|

|

Insert one of the two enclosed DVDs into a Windows PC to auto-open this page. Left click on it and then left click on the welter of embedded URLs in Blue Text or Red Text to open associated files. To leave a page and return to the previous page, click on the arrow at top left of your screen/monitor.

If this page accidentally closes when you leave another page, right click on

your DVD Drive icon and left click on 'Open Auto Play'.

If using a MAC, or the enclosed USB stick, or the enclosed DVDs do not auto-open this letter, then navigate to

CreditCards/SMH/Shane_Wright/Letter_to_Shane_Wright_8-Apr-21.htm.htm

1305, 12 Glen St -

The Pavilion on the Harbour' scribepj@bigpond.com 0434 715.861 8 April 2021

Shane Wright Department of Applied Finance 4 Eastern Road,

Macquarie University

Late last year Paul Keating asserted that he has done more to induce the "Reverse Bank" to take action on controlling interest rates, than anyone else had.

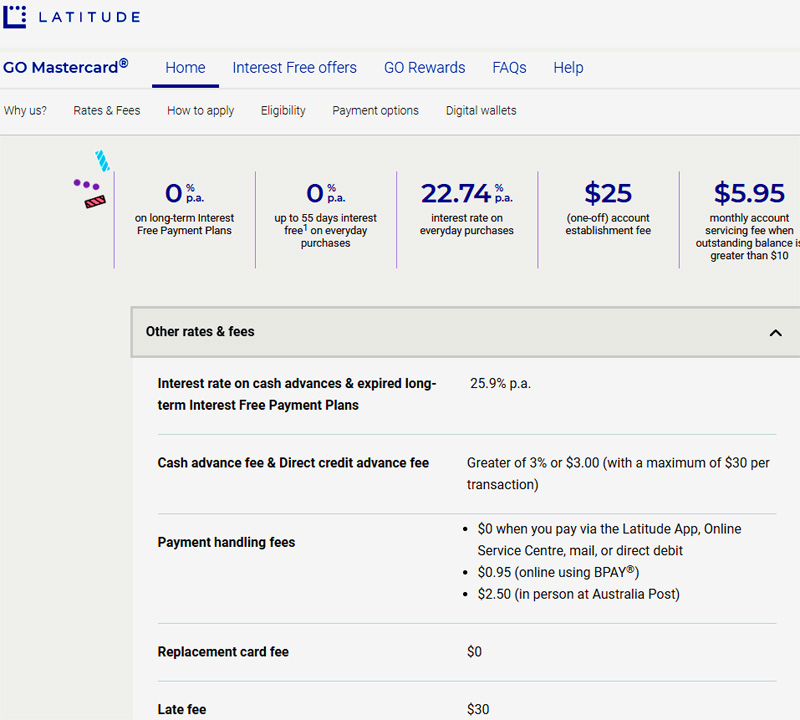

After talking to and emailing Paul Keating's PA, susan.grusovin@aph.gov.au, the Writer's Letter to Paul Keating dated 28 Oct 2020 (on DVD, USB and A4) - A. set out the Parliamentary bestowed Extensive Powers and Responsibilities to ALL Australians conferred upon the RBA by Parliamentary Acts, together with various undertakings and representations the RBA has made in Three 'Landmark' RBA Published Papers; and B. provided patent evidence that the Reserve Bank has breached its Statutory Duty and Fiduciary Duty to Credit Cardholders with poor Financial Literacy Capacity (400,000 circa of them) for inter alia not informing the Federal Govt. as far back as late 1992 (obligated under Section 11(1) of the Reserve Bank Act 1959) that it (the RBA) needed to re-impose a maximum interest rate Cap (limit) on Credit Cards because the spread between the Overnight Cash Rate and the Purchase Interest Rate exceeded 16% (in June 1992). Whereas when the 18% interest rate cap on all Credit Cards was removed by the RBA in April 1985, the spread was less than 1%, which is why that 18% cap was removed. The spread between the current Overnight Cash Rate of 0.10% and the highest Cash Advance interest rate (Latitude Financial's Go Mastercard) is now appallingly over 28% (25.9% + 3% - 0.10%) = 28.8%. Upon receiving the Writer's extensive letter setting out his concerns about the RBA's negligence to Credit Cardholders with poor Financial Literacy Capacity, should the former Labor Prime Minister have rebuked the RBA for not re-imposing a maximum interest rate Cap (as far back as June 1992) on all Credit Cards, in order to halt the pillaging of Financially Uneducated And Vulnerable Credit Cardholders, identified by the RBA as Persistent Revolvers? Or did Mr. Keating ponder that he and the Labor Party might be criticised for not so imploring the RBA back in June 1992 to re-impose a Cap because of its Statutory obligation under Section 11(1) of the Reserve Bank Act 1959.

The Writer is chuffed that your recent article The central bank under fire: Has the RBA failed Australians? includes "... furthering the “economic prosperity and welfare of the people of Australia”, because the Writer had thought that no journalist understood the legal obligations of Australia's Principal Regulator of the Payments System to the “economic prosperity and welfare of (ALL) the people of Australia” which includes Credit Cardholders, identified by the RBA as Revolvers, that pay Credit Card Issuers delivery costs of the Lines of Credit enjoyed by Transactors.

