|

|

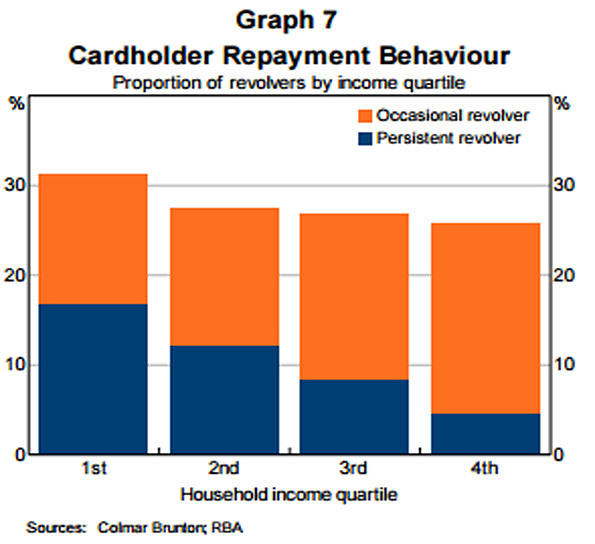

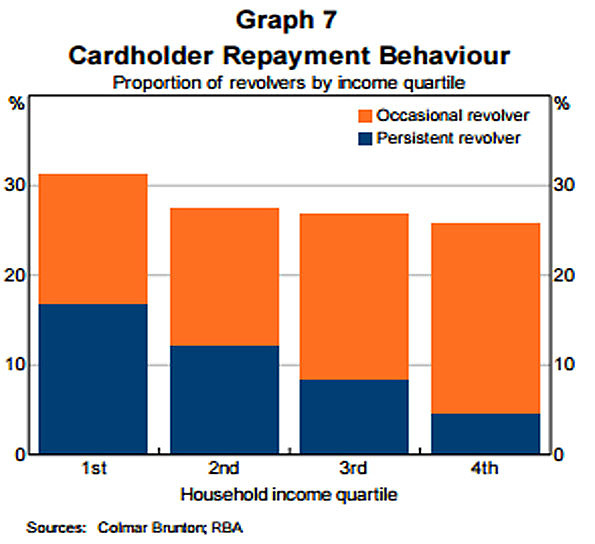

Thirty Two Questions and Supporting Evidence Submission Letter to Royal Commission April-2018 Defined Terms & Documents 16th Question Will the Royal Commission ask the Chair of the Council of Financial Regulators if it sought financial data from the primary six or seven Credit Card Issuers (Four Pillars, Citibank and Latitude Financial nee G.E. Capital) that identifies the number, Outstanding Indebtedness and demography of Credit Cardholders that are Persistent Revolvers after the RBA quantified in Graph 7 of RBA Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - Aug 2015 the indebtedness borne by Persistent Revolvers? ================================================= Supporting Documented Evidence re 16th Question

1. Submission 20 to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - Aug 2015 (Reference A listed at top of this page - 3rd Publication) evidenced the RBA introduce a new nomenclature, Persistent Revolvers, in Aug 2015 to describe Credit Cardholders that were hopelessly in debt: * Graph 7 titled ''Cardholder Payment Behaviour" quantified the magnitude of the gross interest burden falling upon Persistent Revolvers that often possess low Financial Literacy Capacity that are often Financially Uneducated And Vulnerable Australians and have paid Usurious Interest Rates. The Writer calculates that Persistent Revolvers accounted for 12.58% circa of the 7,515,000 Credit Cardholders (June 2016), namely 945,000 [cell b36] Credit Cardholders (ASIC 'Credit card debt clock' 27-Apr-17) paid an Unconscionable 80% circa of Interest And Penalty Fees Revenue levied by Credit Card Issuers; and * Noted that "..... In addition, many credit card holders take advantage of interest-free periods such that they do not pay interest on their card balances " identified by the RBA as Transactors.

2. Federal and State Govt's allocated $43.38 million in 2014 to 44 Australian charities to provide 500 circa financial counselling to Australians, over the subsequent year, that are experiencing Extreme Financial And Emotional Distress. The vast majority of those counselled are Credit Cardholders with poor Financial Literacy Capacity (Chapter 7). The Federal Govt. funds $20m and the State Govts collectively fund a further $23m to 44 circa community organisations throughout Australia annually towards the salaries of approx. 500 Financial Counsellors that provide financial counselling, ostensibly to Australians carrying high Credit Card Debt Accruing Interest and others also suffering a gambling addiction.

3. Financial Counsellors at Australia's major charities should require these community organisations (or at least the larger community organisations) to provide periodic returns/reports to these Government agencies which inform 'inter alia' the - 1. number, indebtedness and demography of the Credit Cardholders (which may include a husband and wife collectively) that the Financial Counsellors are assisting; and 2. number of Credit Cardholders that are carrying Credit Card Debt Accruing Interest over the following brackets of indebtedness and the average number of Credit Cards that the Credit Cardholders in these six segments carry indebtedness?

·

$10,000 but less than $20,000 - (eg. 2,556 Credit Cardholders (individual

or couples) own 10,767 Credit Cards (= 4.2 Credit Cards per person or husband

and wife/partner) across 10 largest community

organisations) |

|

|

|

{kind=link}

{kind=link}