|

|

Writer's CD submission to RBA sent 8 Dec 2011 Intro Letter to Maurice Blackburn Submission Letter to Maurice Blackburn Defined Terms and Documents EVIDENCE CHECK LIST

A. Evidence of "vulnerable consumers" or "at risk consumers" amongst Credit Cardholders that the RBA has NEVER acknowledged in its Copious Publications on Credit Cards (Item E. of EVIDENCE CHECK LIST listed further below establishes that the UK regulator, BIS, overtly explained the need to protect "vulnerable consumers" or "at risk consumers")

Productivity Commission and ABS have published several detailed reports about the divergent Numeracy and Literacy Capacity across the Australian population (Chapter 1) Federal and State Govt's allocate $43.38 million annually to 44 Australian charities to provide 500 circa financial counselling to Australians that are experiencing Extreme Financial And Emotional Distress where the vast majority of those counseled are Credit Cardholders with poor Financial Literacy Capacity. (Chapter 7) The following 'interest parties' have evidence of Predatory Advertising that Target Credit Cardholders with Low Financial Literacy Capacity that are suffering Extreme Financial and Emotional Distress and often hold/use several/many Credit Cards: 4. Credit Card Distress Authorities Australia's "... principal regulator of the payments system ..." has failed to impose a 'Standard', pursuant to Division 4, Section 18 of the Payments System Regulation Act 1998, upon Credit Card Issuers to ensure Credit Cardholders that are suffering Extreme Financial And Emotional Distress are not issued additional Credit Cards evident in Quotes from reputable authorities about unconscionable advertising of Credit Cards by Credit Card Issuers resulting in some indebted Credit Cardholders being issued multiple Credit Cards. A1. Labyrinth of ‘Concealed Spiders' provides nine examples of Unconscionable Conduct by Credit Card Issuers in Predatory Advertising their various Credit Card Products to extricate maximum Interest and Penalty Fees Revenue from Financially Uneducated Credit Cardholders which constitutes Numeracy And Literacy Targeting - also acknowledged in Quotes from reputable Credit Card Distress Authorities about unconscionable advertising of some Credit Cards by some Credit Card Issuers resulting in some indebted Credit Cardholders being issued multiple Credit Cards. =================== B. Reserve Bank Enjoys Extensive Powers and shoulders Responsibilities to All Australians far beyond those held by U.S. Federal Reserve or the Bank of England to - * request any financial information from ADIs that it wants to examine; or * responsibilities to "........best contribute to........the economic prosperity and welfare of (ALL) the people of Australia". =================== C. History of regulation and de-regulation Australian banks had been highly regulated through 19th and most of 20th century due to crashes. Commonwealth Bank lost its central bank functions in 1959. Thence, the new Reserve Bank controlled bank interest rates until 1981 (Chapter 17) notes:

The Reserve Bank removed the 18% cap on the maximum Credit Card interest rats in April 1985. Prior to Aug 1993, Credit Card Issuers were restricted from charging an Annual Fee on Credit Cards as the various State Credit Acts prohibited most Credit Card Issuers from charging annual fees if they charged interest on credit card purchases (e.g. Credit Act 1984 (NSW) s 54). Following a recommendation from the Prices Surveillance Authority’s 1992 ' Inquiry Into Credit Card Interest Rates', State legislatures issued exemption orders which allowed all financial institutions to charge both interest and fees on credit cards from 1 August 1993.Below is an extract from Consumer Affairs Victoria - Regulating the cost of credit which evidences that in the past if de-regulation did not achieve the desired results, then re-regulation followed.

