|

|

CONFIDENTIAL CONFIDENTIAL CONFIDENTIAL CONFIDENTIAL CONFIDENTIAL Defined Terms and Documents Discussion Paper regarding regulatory responsibilities over Credit Card Products primarily addressing breaches of Statutory Duty by the RBA as Principal Regulator of the Payments System through its Payments Systems Board that possesses investigative powers "unique among central banks" 1. T he below sentence in ABC News article What lies ahead for the property market this year: more apartments and low interest rates (Peter Lasker - RBA has done a masterful job of hoodwinking and bamboozling a lot of Australians, not limited to financial journalists:"The banking royal commission highlighted the lending excesses that helped fuel a property boom with the blessing of regulators and the Reserve Bank."2. The RBA lied to a Senate Economics Legislation Committee in June 2015 regarding its Extensive Powers and Responsibilities to ".... promote competition in the market for payment services" for Credit Card Products for ALL Australians - Section 7 below 3. Banks blasted for “unconscionable” credit card lending at Senate enquiry 4. Prime Minister, Scott Morrison, acknowledged on 22 June 2017 that "...unfair and predatory practices..." have existed with Credit Cards in "Protecting Aussies from predatory credit card practices" whilst under the watch of the Principal Regulator of the Payments System 5. The Hayne Royal Commission did not resolve the most abundant injustice in banking; many Credit Card Issuers have applied Predatory Marketing (evident in Unconscionable Credit Card Advertising and Unconscionable Credit Card Interest Charging) that targeted Financially Uneducated And Vulnerable Australians; many have suffered Extreme Financial And Emotional Distress - acknowledged by the P.M. in 4. above 6. Relying on Section 50 of the Banking Act 1959 'et al' Two Effortless Legislative Changes could have corrected 20+ years of negligence by the RBA as Principal Regulator of the Payments System that itself acknowledged those problems many years ago in Six Pivotal Credit Card Publications - Section 6 below Preface The Writer posted his 1st Submission Letter to Maurice Blackburn on 8 May 2017 and his 2nd Submission Letter to Maurice Blackburn on 25 June 2017 (on DVD) beseeching it to launch a Class Action representing 400,000 circa Eligible Persistent Revolver Plaintiffs against the RBA for breach of its Statutory Duty and Fiduciary Duty. The Writer's Labyrinth of ‘Concealed Spiders' provided nine examples of Unconscionable Conduct by Credit Card Issuers of Predatory Advertising their various Credit Card Products to extricate maximum Interest and Penalty Fees Revenue from Financially Uneducated Credit Cardholders which constitutes Numeracy And Literacy Targeting.

His allegations are acknowledged in Quotes from reputable Credit Card Distress Authorities about unconscionable advertising of some Credit Cards by some Credit Card Issuers resulting in some indebted Credit Cardholders being issued multiple Credit Cards.

Maurice Blackburn’s response letter to the Writer dated 14 July 2017 included:

"Conclusion In our view there would be legal risks associated with a claim in relation to the circumstances outlined in your letter and for this reason the proposed claim does not meet our criteria for the pursuit of a class action. Although it may be the case that financially vulnerable consumers are at risk when it comes to credit card products, we think that the concerns outlined in your letter would be best addressed by legislative or regulatory change that is designed to protect the interests of these consumers. In this regard, we suggest that you contact your local Member of Parliament to continue your advocacy on behalf of vulnerable consumers." 1. Two Purposes of this Letter to BRN 1st Purpose of this Letter to BRN This letter chronicles that the RBA has abrogated its Statutory Duty and Fiduciary Duty in particular to Persistent Revolvers by not drawing upon its 'extensive powers' to recommend to the Federal Govt. as required under Section 11(1) of the Reserve Bank Act 1959 to set new Standards, pursuant to Division 4, Section 18, to - A.) force Credit Card Issuers to apply the User Pays Principle to user costs/fees because Credit Cardholders with poor Financial Literacy Capacity pay the Line/s of Credit Costs of Credit Cardholders with high Financial Literacy Capacity identified by the RBA as Transactors; and B.) re-regulate a maximum interest rate for Purchases and re-regulate a maximum interest rate for Cash Advances, under Section 50 of the Banking Act 1959 as amended for "Control of interest rates", with the approval of the Federal Treasurer, as requested by the Writer in Section 8 A) to H) of his CD Submission to the RBA dated 8 Dec 2011 after the Writer had earlier shared emails with Ms. Sharon van Etten, Public Relations Officer, Media & Public Relations Office, RESERVE BANK, Ms. van Etten's email sent 10 Nov 2011 re the RBA's powers over Credit Card Issuers.