In May 2020, Choice CEO, Alan Kirkland, asserted that Credit Card Providers have stolen $6.3 billion from customers “by failing to pass rate cuts on for credit cards, banks have effectively stolen $6.3 billion from the pockets of Australians,” Mr Kirkland said. * "The 10 costliest credit cards in Australia – and why you should avoid them like the plague" - CHOICE

Paul Keating recently spurned the RBA to follow the 'long lead' of several 'central banks' to increase their fiscal pot, by buying long dated Govt. bonds from new electronically created money sourced 'out of the ether' - QE. In light of the below assertion, the former Labor Prime Minister should be concerned about the plight of hundreds of thousands of Persistent Revolvers that represent a mere 12.58% circa of all Credit Cardholders, yet contribute a whopping 80% circa of all Interest And Penalty Fees Revenue generated from Credit Card Products, often suffering Extreme Financial And Emotional Distress: "No one in Australian public life had done more to lift up the Reserve Bank while giving it a singular discretion over interest rates than I did. And no one carried a greater cost of it." 67% of Credit Cardholders, identified by the RBA as Transactors, enjoy their Lines of Credit by regularly using their Credit Cards at virtually no financial cost, even though the RBA has previously asserted that the User Pays Principle should apply to Credit Card Products. The other 33% of Credit Cardholders, identified by the RBA as Revolvers, pay Credit Card Issuers delivery costs of Lines of Credit enjoyed by Transactors. Why has none of Australia's venerated constitutional lawyers 'called out' Australia's Principal Regulator of the Payments System for breaching its Statutory Duty and its Fiduciary Duty to "best contribute to.......... the economic prosperity and welfare of (ALL) the people of Australia" due to the RBA not recommending to the Commonwealth Govt (under Section 11(1) of the Reserve Bank Act 1959) that it (RBA) re-impose a maximum interest rate Cap on Credit Cards when as far back as June 1992 the spread between the Overnight Cash Rate and the average Purchase interest rate exceeded 16%? That Cap had stood at 18% until it was removed in April 1985 the spread/margin between Overnight Cash Rate and that 18% Cap was less than 1%.Prior to the Campbell Report circa early 1980's, the RBA regulated all Australian bank interest rates with an Iron Fist dating back to the failure of banks in the 19th century - "... when de-regulation resulted in adverse consequences, re-regulation ensued...". The Writer attributes the deft silence from constitutional lawyers and legal academia that a Cap should be re-imposed to protect Financially Uneducated And Vulnerable Australians is due to ignorance, apathy and an unwillingness to challenge a division of government, when government directly or indirectly has fed many of them.On 24 Sept 2020, Paul Keating delivered a letter to the media that was critical of the RBA for inter alia not increasing the money supply (creating new fiscal monies under QE) by purchasing long dated Govt bonds from Treasury in order for the Commonwealth Govt to finance its COVID impacted budget deficit. Six weeks' later, on 4 Nov 2020, the RBA announced that it would purchase $100 billion of Govt bonds by increasing the money supply to fund the bond purchases. "RBA governor Philip Lowe has announced a $100 billion quantitative easing program to lower interest rates across Australia's economy." Two months later on 2 Feb 2021, the RBA announced that it would "...purchase an additional $100 billion of bonds issued by the Australian Government and states and territories when the current bond purchase program is completed in mid April." Prima facie, Paul Keating's critical 24 Sept '20 letter to journalists, and accompanying brazen comments venting his disappointment at the RBA 'not being pro-active', brought on a rapid result, particularly as the RBA had refrained from following the lead of 'central banks' in many Western economies that have resorted to QE.The Writer telephoned Paul Keating's PA, Susan Grusovin, in mid-Oct and explained that he was keen to present evidence to Paul Keating that the RBA should have re-imposed a Cap on Credit Card interest rates (over 25 years ago) to protect Australians with poor Financial Literacy Skills. On 28 Oct 2020 the Writer posted his detailed Letter to Paul Keating dated 28 Oct 2020 (on 2 @ DVD, 2 @ USB and 3 @ A4) hopeful that Paul Keating would similarly trumpet criticism of the RBA for not having re-imposed a maximum interest rate Cap on Credit Cards (as far back as June 1992 when the spread between the Overnight Cash Rate and the average Purchase interest rate exceeded 16%). The powers and obligations bestowed upon the RBA by Parliamentary Acts far exceed the obligations upon the USA and UK 'central banks' to protect vulnerable citizens in banking transactions - refer Section 2B of Extensive Powers bestowed upon the Reserve Bank. The Writer emailed Paul Keating's PA, Susan Grusovin on 29 Oct 20 and on 4 Nov 20 explaining his letter to Paul Keating dated 28 Oct 20 that include several Attached files. Many Credit Card Issuers have engaged in Predatory Advertising charging Usurious Unsecured Personal Loan Interest Rates overtly Targeting Credit Cardholders with Low Financial Literacy Capacity Financially - Uneducated And Vulnerable Australians suffering Extreme Financial And Emotional Distress for over 25 years, whilst 67% of Credit Cardholders, identified by the RBA as Transactors, have enjoyed their Lines of Credit from regularly using their Credit Cards at virtually no cost, even though the RBA has previously written that the User Pays Principle should apply to Credit Card Products. Labyrinth of ‘Concealed Spiders’ exposes 'n ine examples' of Unconscionable Conduct from Predatory Advertising of some Credit Cards.Inaction by APRA and ASIC was attributed to some scandals exposed in the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry. ABCNews Business Editor, Ian Verrender, article (26 Nov 2018) Is it time for corporate watchdog ASIC to be put down? includes "It is this cosy relationship that forms the nub of the problem".Yet far more consequentially, Australia's Principal Regulator of the Payments System has been complicit with Credit Card Issuers that engaged in Predatory Advertising even though the Commonwealth Govt had enacted legislation for the Principal Regulator of the Payments System to act upon Unconscionable Conduct from Predatory Marketing, in particular concealed interest penalties in 9 font Arial dark grey in 98 pages T&Cs, of some Credit Cards. Post the 2018 Royal Commission, "ASIC and APRA, in addition to the Royal Commission recommendations addressed to them specifically, are now working with the Federal Government to assist the development of legislative reform":

