Writer's CD submission to RBA sent 8 Dec 2011 Defined Terms and Documents

1305, 12 Glen Street 'The

Pavilion'

Milsons Point NSW 2061

0434 715.861

17 August 2017

Senator Nick Xenophon

PO Box 6100

Senate, Parliament House

Canberra ACT 2600

Dear Senator Xenophon

THIS SUBMISSION LETTER IS CONFIDENTIAL TO THE NICK XENOPHON TEAM - FOR THE TIME BEING

A Royal Commission with only Two Terms Of Reference into the 'standout' Unconscionable Product in Australia's Financial Services Industry, namely Credit Cards, in order to reduce the Extreme Financial And Emotional Distress suffered by almost one million Credit Cardholders, identified by the Reserve Bank as Persistent Revolvers, many of whom are Financially Uneducated And Vulnerable Australians

Australian Governments allocate $43.38 million annually to 44 circa charities to provide financial counselling to predominantly Persistent Revolvers.

Time to treat the unconscionable CAUSE and not merely put more bandaids on the often catastrophic EFFECTS

The evidence herein against the Seven Parties named in the Two Terms Of Reference is palpable.

Maurice Blackburn has "...reviewed and considered the material that you provided to us".

A Royal Commission into many facets of the Financial Services Industry would take at least four years to table a report to Federal Parliament and cost several multiples of the forecast $53 million dollars, as the Commissioners investigated over 300 Products and Services delivered by over 130 approx. large companies that employ 500,000 staff circa in the Financial Services Industry, many of which, particularly within Credit Card Products, are highly differentiated. There would be very little of 'comparing apples with apples' to determine what is "...illegal and unethical behaviour and how the financial services industry institutions understood and gave effect to their duty of care to consumers."

Merely considering the banks, there are 37 Australian-owned banks, nine foreign-owned subsidiary banks and another 35 circa branches of foreign banks that collectively provide 200 circa banking Products and Services in Australia. Looking in isolation at only one of the Four Pillars, ANZ Bank with 50,152 employees (in 2015), under 7 Divisions, delivers approx. 200 Products and Services.

However, to ascertain the scope and depth of Labor's sought after royal commission, the Financial Services Industry has Three Sectors that collectively provide over 300 'Products' and 'Services' delivered by approx. 130 companies that employ 500,000 staff circa. That is a lot to understand in order to identify Unconscionable Conduct, pursuant to the 'Warranted Terms' of a Royal Commission, and table it all to Federal Parliament in a robust report.

Australia has had 133 Royal Commissions since 1902, but none previously with the broad terms of reference and density of matters to examine than that announced by the Federal Labor Party in April 2016.

Previous Royal Commissions have been granted both time and budget extensions. In April 2016, Labor pledged a Royal Commission into the Financial Services Industry in Australia that would assertedly cost $53 million over two years, as costed by the independent Parliamentary Budget Office.

How could an independent Parliamentary Budget Office estimate the -

* tax-payer' cost to be $53 million; and

* table-able in Federal Parliament in two years.

when Labor has not announced specific Terms Of Reference, saying it would do so upon taking government?

Empirical evidence of the previous 133 Royal Commissions establishes that the -

* cost estimate could double, triple or quadruple; and

* ultimate tableable for tabling in the Lower House of the Commonwealth Parliament time would double to four years or triple to six years or take even longer.

In order to protect the credibility of the Senators that have supported a Royal Commission, pursuant to the Labor Party's website, an accredited independent third party should review the independent Parliamentary Budget Office assumptions, and scope of investigative works, to opine (for the public domain) on the integrity of the forecast cost of only $53m, to be delivered in two years.

I. By supporting a Royal Commission with only Two Terms Of Reference, looking at only five large banks (and any banks they own) and Two Financial Services Regulators, Labor can establish a robust 'launching pad' for further Royal Commissions into Unconscionable Conduct within specific 'Products' and 'Services' in Australia's Financial Services Industry where time extensions and budget 'blowouts' would not occur

The Labor Party supporting a Royal Commission into the 'standout'' Unconscionable Conduct in Australia's Financial Services Industry, namely Credit Card Products limited to "the Four Pillar Banks now account for around 80 per cent of the credit card market" and Citibank Australia (and any banks they own that provide Credit Cards), would -

A. 'fast track' fees redistribution where the almost ubiquitous User Pays Principle would then also apply to Credit Cards, which the Writer implored the Reserve Bank to implement in his submission to the RBA sent 8 Dec 2011;

B. reduce Predatory Advertising and Numeracy And Literacy Targeting presently evidencing many Financially Uneducated And Vulnerable Australians paying Usurious Interest Rates with no Interest Free Period and usually incurring Late Payment Fees (some also incurring OverLimit Fees), whilst 67% circa of Credit Cardholders, referred to by the Reserve Bank as Transactors, make almost no payment for enjoying a Line/s of Credit for up to 55 days and some receiving Rewards Points; and

C. establish a robust 'launching pad' for further Royal Commissions into Unconscionable Conduct within Specific Products and Services in Australia's Financial Services Industry where time extensions and budget 'blowouts' would not occur.