This letter provides irrefutable evidence that - 1. then RBA employee, Ms. Sharon van Etten, political Journos and Senate Committees have been hoodwinked, because comprehending Parliamentary Acts, MOUs, and understanding the 'history' of the RBA's previous regulation of interest rates (also Section 3 below) has been beyond them; and 2. more recent senior RBA executives have been spineless to the detriment of, in particular vulnerable Persistent Revolvers, because as the plight of Persistent Revolvers worsened with the 'spread' between the cost of funds and interest rates of Predatory Credit Cards further widening, the RBA has asserted Nothing to do with us! Our mandate is solidarity of the banking system. Yet as the below facts evidence, the RBA has been complicit with the Credit Card Issuers that it was legislated to regulate.

Post Hayne Royal Commission, many Credit Card Issuers continue to apply Predatory Marketing targeting Financially Uneducated And Vulnerable Australians; many have suffered Extreme Financial And Emotional Distress. Relying on Section 50 of the Banking Act 1959 'et al' Two Effortless Legislative Changes (Section 6 below) can correct 20+ years of neglect by the Principal Regulator of the Payments System recognised/acknowledged in Six Pivotal Credit Card Publications (Section 5 below).2nd Purpose of this Letter to BRNThe Writer has prepared Thirty Two Written Questions (and the Supporting Documented Evidence) for the next Federal Govt. to extend the Royal Commission to address breaches of Statutory Duty, ostensibly by the RBA (Principal Regulator of the Payments System) and minimally by APRA or ASIC (Council of Financial Regulators) in NOT facilitating the RBA Setting New Standards for Credit Card Products, because of Predatory Marketing of Credit Cards that - a) have charged Usurious Interest Rates involving Numeracy And Literacy Targeting of Credit Cardholders that possess level 1 (or below) and level 2 Financial Literacy Capacity - identified by the Productivity Commission and the ABS; andb) Unconscionable Credit Card Interest Charging which was finally banned by the ABA under its latest Code of Practice ("commences 1 July 2019" after 20+ years of avarice exploitation where Credit Card "Customers (now) only paying interest on what remains on a credit card (after expiry of any Interest Free Period) and not the full amount of purchase if a loan is being paid down", but may still forfeit their Interest Free Period for up to two months after repaying any Outstanding Indebtedness.2. The RBA is the principal regulator of the payments system through its Payments System Board - with powers "unique among central banks" The RBA shoulders patent and unambiguous obligations under Parliamentary Acts to ".... promote competition in the market for payment services" for ALL Australians - which includes Credit Cardholders (identified by the RBA as Persistent Revolvers) - many have suffered Extreme Financial And Emotional Distress. Section 6 below establishes unequivocally that the Credit Card System falls within the province of the Payments System. Extensive Powers and Responsibilities of the RBA to All Australians notes that - * "The Reserve Bank is the principal regulator of the payments system through the PSB"; * details the RBA's obligations and responsibilities to ALL Australians, in particular "control of interest rates"; and

* informs that the RBA's - A. powers to gather financial information from ADIs; and B. responsibilities to 'inter alia' "best contribute to.......... the economic prosperity and welfare of the people of Australia",

Below is a brief extract from description of the Reserve Bank of Australia (RBA) by Clayton Utz:

The UK Guardian article 'The interest-free credit card trap snaring unwitting borrowers' is rife with examples of UK Credit Card Issuers' Predatory Marketing directed at Financially Uneducated And Vulnerable Credit Cardholders that Lack Financial Acumen. There is a welter of evidence that U.S. Credit Card Issuers are not immune from similar Unconscionable Credit Card Advertising.

One could presuppose: "Well why shouldn't it be any different in Australia?" It SHOULD be different in Australia, because Australia's 'central bank' has unique powers and exceptional responsibilities "...to.......... the economic prosperity and welfare of the people of Australia" and for its Payments Systems Board to always Act in the Public Interest; unique powers of the PSB not held by the 'central bank' of the UK or the USA - explained above.

