Equitability Cost Contribution Scheme or Equitable User Pays Cost Contribution Scheme means under the Proposed User Pays Fee Structure that accords with the User Pays Principle all Credit Cardholders pay a small Purchaser User Pays Fee towards the cost of items 2. and 3. of Three Purchase Benefits Of 'Tap And Go because -

i) the Average debit balance per Credit Card was $2,923 as at 8 Nov '22 - up to 55 days Interest Free Period; and

ii) the average interest cost of a $3,000 personal loan (overdraft) is between 6.75% and 23.84%.

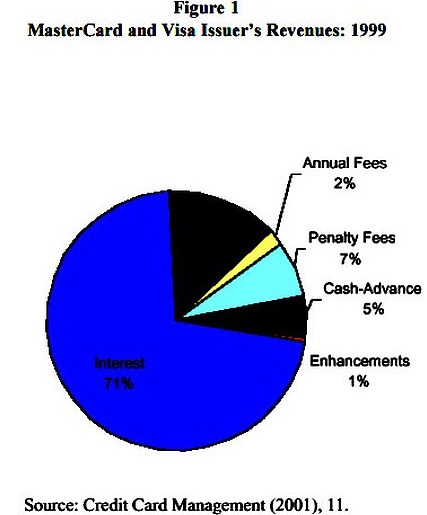

The below extract from RBA's Consultation Document titled Executive Summary - Reform of Credit Card Schemes in Australia: RBA's "A Consultation Document" – Dec 2001

notes -* under point 6 of '

Introduction' that some Credit Cardholders enjoy the convenience of their Revolving Line/s of Credit without materially contributing to Credit Card Issuers' operating costs:"Within the latter group, there is a third group which directly contributes very little to the costs of credit card schemes – these are the cardholders (known as Transactors) who settle their credit card account in full each month. Although they normally pay an annual fee, they pay no transactions fees, enjoy the benefit of an interest-free period and in many cases earn loyalty points for each transaction."

* on page 15:

redit cardholders who use the credit card purely as a payment instrument (“transactors”), that is, who pay off their balance by the end of the interest-free period, make only a very small contribution to total issuing revenues, mainly through annual fees.""The other two-thirds of total issuing revenues is generated by cardholders who make use of the revolving line of credit (“revolvers”), that is, who do not pay off their accounts by the end of the interest-free period. Preliminary data from the Reserve Bank’s new payments system collection indicate that about three-quarters of credit card outstandings are interest-bearing. C

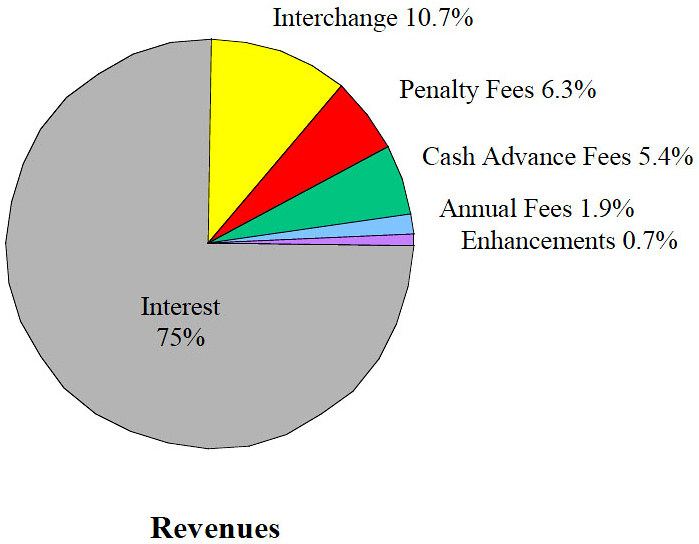

Approx. 67% of Credit Cardholders, those that are Financially Educated with Level 3, 4 or 5 Financial Literacy Capacity (identified as Transactors by the Reserve Bank) make almost no payment for enjoying a Line/s of Credit for between 45 and 55 days (on one or more Credit Card Products) because Annual Credit Cardholder Fees represent a mere 2% of a Credit Card Issuers annual 'Revenues'. The majority of Transactors receive Rewards Programs. Transactors invariably enjoy a Free Ride.

The remaining 33% circa of Credit Cardholders who are Financially Uneducated And Vulnerable Australians, generally with Level 1 and 2 Financial Literacy, as quantified in extensive written reports separately published by the ABS, Productivity Commission and ASIC, pay the operating costs and generate the profits in Interest And Fees Revenue, of Credit Card Issuers. A few Reserve Bank published reports refer to this 33% cohort as Revolvers.

Hence, one third of Credit Cardholders (Revolvers) pay the cost of the other two thirds of Credit Cardholders that enjoy a Line/s of Credit for an average of $2,923 (per Credit Card as at Sept '22) for between 45 days and 55 days before those "two thirds" physically pay for their Purchases. Revolvers also pay the $18 billion dollars annually of interest (Aug '22) as well as Late Payment Penalty Fees.

Enjoying a Line/s Of Credit by paying for goods and services for between 45 and 55 days, rather than visiting an ATM to draw cash and then carry cash the way we all did 20 or more years ago is a material convenience and security benefit. Paying Tap and Go with a Credit Card is a highly sought after and convenient payment method for many millions of Australians. Yet one third of Credit Cardholders (Revolvers) presently pay the provisioning costs of the other two thirds of Credit Cardholders (Transactors).

The Writer believes that Revolvers (33% circa of Credit Cardholders that possess only Level 1 or Level 2 Financial Literacy) (separately measured by ABS, Productivity Commission and ASIC published reports) would not pay the provisioning costs of Transactors (67% circa of Credit Cardholders that possess Level 3, 4 and 5 Financial Literacy) Line/s Of Credit if the Australia's Principal Regulator of the Payments System observed/applied its Parliamentary Bestowed Mandate to regulate the User Pays Principle to Credit Card Products so that Transactors paid for the aforementioned benefits they readily/frequently enjoy.

Sadly in April 1985 amidst exceptionally high interest rates, Australia's Principal Regulator of the Payments System 'tossed in the towel' by Deregulating Credit Cards and removing the 18% Cap on Credit Card rates interest rates the RBA had regulated with an Iron Fist from the late 1970s. It would have been better to merely raise that 18% regulatory Cap to 24% or thereabouts, and lower it as the RBA pruned in inflation and associated interest rates. Australia's burgeoning NBFIs was beyond the RBA's capabilities notwithstanding its Parliamentary decreed regulatory obligations. "The first response was to set in train a process whereby interest rate ceilings would be extended to cover all non-bank financial institutions. An Act of Parliament was passed – the Financial Corporations Act of 1974 – to do this, but Part 4 of the Act was not proclaimed and therefore the powers to extend controls never came into effect."