II.

An SMH article in 2011 was the catalyst to t

The

Writer

opted to research

Credit Card injustices after reading SMH 'Business

Day' article "Middle class hit by debt.....

credit cards bills are taking their toll"

Would you ask one of the Nick Xenophon Team that possesses financial acumen and legal skills to read the below four letters (also listed at the very top of this page) and then mull through some of the 500+ Defined Terms and Documents that the Writer has prepared over the last six years in researching Credit Card Products which uniquely defy the laissez faire market pricing mechanism, known as the User Pays Principle (Your team member/s will need to click on a lot of embedded URLs):

1. Intro Letter to Maurice Blackburn dated 8 May 2017

2. Submission Letter to Maurice Blackburn dated 8 May 2017

3. Second Letter to Maurice Blackburn dated 25 June 2017

4. Maurice Blackburn response letter dated 14 July 2017

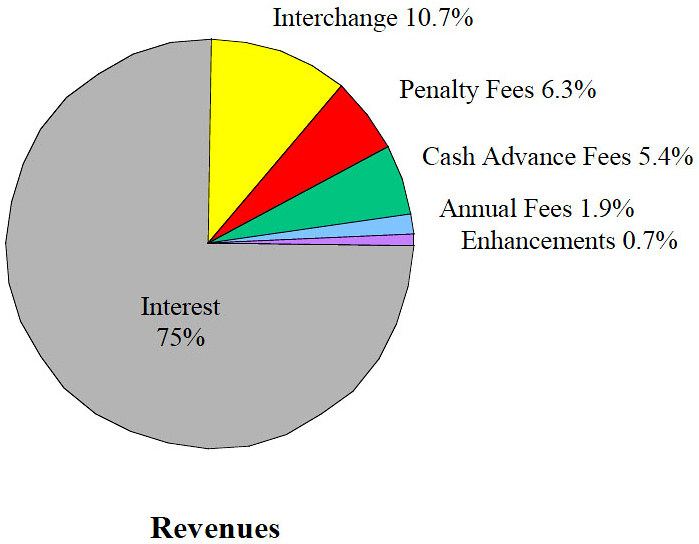

Usurious Interest Rates notes 'inter alia' that the Four Pillars offer Credit Card Products which charge up to -

* 20% on Purchases after expiry of an Interest Free Period which may be up to 55 days from the 'Purchase Date'; and

* 22% on Cash Advances where interest is charged from the date of the Cash Advance, with some also charging an explicit one-off Cash Advance Fee up to $5 or a percentage of the Cash Advance.

Purchase Interest Rate notes 'inter alia' that the -

* highest Purchase interest rate is 25.9% from "Lombard Visa Card Classic"; and

* highest Cash Advance interest rate is 29.49% from G.E. Money's "Go MasterCard"

Mindful that the Cash Rate is only 1.5% and the interest meter is running at exceedingly high interest rates (listed above) after the expiry of the Interest Free Period (or immediately in the case of a Cash Advances), when contemporaneously a Late Payment Fee may also be levied, it is puzzling that only one of the five High Court judges in Paciocco & Anor v the ANZ Bank ruled that a Late Payment Fee is a 'penalty'.

Following the above High Court decision in Paciocco & Anor v the ANZ Bank in in July 2016, Several law firms 'et al' wrote commentaries on the consequences of the majority decision (4 to 1).

Below is a pertinent extract from Coralling the penalties horse: Paciocco v Australia and New Zealand Banking Group Ltd - Melb. Law School - 8 Aug. 2016

"Conclusion – Whither the penalties doctrine?

Paciocco explicitly confirms the continued existence of the penalties doctrine in common law and equity, but one must query whether there is any point retaining it when it has such a narrow application once the law is applied to a particular clause, as in this case. To continue the metaphor, the shutting of the second door has effectively gelded the penalties horse in all but the most extreme cases. And it does not seem that consumers can gain much hope from statute either. Although this post has focused on the common law aspect of the decision, a majority of the High Court found that ANZ had not contravened any statutory provision against unconscionable or unfair terms. This is unsurprising, as what was at issue in this case was not unconscionability in terms of unfair pressure, vulnerability, lack of knowledge or the like. It was an allegation of substantive unfairness of the bargain itself, which seldom gives rise to relief. If Parliament wishes to provide relief for such bargains, it will have to legislate more explicitly."