In Dec 2011, the Writer chronicled to the RBA (on CDs and A4) that the User Pays Principle did not apply to Credit Cards, and that it should apply to protect Financially Uneducated And Vulnerable Australians Back in 2011, after sharing emails with Ms. Sharon van Etten, Public Relations Officer, Media & Public Relations Office, RBA, the Writer posted his extensive submission (on 3 CDs and A4) to the RBA on 8 Dec 2011 seeking application of the User Pays Principle to Credit Card Products. Section 8 of his submission accords with recommendations within "RBA's Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001. "A movement towards a “user pays” approach to credit card payment services would be consistent with the approach adopted by Australian financial institutions in pricing other payment instruments under their control." Following receipt of the Writer's comprehensive letter to the RBA dated 8 Dec 2011 in 3 identical CDs, the RBA should have then re-imposed a maximum interest rate on all Credit Cards of - 1. 850 basis points circa for Purchases; and 2. 950 basis points circa for Cash Advances,above the RBA official interest rate (Overnight Cash Rate) as the Writer's comprehensive letter implored. But it should have re-imposed a maximum interest rate almost 19 years earlier when the spread between the Overnight Cash Rate and the Standard Purchase Interest Rate exceeded 16% - back in June 1992. The Writer emailed Ms. Sharon van Etten that he had posted those CDs and A4 hardcopies (and two updated versions - 9 CDs in toto). He received no response to his letter on 9 CDs dated 8 Dec 2011. The central issue: Prior to the Campbell Report circa early 1980's, Australia's 'central bank' regulated all Australian bank interest rates with an Iron Fist dating back to the failure of banks in the 19th century - "... when de-regulation resulted in adverse consequences, re-regulation ensued...". "CHOICE is concerned that low income earners are disproportionately affected by the costs of credit cards. Persistent Revolvers are overwhelmingly from low income households.18 Interest payments made by these consumers help subsidise the rewards programs offered to Transactors, who tend to be wealthier and attracted to high-interest cards that offer redeemable points as prizes for frequent usage". In April 1985 the RBA removed an 18% interest rate Cap on Credit Cards when the Overnight Cash Rate was 17.2% circa - spread was less than 1%. The spread between the current Overnight Cash Rate of 0.10% and the highest Cash Advance interest rate (Latitude Financial's Go Mastercard) is now over 28% (25.9% + 3% - 0.10%) = 28.8%. Persistent Revolvers that account for a mere 12.58% circa of Credit Cardholders contributed a whopping 80% circa of that $6.3 billion Interest And Penalty Fees Revenue due ostensibly to Credit Card Issuers not passing on falls in the Overnight Cash Rate. The remaining 20% of that $6.3 billion was paid by other Revolvers that account for 20.42% circa of all Credit Cardholders. The remaining 67% circa of all Credit Cardholders, described by the RBA as Transactors, contributed zilch of that $6.3 billion of Interest And Penalty Fees Revenue. Hardly, an example of the User Pays Principle that "RBA's Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001 advocated it apply to Credit Card Products "....consistent with the approach adopted by Australian financial institutions in pricing other payment instruments under their control." But its Board never adopted its own published policy document.

Question: Thirty-Two Questions Directed at Three Financial Services Regulators, or a Royal Commissioner, and Supporting Evidence that warrant each question being asked in a Second Wave of the Royal Commission into Financial Services: The Writer's Letter to Paul Keating also provided - A) Thirty-Two Questions Directed at Three Financial Services Regulators, or a Royal Commissioner, and Supporting Evidence that warrant each question being asked in a Second Wave of the Royal Commission into Financial Services; and B) an Evidence Facts Sheet that further supports each of the Thirty-Two Questions. Yours sincerely Philip J. Johnston ==================================

|

|

|

|

{kind=link}