=================== D. Incriminating evidence of Reserve Bank failing "vulnerable consumers", "at risk consumers" (i) Reserve Bank published a 'Research Discussion Paper' LOAN RATE STICKINESS: THEORY AND EVIDENCE in June 1992 that the current Governor of the Reserve Bank, Phillip Lowe, and colleague, Thomas Rohling, wrote. It investigated whether movements in the Cash Rate were reflected in commensurate movements in loan and investment rates. It found that:

(ii) Section 5.2 'Scheme regulations and competition benchmarks' of "RBA's Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001 (Chapter 5) merited the User Pays Principle: - page 116 to "...meet the public interest test ...." ........."Reform of credit card schemes will also have a direct impact on credit cardholders and is likely to result in some re-pricing of credit card payment services. However, this is the means by which the price mechanism is to be given greater rein in the credit card market. A movement towards a 'user pays' approach to credit card payment services would be consistent with the approach adopted by Australian financial institutions in pricing other payment instruments under their control. It is also fairer and efficient, because consumers only pay for what they use.” - explained in User Pays Principle. (iii) Below is an extract from Revolvers that notes that the RBA published a report as early as Dec 2001 that alerted that roughly 33% of Credit Cardholders, labeled by the RBA as Revolvers, pay all Interest and Penalty Fees Revenue, while 67% circa Transactors enjoy a Convenient Free Ride: "The below extract from RBA's Consultation Document titled Executive Summary - Reform of Credit Card Schemes in Australia: RBA's "A Consultation Document" – Dec 2001 notes - * under point 6 of 'Introduction' that some Credit Cardholders enjoy the convenience of their Revolving Line/s of Credit without materially contributing to Credit Card Issuers' operating costs:

* on page 15:

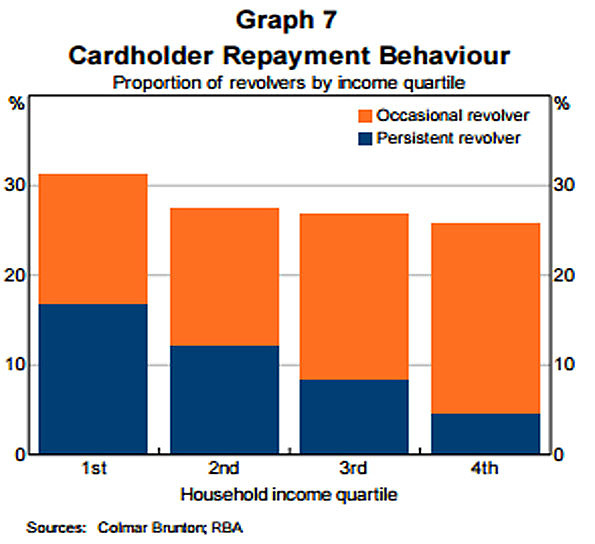

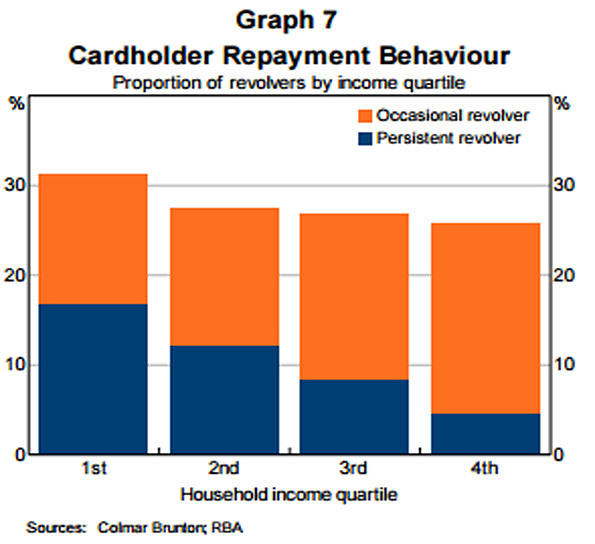

(iv) The nomenclature, Persistent Revolvers, was first used/applied by the Reserve Bank in its Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - Aug 2015 when it published Graph 7 "Cardholder Payment Behaviour" (Chapter 5). The definition of Persistent Revolvers explains that 33% circa of Credit Cardholders transactions are made by Revolvers and 37.25% circa of Revolvers are Persistent Revolvers. Persistent Revolvers hold 12.58% circa of the 16.8 million Credit Cards on issue in Australia (i.e. 2,057,234 Credit Cards circa). Yet those two odd million Credit Cards owned by Persistent Revolvers that have very low Financial Literacy Capacity (as measured by the Productivity Commission, ABS and ASIC reports - Chapter 1) contribute 80% circa of all Interest and Penalty Fees Revenue generated from Credit Card Products. The average Persistent Revolver holds approx. four times the number of Credit Cards that each Transactor holds.

