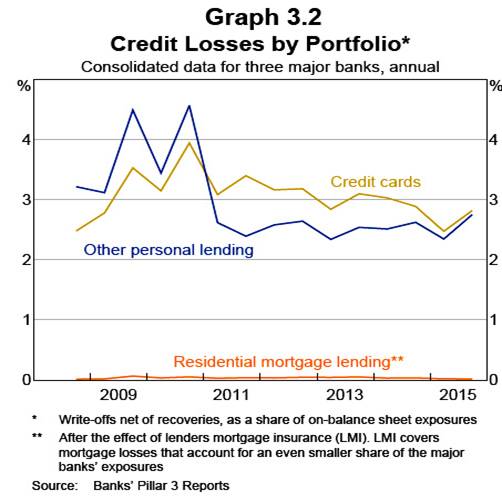

|

Thirty Two Questions and Supporting Evidence Submission Letter to Royal Commission April-2018 Defined Terms & Documents 9th Question SMH article titled APRA says everything is fine in housing market, but look at credit cards by Gareth Hutchens (4 June 2015) quoted that APRA Chairman, Wayne Byres, told senators in Canberra:

Mr. Byres also agreed with Treasury, the RBA, and the Australian Securities and Investments Commission officials that there ought to be closer scrutiny of the interest rates banks are charging on their credit cards, because the current "spread" between the official cash rate and rates charged on credit cards was at record levels. "I understand the point fully that the margins on credit card business look very high, certainly to any other form of credit, and certainly I can't sit here today with an explanation of why that is," Mr Byres said. "Informing us all about that is probably a useful piece of work." Will the Royal Commission ask the APRA Chairman, Wayne Byres, what has APRA actioned to quantify the profits earned by Credit Card Issuers due to the APRA Chairman's comments to senators in Canberra on 3 June 2017 that included "....the margins on credit card business look very high , certainly to any other form of credit, and certainly I can't sit here today with an explanation of why that is,"............ and ............ "Informing us all about that is probably a useful piece of work"? Will the Royal Commission ask the Governor of the Reserve Bank who is the Chair of the Council of Financial Regulators, and co-wrote LOAN RATE STICKINESS: THEORY AND EVIDENCE in June 1992, if he has ever discussed with the other two members of that Council, namely APRA and ASIC, the RBA informing the Government, pursuant to section 50 of the Banking Act 1959, of the need for the RBA to re-regulate a maximum interest rate for Purchases and for Cash Advances due to the burgeoning gap between the Overnight Cash Rate of 1.5% and interest rates charged on low interest and on high interest Credit Cards that peak at 29.49% for a Cash Advance using a Latitude Financial "Go MasterCard". ================================================= Supporting Documented Evidence re 9th Question 1. As chronicled in Chapter 5, in April 1985, when the 18% cap on Credit Card interest rates was removed by the RBA, the spread between the cost of funds and the 18% cap was less than 1%. That spread has widened and widened and is now as high as 22.4% for a Purchase and 26.5% for a Cash Advance to the material detriment of Financially Uneducated And Vulnerable Australians that Lack Financial Acumen often due to poor Financial Literacy Capacity identified by the Reserve Bank as Persistent Revolvers. 2. Below are extracts from the Productivity Commission's Draft Report titled "Competition in the Australian Financial System" dated Jan 2018 - 401 pgs - accessible at Competition in the Australian Financial System: · The institutional responsibility in the financial system for supporting competition is loosely shared across APRA, the RBA, ASIC and the ACCC. In a system where all are somewhat responsible, it is inevitable that (at important times) none are.

3. Australia's Highest Interest Rate Credit Cards. 4. It is an indictment that Three Parliamentary Appointed Bodies That Regulate Financial Services that are bound to "act in the public interest" do not publish Minutes of the quarterly meetings of the Council of Financial Regulators which would provide an audit trail that these three regulators are, in fact, "acting in the public interest", particularly as the RBA Board Meetings are Minuted. One ponders the reason. Perhaps Dr. Norman Edey would assert that they sometimes discuss commercially sensitive matters, but Minuting discussions re information sharing regarding the Counsel's responsibilities, in particular "to discuss regulatory issues", should not be commercially sensitive. And if it is, then we all have a problem with the efficacy of our Three Parliamentary Appointed Financial Services Regulates. 5. The Writer emailed RBA_Info on Friday, 16 March 2018 4:57 PM asking where he could access the Minutes of the quarterly meeting of the non-statutory Council of Financial Regulators. On 19 March RBA_Info informed that there are no published Minutes, but directed him to page 57 of RBA's Financial Stability Review - Oct 2017 titled Domestic Regulatory Developments. Sadly, the word Credit Card or Credit Cards does not warrant a mention. But it does contain a lot of impressive ACRONYMS. 6. RBA's Financial Stability Review - Oct 2015 was the first meeting of the Council of Financial Regulators after APRA Chairman, Wayne Byres' below repeated undertaking to Senators on 4 June 2015: "Informing us all about that (the current "spread" between the official cash rate and rates charged on credit cards was at record levels) is probably a useful piece of work." Sadly, that "..... useful piece of work" failed to materialise at the quarterly October CFR meeting of Australia's three statutory appointed regulators. 7. Below is the only reference to Credit Cards in the RBA's Financial Stability Review - Oct 2015:

8. The word 'competition' appears in the RBA's Quarterly Financial Stability Review - Oct 2015 on 16 occasions. The FSR discussed the following issues mentioning the word 'competition', but not about what APRA Chairman, Wayne Byres told senators "....is probably a useful piece of work." · nominal housing price growth · Funding and liquidity · the owner-occupier part of the mortgage market and in parts of the business lending market. · a further deterioration in banks’ asset quality in conjunction with slower rates of credit growth and the potential for net interest margins to narrow if the liberalisation of interest rates increases price competition for funding. · Household and Business Finances · competition in the owner-occupier lending market remains strong · price competition for business lending · mortgage lending insurance · price competition for new and lower-risk owner-occupier borrowers · competition for new large corporate loans · cost of banks’ domestic deposit funding · Profitability · competition in the mortgage market and the housing price cycle 9. Below are extracts from Reserve Bank of Australia Bulletin - July 1998 - Australia’s New Financial Regulatory Framework that chronicles the Reserve Bank's powers, set out in the Payment Systems (Regulation) Act 1998, that allow the Reserve Bank to undertake more direct regulation of ‘designated’ payments systems to – "... promote competition in the market for payments services, consistent with the overall stability of the financial system..." when it judges it to be "in the public interest" which may involve the imposition of access rules or operating standards for participants in such systems: "The new Payments System Board is responsible for the Bank’s payments system policy, the objectives of which are: • controlling risk in the financial system arising from the operation of the payments system; • promoting the efficiency of payments systems; and • promoting competition in the market for payments services, consistent with the overall stability of the financial system. The Bank’s powers in this area, set out in the Payment Systems (Regulation) Act 1998, allow it to undertake more direct regulation of ‘designated’ payments systems when it judges it to be in the public interest. This may involve the imposition of access rules or operating standards for participants in such systems. The Act also provides a framework for regulation of purchased payment facilities, such as travellers cheques and stored-value cards." |