|

|

Letter to Adele Ferguson 5 Oct 2019 Defined Terms and Documents 1. Pertinent events since mid-2010 by the Writer re Credit Card Products: (a) Has undertaken well over a thousand hours gathering evidence of Unconscionable Conduct by some Credit Card Issuers of Credit Card Products that have mislead and deceived using Predatory Advertising, charging Usurious Interest Rates Targeted At Credit Cardholders With Low Financial Literacy Capacity - evident in the embedded URL threads in his 570 circa Defined Terms and Documents, in particular Labyrinth of ‘Concealed Spiders’. (b) Posted on CDs to the Reserve Bank his Submission dated 8 Dec 2011 that beseeched the RBA to rely upon its Extensive Powers to require Credit Card Issuers in Australia to adopt the User Pays Principle because Transactors enjoy their Lines of Credit at virtually no cost and Persistent Revolvers that regularly possess poor Financial Literacy Skills and account for only 12.58% circa of Credit Cardholders contribute a whopping 80% circa of all Interest And Penalty Fees Revenue generated from Credit Card Products. Section 8 of his submission to the RBA accords with recommendations within "RBA's Reform of Credit Card Schemes in Aust: "A Consultation Document" – Dec 2001 in particular "A movement towards a “user pays” approach to credit card payment services would be consistent with the approach adopted by Australian financial institutions in pricing other payment instruments under their control."(c) Posted a Submission to Maurice Blackburn on 25 June 2017 (on DVD) asking it to run a Class Action representing 400,000 circa Eligible Persistent Revolver Plaintiffs against the Reserve Bank for breach of its Statutory Duty and Fiduciary Duty to the material detriment of those Eligible Persistent Revolver Plaintiffs. (d) Maurice Blackburn response letter dated 14 July 2017 included:

(e) Emailed his Public Submission sent 22 April 18 to the Royal Commission which was deemed ineligible because he had not personally suffered a financial loss.

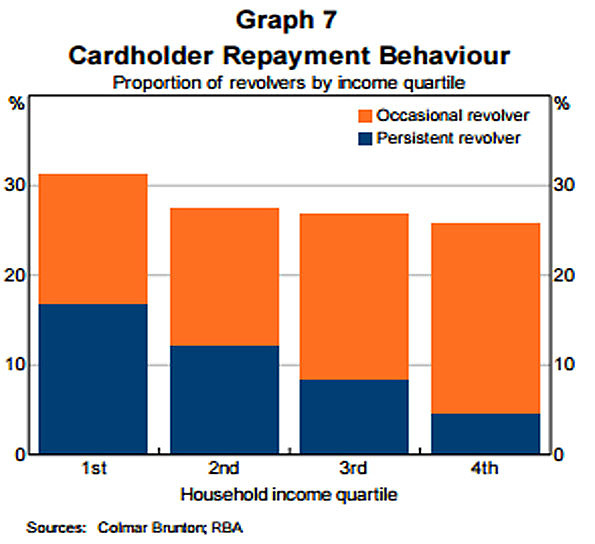

(f) Posted all requisite information to Dr. Peter Brandson, CEO, Bank Reform Now, PO Box 497, Batemans Bay NSW to justify a second wave of the Royal Commission (only two weeks of hearings and cross examination), specifically to address an alleged breach of Statutory Duty by Australia's Principal Regulator of the Payments System that has cost 400,000 circa Credit Cardholders across Australia (first identified as Persistent Revolvers by the Reserve Bank of Australia in its Submission to the Senate Inquiry into Matters Relating to Credit Card Interest Rates - Aug 2015 in Graph 7 titled ''Cardholder Payment Behaviour") because 400,000 circa Credit Cardholders -

|

|

|

|

{kind=link}