3. Prior to the Campbell Report circa early 1980's, the RBA regulated all bank interest rates with an Iron Fist - "... when de-regulation resulted in adverse consequences, re-regulation ensued..." The Unpleasant Truth About Australian Banking notes:"Before 1981, activities of major Australian banks, including the manner they dealt with customers, were subject to detailed regulations imposed by the Federal Government. Following the 1981 Campbell Committee Report, banking regulations were significantly reduced." The Reserve Bank and its then predecessor, the Govt. owned Commonwealth Bank, had increasingly regulated 'with an iron fist in a velvet glove' the commercial banks since 1911. Historically when de-regulation resulted in adverse consequences, re-regulation by Australia's 'central bank' ensued. Below is an extract from 'Overview of Financial Services Post-Deregulation' by (Dr) Diana Beal, Director, Centre for Australian Financial Institutions, University of Southern Queensland, Toowoomba, 2002:

Below is an extract from the bottom of page 7 of University of Wollongong 'Economics Working Paper Series 2012': Chapter 5 and Chapter 17 note inter alia that between 1960 and 1980 the Reserve Bank diligently regulated Australian commercial bank interest rates relying on Section 50 of the Banking Act 1959 as amended. Chapter 5 chronicles that when the max 18% interest rate cap was removed in April 1985 by the RBA, the Overnight Money Market Interest Rate was less than 1% lower - a whisker over 17%. The highest Cash Advance interest rate is now 29.49% for a 'Go' Credit Card from Latitude Financial. That is 28.50% higher than the current Overnight Money Market Interest Rate of 1%. 4. In 1988 the RBA received further extensive powers over any Payments System that it Designates and it then Imposes an Access Regime as it can then request information re transaction activity, pricing profits and/or impose new Standards in order to promote competition Thirteen years after the RBA removed the 18% interest rate cap on all Credit Cards, the RBA received additional 'extensive powers', set out in the Payment Systems (Regulation) Act 1998, that allowed the Reserve Bank to undertake more direct regulation of Designated Payment Systems to – "... promote competition in the market for payments services, consistent with the overall stability of the financial system..." when it judges it to be "in the public interest" which may involve the imposition of access rules or operating standards for participants in such systems: "The new Payments System Board is responsible for the Bank’s payments system policy, the objectives of which are: • controlling risk in the financial system arising from the operation of the payments system; • promoting the efficiency of payments systems; and • promoting competition in the market for payments services, consistent with the overall stability of the financial system. The Bank’s powers in this area, set out in the Payment Systems (Regulation) Act 1998, allow it to undertake more direct regulation of ‘designated’ payments systems when it judges it to be in the public interest. This may involve the imposition of access rules or operating standards for participants in such systems. The Act also provides a framework for regulation of purchased payment facilities, such as travellers cheques and stored-value cards."

5. The below four RBA detailed publications cited in A.) & B.) below evidence that the RBA "talked it", but to the financial and emotional detriment of vulnerable Persistent Revolvers, failed to "walk it":

Most of the above Six Pivotal Credit Card Publications evidenced that Credit Card Issuers had engaged in Predatory Sale Of Financial Products involving Numeracy And Literacy Targeting of Credit Cardholders that possess level 1 (or below) and level 2 Financial Literacy Capacity, whereupon many had become Revolvers (61.87 circa Occasional Revolvers and 38.13% circa Persistent Revolvers) that have paid Usurious Interest Rates which is contrary to the RBA's parliamentary decreed role to ensure "...the economic prosperity and welfare of (all) the people of Australia".

6. Because the RBA Designated and subsequently Imposed an Access Regime over Credit Card Issuers in Australia, - a) ACCC's responsibilities to ensure competition between Credit Card Issuers were subrogated to the RBA; and b) RBA could have set new Standards to - A.) enforce the User Pays Principle to Credit Card Issuers B.) re-regulate a maximum Credit Card interest rate, because four Pivotal RBA Discussion Papers collectively recommended A.) and detailed the burden on Persistent Revolvers of the massive spread between the Cash Rate and Usurious Credit Card Interest Rates, whereupon B.) above should have been re-regulated yonks ago as evident in the blue table midway down Chapter 5

The above two overt actions/steps by the RBA subrogated responsibility for ensuring competition from the ACCC to the RBA - explained in MOU dated 8 Sept 1998 and The Reserve Bank had 'lined up all the requisite wood ducks' to set Standards for Credit Cards.The RBA -

