Annexure - Q & A

Question 1.

How can Credit Card Issuers provide the majority of Credit Cardholders, referred to as Transactors, with 'up to 55 days' Line Of Credit for a mode $10,000 Card Limit at no interest cost and in most instances only a small Credit Card Annual Cardholder Fee of say $65?

Answer 1.

A minority of Credit Cardholders, referred to above as Revolvers, pay Usurious Unsecured Personal Loan Interest Rates On Their Credit Cards which is an average of 7% above the market rate for an Unsecured Personal Loan which is principally contributed by Financially Uneducated And Vulnerable Australians.

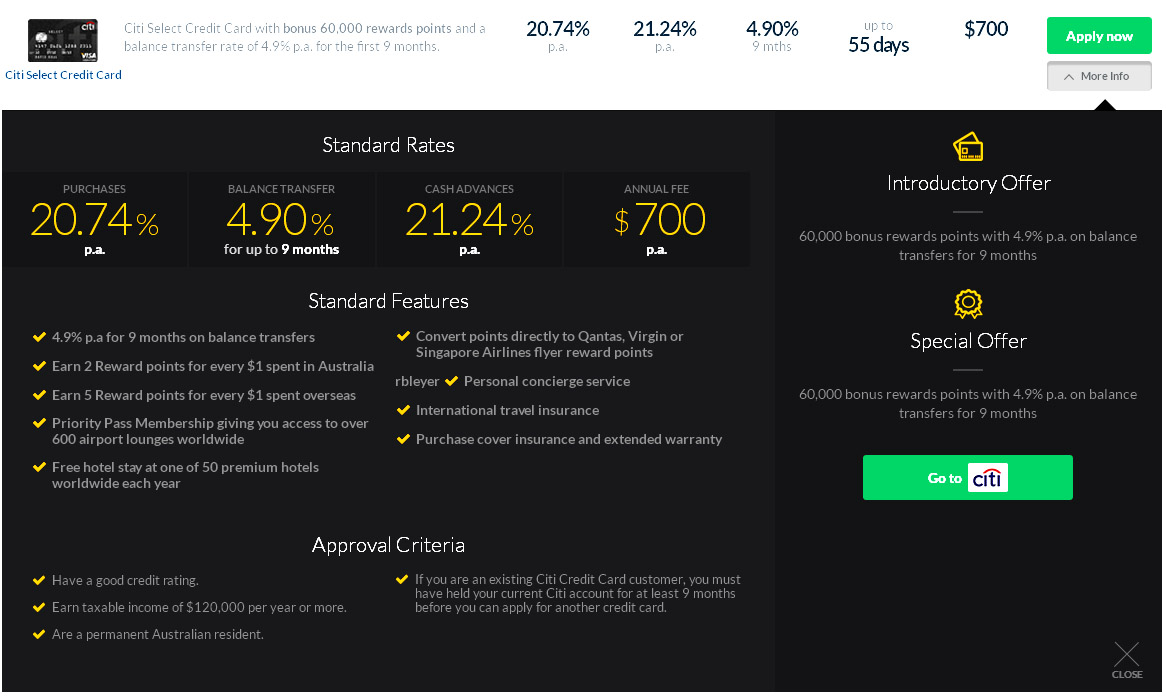

Question 2.

How can a Credit Card Issuer, offer a Credit Card Product, namely Citi Select Credit Card -

{kind=link}

*

grant 60,000 reward points worth between $600 and $800 (depending on method of

using them);

* provide

up to 55 days'

Line Of

Credit;

and

* charge an annual fee of $700?

Answer 2.

Because Credit Cardholders of Credit Cards such as the 'Citi Select Credit Card' treat their an annual fee of $700 as a 'company tax write-off', and the $600 to $800 in flight tickets, luxury items or cash that they receive annually as 'tax free income'.

If Rewards Programmes 'Reward Points' are converted to flight tickets, luxury items or cash and the Credit Cardholder of the 'Citi Select Credit Card' (or comparable) is

(a) an employee and the Credit Card is provided by the employer, then the ATO should deem such receipts as a fringe benefit; and

(b) NOT an employee, then the ATO can deem such receipts as taxable income in the same manner that the ATO deems bank interests receipts as taxable income.

Question 3.

How did a Credit Card Product, namely Westpac's Low Rate Visa Credit Card offer a 14 months Balance Transfer Interest-Free Period at 0% interest with a Cash Advance interest rate of 21.49% and an annual fee of only $45.

Answer 3.

Predatory Marketing explains that Balance Transfer Interest-Free Period Offers -

(i) target Financially Uneducated And Vulnerable Australians that are already burdened by high monthly interest costs on large Outstanding Indebtedness, and probably incurring Late Payment Fees and Over-the-Limit Fees, that assertedly does not charge interest on the 'Balance Transfer Amount' for somewhere between 6 months and 24 months; and

(ii) identify that Balance Transfer Interest-Free Period Offers were exceedingly profitable until 1 July 2012 because an 'Order of Payments' Allocation Practice for every Credit Card contract specifies which balance(s) from a 'payment' will be applied to first. Hence, prior to 1 July 2012 in nearly all Balance Transfer Interest-Free Cards, payments were applied to lowest interest rate balances first - highest interest rate last. Whereupon the holder of a new credit card, that had a Balance Transfer Amount, was paying interest on all Purchases from the date of each Purchase due to forfeiting the Interest Free Period. Post 1 July 2012, Balance Transfer Interest-Free Period Offers do not provide an Interest Free Period, so the metre is running at 20% interest approx. from the date of each Purchase. If it is a Citi Rewards Credit Card, a $10 Late Payment Fees is levied every 7 days if the Minimum Payment is not made by the Payment Due Date. At the expiry of the Balance Transfer Interest-Free Period any residue of the Balance Transfer Amount is charged at the Cash Advance interest rate of 21.74% p.a.

