|

|

1305, 12 Glen St -

The Pavilion on the Harbour' scribepj@bigpond.com 0434 715.861

Insert

one of the enclosed DVDs in a Windows PC

to auto-open at this

SubmissionToRoyalCommission_18-Apr-18.htm

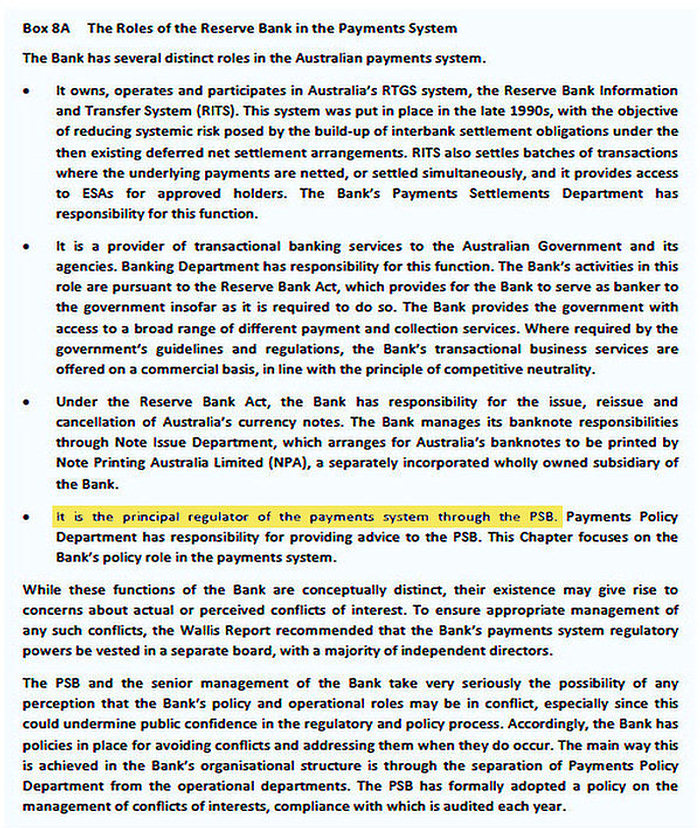

13 November 2018 Mr. (03) 8623 9900Crikey Level 6, 22 William St, Melbourne Vic. 3000 Dear Bernard I have prepared Thirty Two Written Questions (and the Supporting Documented Evidence) for the Royal Commissioner regarding breach of Statutory Duty, ostensibly by the Reserve Bank of Australia (Principal Regulator of the Payments System) and minimally by APRA or ASIC in NOT Setting New Standards for Credit Card Products: * 14 Questions to ask the Governor of the Reserve Bank of Australia - RBA's Submission to the Financial System Inquiry - March 2014 declared it to be the Principal Regulator of the Payments System through the PSB in Box 8A: The Roles of the Reserve Bank in the Payments System* 2 Questions to ask the Chair of APRA * 1 Question to ask the Chair of ASIC * 2 Questions to ask the Chair of the Council of Financial Regulators

* 2 Questions to ask

Chair of the ACCC * 10 Questions that ask the Royal Commissioner to implement material changes re Credit Card Products 32 I wish to publish my Thirty Two Written Questions (and the Supporting Documented Evidence) on a website (after each Question has been peer reviewed). I would then email Financial Services Reformists and other Interested Entities seeking them to review my Thirty Two Written Questions in the hope that the Royal Commission would be encouraged to rely upon them Could you provide to me contact details of one or two economic/legislative academics, or others, that are fervent that the Royal Commission ensures that Two Of Australia's Three Financial Services Regulators rely upon their existing regulatory powers to regulate that Credit Card Issuers desist inter alia Predatory Marketing by Numeracy And Literacy Targeting of Financially Uneducated And Vulnerable Australians? Such targeted Credit Cardholders possess only level 1 (or below) and level 2 Financial Literacy Capacity and are vulnerable to becoming a Revolver (61.87% circa are Occasional Revolvers and 38.13% circa are Persistent Revolvers) that often pay Usurious Unsecured Interest Rates which is contrary to the RBA's parliamentary decreed role to ensure "...the economic prosperity and welfare of (all) the people of Australia" Should you provide me the contact details of one or two academic economists/legislators that peer reviewed my Thirty Two Written Questions and gave it the Thumbs Up, if you were interested I would provide a written commitment to you to have first rights to write an article/s in Crikey, on any of them that you wanted to. I would also provide a written undertaking to acknowledge the input of any economic/legislative academic/s who reviewed my Thirty Two Written Questions and vitally the Supporting Documented Evidence. Such acknowledgement of any peer reviewer's would appear immediately under my final Written Question on the website ------------------------------------------------------------------------------------------------------------------------------------------

I worked for CBA for 37 years, retiring in 2007. I evidenced a lot of change in CBA and across the banking sector - some good and some bad. I hold a Master Degree in Applied Finance from Macq University. I write to you because of your article ' The real story behind the credit card debt headlines' 5 July 2018 (with Glenn Dyer) which reported on 18-201MR ASIC’s review of credit cards reveals more than one in six consumers struggling with credit card debt that noted inter alia:

If you click on my Defined Terms and Documents file re Credit Card Products you will glean -

· 330 circa Documents that I have read and summarised in htm files all accessible through embedded threads; and · 230 circa Defined Terms that I have created to establish certainty of mindset, that I have created since 2011 when in that December I posted a comprehensive submission (on CD) to the RBA which implored it to Set New Standards to apply the User Pays Principle for Credit Cards issued in Australia.

