding of the impacts of financial services policies and practices on consumers and communities." in the below item 7. "Promoting Consumer Protection and Community Development.":

"The Federal Reserve advances supervision, community reinvestment, and research to increase understanding of the impacts of financial services policies and practices on consumers and communities."

===========================================

6.

The Writer's Introductory Letter to Slater and Gordon dated 17 July 2015 and his more comprehensive Submission Letter to S & G also dated 17 July 2015 did not provide the information under the below Section 2 of the Writer's Submission Letter to Maurice Blackburn:

2. Issues to warrant/justify a Class Action against the Reserve Bank and ASIC for breach of their respective Statutory Duty and Fiduciary Duty to Persistent Revolvers, that represent a majority portion of Financially Uneducated And Vulnerable Australians, with very low Financial Literacy Capacity ("nearly half of the population were assessed at either levels 1 (the lowest level) or 2, both of which are below the minimum level deemed necessary to participate in a knowledge-based economy (level 3)" - Level 5 is the highest level

A. Reasons for de-regulation of the commercial banks from 1980 - after over 100 years of regulation

B. Precedent to re-regulate after deregulation exposed flaws

C. What has Australia's "... principal regulator of the payments system ..." done about some Credit Cardholders that are suffering Extreme Financial And Emotional Distress being issued numerous Credit Cards as evidenced in:

* Credit Card Distress Authorities

D. Further evidence of RBA's Negligence under Common Law by failing a Duty of Care "to act in the public interest" to re-set a max Credit Card interest rate/s after it published in 1992 "LOAN RATE STICKINESS: THEORY AND EVIDENCE" that evidenced a material drop in the cost of funds, yet Credit Card Issuers had failed to lower Credit Card interest rates

E. RESERVE BANK ACT 1959 - SECT 11 sets out the 'modus operandi' that the Reserve Bank and the PSB must abide by to inform its financial policy to the Federal Govt. and that the Grosvenor General has the 'final call' on any Reserve Bank and the PSB 'financial policy' that the Federal Govt. does not believe "is directed to the greatest advantage of the people of Australia".

F. Some Papers/Articles on Statutory Duty and litigation that do not seem to preclude the proposed Class Action

===========================================

7.

The Writer has prepared 1. and 2. below which evidence that the Reserve Bank has breached its Statutory Duty and Fiduciary Duty through Negligence under Common Law by failing a Duty of Care "to act in the public interest" by not drawing upon its Extensive Powers to seek meaningful financial information to establish, inter alia, which cohorts of Credit Cardholders are paying "The Lion's Share" of Interest And Penalty Fees Revenue:

1. Written Questions (re Credit Card Products) that the Shadow Minister for Revenue and Financial Services could submit to the Minister for Revenue and Financial Services during Question Time in the Lower House of Federal Parliament - that evidences negligence by the Reserve Bank not relying upon its Extensive Powers under the Payment Systems Regulation Act 1998 to ask commercial banks for a broad range of financial information to identify -

(A) how much of Interest And Penalty Fees Revenue is being born by Persistent Revolvers; and

(B) what percentage of the 16.686 million Credit Cards are held by Persistent Revolvers.

2. Grounds/Reasons explain why the Shadow Minister for Revenue and Financial Services should submit Written Questions (re credit card products) to the Minister for Revenue and Financial Services during Question Time in the Lower House of Federal Parliament - contains many graphs and tables primarily draw from RBA website - which expose the Reserve Bank for maintaining the below statistical information 'of no material use' re Credit Cards and Charge Cards, but it fails to seek financial information from Credit Card Issuers that establishes that Revolvers -

(A) are paying 100% circa of all Interest And Penalty Fees Revenue; and

(b) the 37.25% of Revolvers that are Persistent Revolvers are paying 89% of Credit Cardholders' Contribution To Credit Card Issuers' Gross Revenue:

===========================================

8.