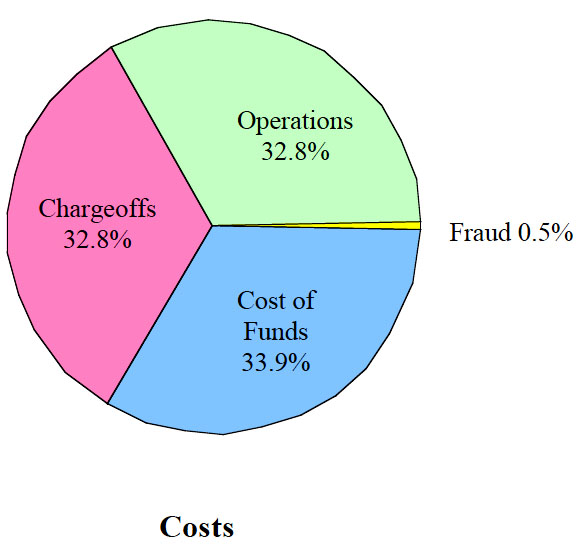

Hence, Parliament has to "...legislate more explicitly..." to provide financial relief by forcing Credit Card Issuers not to impose 'penalties' such as Late Payment Fees that are far beyond Credit Card Issuers' default risk costs, due to their excessive Credit Card Interest Rates. Because the High Court has been unable to understand the quantum and diversity of Revenues and Costs explained in the Writer's Submission Letter to Maurice Blackburn and more so detailed in -

{kind=link}

{kind=link}

* Grounds/Reasons for the 13 Written Question re Credit Cards; and

* Written Questions re Credit Cards

Many Credit Card Issuers charge Usurious Interest Rates on the Total Amount Owing for the Previous Month's Purchases -

* even if the 'Repayment' is only $1 short of the Total Amount Owing, or

* the 'Repayment' is one day after the Payment Due Date.

Some Credit Card Issuers then cancel the Interest Free Period for the two subsequent months (Example 1), whereupon interest is charged at the Purchase Interest Rate from the date of each Purchase for each and every Purchase over the subsequent two months.

Predatory Advertising by too many Credit Card Issuers has evidenced Unconscionable Conduct, because -

(I.) the Financial Literacy 'strong' have exploited the Financial Literacy 'weak';

(II.) Our competition is getting away with it, so why shouldn't we do it as well; and

(III.) Two of Australia's Three Financial Services Regulators have been patently conflicted and derelict and when they have made reforms it has been many years to late, and only after the UK. has acted..

III. In Dec 2001, the Reserve Bank published a Consultation Document titled "Reform of Credit Card Schemes in Aust" that advocated the User Pays Principle be better applied to Credit Cards

As chronicled in the Writer's Submission Letter to Maurice Blackburn dated 8 May 2017, back in 2001 the Reserve Bank released "RBA's Reform of Credit Card Schemes in Aust: "Consultation Document" – Dec 2001 which announced:

towards a 'user pays' approach to credit card payment services would be consistent with the approach adopted by Australian financial institutions in pricing other payment instruments under their control. It is also fairer and efficient, because consumers only pay for what they use.”"Reform of credit card schemes will also have a direct impact on credit cardholders and is likely to result in some re-pricing of credit card payment services. However, this is the means by which the price mechanism is to be given greater rein in the credit card market. A movement

History evidences that the Reserve Bank, with it's Extensive Powers and Responsibilities to ALL Australians, did not put up a fight back in 2002 to "....re-price credit card payment services to... be .....consistent with the approach adopted by Australian financial institutions in pricing other payment instruments under their control."

"The Reserve Bank is the principal regulator of the payments system through the PSB." Section 3 of Extensive Powers and Responsibilities of the RBA to ALL Australians chronicles that the Reserve Bank -

A. possesses enormous powers to gather financial information from ADIs; and

B. carries responsibilities to 'inter alia' "best contribute to.......... the economic prosperity and welfare of the people of Australia",

far beyond those of the USA central Bank or the UK Central Bank. Point 3 of 'Extensive Powers and Responsibilities of the RBA' evidences that the Reserve Bank has explicit obligations/responsibilities to Revolvers, whereas the U.S. Federal Reserve or the Bank of England do not..