After a few emails and a 'phone chat

with

Ms. Sharon

van Etten,

Public Relations Officer, Media & Public Relations Office, Reserve Bank of

Australia in late Nov 2011,

the

Writer

posted on

CD his detailed Submission dated 8 Dec 2011 to the Reserve Bank that

beseeched the RBA to rely upon its existing

Extensive Powers to

Determine and Set New Standards, relying on

Section 18, that would require

Credit Card Issuers in Australia to apply the

User Pays Principle -

listed A) to H) in his Section 8 - because - I am pleased with the performance of the Royal Commission into misconduct in the Banking, Superannuation and Financial Services Industry. However, Terms of Reference to a Public Submission pursuant to the Royal Commissions Act 1902 (Cth) and clauses (g), (h) and (j) of the Terms of Reference are limited to submissions from wronged customers that describe their grievance/s. I haven't been wronged. I hold two credit cards. I have not paid a cracker in fees or interest in well over 20 years. Alas, with regard to holding Australia's Three Financial Services Regulators to account, in particular Australia's Principal Regulator of the Payments System, regarding Unconscionable Conduct by some Credit Card Issuers, those narrow Terms of Reference are not recognising and rectifying 'regulator bias' which has, in particular, plagued the RBA to the detriment of Persistent Revolvers for over 20 years; most of whom possess low Financial Literacy Capacity with many experiencing Extreme Financial And Emotional Distress. As further evidence of my research of Credit Card Products, (a) I posted my 1st Submission Letter to Maurice Blackburn on 8 May 2017 and my 2nd Submission Letter to Maurice Blackburn on 25 June 2017 (on DVD) asking it to run a Class Action representing 400,000 circa Eligible Persistent Revolver Plaintiffs against the Reserve Bank of Australia for breach of its Statutory Duty and Fiduciary Duty. My Labyrinth of ‘Concealed Spiders' provided nine examples of Unconscionable Conduct by Credit Card Issuers of Predatory Advertising their various Credit Card Products to extricate maximum Interest and Penalty Fees Revenue from Financially Uneducated Credit Cardholders which constitutes Numeracy And Literacy Targeting - My allegations are also acknowledged in Quotes from reputable Credit Card Distress Authorities about unconscionable advertising of some Credit Cards by some Credit Card Issuers resulting in some indebted Credit Cardholders being issued multiple Credit Cards.

(b) I emailed my Public Submission: Sent 22 April 18 to the Royal Commission which included 30 Written Questions for the Royal Commissioner to consider asking to either: · Governor of the RBA · Chairman of APRA · Chair of ASIC · Chair of the Council of Financial Regulators · Chair of the ACCC. Unfortunately the Terms of Reference for the Royal Commission into misconduct in the Banking, Superannuation and Financial Services Industry are limited to wronged customers describing their grievances. As acknowledged further above, I do not fall within those narrower eligibility Terms of Reference. (c) The UK Guardian article 'The interest-free credit card trap snaring unwitting borrowers' is rife with examples of UK Credit Card Issuers' Predatory Marketing directed at Financially Uneducated And Vulnerable Credit Cardholders that Lack Financial Acumen. There is a welter of evidence that U.S. Credit Card Issuers are not immune from similar Unconscionable Credit Card Advertising.

References to this Letter: A. Three Pivotal 'Landmark' RBA Published Papers in the last 26 years B. The Writer's CD submission to RBA sent 8 Dec 2011 that implored the RBA to regulate introduction of the User Pays Principle to Credit Card Products C. 1st Submission Letter to Maurice Blackburn on 8 May 2017 and my 2nd Submission Letter to Maurice Blackburn on 25 June 2017 (on DVD) asking it to run a Class Action representing 400,000 circa Eligible Persistent Revolver Plaintiffs against the Reserve Bank of Australia for breach of its Statutory Duty and Fiduciary Duty D. Maurice Blackburn’s response letter to me dated 14 July 2017 E. Over 550 Documents and Defined Terms Parliamentary Acts, MoU's and RBA Credit Cards Regulatory Decisions relied upon in this Letter * Banking Act 1959 - Banking Act 1959 (222 pgs) * Reserve Bank Act 1959 - Reserve Bank Act 1959 (57 pgs) * Payment Systems (Regulation) Act 1998 - Payment Systems Board Act 1998 (33 pages) * APRA Act 1998 - APRA Act 1998 (72 pgs) * Australian Securities and Investments Commission Act 2001 (394 pgs) * Competition and Consumer Act 2010 (544 pgs) * Memorandum of Understanding - Australian Competition and Consumer Commission and Reserve Bank of Australia dated 8 Sept 1998 * Memorandum of Understanding - Australian Prudential Regulation Authority and Reserve Bank of Australia dated 12 October 1998 * Memorandum of Understanding - Australian Prudential Regulation Authority and Australian Competition and Consumer Commission dated 30 November 1999 * Credit Cards Regulatory Decisions by the RBA Primary Sections of Acts relied upon: · Section 50 ‘Control of interest rates’ of the Banking Act 1959 · Section 10(2) 'Functions of Reserve Bank Board' of Reserve Bank Act 1959 · Division 2—Section 11 of the Payment Systems (Regulation) Act 1998 · Division 3—Section 12 of the Payment Systems (Regulation) Act 1998 · Division 4---Section 18 of the Payments System (Regulation) Act 1998 Yours sincerely Phil Johnston aka Bank Teller |

|

|

|

{kind=link}