The below analysis of steps 1. 2. and 3 (immediately above) behove the Reserve Bank to have relied upon - * Division 4, Section 18 of the Payments System Regulation Act 1998 to make new 'Standards' for payment systems that "are in the public interest"; of the Banking Act 1959 as amended for "Control of interest rates" to, with the approval of the Treasurer, make regulations; and* Section 8 'Meaning of public interest' of the Payments System Regulation Act 1998 in particular "The Reserve Bank may have regard to other matters that it considers are relevant, but is not required to do so",to re-regulate a maximum interest rate on Credit Cards (explained in Chapter 17) after it published LOAN RATE STICKINESS: THEORY AND EVIDENCE (in June 1992 - 27 years ago - written by the present Governor of the Reserve Bank, Phillip Lowe and Thomas Rohling) which established that Credit Card interest rates were 'sticky':· "The rate on credit cards is found to be the most sticky followed by personal loan rates, the housing loan rate and the small business overdraft rate.· In contrast, the rates on personal loans and credit cards do not appear to be more flexible in the deregulated period." Rationale:

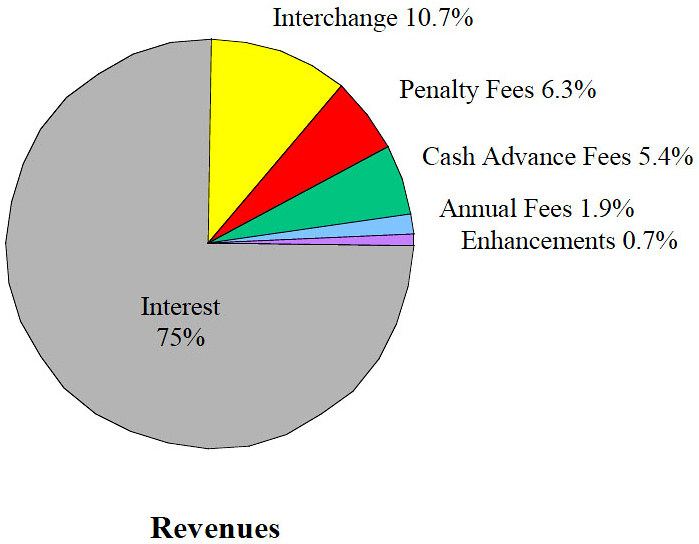

(a) The blue table midway down Chapter 5 establishes that the spread between the Wholesale Cost Of Funds and Standard Credit Card Purchase Interest Rate has widened and widened and further widened:* was less than 1% when the 18% cap was removed in April 1985 * was 10% in 2001 * was 18.5% in March 2017; AND (b) Persistent Revolvers that hold 12.58% circa of the 16.686 million Credit Cards held by Credit Cardholders in Australia often with Level 1 or less Financial Literacy Capacity have suffered Extreme Financial And Emotional Distress and contributed 80% circa of all Interest and Penalty Fees Revenue to Credit Card Issuers of which 80% of all Revenues to Credit Card Issuers from Credit Card Products is Interest and Penalty Fees Revenue; ipso facto Persistent Revolvers that hold only 12.58% circa of the 16.8m Credit Cards held by Credit Cardholders are paying 64% of all Revenues from Credit Card Products - get that, 12.58% circa of Credit Cards are paying 64% of all Revenues and the Reserve Bank is aware of detailed written reports by the Productivity Commission, ABS and ASIC (that date back to 2006) re the material disparity in Financial Literacy Capacity across Credit Cardholders (Chapter 1).

Re (a) above, Highest Interest Rate Credit Cards and Australia’s most predatory credit cards revealed evidence that many Credit Card Issuers offer Credit Cards that charge well above the Standard Credit Card Purchase Interest Rate.