Credit Cardholders' Contribution To Credit Card Issuers Gross Revenue notes that 12.58% circa of Credit Cardholders (not 20%), namely Australia's Persistent Revolvers (referred to by McKinsey in the USA as 'Financially stressed'), identified in RBA Graph 7 "Cardholder Payment Behaviour" (in RBA report RBA Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - Aug 2015) pay 80% circa of Interest and Penalty Fees Revenue. Interest and Penalty Fees Revenue represent 80% circa of Credit Card Issuers' Gross Revenue. After removing Merchant Service Fees revenue (ostensibly Interchange Fees and Card Acquirer Fees drawn from the Wholesale Supply Side) from Credit Card Issuers' Gross Revenue, Interest and Penalty Fees Revenue paid by Persistent Revolvers accounts for 89% of Credit Cardholders' "Contribution To Gross Revenue" from the Retail Supply Side.

Of the Four Types of Revolvers, the initial two types would be candidates to be Eligible Persistent Revolver Plaintiffs. It would be necessary to 'Test/Measure' potential Eligible Persistent Revolver Plaintiffs rigorously to ensure that each met the requirements in (2.) d) of Eligible Persistent Revolver Plaintiffs. (v) Below is an extract from Chapter 16 titled "The Reserve Bank could reduce insolvencies, bad debts and Extreme Financial And Emotional Distress by regulating Credit Card Issuers to conform Credit Cards closer to the original Charge Card. The current arrangement of Credit Card Issuers seeking data from one or two of Three Credit Rating Agencies is not working as the credit data is not complete, unless data from all three Credit Reporting Agencies is sourced":

Notwithstanding the evidence in A. B. C. and D. above, incongruously over the subsequent 25 years since RBA published LOAN RATE STICKINESS: THEORY AND EVIDENCE back in June 1992, RBA has failed (as obligated under Section 11 of the Reserve Bank Act 1959) to inform the Commonwealth Government that - A. the spread between Credit Card Issuers' Wholesale Cost Of Funds has increased from less than 1% in April 1985 (when the Reserve Bank removed the 18% cap on the maximum Credit Card interest rate) to the current spread of 18.5% (Overnight Cash Rate of 1.5% and the Credit Card Purchase Interest Rate of 20%) [max Cash Advance interest rate in April 2017 is 29.49% representing a spread of 26.49% after Latitude Financial's cost of funds]; and B. the Reserve Bank deems it necessary to re-introduce a cap on the maximum - * Purchase Interest Rate of 12% circa above the Overnight Cash Rate; and * Cash Advance interest rate of 15% circa above the Overnight Cash Rate - refer Low Interest Rate Credit Cards - at March 2017, because of the RBA's findings in - (i) LOAN RATE STICKINESS: THEORY AND EVIDENCE - June 1992 that noted that Credit Card interest rates did not reduce in line with the Overnight Cash Rate; (ii) Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001 evidences that Reserve Bank wanted to move ".....towards a 'user pays' approach to credit card payment services....” but failed to do so; (iii) RBA's Consultation Document titled Executive Summary - Reform of Credit Card Schemes in Australia: RBA's "A Consultation Document" – Dec 2001 published a report as early as Dec 2001 that alerted that roughly 33% of Credit Cardholders, then labeled by the RBA as Revolvers, pay all Interest and Penalty Fees Revenue, while 67% circa Transactors enjoy a Free Ride; and (iv) Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - Aug 2015 in Graph 7 titled ''Cardholder Payment Behaviour" re the gross interest burden upon Persistent Revolvers [and earlier similar RBA findings noted in Persistent Revolvers and Revolvers] that possess very low Financial Literacy Capacity and fall within Financially Uneducated And Vulnerable Australians.

