Dr. Edey was

questioned before the Acting Chairperson of the

Senate Economics Legislation

Committeeon 1 June 2015 regarding a dearth of competition in Credit Card interest

rates when the Overnight

Cash Rate is at an all-time low of 1.5% and the highest -

Dr. Edey responded:

"... we do not have an interest rate regulator in

Australia............... What

we do have is an ACCC that can investigate uncompetitive conduct if they see it,

but they clearly have not seen it in this market".

Will the Royal Commission ask the

Governor of the Reserve Bank

why the former

Assistant Commissioner, Dr. Malcolm Edey, provided the above response that resiled the RBA's

obligations and responsibilities to

".....promoting competition in the market for payment services,

.....",

pursuant to -

How could a very

senior representative of the RBA with over 20 years experience working for

the RBA not know that the RBA shouldered all of the ACCC's obligations re

ensuring competition from 23 Feb

2004?

It defies belief for Dr. Edey to have responded

"What

we do have is an ACCC that can investigate uncompetitive conduct if they see

it, but they clearly have not seen it in this market".

The above extract "... we do not have an interest rate

regulator in Australia.............."

from an address by Dr. Malcolm Edey (RBA) contradicts the below indented

extracts from

Reserve Bank of Australia Bulletin - July 1998 - Australia’s New Financial

Regulatory Frameworkthat

chronicles the Reserve Bank's powers, set out in the

Payment Systems (Regulation) Act 1998,

that allow

the Reserve Bank

to undertake

more direct regulation of ‘designated’ payments systems to "... promote competition in the market for

payments services, consistent with the overall stability of the financial

system..."

when it judges it to be

"in the public interest" whichmay

involve the imposition of access rules or operating standards for

participants in such systems:

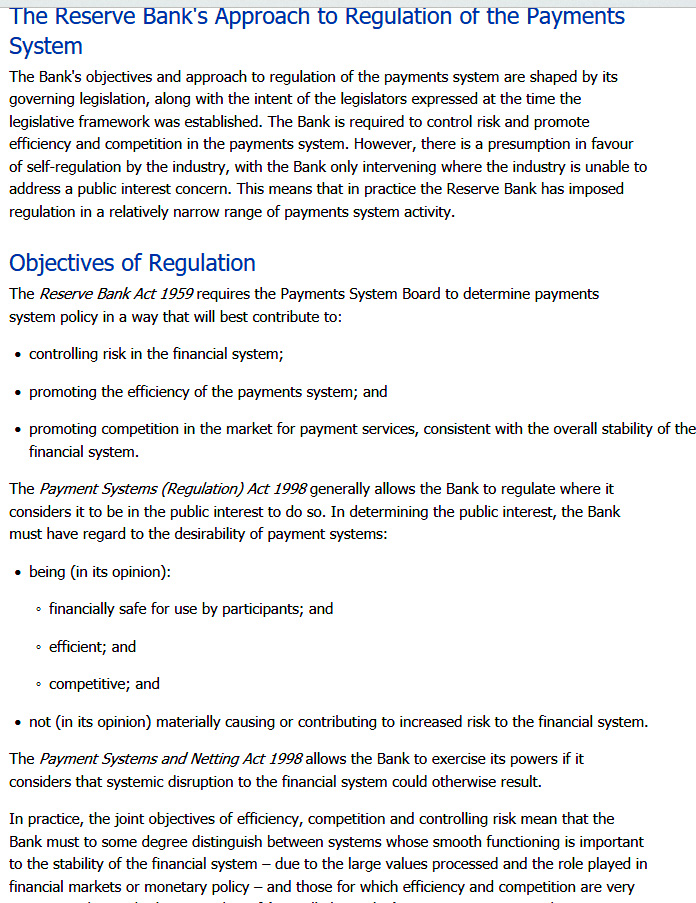

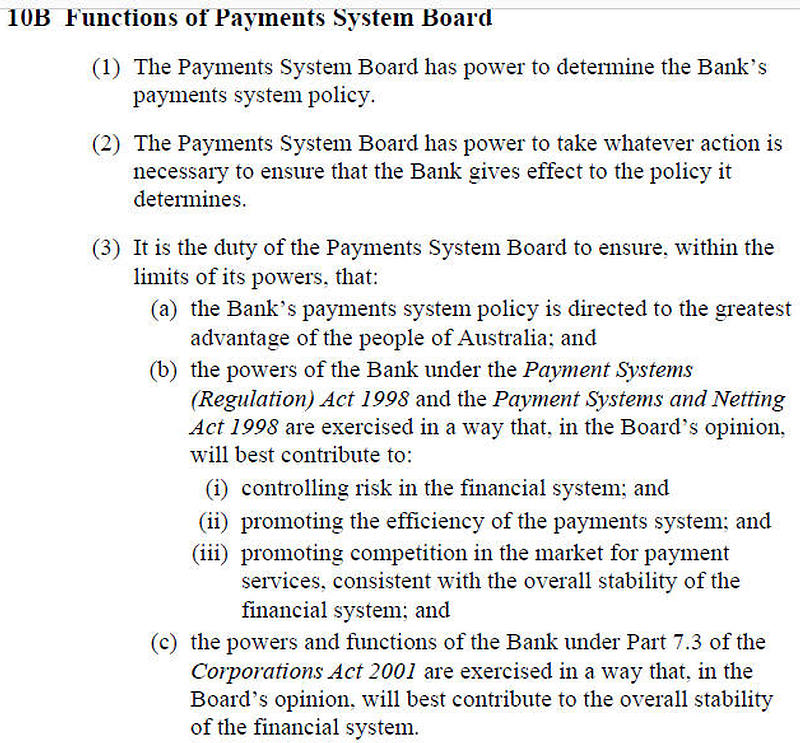

"The

new Payments System Board is responsible for the Bank’s payments

system policy, the objectives of which are:

•

controlling risk in the financial system arising from the operation

of the payments system;

•

promoting the efficiency of payments systems; and

•

promoting competition in the market

for payments services, consistent with the overall stability of the

financial system.

The Bank’s powers in this area, set out in the

Payment

Systems (Regulation) Act 1998,

allow it to undertake more direct

regulation of ‘designated’ payments systems when it judges it to be

in the public interest. This may involve the imposition of access

rules or operating standards for participants in such systems. The

Act also provides a framework for regulation of purchased payment

facilities, such as travellers cheques and stored-value cards."

the

ACCC is responsible for ensuring that payments system arrangements

comply with the competition and access provisions of the

Competition and Consumer Act 2010,

in the absence of any specific Reserve Bank initiatives.

Under its adjudication role, the ACCC may grant immunity from court

action for certain anti-competitive practices, if it is satisfied

that such practices are in the public interest. It may also accept

undertakings in respect of third-party access to essential

facilities; and

if the

Reserve Bank, after public consultation, uses its powers to impose

an access regime and/or set standards for a particular payment

system, participants in that system will not be at risk under the

Competition and Consumer Act 2010

by complying with the Bank's requirements.

The effect is that the ACCC retains responsibility for competition and

access in a payment system, unless the Bank designates that system and

follows up by imposing an access regime and/or setting standards for it.

If the Bank does so, its requirements are paramount. Designation does

not, by itself, remove a system from the ACCC's coverage."

{kind=link}

{kind=link}