Below are two extracts from Westpac's sub mission to the Wallis Inquiry, submitted by the then CEO, Bob Joss, who anticipated the effect of Credit Card Issuers enjoying a free run (post Wallis) at Credit Cardholders with poor Financial Literacy Capacity:

Consequently, the RBA Board, and also the Payments Systems Board, has each abrogated its Statutory Duty and Fiduciary Duty, in particular to Persistent Revolvers, many of whom are Financially Uneducated And Vulnerable Australians, by not recommending for 'public interest issues' to the Federal Govt, as required under Section 11(1) of the Reserve Bank Act 1959, to exercise their 'extensive powers' over the Credit Card Payment Schemes by setting new Standards, pursuant to Division 4, Section 18 to -A.) regulate "a User Pays pricing to credit card payment services" because it - * published Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001 that recommended " A movement towards a “user pays” approach to credit card payment services would be consistent with the approach adopted by Australian financial institutions in pricing other payment instruments under their control. As the ABA itself has confirmed: “Pricing services efficiently provides consumers with choice to use lower cost distribution channels and, therefore, facilitates a more efficient financial system. It is also fairer and efficient, because consumers only pay for what they use.198"; and* received the Writer's CD submission to RBA sent 8 Dec 2011 that argued that banks profits from credit cards on the Retail Supply Side did not accord with the User Pays Principle because Credit Cardholders with poor Financial Literacy Capacity were paying the costs of Credit Cardholders with high Financial Literacy Capacity - the Writer's CD submission included Section 8 A) to H) to ensue that User Pays;and B.) re-regulate a maximum interest rate for Credit Card Purchases and a maximum interest rate for Credit Card Cash Advances after Three Landmark RBA Published Papers in the last 26 years that recognised the increasing spread between the Overnight Cash Rate and Highest Credit Card Interest Rates because of the financial burden falling upon Persistent Revolvers that invariably possess low Financial Literacy Capacity and are perpetually paying Usurious Interest Rates. An Unconscionable 80% circa of all Interest And Penalty Fees Revenue levied by Credit Card Issuers annually is paid by Persistent Revolvers.

Re B.) above, below is an extract of Section 8 A) to H) of the Writer's CD Submission to the RBA dated 8 Dec 2011:

Mindful that the RBA regulated many retail interest rates with and Iron Fist until the Campbell Report in the early 1980s, why would the RBA make such written admissions about vulnerable Credit Cardholders in the above Six Pivotal Credit Card Publications and then fail to recommend to the Federal Govt both A.) and B.) above? Prima facie such behaviour from Australia's 'central bank' is non-sensical! It is intriguing that the RBA would not address Unconscionable Conduct by some Credit Card Issuers evident in those publications.

The RBA abrogated its obligation to recommend A.) and B.) above to the Federal Govt. (required under Section 11(1) of the Reserve Bank Act 1959) to set new Standards, pursuant to Division 4, Section 18, where - (i) Credit Cardholders with poor Financial Literacy Capacity pay the costs of Credit Cardholders with high Financial Literacy Capacity; and (ii) Transactors do not pay the full cost of their Revolving Lines of Credit, and RBA written publications pointed out that Unconscionable Conduct.

The Reserve Bank had 'lined up all the requisite wood ducks' to set Standards for Credit Cards to 'inter alia' set a maximum Purchase interest rate and a maximum Cash Advance interest rate for 'public interest issues' (To Act In The Public Interest). But seemingly it has never opted to recommend the re-introduction of an interest rate cap on Credit Cards that existed until April 1985 because of the massive variance between the 1% Overnight Cash Rate and the plethora of Credit Cards that charge 20% right up to 29.49% for a Cash Advance.

Australia's 'central bank' has never exercised its rights - * under Part 5—Miscellaneous, Section 26 of the Payment Systems (Regulation) Act 1998 to ask for meaningful financial data from the major Credit Card Issuers of Interest & Penalty Fees revenue for each of their Credit Cardholders for all Credit Card Products for a minimum of 12 months in order to establish if the User Pays Principle applies, notwithstanding that the RBA argued for greater application of the User Pays Principle in its paper "Reform of Credit Card Schemes in Aust: "A Consultation Document" in Dec 2001; or * under Section 11(1) of the Reserve Bank Act 1959 to " ....inform the Government, from time to time, of the Bank's monetary and banking policy" having regard to its obligations under Section 10(2) '* the RBA recommended in Dec 2001; and * the Writer recommended in Section 8 of his letter (on CD) to the RBA dated 8 Dec. 2011 - explained in Point 9 of Supporting Evidence re 1st Question. 7. In June 2015, the RBA lied to a Senate Economics Legislation Committee investigating high Credit Card Interest RatesOn 1 June 2015 (then soon to retire) RBA Assistant Governor (Financial System), Dr. Malcolm Edey, bald faced lied to a Senate Economics Legislation Committee into high Credit Card Interest Rates (chaired by then Senator, Sam Dastyari, and Senator, Nick Xenophon) when Dr. Edey responded to a question from Sam Dastyari: "... we do not have an interest rate regulator in Australia............... What we do have is an ACCC that can investigate uncompetitive conduct if they see it, but they clearly have not seen it in this market. ............................. We do not have laws for the regulation of interest rates." But as explained above, if the Reserve Bank Designates a Payments System and then Determine Standards (or sets new Standards) for that Payments System, all the obligation to ensure competition are subrogated from the ACCC to the Reserve Bank's Payments Systems Board that is thereby chartered/legislated/regulated to set new Standards to always Act in the Public Interest; unique powers of the PSB not held by the 'central bank' of the UK or the USA. This critical subrogation - explained in MOU dated 8 Sept 1998 - has been obfuscated by the RBA and overlooked by all and sundry.8. Thirty Two Written Questions and the Supporting Evidence for a second Royal Commission into Credit Cards