Determine Standards to 'inter alia' re-cap Credit Card interest rates for 'public interest issues' (To Act In The Public Interest) explains the three steps (1. 2. and 3.) for the Reserve Bank to re-impose an interest rate cap on Credit Cards or impose any other material regulation. D1. Implicating evidence of ASIC failing "vulnerable consumers", "at risk consumers" ASIC Has Ignored Its Acknowledgement Made in 2010 "That these findings [re financial literacy 5 levels] "....have implications for our regulatory regime,... "....which relies upon disclosure as a critical element of our consumer protection system." =================== E. Reserve Bank has explicit 'Obligations' to "the economic prosperity and welfare of (ALL) the people of Australia". Yet RBA's Copious Publications on Credit Cards are bereft of any mention whatsoever of protecting "vulnerable consumers" or "at risk consumers", - hasn't been on the RBA's radar, whereas - * the UK regulator, BIS, that administered the removal of five 'Spiders' in 2010 (effective 31 Dec 2010) regularly makes specific mention of providing "real help for vulnerable consumers" (and similar) in its three published reports E1. Joint Media Release "Getting a Better Deal on Credit Cards and Mortgages" issued on 5 July 2011 evidences that RBA plagiarized (from UK BIS) the metaphor "Getting a Better Deal" - first used in BIS report (to the UK Parliament) dated 5 July 2009 titled "A Better Deal for Consumers - Delivering Real Help Now and Change for the Future" E2. RBA breached it Extensive Responsibilities to Persistent Revolvers by taking 12 years circa to 'stamp out' five ploys of Unconscionable Conduct listed in Joint Media Release "Getting a Better Deal on Credit Cards and Mortgages" that initially surfaced in the USA, migrated to the UK and onto Australia - 18 months slower than the UK Regulator enacted E3. Credit Card Issuers have since conjured up more Predatory Advertising to Target Credit Cardholders With Low Financial Literacy Capacity that continued unchecked by Two Of Australia's Three Financial Services Regulators =================== F. The Australian govt. website, "The strength of Australia’s financial sector" boasts that "The four major banks ........... are also some of the most profitable in the world." This submission presents one of the material reasons why the Four Pillars are so profitable ie. because two of Australia's Three Financial Services Regulators have abrogated their statutory appointed mandates to the detriment of many of those Australian people that are not shareholders (Chapter 12). =================== G. Credit Card Issuers are Unconscionably punishing Credit Cardholders with poor Financial Literacy Capacity by Withdrawing their Interest Free Period And Paying Interest On Each Purchase From The Purchase Date for the subsequent two months often at Usurious Interest Rates For most of the 55+ years existence of Credit Cards, the Credit Cardholder paid Interest on that part of the Total Amount Owing that was not repaid by the Payment Due Date. If the Total Amount Owing was $500 and the Credit Cardholder repaid $400 by the Payment Due Date, the Credit Cardholder was charged Interest on the $100 until the remaining $100 was repaid. And then the Interest Free Period was re-instated. Almost all Credit Card Issuers have moved from the above former interest charging model of charging interest on any shortfall until repaid, to charging Interest on all Purchases if the Total Amount Owing is not repaid by the Payment Due Date, even if the payment was 'a dollar short or a day late'. Some Credit Cards also cancel the Interest Free Period for up to two subsequent months, if the Total Amount Owing is not paid by the Payment Due Date, which means that if a Credit Cardholder failed to pay the Total Amount Owing in the third month, he/she could forfeit their Interest Free Period for five months; many Financially Uneducated And Vulnerable Credit Cardholders have so forfeited - see Example 1. Credit Cardholders with poor Financial Literacy Capacity are much more prone to Forfeit Interest Free Period And Pay Interest On Each Purchase From The Purchase Date which can spiral into accelerating Outstanding Indebtedness and Extreme Financial And Emotional Distress; this Spider is invariably not noted in advertisements, nor included in the Key Facts Sheet, rather concealed in the Terms & Conditions document up to 90 pages in tiny 9 font in dark grey text - see Example 1:

|

|

|

|

{kind=link}

{kind=link}

{kind=link}

{kind=link}