Determine Standards to 'inter alia' re-cap Credit Card interest rates for 'public interest issues' debunks Ms. van Etten's Media & Public relations, RBA, email sent 10 Nov 2011 to the Writer that noted: "The Payments System Board of the Reserve Bank has no regulatory power over these aspects of credit cards", because the Reserve Bank could have determined Standards to re-introduce a cap/s over Credit Card interest rates, by according with Section 11 of the Reserve Bank Act 1959, any time it wanted to since the Reserve Bank published LOAN RATE STICKINESS: THEORY AND EVIDENCE in June 1992.

===========================================

9.

Labyrinth of ‘Concealed Spiders’:

(i) Contained four examples of Predatory Advertising that falls within the ACCC definition of Unconscionable Conduct in the Writer's Submission to S&G dated 17 July 2015.

(ii) Now contains nine examples of Predatory Advertising that falls within the ACCC definition of Unconscionable Conduct.

===========================================

10.

Reserve Bank has explicit 'Responsibilities/Obligations' to "the economic prosperity and welfare of (ALL) the people of Australia". The UK Credit Card Regulator, BIS, overtly recognised in three published reports protecting "the most vulnerable in society" in implementing Five New Rights for Credit Cardholders - effective 31 Dec 2010

RBA's copious 'Submissions', 'Reviews', 'Reports', 'Discussion Papers', 'Staff Working Papers' and 'Enquiries' into Credit Cards are bereft of any mention whatsoever of protecting "vulnerable consumers" or "at risk consumers", whereas the UK regulator regularly makes specific mention of providing "real help for vulnerable consumers" (and similar) in its published reports

Does the Reserve Bank consider that all Credit Cardholders possess the same Numeracy and Literacy Capacity?

Or does it assume 'caveat emptor'?

As noted in 'Proponents in Australia that ........' (further below), other contributing Australian interested parties recognise protecting 'vulnerable consumers', but not the RBA

Productivity Commission and ABS have published several detailed reports about the divergent Numeracy and Literacy Capacity across the Australian population (Chapter 1)

Reserve Bank failing to recognise/comment (in its 'Submissions', 'Reviews', 'Reports', 'Discussion Papers', 'Staff Working Papers' and 'Enquiries' into Credit Cards) 'vulnerable' or 'at risk' Credit Cardholders (with only low Financial Literacy Capacity) constitutes breach of its Statutory Duty and Fiduciary Duty to Persistent Revolvers

Joint Media Release Getting a Better Deal on Credit Cards and Mortgages issued on 5 July 2011 evidences that RBA plagiarized (from UK BIS) the metaphor "Getting a Better Deal" - first used in BIS report (to the UK Parliament) dated 5 July 2009 titled "A Better Deal for Consumers - Delivering Real Help Now and Change for the Future" - 18 months slower than the UK Regulator, BIS

10(a).

Reserve Bank webpage 'Credit Cards Regulatory Decisions' evidences that the Reserve Bank, the legislative appointed protector of Credit Cardholders, did naught for the Retail Supply Side prior to March 2014

RBA breached it Extensive Responsibilities to Persistent Revolvers by taking 12 years circa to 'stamp out' five ploys of Unconscionable Conduct listed in Joint Media Release Getting a Better Deal on Credit Cards and Mortgages that initially surfaced in the USA, migrated to the UK and onto Australia - 18 months slower than the UK Regulator, BIS

===========================================

11.

Credit Card Issuers have since conjured up more Predatory Advertising to Target Credit Cardholders With Low Financial Literacy Capacity that continued unchecked by Two Of Australia's Three Financial Services Regulators

===========================================

12.

Has the RBA ever been -

* conflicted; and/or

* Asleep at the wheel?

Banknotes scandal covered up - The Age INVESTIGATIVE UNIT - 5/10/2011

Crooked As A Dog's Hind Leg | Barnaby Is Right

Probe Reserve Bank 'dirty deals' with Saddam Hussein, Greens urge - The Australian - 30 Sept 2013

RBA in Notes deal - The Australian

New evidence raises questions of RBA bribery response - ABC 7:30 Report

You don't fit in, f--- off', Reserve Bank whistleblower told - SMH - 30 Sept 2013

AFP lay bribery charges against RBA currency firms, Securency ...

===========================================