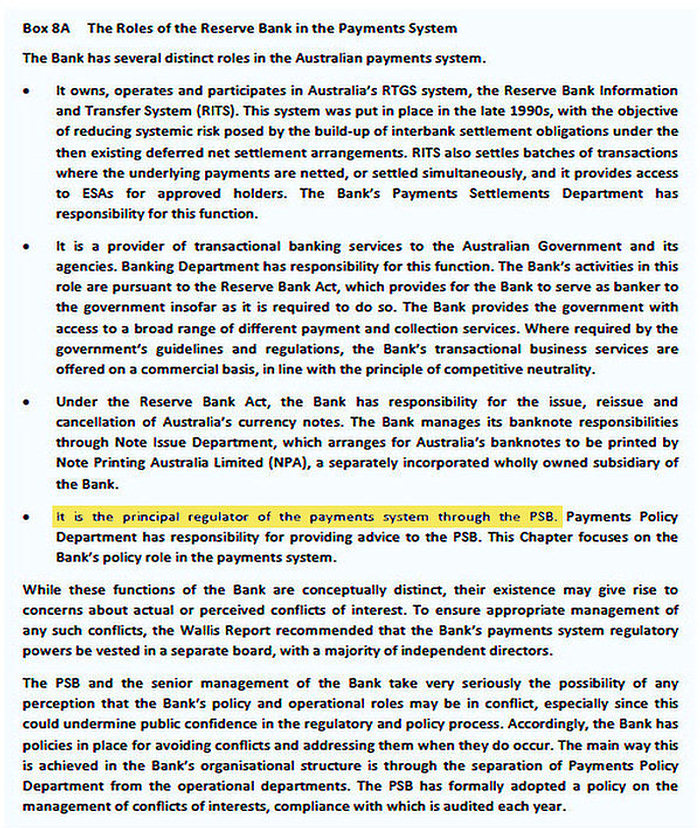

The Writer has prepared Thirty Two Written Questions (and the Supporting Documented Evidence) for the next Federal Govt. to review when considering a Second Royal Commission regarding breach of Statutory Duty, ostensibly by the RBA (Principal Regulator of the Payments System) and minimally by APRA or ASIC in NOT Setting New Standards for Credit Card Products: * 14 Questions to ask the Governor of the Reserve Bank of Australia as the RBA's Submission to the Financial System Inquiry - March 2014 declared it to be the Principal Regulator of the Payments System through the PSB in Box 8A: The Roles of the Reserve Bank in the Payments System* 2 Questions to ask the Chair of the Council of Financial Regulators * 2 Questions to ask the Chair of APRA * 1 Question to ask the Chair of ASIC

*

2 Questions to ask

Chair of the

ACCC * 10 Questions that ask the Royal Commissioner to implement material changes re Credit Card Products 32 Regarding Section 7 above, read Question 5 and Supporting Documented Evidence re Question 5 in Thirty Two Written Questions.Unfortunately, because the Writer had not personally suffered a loss from a financial product or advice, his Thirty Two Written Questions did not meet the Terms of Reference for Submissions to the Royal Commissioner. He sent several emails to the Royal Commission that provided his evidence of inter alia negligence and misconduct by financial regulators, particularly the RBA, but he didn't receive a response. Yours sincerely Phil Johnston aka Bank Teller |

|

|

|

{kind=link}

{kind=link}