The Writer's CD submission to RBA sent 8 Dec 2011 thought that the RBA would want the User Pays Principle applied to Credit Cards, although at the time of writing it in Dec 2001, the Writer was not aware of the above "Consultation Document" – Dec 2001 that advocated that the User Pays Principle be better applied to Credit Cards. The RBA did not respond. Up until posting that CD submission to the RBA, the Writer had enjoyed fruitful discussion emails with:

Ms. Sharon van Etten

Public Relations Officer, Media & Public Relations OfficeReserve Bank of Australia

Nine Examples of Unconscionable Conduct in Labyrinth of ‘Concealed Spiders’ is probably the most material evidence against term 1. of Two Terms Of Reference. Tony Devlin, who featured in the SMH article, Middle class hit by debt, or most of the 'Credit Card Distress' Authorities could point out other patent Predatory Advertising of Credit Cards that 'inter alia' Target Credit Cardholders With Low Financial Literacy Capacity and often land them into much more debt than they envisaged from the tactfully presented advertisement .

IV. A separate consequence from a lack of competition due to The Four Pillars enjoying Oligopoly dominance

Looking beyond Credit Card Products, Chapter 12 explains that the Australian banking industry has consolidated substantially since Campbell recommended deregulation from 1980. The Four Pillars continue to announce record profits, but Australia's Three Regulators for Financial Services have not displayed any interest in whether any of the Four Pillars are exploiting their unique Oligopoly market conditions by not paying interest on transaction bank accounts, but rather often charging an account keeping fee $5p/m circa. When the Writer commenced working for CBA in 1970 a passbook account paid 3.75% pa interest. Banks' mainframe computer systems have materially reduced in cost since the legacy mainframe EDP systems of the '80's and 90s.

Former Reserve Bank employee, and now Crikey finance journalist, Peter Mair, in his SUBMISSION TO SENATE STANDING COMMITTEE ON ECONOMICS dated 17 July 2015 noted that the Four Pillars hold 'depositors balances' of " ... one trillion dollars ..." approx that pay no interest:

"Ponder the consequences of banks, mainly the Four Pillars, now holding some $1,000 billion -- that’s one trillion dollars – in transaction deposit accounts on which no interest of material consequence is paid to depositors but which, invested by banks, returns market-rate revenue to banks."

The Reserve bank provides a welter of statistical data reporting on Credit Cards and depositors' balances at Statistical Tables. Alas, that behemoth of numerical reporting provides negligible meaningful information about -

(i) which demographic cohorts are paying a disproportionate share of Credit Card delivery costs and profits; and

(ii) the quantum of funds held in zero interest paying bank accounts, and the component (for a particular month) that is charged a monthly fee of $5 or more.

Little wonder CBA was able to pay its CEO, Ian Narev, an extraordinary $12.3m total rem for the 12 months to 30 June 2016. The dark cloud of the GFC did had a 'silver-lining'. The 'blue sky' was that the Four Pillars lost their competition:

-

Westpac acquired Rams Home Loans and St. George Bank. Westpac and St. George should never have been permitted to merge in 2008.

-

CBA acquired Bankwest under "Project Magellan" for $2.1b in 2008.

In summary, the Four Pillars enjoy a unique competitive advantage that no other banks in the Western world benefit from.

V. Conclusion

The Writer beseeches you to enthuse the Labor Party to support meaningful assistance to almost 1,000,000 Credit Cardholders, that the Reserve Bank has identified as Persistent Revolvers, by supporting this request for a Royal Commission with only Two Terms Of Reference, because the evidence that the Writer recently provided to Maurice Blackburn (of Unconscionable Conduct and inept, painfully slow to regulate, and conflicted regulation - in 1. 2. and 3 of II. above) is substantial and material.

There may be merit in the Nick Xenophon Team seeking Maurice Blackburn's opinion and thoughts on that evidence.

Prior to posting this letter (in two DVDs and a USB stick) to you on 17 August 2017, the Writer posted a DRAFT of this letter to Mr. Julian Schimmel (who signed Maurice Blackburn response letter dated 14 July 2017) at Maurice Blackburn a week earlier on 9 August 2016 to put Julian Schimmel, in the loop, notably that -

(A) the Writer intended to approach a member of Parliament, albeit not his local member; and

(B) the Nick Xenophon Team might seek Maurice Blackburn's opinion and thoughts on the Writer's Submission Letter to Maurice Blackburn dated 8 May 2017, in particular the materiality of -

* Unconscionable Conduct by some Credit Card Issuers in Nine Examples; and

* Two Financial Services Regulators breaching their respective Statutory Duty and Fiduciary Duty.

NB: SMH - 31 May 2016 - Fancy dress financial regulators ASIC and APRA must go

Yours sincerely