Question 4.

Why do a minority of Credit Cardholders pay Usurious Interest Rates and which provides 75% circa of Revenue to Credit Card Issuers as explained in Chapter 8?

Answer 4.

Because -

(A) this minority of Credit Cardholders are Financially Uneducated And Vulnerable Australians who, through no fault of their own, possess low Financial Literacy Skills (ie. possess level 1 and level 2 numeracy and literacy skills as identified by the Productivity Commission) and the advertising of many Credit Card Products involve a Labyrinth of ‘Concealed Spiders’; and

(B) Australia's Principal Regulator of the Payments System, the RBA, has breached its Fiduciary Duty and its Statutory Duty by abrogating its Parliamentary Bestowed Mandate to -

(i) ensure "...the economic prosperity and welfare of (all of) the people of Australia"; and

(ii) not merely ensure "...the economic prosperity and welfare of..." the Financially Educated which would usually include employees of the RBA.

Question 5.

Does the current interest and fees structure for Credit Card Products apply the User Pays Principle (as sought by the Reserve Bank in RBA's Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001) where all Credit Cardholders who benefit from Credit Card Products contribute towards its costs?

Answer 5.

No. The majority of Credit Cardholders make no meaningful contribution to the profits of Credit Card Issuers because there is no 'Transaction Fee' based on the frequency of Purchases and the aggregate of Purchases.

Question 6.

Does the current interest and fees structure for Credit Card Products discriminate against Financially Uneducated And Vulnerable Australians that only possess level 1 and level 2 numeracy and literacy skills?

Answer 6.

Yes. But after liaising with a lady at Australian Human Rights Commission regarding Australia's anti-discrimination laws, none of the existing anti-discrimination acts specifically cover commercial enterprises targeting Australians with poor numeracy and literacy skills in the manner many Credit Card Issuers do with advertising that employs a Labyrinth of ‘Concealed Spiders’, although the Disability Discrimination Act 1992 would be the closest.

Question 7.

Does the RBA possess extensive powers over Credit Card Issuers to regulate interest rates and gather information on Credit Cards?

Answer 7.

Yes.

- 'designate' a particular payment system as being subject to its regulation. Designation has no other effect; it is simply the first of a number of steps the Bank must take to exercise its powers - ("Designation is the first step in establishing standards and access regimes for a payment system to deal with public interest issues.") - "Designation of a payment system occurs only after substantial consultation

with participants and after voluntary arrangements have been exhausted.";- determine rules for participation in that system, including rules on access for new participants. Since access is inextricably linked to efficiency the Bank works closely with the Australian Competition and Consumer Commission (ACCC) (see below);

- set standards for safety and efficiency for that system. These may deal with issues such as technical requirements, procedures, performance benchmarks and pricing;

- direct participants in a designated payment system to comply with a standard or access regime; and

- arbitrate on disputes in that system over matters relating to access, financial safety, competitiveness and systemic risk, if the parties concerned wish.

Question 8.

Are there any databases of Financially Uneducated And Vulnerable Credit Cardholders that have paid Material Interest And Fees at a Comparison Rate Over 20% Per Annum?

Answer 8.

The RBA has released financial 'Bulletins' each quarter on a plethora of topics since 1985.

The RBA has conducted a survey on bank fees each year since 1997, usually published amongst its June Qtr Bulletins.'Banking Fees in Australia' - 'Bulletin' – June Quarter 2014 notes in "Table 2: Banks' Fee Income from Households" $1,363,000,000 in Credit Cards Interest And Fees Revenue for 12 months to 30 June 2113 .

Notwithstanding that Numeracy And Literacy Targeting is a Statutory Duty pursuant to the RBA's Role, the RBA refuses to request Credit Card Issuers to provide data which identifies whether Interest And Fees Revenue are spread evenly across all Credit Card Users. Or alternatively gather data across the level 1 to level 5

Financial Literacy cohorts (recognised by Australia's various Numeracy And Literacy Authorities) to identify whom is paying the weight of Interest And Fees Revenue to Credit Card Issuers. The Writer, and his friends, use Credit Cards extensively and enjoy up to 42 days Line Of Credit, but do not contribute to the annual revenue of $1,363,000,000 to 30 June 2113.Australian Governments allocate $43 million annually to 44 Australian charities to provide financial counselling to Australians. In identifying a vehicle to source 'plaintiffs' and 'Credit Card Distress' Authorities, thousands of Financially Uneducated And Vulnerable Australians can readily be contacted by these 44 Australian charities that fund "....financial counsellors who provide free, confidential advice for people who are struggling to pay their bills."

SMH article Middle class hit by debt - Huge mortgage repayments and credit cards bills are taking their toll snapshots the problem that non-conflicted ‘Not-For-Profits’ (Salvation Army's Moneycare service, Centacare, Anglicare, Lifeline, Wesley Mission's Credit Line, Smith Family, St Vincent de Paul's Budget and Financial Counselling Service, Centacare ‘et al’) deal with the damage when families become hopelessly credit cards indebted.